Modern-day consumers crave instant gratification, especially when it comes to shopping. But what if that new dress or the latest tech gadget could be yours today without the financial burden? Buy now, pay later apps like Afterpay have tapped into this emotional desire and have exploded in popularity with over 16 million users in the USA alone. Afterpay’s success story isn’t just about convenience – it’s about empowering customers to treat themselves without guilt!

However, the benefits extend far beyond the initial purchase. BNPL apps foster a sense of control and financial well-being. By dividing payments into manageable chunks, customers can avoid the burden of high-interest debt and remain in charge of their finances. This emotional connection with customers is what makes developing a BNPL app such a compelling opportunity for businesses. By offering a solution that prioritizes convenience, flexibility, and financial empowerment, your company can win the hearts, minds, and, ultimately, the wallets of today’s savvy consumers.

What are BNPL Apps?

BNPL stands for Buy Now, Pay Later. These are mobile applications that have become increasingly popular with shoppers, offering a new way to manage finances. Unlike traditional credit cards, BNPL apps allow customers to split their purchases into smaller installments, usually interest-free, and pay them off over a short period of time. This provides greater flexibility and control over spending compared to putting everything on a credit card with high interest rates.

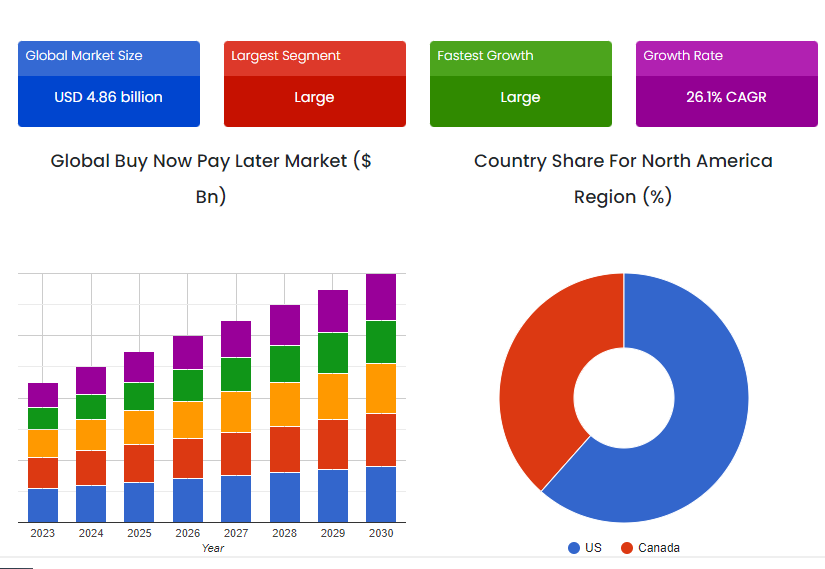

Key Market Takeaways for BNPL

Source: Skyquestt

These days, consumers are overwhelmingly embracing digital transactions. An interesting statistic from the UNCTAD reveals that over 80% of global shoppers now rely on digital payment methods for online purchases. This preference is driven by the clear advantages these methods offer. Compared to traditional cash or check payments, digital transactions boast lower transaction costs, faster fund transfers, and enhanced security, making them a more convenient and secure option for both businesses and consumers. This widespread adoption of digital payments creates a fertile ground for the BNPL market to flourish.

Moreover, the ubiquitous presence of smartphones acts as a major catalyst for BNPL growth. The exponential increase in smartphone penetration coupled with high-speed internet access empowers both businesses and consumers. Businesses can now seamlessly integrate BNPL options into their online stores, while customers can effortlessly make purchases using their smartphones. A compelling case study is Klarna, a leading BNPL provider. By partnering with major retailers like IKEA and H&M, Klarna has leveraged the power of mobile technology to offer a smooth in-app BNPL experience, contributing significantly to their success and the overall growth of the BNPL market.

How Afterpay Sets Itself Apart?

The BNPL market is pretty fierce, to be honest, but Afterpay has carved out a unique space for itself with features that directly impact how businesses and consumers interact with the app. Here’s how Afterpay sets itself apart:

1. Transparency with ClearPay

Unlike some BNPL options that bury fees in the fine print, Afterpay offers a feature called ClearPay. This upfront transparency shows users the total cost of their purchase divided into four equal installments. There’s no interest added if you make your payments on time, so you know exactly what you’re spending. This focus on clear pricing builds trust and encourages responsible spending habits with Afterpay.

2. In-store Power with Afterpay Card

While many BNPL services cater to online transactions, Afterpay doesn’t forget about brick-and-mortar stores. Their innovative Afterpay Card allows users to pay using the app at partnering stores. This expands Afterpay’s reach and makes it more attractive to retailers. This approach, called omnichannel, benefits both businesses and consumers by increasing buying options and driving foot traffic to physical stores.

3. Instant Decisions with Upfront Limits

Afterpay uses a feature called Upfront Limits to streamline the approval process. This sophisticated system gives you a spending limit and lets you know instantly if you’re approved for a purchase. There’s no waiting for lengthy applications or credit checks, making the shopping experience smooth and frictionless. This is a major advantage in today’s fast-paced retail environment, where getting that instant “yes” can be the difference between making a purchase or abandoning your cart.

4. Focus on You with My Afterpay

Afterpay prioritizes a user-friendly experience through a feature they call My Afterpay. This intuitive section of the app makes it easy for you to track upcoming payments, manage your budget, and discover stores that partner with Afterpay. This focus on user experience keeps you engaged and builds brand loyalty within the app itself.

Cost of Developing a BNPL App Like After Pay

Here’s a detailed cost breakdown for developing a BNPL app like Afterpay,

| Development Stage | Cost Range | Details |

| 1. Research & Planning | $5,000 – $15,000 | |

| Market Research | $2,000 – $5,000 | Analyzing competitor apps, market trends, and target audience needs. |

| User Experience (UX) Design | $1,000 – $3,000 | Wireframing app flow, creating user personas. |

| Project Management & Documentation | $2,000 – $7,000 | Defining project scope, milestones, deliverables, and creating technical specifications. |

| 2. Front-End Development | $20,000 – $75,000 | |

| Basic UI Design | $10,000 – $20,000 | Designing clean and intuitive app screens for core functionalities. |

| Advanced UI Design | $20,000 – $50,000+ | Custom animations, interactive elements, and unique brand identity. |

| Front-End Development | $15,000 – $40,000 | Building the user interface using frameworks like React Native or Flutter. |

| 3. Back-End Development | $30,000 – $100,000+ | |

| Server Setup & Security | $10,000 – $20,000 | Secure cloud infrastructure for handling user data and transactions. |

| Payment Gateway Integration | $15,000 – $30,000 | Integrating with secure payment processors. |

| Fraud Detection & Risk Management | $5,000 – $15,000 | Implementing systems to identify and prevent fraudulent transactions. |

| Database & Order Management | $10,000 – $35,000 | Robust database for storing user information, order details, and transaction history. |

| Credit Check Integration (if applicable) | $10,000 – $50,000+ | Integrating with credit bureaus for creditworthiness assessment. |

| 4. App Features | $10,000 – $100,000+ | |

| Basic Features | $5,000 – $20,000 | User accounts, login, product listings, search functionality, shopping cart, and checkout process. |

| Intermediate Features | $15,000 – $40,000 | Transaction history, budgeting tools, push notifications, in-app messaging, loyalty programs, rewards. |

| Advanced Features | $30,000 – $100,000+ | Integration with merchant platforms, gamification elements, personalized recommendations, AI-powered fraud detection and risk scoring. |

| 5. Testing & Deployment | $5,000 – $15,000 | |

| Quality Assurance (QA) Testing | $3,000 – $10,000 | Rigorous testing to ensure app functionality across platforms and devices. |

| App Store Submission Fees | $100 – $200 | Fees for releasing the app on the iOS App Store and Google Play Store. |

| Total Cost Range | $100,000 – $300,000+ |

What Factors Can Influence the Cost of Developing an App Like Afterpay?

Building a successful BNPL app requires careful planning, and a significant part of that plan revolves around understanding the cost involved. Here are the key factors that impact the overall price tag,

1. Feature Focus: Tailoring the App to Your Target Audience

The functionalities you choose to integrate significantly impact development costs. Core features like account management, transaction history, and installment management are essential. However, consider your target audience. Are you targeting young, tech-savvy millennials who crave real-time notifications and personalized offers? Or are you focusing on budget-conscious Gen Z shoppers who prioritize a streamlined, no-frills experience?

Adding features like gamified rewards programs or educational and financial tools might appeal to younger demographics but will come at an additional cost. Businesses need to strike a balance between offering a compelling feature set that resonates with their target users and keeping development costs manageable.

2. Enhancing User Experience: Creating a Frictionless Journey

A user experience that feels effortless is crucial for the success of the BNPL app. A smooth checkout process with clear instructions and multiple payment options is essential. A visually appealing interface that’s easy to navigate ensures a positive experience. Investing in user research can help identify potential pain points and refine the user journey. For instance, testing the app with users from diverse backgrounds can reveal potential language barriers or cultural nuances that need to be addressed. This ensures a seamless experience for a wider audience.

3. Going Multi-Platform: Reaching Every Customer

Building your app for both iOS and Android is a must for wider user accessibility. However, companies with a strong online presence might also consider a web-based version, allowing users to access BNPL functionalities directly from their desktops. Each platform has its own development requirements and needs to be optimized for performance and user experience. For instance, integrating fingerprint or facial recognition for secure logins might be a consideration for mobile app versions, while offering social login options on the web platform can streamline the registration process.

4. Connecting the Ecosystem: Integrating Seamlessly

To function effectively, your BNPL app needs to work seamlessly with various external systems. Integrating your app with his existing payment gateway and point-of-sale system is essential for a smooth transaction flow. BNPL apps also need to connect with banking APIs to verify user accounts and manage financial transactions. Regulatory compliance tools come into play as well, ensuring adherence to data protection laws and financial regulations. Companies should factor in the cost of integrating these external systems and implementing robust error-handling mechanisms to manage potential issues.

5. Security is Paramount: Building a Fortress of Trust

Security is a top priority for any financial app. Data encryption, tokenization of private data, and secure transmission protocols like SSL/TLS are essential safeguards. Additionally, implementing access restrictions, audit trails, and monitoring systems further strengthens security. Regular security assessments, vulnerability scans, and penetration tests are quite important for identifying and addressing potential weaknesses. By prioritizing security, companies build trust with users and avoid costly data breaches.

6. Regulatory Compliance: Navigating the Evolving Landscape

BNPL apps operate within a complex regulatory landscape. Staying compliant with data protection laws like GDPR and CCPA, financial regulations, and industry standards like PCI DSS is essential. Businesses need to understand and adhere to these regulations to avoid hefty fines and ensure responsible data practices. For instance, implementing user permission systems allows users to control their data, while data retention policies define how long data is stored. Building a culture of data privacy demonstrates transparency and fosters trust with users.

7. Location & Team Size: Balancing Costs and Expertise

The location of your development team can significantly impact costs. Regional differences in development rates play a role, with teams in certain locations commanding higher fees. Companies need to balance team size, project requirements, and budget. Larger teams offer specialized expertise and comprehensive testing capabilities but require better coordination and incur higher resource needs. Smaller teams may be more cost-effective but might require additional time to complete the project and ensure thorough testing.

What are Some Must-Have Features for an App Like to Afterpay

The BNPL market is flourishing for good reasons. These apps provide consumers with a convenient and flexible way to manage their finances. But what makes a BNPL app truly successful? Here’s a breakdown of all the essential features,

User Panel

To entice users, businesses should always prioritize features that can make their interaction with the app smooth.

1. Effortless Onboarding

Signing up should be a breeze. A smooth registration process with minimal steps encourages user adoption and keeps them engaged.

2. One-Click Checkout

Speed and simplicity are essential. A one-click shopping experience with automatic installment selection makes the checkout process a breeze.

3. Customer Support at Your Fingertips

Prompt resolution of questions, issues, and disputes is essential. Multiple channels like chat, email, and phone ensure users can get the help they need quickly.

4. Personalized Touches

Tailored product suggestions and offers based on user preferences enhance the shopping experience.

5. Flexible Payment Options

Catering to diverse financial situations is key. Users should be able to choose from different payment methods and installment plans that fit their budget and preferences.

6. Transparency is King

Clear disclosure of fees, terms, and payment schedules ensures users understand the financial commitment they’re making. No hidden surprises.

7. Real-Time Updates

Staying informed is crucial. Instant alerts for upcoming payments, transaction confirmations, and promotional offers keep users engaged and in control.

Retailer Panel

The primary goal of a retailer panel should be to allow businesses to effortlessly connect their existing point-of-sale systems, unlock valuable insights from transaction data, and achieve optimal inventory management.

1. Seamless Integration

Frictionless linking with retailers’ existing Point-of-Sale (POS) systems is a must. This allows in-store purchases to be made on BNPL terms, expanding reach and convenience.

2. Data-Driven Insights

It is essential to comprehend customer behavior and sales trends to achieve success. Detailed reporting and analytics tools provide retailers with valuable insights to optimize their offerings.

3. Inventory Management

Accurate product availability and pricing are essential for a smooth user experience. App integration with inventory data ensures users see what’s truly in stock.

4. Marketing Made Easy

Built-in features like promotional campaigns, discount codes, and targeted messaging empower businesses to attract and retain customers.

5. Branded Experience

Maintaining brand consistency is important. The ability to customize the app’s branding ensures a seamless experience for users who recognize and trust the retailer.

6. Compliance Support

Keeping up with regulations can be complex. Guidance on data protection laws and industry standards helps businesses navigate the landscape.

Admin Panel

A robust admin panel provides a centralized hub for managing all aspects of the BNPL app. Features include:

1. Performance Dashboards

Real-time insights on key metrics like user activity, transaction volumes, and revenue generated keep businesses informed and agile.

2. Transaction Monitoring

Real-time monitoring of transactions helps detect fraud, identify unusual activity, and ensure regulatory compliance.

3. Financial Management

Streamlined operations management, including releasing funds, accumulating revenue, and managing payouts to retailers.

4. Customer Support

Dedicated tools for managing customer inquiries, disputes, and escalations ensure a positive user experience.

5. Advanced Reporting & Analytics

These tools offer in-depth insights into user behavior and business performance, empowering data-driven decision-making.

6. Merchant Management

Efficient onboarding and management of merchants, including contracts, access permissions, and performance reviews.

7. User Management

Tools for managing user accounts, including verification, account suspensions, and password resets, ensure a secure environment.

8. Risk Management

Credit protection tools and mechanisms help businesses manage risk, minimize defaults, and prevent fraud.

Advanced Features of a BNPL App Like Afterpay

Beyond simple installment management and payment processing, the capabilities of a BNPL app like Afterpay offer improved functionality and user experience. The following are some of its advanced features:

Advanced Features You Should Include in a BNPL App

By incorporating the above features, you might have got yourselves a solid MVP or Minimum Viable Product. But you need to stand out, right?

To do that, businesses need to offer features that go beyond the core functionalities. Here’s a look at some advanced features that can elevate your BNPL app,

1. Subscription Management Hub

Simplify the subscription jungle. Create a central hub for users to manage all of their subscriptions, including BNPL plans. This allows users to easily track recurring payments, adjust or cancel subscriptions, and avoid unwanted charges. This transparency and control empower users and foster trust in the BNPL platform.

2. Voice-Activated BNPL Transactions

The future is voice-controlled. Integrate voice-activated technology for a seamless shopping experience. This voice-based functionality enhances accessibility and convenience, particularly for users on the go.

3. Smart Notifications

Simple transaction alerts are good, but smart notifications take it a step further. Personalized and context-aware push notifications can warn users about potential overspending based on their spending patterns. They can also send timely reminders about upcoming payments, allowing users to stay on top of their finances.

4. Augmented Reality

When shopping for clothes or accessories online, there can be some risk involved. However, the use of AR try-on features can help users to virtually ‘try on’ their products before buying them. This helps reduce the risk of having to return items and enhances the overall shopping experience. Ultimately, this can help increase customer satisfaction and potentially reduce business hassle.

5. Green Financing for Eco-Conscious Consumers

Sustainability is becoming an increasingly important issue for many consumers. Forward-thinking BNPL apps are incorporating green financing options. This could involve carbon-neutral payment schedules or BNPL purchases that include donations to environmental charities. By aligning with eco-conscious values, businesses can attract a wider user base and contribute to a more sustainable future.

6. Localized Currency and Language

Localization is crucial for any business looking to expand internationally. Supporting different currencies and languages allows BNPL apps to serve a worldwide user base. This not only increases the potential customer pool but also simplifies international transactions for users, removing barriers to global shopping.

7. AI for Smarter Risk Management

Traditional credit checks can be slow and impersonal. Advanced BNPL apps leverage AI-driven risk assessment. Machine learning algorithms analyze a user’s financial data in real time, enabling dynamic spending limits and tailored risk profiles. This allows businesses to approve responsible users quickly while mitigating potential risks.

8. Financial Wellness Tools

Financial literacy is key to responsible spending. Some BNPL apps offer financial wellness tools like savings calculators, budgeting tools, and educational resources. These features empower users to make informed financial decisions and build a healthy relationship with credit.

How to Monetize a Buy Now Pay Later app?

Did you know that in just one quarter, Afterpay processed over $18.9 billion in underlying sales? This Australian BNPL giant is revolutionizing the way people shop, boasting over 16 million active users globally.

But with all this activity, how do BNPL apps turn millions of transactions into billions in profits? Here’s a look at some key monetization strategies that can keep your BNPL app financially healthy and capitalize on this booming market:

1. Late Fees

Let’s face it, late fees aren’t the most popular strategy, but they do serve a purpose. A recent study by Credit Karma found that 72% of BNPL users have missed a payment at least once. While late fees incentivize timely payments, they can also damage user loyalty. The key is to strike a balance. For example, Klarna, another major BNPL player, offers a grace period before late fees kick in, giving users a chance to catch up without penalty.

2. Merchant Fees

Merchant fees are a significant revenue stream. According to Forbes, Afterpay typically charges merchants 3-4% per transaction. The high volume of transactions processed by BNPL apps translates to significant income. But it’s a two-way street. BNPL apps can offer value-added services to merchants, like access to a wider customer base or data-driven insights into consumer spending habits. This strengthens partnerships and creates a win-win situation.

3. Currency Conversion

As BNPL goes global, currency conversion fees become a factor. A recent study reported that millennials, a key BNPL user demographic, are increasingly comfortable shopping internationally. Transparent currency conversion fees are crucial here. Apps like Affirm display the exact amount users will pay upfront, including any conversion fees, fostering trust and avoiding unpleasant surprises.

4. Merchant Marketing Services

BNPL apps can be powerful marketing platforms for businesses. Imagine a clothing store offering a sponsored product placement on the app’s homepage during a seasonal sale. This increases the store’s visibility and attracts app users who might be interested in those specific sale items. Targeted advertising based on user purchase history can further personalize the experience and boost sales for merchants, generating revenue for the app through these marketing services.

5. Interest on Extended Plans

While standard BNPL plans are often interest-free, some apps offer extended payment options with interest charges in partnership with lenders. This can be a lucrative strategy, but responsible lending practices are essential. Clear communication of interest rates and terms is key to building trust with users. Regulations around this are also evolving as the CFPB recently announced plans to examine BNPL lending practices to ensure consumer protection.

How to Develop a BNPL App Like Afterpay?

Businesses need to have a well-developed app to enter the BNPL market. Let’s discuss the key steps involved in creating a successful BNPL app like Afterpay:

1. Know Your Market and Users:

A thorough understanding of the BNPL landscape is essential. BNPL companies need to conduct market research to identify current trends, analyze user needs, and study competitor offerings. This involves gathering data on popular features, target demographics, potential challenges, and even observing consumer purchasing habits. Direct user input through focus groups or surveys helps further refine the app’s value proposition.

2. Craft a Compelling Feature Set:

The app’s core functionalities are essential: account management, transaction history, installment management, secure payment processing, user authentication, and seamless integration with popular eCommerce platforms. However, differentiation is key. Businesses should prioritize features that cater to customer needs while setting the app apart from competitors. This could include social sharing functionalities, budgeting tools, loyalty programs, and personalized product suggestions. Remember, it’s crucial to develop features with scalability in mind, ensuring the app can adapt to future market changes and updates.

3. Design for User Delight:

A user-friendly experience is paramount. Here, developing intuitive interfaces takes center stage. Businesses should create clear and user-friendly wireframes and prototypes, ensuring a smooth user journey. Maintaining brand consistency, typically by adhering to established guidelines like Afterpay’s branding, is crucial for a cohesive design. Testing with the target audience throughout the design process is vital for gathering feedback and refining usability. For today’s multi-device world, optimizing the app for various screen sizes and ensuring a seamless experience across mobile and desktop platforms is essential.

4. Building the App: A Technical Journey:

Developing a robust app requires building both the user-facing front-end and the backend systems that handle data processing and integrations. Choosing the right technology stack is crucial. Businesses need to select scalable, secure, and compatible technologies and frameworks to ensure the app’s stability and performance. Agile methodologies, which promote flexible and iterative development cycles, are ideal for BNPL app development, allowing for quick adaptation based on user feedback and market changes. Implementing code reviews and rigorous testing throughout the development process ensures high code quality and swift identification of any issues.

5. Security: Building Trust Through Protection

Protecting user data is a top priority. Businesses should implement robust data encryption techniques to safeguard sensitive information. Employing secure authentication methods, including biometrics and two-factor authentication, adds another layer of security. Regular security audits are essential to proactively identify and address vulnerabilities. Furthermore, monitoring systems and algorithms help detect suspicious activities quickly, allowing for prompt mitigation.

6. Testing and Refinement: Ensuring Quality

Before launching the app, comprehensive testing is crucial. This involves identifying and fixing flaws in functionality, usability, and security. Different types of testing, including functional, performance, usability, and security testing, ensure a polished final product. User acceptance testing gathers feedback from real users to validate the app’s usability and functionality before the official launch. By adopting an iterative approach to testing, businesses can continuously refine their testing methodologies and maintain high-quality standards.

7. Launch and Beyond: Reaching Users and Adapting

Launching the app is just the beginning. Developing marketing materials, creating app store listings that optimize discoverability, and planning launch activities are all crucial steps. Following the launch, businesses need to monitor key performance indicators using analytics tools. These KPIs, including download rates, user engagement, and retention rates, provide valuable insights for data-driven decision-making and continuous improvement plans.

8. Continuous Improvement: A Commitment to Users

The BNPL industry is constantly evolving. To stay ahead, it’s crucial to continually update based on user feedback. Addressing user-reported issues and rolling out new features demonstrates a commitment to improvement. Businesses should actively gather feedback through various channels, such as community forums, in-app forms, and customer support. By adopting an agile approach to updates, businesses can ensure their BNPL app remains competitive, aligned with user needs, and reflective of the latest industry trends.

Top 5 Unique BNPL Apps Recently Launched in the USA

While Afterpay dominates headlines, several other BNPL apps are making waves in the USA market. Let’s have a closer look at these BNPL apps,

1. Sezzle: Targeting Millennials and Gen Z

Sezzle is an Australian BNPL giant that recently launched in the USA in 2020. It offers a virtual credit card that allows users to split their purchase into four interest-free payments over six weeks. They have a focus on millennial and Gen Z shoppers and partner with a wide range of retailers, including Forever 21, Urban Outfitters, and końco.

They hold a strong position with younger demographics, with over 80% of their users being millennials and Gen Z. Sezzle partners with over 40,000 USA retailers and processes over $1 billion in transaction volume annually. In a strategic move, Sezzle partnered with Klarna in February 2024 to offer customers a wider range of payment options.

2. PayLater by Zip: Leveraging Established Brand Recognition

This app, launched in the USA in 2022, is a subsidiary of the established Australian BNPL player Zip. It allows you to split your purchase into four interest-free payments spread over six weeks. They target a general audience and partner with a variety of popular retailers, which include Bed Bath & Beyond, J Crew, and West Elm.

It boasts a user base exceeding 10 million globally. They partner with over 50,000 merchants worldwide. Capitalizing on their growth, PayLater announced a collaboration with a major USA bank in May 2024 to expand their reach and offer co-branded BNPL options.

3. Split it: A Social Spin on BNPL

Split it offers a unique twist on BNPL. It allows you to split the cost of a purchase with friends and family. It works directly through the user’s bank account, so no additional accounts are needed. Launched in the USA in 2021, Split partners with a smaller number of retailers, including Macy’s, Sam’s Club, and Michaels.

A Credit Karma study in March 2024 found that 62% of USA millennials prefer to split large purchases with friends or family. This aligns with Split’s target market. Demonstrating its focus on social integration, Split launched a new feature in April 2024, allowing users to request splits directly through social media platforms.

4. Perpay: Empowering Small Businesses

Perpay is a point-of-sale financing option launched in the USA in 2022. They target small business owners by offering them BNPL options to increase their average order value. Perpay integrates directly with a merchant’s existing point-of-sale system.

Perpay gained recognition in a Forbes article (May 2024) highlighting innovative BNPL solutions for niche markets.

5. Affirm: Fractional Share Investing with BNPL

Affirm Equities is a new twist on BNPL, launched in 2022, that allows users to invest in fractional shares of stocks with the option to pay in installments. This can be a great way for new investors to get started in the stock market without a large upfront investment.

A Charles Schwab investor insights report (2023) revealed that over 60% of Gen Z individuals are interested in investing, aligning with Affirm Equities’ target audience. Recently, Affirm Equities announced a partnership with a leading micro-investing platform in June 2024 to offer their fractional share BNPL option to a wider audience.

Conclusion

These days, consumers crave convenience and flexibility when it comes to shopping. BNPL apps like Afterpay have emerged as a powerful force, addressing this need and disrupting traditional payment methods. Developing a BNPL app can be a strategic move for businesses aiming to enter this rapidly growing market.

A well-designed BNPL app offers several advantages. It attracts a wider customer base, particularly younger generations who are comfortable with mobile-first financial solutions. Moreover, BNPL apps can boost sales conversion rates by enabling users to split payments, potentially resulting in larger average order values for businesses. By emphasizing a user-friendly experience, strong security features, and cutting-edge functionalities, companies can create a BNPL app that encourages customer loyalty and sets them up for success in the constantly changing financial technology industry.

Looking to Develop a BNPL App Like AfterPay?

Don’t just keep up with the BNPL revolution; lead the charge! At Idea Usher, our 500,000 hours of coding expertise in the field will translate into a best-in-class BNPL app for your business. We go beyond building an Afterpay copycat – we craft a user-centric platform that anticipates the evolving needs of both users and merchants, guaranteeing an app that exceeds expectations and captures a loyal following. Let Idea Usher turn your BNPL vision into reality.

FAQs

Q1: How much does it cost to develop a BNPL app?

A1: The cost of developing a BNPL app depends heavily on the features you choose to include and the overall complexity of the app. A stripped-down version with core functionalities will naturally cost less than a feature-rich app with robust security measures. Additional factors like the development team’s location and the level of customization you desire can also influence the final price tag. Considering the initial investment may appear significant, view it as an entry into a thriving market with the potential for substantial returns from various revenue streams.

Q2: What is the cost structure of BNPL?

A2: The BNPL cost structure is two-sided. For users, late fees are the main cost, while merchants typically pay a transaction fee ranging from 3% to 7% to cover processing and potential defaults. BNPL companies also incur costs for development, marketing, fraud prevention, and loan repayments if they offer interest-bearing extended plans. Building a user base and managing these costs effectively are key challenges for BNPL businesses in achieving profitability.

Q3: How much does BNPL charge merchants?

A3: BNPL fees for merchants typically range from 3% to 7% of the transaction value. This fee compensates BNPL companies for processing the transaction, managing the installment plan, and assuming the risk of defaults. The exact fee can fluctuate depending on the merchant’s industry, transaction volume, and negotiation with the BNPL provider. Some BNPL companies may also offer tiered fee structures with lower rates for higher transaction volumes.

Q4: Are any BNPLs profitable?

A4: The profitability of BNPL companies is currently being debated. While the market is experiencing explosive growth, many BNPL businesses are not yet turning a profit. This is due to factors like low merchant fees, costs associated with late fees and fraud prevention, and the emphasis on user acquisition over immediate income. However, some established players are exploring alternative revenue streams, such as interest in extended plans and strategic partnerships. With careful planning and a diversified revenue model, BNPL companies have the potential to achieve profitability in the long run.