Since Satoshi Nakamoto pointed out that traditional transaction systems are way behind and does not sync well with the information age in 2009, blockchain solutions started gaining momentum. They operate with a commonly shared consensus among network users. What makes the public network better? Well, transparency! If you were searching for “how to make a public blockchain platform?”, the blog has everything for you.

Understanding Public Blockchains

Public blockchains are open networks that permit participation from anyone. They operate on a permissionless basis, allowing any individual to join the network, read, write, or engage with the blockchain. These blockchains are characterized by decentralization, lacking a singular controlling entity. They can function as the underlying infrastructure for various decentralized solutions. The security of a public blockchain is strengthened by a substantial number of participants, providing protection against data breaches, hacking attempts, and other cybersecurity threats.

The consensus mechanisms employed by most public blockchains involve either proof-of-work or proof-of-stake systems. In a proof-of-work system, the initial node or participant validating a new data addition or transaction on the digital ledger is rewarded with a specific number of tokens.

This adoption extends beyond statistics, with 2.8% of the world’s population already engaged in blockchain, signifying a paradigm shift in societal norms. Public blockchains, thus, not only serve as technological pillars but also as agents of a digital transformation, reshaping our collective future.

Importance In Decentralized Systems

The importance of public blockchains in decentralized systems lies in their ability to establish trust and transparency without reliance on a central authority. Public blockchains facilitate peer-to-peer transactions and data sharing, reducing the need for intermediaries. This decentralization enhances security by eliminating single points of failure, making the system more resilient to attacks. Furthermore, public blockchains empower a diverse network of participants to validate transactions, ensuring a democratic and inclusive environment. Their open nature fosters innovation and inclusivity, enabling anyone to participate and contribute to the development of decentralized applications, ultimately reshaping traditional paradigms of trust and governance in various industries.

Understanding Blockchain Protocol

A blockchain protocol emerges as an important framework dictating the complexity of a blockchain network’s functionality. These protocols establish standardized rules governing key aspects of the network, encompassing transaction handling, node interactions, ledger data synchronization, validation rewards, and the Application Programming Interface (API).

Types Of Blockchain Protocol

Blockchain protocols encompass various types, each defining the rules governing their respective networks. Proof of Work (PoW), notable in Bitcoin, relies on computational puzzles for consensus. Proof of Stake (PoS), favored by Ethereum’s future updates, selects validators based on their stake in the network. Delegated Proof of Stake (DPoS) streamlines consensus with a select group of delegates validating transactions. Practical Byzantine Fault Tolerance (PBFT) emphasizes efficiency and is common in permissioned blockchains. Directed Acyclic Graphs (DAGs), as seen in IOTA’s Tangle, eliminate traditional blocks, enabling parallel transactions. Hashgraph employs a patented consensus algorithm using gossip protocol and virtual voting. Hybrid approaches combine elements from different protocols to optimize efficiency, security, and scalability.

Each protocol caters to specific needs, with newer entrants exploring hybrid approaches, emphasizing efficiency, security, and scalability in diverse blockchain ecosystems.

Generally, developing a blockchain protocol includes the following:

- Transactions handling and validation procedure

- Block producers

- Interaction between nodes

- Synchronization of ledger data and data broadcasting

- Validation rewards for the users (if any), and lastly,

- The application programming interface.

The prevailing blockchain protocols can be broadly segregated into #3 layers:

Layers Of Blockchain Protocol

Layer 1 Protocols: The Foundation of Blockchain Infrastructure

At the base Layer 1, essential blockchain operations take place. This layer manages core processes such as transaction processing and finalization. Examples like Proof of Work (PoW) in Bitcoin and Proof of Stake (PoS) in Ethereum showcase the diversity of Layer 1 protocols.

Layer 2 Protocols: Boosting Speed and Scalability

Building on Layer 1, Layer 2 protocols enhance capabilities, particularly in terms of speed and scalability. These protocols handle transactions off the main blockchain (Layer 1), reducing transaction costs and increasing throughput. An example like Polygon (MATIC) addresses challenges such as slow transaction speeds and high gas fees on the Ethereum network.

Layer 3 Protocols: Empowering the Application Layer

Zooming into the application layer, Layer 3 protocols house decentralized applications (dApps) and protocols, empowering users to engage in various activities. These protocols focus on overcoming application and execution bottlenecks, with decentralized applications often acting as Layer 3 protocols. Notable examples include Uniswap, a decentralized exchange, and the NBA Top Shot NFT marketplace.

Key Consideration For Choosing The Right Protocol For Your Platform

When it comes to choosing the most suitable blockchain protocol for your platform, a thorough evaluation of several key considerations is paramount:

1. Scalability and Throughput

The chosen protocol must seamlessly handle a substantial volume of transactions per second without compromising performance. This is particularly vital for platforms that anticipate high transaction loads.

2. Security and Consensus Mechanism

Robust security measures should be a non-negotiable aspect of the selected protocol. Additionally, careful scrutiny of the consensus mechanism, the method by which network agreement is achieved, is imperative for ensuring the integrity of the platform.

3. Smart Contract Functionality and Flexibility

If your platform relies on smart contracts, it’s essential that the chosen protocol not only supports them but also offers flexibility in their implementation. This ensures that your specific smart contract requirements can be seamlessly accommodated.

4. Interoperability and Integration

The selected protocol should possess the capability to interact with other blockchains and systems. This becomes crucial when your platform necessitates data or asset exchange with other blockchain networks.

5. Community and Ecosystem Support

A thriving community and ecosystem can be invaluable for garnering resources and support for your platform. Considering the strength and vibrancy of the community associated with a particular protocol is a strategic move.

6. Transaction Speed

For certain applications, the speed at which transactions are processed can be a decisive factor. Assessing the transaction speed offered by a protocol is essential for meeting the real-time demands of specific use cases.

7. Cost

The overall cost implications of utilizing the blockchain must be carefully weighed, encompassing transaction fees and the expenses associated with implementing and maintaining the system. This comprehensive cost assessment is integral to ensuring the financial viability of your platform.

How To Develop A Public Blockchain Platform?

Here is a step-by-step process of development curated for you.

Step 1: Identification Of A Suitable Use-case

To begin with, you must identify a solid use case for the platform that makes sound business sense. It has a plethora of use cases in data authentication, smart contracts, IoT, money transfer, logistics, etc.

- Thanks to the billions of connected devices, it is becoming easier for hackers to breach your data through a single connected device. Integration of blockchain technology with IoT devices can prevent that.

- Smart contracts eliminate the middlemen and introduce accountability for all involved parties, which is impossible in traditional agreements.

- Developing a blockchain solution also facilitates lightning-fast transactions and is already transforming the BFSI sector. It eliminates transaction fees levied by traditional financial institutions.

- Data siloing, miscommunication, and transparency continue to plague the logistics industry. Blockchain solutions can recognize logistics data sources & automate processes, boosting speed, efficiency, and transparency.

There are plenty of other use cases like the metaverse through integration with VR software development and NFTs. The use case of the blockchain should be the guiding force behind all the forthcoming steps.

Step 2: Identification Of The Best Consensus Mechanism

While Bitcoin utilizes the Proof of Work consensus mechanism, there is a wide range of consensus mechanisms today. Examples include Proof of Stake, Byzantine fault-tolerant consensus, Proof of Elapsed Time, Federated consensus, Derived PBFT, and much more. Choose the consensus mechanism that appropriately complements the use case for the public blockchain you want to develop.

Step 3: Creating The Blockchain Protocol

While setting up the blockchain protocol, you must have a clear idea of the following:

- Account Model- What are the requisites of the account model when you are designing a blockchain protocol? Is the account balance-based or UTXO-based? It would also help if you also brainstormed the rules to generate your account name and account type. Ellipse algorithms such as Curve 25519 can be deployed.

- Encryption Algorithm- You must pick the best encryption model for the protocol. Currently, asymmetric encryption algorithms are trending!

- Data Architecture- The data architecture forms the backbone of the protocol. It encapsulates block data structure, account data structure, node data structure, and transaction data structure. Each block demands a block header, and you can design it to suit the project requirements. An interoperable design can blend the consensus mechanism of the blockchain with data storage.

Also Read: Top 13 programming Languages For Blockchain App Development (2022)

Step 4: Data Structure & Storage

The block data structure, account data structure, node data structure, and transaction data structure are all examples of data structures.

If you are working with a relational database system, this will primarily include the database tables you create.

Based on the requirements, you can opt for a data-storing mechanism. It is possible to decouple data storage from a sufficiently independent location. You can implement an interoperable design for a blockchain’s consensus mechanism & data storage with an API.

Dealing With The Byzantine Nodes

As discussed above, developers code the seed of a node. The problem arises when some of these nodes fail to act as per the coding guidelines.

A few nodes may turn on just once and fail to do it again. Or they might return the wrong data. While coding has a lot to do to deal with these issues in the first place, blockchains should nevertheless have an inherent mechanism in place as a countermeasure.

While defining the node database table, a field marks the kind of node it is. If it’s a Byzantine node, it should be punished. The general approach is to place that node under a blacklist. However, it should not be a permanent measure, and a release mechanism must be present to reinstate them at a later stage if they are found to be good.

For example, a bad network, an offline node, or lost data (during the transmission process) can all trigger the Byzantine protocol. Under such circumstances, these nodes won’t permanently lose access to a sound design.

Thus, to ensure fairness, a release mechanism is vital. While rechecking the node, if it still performs unreasonably, the length of its blacklist time can be increased.

Step 5: Designing The Node Communication Protocol

Here, the seed of blockchain nodes are designed. Blockchain solutions can be diverse. It can be private (for example, implementation agreement management system in a defense company), public (for instance, an asset-backed cryptocurrency), or hybrid (for example, a group of financial institutions operating a common KYC platform).

Node communication means that you can access the nodes, providing you feedback. One can utilize Socket, HTTP, or GRPC to compute. However, GRPC offers a slight efficiency advantage over HTTP.

You can also decide whether the nodes execute on-premise, cloud, or both. The hardware configuration comes next, where you can opt for the processors, memory, disk size, etc. Additionally, you can choose operating systems like Ubuntu, CentOS, Windows, Debian, etc.

Step 6: Designing the Blockchain Instance

Designing a blockchain instance requires careful planning and configuration of various elements. These elements form the backbone of the blockchain’s structure and functionality. Here are some key components:

- Parameters: These are the variables that define the behavior of the blockchain. They include block size, block time, consensus mechanism, and more.

- Asset Issuance: This refers to the creation of new assets on the blockchain, such as tokens in a tokenized system.

- Atomic Exchanges: These are transactions in which multiple parties exchange assets simultaneously, ensuring that if any part of the transaction fails, the entire transaction is rolled back.

- Native Assets: These are the primary assets of the blockchain. For example, Bitcoin is the native asset of the Bitcoin blockchain.

- Asset Re-issuance: This is the process of creating additional units of an asset after its initial issuance.

- Key Management: This involves managing the cryptographic keys that users employ to sign transactions and access their assets.

- Multi-signatures: These are security features that require multiple parties to sign off on a transaction before it can be executed.

- Permissions: These determine who can participate in the network and what actions they can perform.

- Address Formats: These are the formats used for the addresses that identify participants in the network.

- Block Signatures: These are the cryptographic signatures that validate the authenticity of each block.

- Handshaking: This is the process by which nodes in the network establish a connection for communication.

While some parameters can be modified during the operation of the blockchain, others are immutable once the blockchain is launched. Therefore, careful planning and consideration are crucial during the design phase to ensure the blockchain operates as intended.

Also Read: The Best 13 Programming Languages For Blockchain App Development (2022)

Step 7: Integrating The Blockchain APIs

While some blockchains implement pre-built APIs, others don’t. The major categories of APIs that you might require are for these purposes:

- Generating addresses & key pairs,

- Data authentication via hashes and digital signatures,

- Conducting audit-related functions,

- Data storage & retrieval,

- Smart contracts

- Smart-asset lifecycle management including issuance, exchange, payment, escrow, and retirement.

Step 8: Designing the Admin & User Interface, Including Additional Techs

You’ll need to decide on the front-end programming languages now. There are many languages such as CSS, HTML5, C#, PHP, Python, Java, Javascript, Golang, Ruby, Solidity, etc.

You should also pick the servers (including FTP servers, web servers, mail servers) and external databases (for example, MySQL or MongoDB).

Additionally, it would be best if you strive to improve the efficiency of the Blockchain solution by integrating additional techs. These include Artificial Intelligence(AI), Data Analytics, Biometrics, Cloud, Bots, Cognitive Services, Internet of Things, and Machine Learning.

That is pretty much the whole development process of developing a public blockchain. Moving on, let’s take a look at some of the other aspects involved in blockchain development.

Dealing With The Byzantine Nodes

As discussed in Step 4 of the development process, developers code the seed of a node. The problem arises when some of these nodes fail to act as per the coding guidelines.

A few nodes may turn on just once and fail to do it again. Or, they might return the wrong data. While coding has a lot to do to deal with these issues in the first place, the blockchains should nevertheless have an inherent mechanism in place as a countermeasure.

While defining the node database table, a field marks the kind of node it is. If it’s a Byzantine node, it should be punished. The general approach is to place that node under a blacklist. However, it should not be a permanent measure, and a release mechanism must be present to reinstate them at a later stage if they are found to be good.

For instance, a bad network, an offline node, or lost data (during the transmission process) can all trigger the Byzantine protocol. Under such circumstances, these nodes won’t permanently lose access in a sound design.

Thus, to ensure fairness, a release mechanism is vital. While rechecking the node, if it still performs unreasonably, the length of its blacklist time can be increased.

Also Read: Top Cryptocurrency Apps In 2022

Importance Of Smart Contracts In Public Blockchain

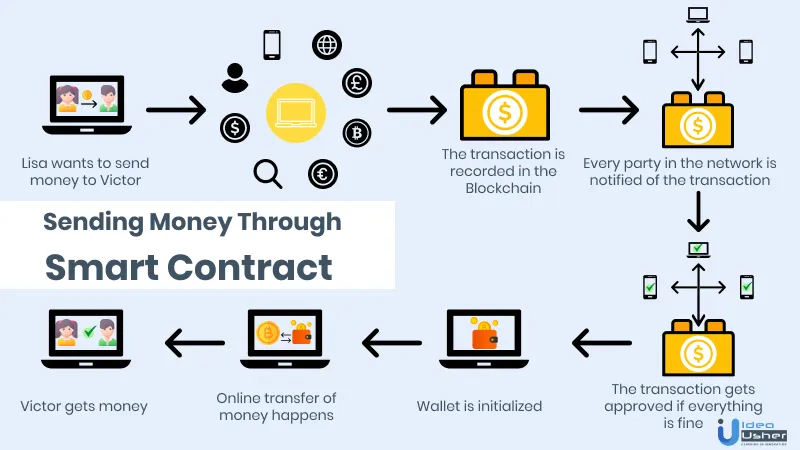

Smart contracts are self-executing agreements where the terms between the buyer and seller are directly coded into lines of code. These contracts, stored on a blockchain, are immutable and cannot be altered. They automatically execute transactions when predetermined conditions are met, eliminating the need for a third-party intermediary.

Contract Execution Through Standard Contracts

An executed contract is a legally binding agreement signed and accepted by all involved parties. This contract establishes a legal relationship, with each party obligated to fulfill the agreed-upon terms.

Smart contracts, which are popularized by Ethereum – the world’s second-largest blockchain platform – have gained widespread use in decentralized applications and other contexts. Standard contracts, like Ethereum’s smart contracts, automate the execution process, ensuring all involved parties have a shared understanding. They offer immediate clarity on the agreement’s outcome without relying on traditional third-party intermediaries. Additionally, they can automate workflows based on predefined conditions.

Here are some examples for you to consider:

Example 1

Consider a situation where a client is paying a freelancer for a job. Instead of depending on a bank (a third party) to approve the fund transfer, the payment process can be automated through a smart contract, provided both the freelancer and the client agree to the terms.

Example 2

Consider a situation where a regulatory body and citizens are debating a law. If both parties agree to a resolution through a blockchain-based process, the law can automatically come into effect through an executed contract.

Therefore, when contemplating the development of a public blockchain network, integrating smart contracts is a critical aspect to consider. They not only streamline processes but also enhance transparency and trust among involved parties.

Overcoming Security Concerns In Public Blockchain

Blockchain, founded on principles like consensus and decentralization, aims to ensure transaction trust. However, the implementation of faulty technology has led to emerging security issues. To improve blockchain security, some strategies are recommended that encompass education, training, and the adoption of industry best practices. Moreover, improving awareness and expertise is pivotal to addressing vulnerabilities and establishing a more secure blockchain network. In safeguarding public blockchains, a straightforward and effective strategy is key. Let’s break it down:

1. Empowering Participants

Educate everyone involved in the blockchain network. By enhancing their understanding of potential risks and how to tackle them, you create a more vigilant and proactive community.

2. Proven Practices

Embrace industry best practices, drawing from established models such as Gartner’s Blockchain Security Model. Integrating these proven practices into the planning and implementation phases can significantly enhance the overall security posture of the blockchain.

3. Robust Access Control

Strengthen security through the implementation of robust authentication methods. By strictly controlling access to authorized individuals, the blockchain network becomes less susceptible to unauthorized intrusions.

4. Encrypted Protection

Employ advanced encryption protocols to safeguard both data and transactions traversing the blockchain. Robust encryption adds an additional layer of protection, ensuring the confidentiality and integrity of the information stored on the network.

5. Regular Software Tune-ups

Stay ahead of potential threats by regularly updating the blockchain software. These updates are crucial for patching known vulnerabilities, maintaining the resilience of the network, and adapting to emerging security challenges.

6. Guard Your Devices

Strengthen the security at the device level by installing reputable antivirus software. This proactive measure helps detect and neutralize potential threats, safeguarding the integrity of interactions between devices and the blockchain.

7. Smart Key Storage

Avoid the risk of unauthorized access by avoiding the storage of blockchain keys as plaintext files. Opt instead for secure key storage solutions, minimizing the vulnerability of sensitive cryptographic keys.

Closing Thoughts!

The network infrastructure of a public blockchain is entirely decentralized. All nodes in such a system will have their very own copy of the ledger. Utilizing the consensus algorithms, the nodes can update their respective ledgers efficiently. Since there is no requirement for a central authority to intervene in any step, a public blockchain offers a truly decentralized network.

You have learned how to make a public blockchain solution in this blog! For an even deeper understanding of blockchain technologies, you can connect with our experts today.

Frequently Asked Questions(FAQs)

Q. What’s The Cost Of Creating A Blockchain In 2024?

A. The cost of creating a blockchain hinges on factors such as the type of blockchain (public, private, or consortium), project complexity, chosen platform and tools, consensus algorithm, features and functionalities, team size and location, development timeline, and infrastructure services. Each of these elements plays a role in shaping the overall expenditure, with considerations ranging from the intricacy of the project to the geographical location of the development team influencing labor costs. The selection of hosting solutions, infrastructure services, and development tools further contributes to the overall cost dynamics.

Q. Does Blockchain Require Coding?

A. Yes, it does. Knowledge of web development, data structures, and basic programming language is required for blockchain development.

Q. What Are The Leading Web 3.0 Frameworks For Blockchain?

A. The best Web 3.0 frameworks to assist blockchain developers in 2022 are the Truffle framework, Hardhat framework, Brownie Framework, OpenZeppelin SDK, and Chainlink SDK. You can learn more about them here.

Q. What Are The Top 5 Blockchains In 2024?

A. The top five blockchains in 2023 are:

- Ethereum (ETH): Ethereum, an open-source blockchain platform, empowers the development of decentralized applications (dApps) and the execution of smart contracts.

- Binance Smart Chain (BSC): Developed by Binance, this blockchain platform operates parallel to Binance Chain and ensures compatibility with the Ethereum Virtual Machine (EVM), facilitating the migration of Ethereum-based projects to BSC.

- Cardano (ADA): Operating with a unique dual-layer structure, Cardano is a blockchain platform designed for smart contracts.

- Polkadot (DOT): As a multi-chain platform, Polkadot enables collaboration between different blockchains within a shared security model.

- Solana (SOL): Renowned for high performance, Solana supports global developers in creating scalable crypto applications.