(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Are you planning to implement blockchain for your business?

Forget everything you think you know about blockchain. It’s no longer just the playground for cryptocurrencies. Businesses of all sizes are waking up to the transformative power of this technology, and it’s fundamentally changing the way they operate.

Imagine a world where trust is built into the system, data is tamper-proof, and transactions are streamlined. That’s the power of blockchain, and it’s not just science fiction anymore. From supply chain management to loyalty programs, this blog will guide you through the exciting world of blockchain implementation and show you how your business can harness its potential to stay ahead of the curve.

NFTs, decentralized apps, cryptocurrencies, and so on, as well as blockchain, offer many benefits to businesses.

Many companies, such as Microsoft and Intel, are looking for blockchain implementation to make their business profitable in the long run.

However, blockchain implementation can be challenging due to the limited number of blockchain developers available.

Still, there is a perfect way for us to discuss implementing blockchain technology in your business correctly. Let’s check how you can add blockchain technology to your business.

What is Blockchain?

Blockchain is a decentralized system of recording information, making it impossible to change or hack once the data is stored on its network.

The network contains a series of blocks, each containing several transactions. When new transactions are made on that blockchain, they are stored as a block and linked to their previous node.

Moreover, blockchain’s decentralized nature helps organizations improve their business in many ways.

Facts That Prove Blockchain is Revolutionizing Industries

- Global Adoption: Did you know 10% of the world already owns cryptocurrency? This is a sign of a financial revolution unfolding.

- US Embracing Crypto: A whopping 16% of Americans, according to Pew Research, are actively investing in crypto, demonstrating widespread acceptance of digital currencies.

- Cost Savings for Businesses: Economic Times reports that blockchain has the potential to save financial institutions a staggering $12 billion annually.

- Healthcare on the Blockchain: The healthcare industry is embracing blockchain, with the market projected to reach $231.0 million by 2023 – a remarkable 63% growth.

- Reduced Trading Fees: Research Briefs suggest that transitioning securities to blockchains could save a jaw-dropping $17 billion to $24 billion annually in global trading fees.

- Banking Leads the Way: A Statista survey reveals that Banking holds the top spot in terms of blockchain market value distribution, followed by process and discrete manufacturing sectors.

Key Market Takeaways For Blockchain Technology

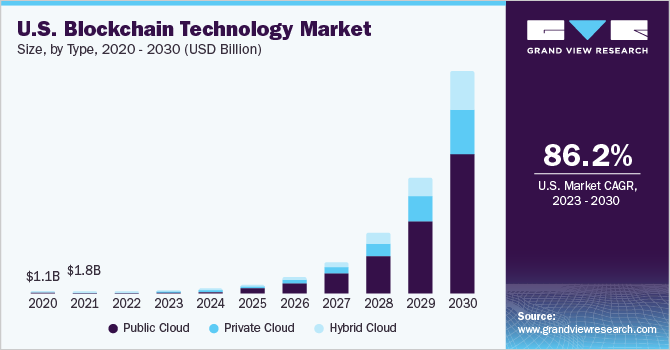

The global blockchain technology market reached a value of USD 17.46 billion in 2023. Analysts predict a significant surge in the coming years, with a compound annual growth rate (CAGR) of 87.7% projected from 2023 to 2030. This growth is fueled by the rising demand for secure and transparent transactions across various industries.

Blockchain technology offers a unique solution with its decentralized and immutable ledger system. This system guarantees the integrity and transparency of transactions, making it highly attractive to sectors like finance, healthcare, and supply chain management. As a result, businesses within these domains are increasingly turning to blockchain solutions to improve the security and transparency of their operations.

Is Blockchain the Turning Point for Startups?

The startup world is buzzing with excitement about blockchain technology. This isn’t surprising, considering the inherent fit between blockchain’s innovative nature and the forward-thinking spirit of startups. As agile young companies, startups are constantly seeking disruptive technologies that can give them a competitive edge and solve existing problems.

For startups, blockchain development offers a compelling array of benefits. Its focus on security and trust aligns perfectly with the need for reliable platforms. Additionally, blockchain’s potential unlocks new avenues for fundraising, democratizing access to capital. From revolutionizing industries to streamlining operations and building stronger customer trust, startups see blockchain as a powerful tool to disrupt the status quo.

But the impact of blockchain extends beyond startups. A telling sign of its widespread adoption is the fact that 81 of the world’s top 100 public companies are already on board with the technology. Even more impressive, 27 of these companies have already launched fully functional blockchain products. This highlights the rapid integration and implementation of blockchain across diverse industries. As a transformative technology that adds significant value, blockchain is fundamentally reshaping how businesses operate and interact with their stakeholders, driving global innovation and efficiency.

How do businesses benefit from blockchain technology?

Multiple blockchain benefits, such as high trustability, security, and many others, make businesses adopt blockchain technology in their architecture.

Understand in detail the benefits blockchain provides to businesses:

1. Transparency

Centralized systems are limited to providing a high level of transparency, which is not the same as in the case of a centralized network. A blockchain contains peers where validation happens through a conscious protocol. In addition, this network provides instant and transparent transactions for businesses.

2. Security

Once the data is stored on the blockchain, it cannot be modified. Also, each block is encrypted and connected to the old transaction. Even more, each node has a copy of older transactions that hackers cannot change, as the nodes will refuse the hackers’ request to write transactions on their network. Thus, in this way, blockchain improves the security and trust of the system.

3. Tokenization

Tokens are digital assets that define ownership in a particular blockchain network. Moreover, many documents of physical assets like gold, equity, real estate, crude oil, legal documents, or any other physical assets can be tokenized on a blockchain network, improving its security and privacy in terms of ownership.

Also, it would be beneficial for you to be familiar with the challenges you may face while implementing blockchain.

4. Individual control of data

Blockchain provides excellent control to individuals to manage their data through the help of smart contracts as no one can modify the data once it gets deployed on the blockchain network.

Since blockchain gives a better way of ownership through NFTs, anyone can tokenize their documents and data into nonfungible tokens and make them resistant to getting stolen or altered.

5. Streamlined Processes and Reduced Costs:

Cut through the paperwork jungle! Blockchain automates processes, eliminates middlemen, and streamlines workflows, leading to significant cost savings.

Now, let’s check the steps to implement blockchain technology into businesses successfully.

Steps to Implement Blockchain Successfully

Follow the steps to ensure you have correctly implemented blockchain technology in your business.

1. Understand the use case of blockchain

You need to understand why you need blockchain technology for your business. To ensure whether your business needs blockchain technology, ask the following question to yourself:

- What pain point will it solve?

- Why does my business need blockchain technology?

- What objectives and targets need to be fulfilled after implementing blockchain technology?

2. Build proof of concept

Building the proof of concept will help you understand whether this technology is essential to your business. Even better, ask these questions yourself:

- What problem is my business trying to solve?

- What results do I expect after blockchain implementation?

- How can I use this technology to transform my business?

3. Choose the right blockchain platform

Selecting the suitable blockchain platform for your business can be done successfully by analyzing your business requirements and deciding what kind of blockchain you need to implement by checking the following criteria:

- Public or private nature of blockchain?

- How many users do you need to handle?

- Permissioned or permissionless blockchain network?

- What level of privacy do you need in your business?

- What use case is required? Do you need smart contracts, cryptos, or NFTs?

- What kind of control do you need, either centralized or decentralized?

However, to make your selection easier, you can choose from the following blockchain network to implement in your business:

I. Ethereum

The platform is best suited for building smart contracts to Improve business scalability. The platform is best used for building various decentralized applications like blockchain games, exchange apps, etc.

II. Stellar

Stellar is the next best platform for building blockchain applications for organizations. The platform partnered with IBM and KickEx in 2017 to fulfill the intent of offering low-cost transaction services in the South Pacific region. Stellar is best for businesses wanting a high-performing and easy-to-use affordable blockchain platform.

III. HyperLedger fabric

Founded by the Linux Foundation and IBM, Hyperledger Fabric offers a list of beneficial tools for building intelligent contracts for crypto developers. The platform provides multiple benefits to the business, such as reliable performance, plug-in components support, and smart contracts to make in various programming languages.

IV. Nem

The platform is built on Java programming language, which makes it an excellent choice for businesses to use Nem blockchain as they can quickly train their developers for blockchain implementation.

However, the name blockchain has a less decentralized nature than other blockchain networks.

4. Selecting blockchain as a service provider

Companies can use blockchain as a service to implement and leverage blockchain models and architecture from the big tech giants like:

- Amazon or AWS (Amazon Web Services)

- Microsoft’s Azure

- Oracle

5. Building and testing solutions

A vice decision is to adopt technology capable of modification to meet business demands. To meet the following criteria, you can check whether blockchain technology supports multichain and multiple platforms.

Also, if you have any app, you can test it on the test network to ensure it works as expected for your business needs.

6. Integrating blockchain with legacy system

The legacy system will help your business link with your partners using traditional centralized platforms. Make sure to integrate a legacy system into your business infrastructure to ensure you won’t lose a lot of opportunities due to an inability to connect with your business partners that depend on centralized technologies.

7. Operate & manage

When ready to deploy your project, build your first block, including all the decided features. Next, create your secondary block to expand your network. The primary intent of creating this block is to send information to the second block so that it can offer grounds for other blocks to receive the information.

8. Deployment

You will have to activate your blockchain solution on the decided blockchain network at this stage. If you have opted for a hybrid solution, which is the combination of on-chain and off-chain entities, you need to start with a cloud server.

9. Select the suitable consensus protocol

Choosing the correct protocol for your business is essential. Therefore you must know all the questions as protocol available in the blockchain and select the one that suits your business:

I. Proof of work

This protocol rewards blockchain miners after they solve tricky equations to maintain the structure of a specific blockchain

II. Proof of stake

The protocol allows crypto owners to stake their coins to create their validator nodes. During the staking period, the coins are locked, making them unavailable for trading.

III. Delegated proof of stake

Voting and election-based protocols compete with proof of work and stake models to verify transactions and promote their blockchain organization.

IV. Byzantine fault tolerance (BFT)

It is a computer ability where the protocol operates if some do not fail or act maliciously. The primary intent of this protocol is to reduce the negative effect of Byzantine nodes on the network.

V. Proof of weight

In this mechanism, the blockchain distributes weight among users based on how many cryptocurrencies they hold. The protocol is highly customizable and has great potential to scale.

Use cases of blockchain for your business

Here’s the common use case of blockchain technology for businesses:

1. Money transfer

Transferring money using blockchain Technology is less expensive and faster than the traditional currency of different countries by eliminating the cross-border transaction fees and other limitations in the current banking system.

Having an account in which to transfer money benefits businesses in multiple ways. They can quickly make payments to their business partner and employees in cryptocurrencies such as Bitcoin or Ethereum to avoid all the challenges when transferring money from one country to another.

2. Logistics and supply chain tracking

Tracking items through logistics using blockchain Technology chain offers money advantages such as securing business data on a secure public ledger.

Next, blockchain technology offers excellent resistance to data notification, which is essential for businesses to protect themselves from hacking or getting stolen by their competitors.

Moreover, integrating blocks and technology into logistics and supply chains can help businesses to build greater trust since the data provided for inventory tracking by blockchain networks are accurate and up to date.

The most common use case of blockchain technology is deploying smart contracts. Let’s understand how you can review smart contracts while integrating blockchain technology.

3. Data storage

Using blockchain technology for data storage offers excellent security and privacy compared to centralized data storage providers. Using decentralized cloud storage makes it almost impossible for hackers to wipe out all the data on a network.

Decentralized cloud storage offers an excellent option for companies to secure and keep their data private from anyone by implementing blockchain technology in their business.

4. Smart contracts

The most common use case of blockchain technology for companies is implementing smart contracts between their business partners. Smart contracts are digital contracts stored on the blockchain network and executed when the contract has predetermined terms and conditions.

Smart contracts are safer and more secure than traditional contracts because no one can modify the digital contracts once they are stored on the blockchain network. Also, you need to follow proper guidelines and auditing methods that you must know to take advantage of your business.

The right way to review the smart contract

No doubt about how powerful smart contracts are; however, some risk is associated with them, such as you can’t modify smart contracts once deployed to the blockchain network.

The only best solution is to review your smart contract completely before deploying it to the blockchain. You can follow the given practices while reviewing your smart contracts.

- Static code analytics and analyzing code quality of smart contracts to find whether they will be able to deliver the desired functionalities through smart contracts auditing

- Identifying critical vulnerabilities like overflows, shadowing of variables, reentrancy, overflows, underflows, incorrect cryptographic signature validation, etc.

Key Considerations for Blockchain Implementation

Blockchain technology holds immense promise, but its implementation requires careful planning and execution. Here’s a breakdown of crucial factors to consider for a smooth and successful integration:

1. Identifying the Right Use Case:

Don’t get caught in the hype! Before diving in, ensure blockchain genuinely addresses a specific challenge in your business. Is it about enhancing data security, streamlining processes, or fostering greater transparency? A clear use case is the foundation for a successful implementation.

2. Building a Strong Team:

Blockchain implementation isn’t a solo act. Assemble a team with the necessary expertise, including developers familiar with blockchain protocols and security best practices. Domain knowledge is also crucial to bridge the gap between technology and your specific business needs.

3. Choosing the Right Platform:

The world of blockchain platforms is vast. Conduct thorough research to identify a platform that aligns with your project’s requirements. Consider factors like scalability, security features, developer tools, and the existing community around the platform.

4. Prioritizing Security:

Security is paramount in blockchain. Implement robust security measures to protect your data and transactions. This may involve regular security audits, secure coding practices, and robust access control mechanisms.

5. Planning for Scalability:

Blockchain projects often start small but have the potential to grow exponentially. Choose a platform and architecture that can scale efficiently to accommodate an increasing user base and transaction volume.

6. Regulatory Compliance:

The regulatory landscape surrounding blockchain is constantly evolving. Stay informed about relevant regulations and ensure your implementation complies with current and potential future regulations.

7. Communication and User Adoption:

Successful blockchain adoption hinges on clear communication with all stakeholders. Educate users about the technology and its benefits to encourage their active participation.

8. Continuous Learning and Improvement:

Blockchain technology is rapidly evolving. Embrace a culture of continuous learning and adaptation. Stay updated on the latest trends and innovations to ensure your blockchain solution remains relevant and effective over time.

Challenges of implementing blockchain

You must be ready to settle down with the limitations temporarily present in the blockchain, which undoubtedly improved over time.

1. Government issue

Proper government regulation has not been implemented yet, which increases the chances of scams on the blockchain network. However, blockchain can’t be hacked due to its irreversible nature.

2. No regulatory clarity

Blockchain technology is fast growing, which means there is no time for a government organization to introduce proper rules and regulations to blockchain technology.

Unclear regulations create challenges for many businesses as no one is sure how the government will treat blockchain technology in the future.

However, many big brands like Samsung and Huawei are preparing themselves with this technology, which assures us that blockchain technology will have proper government regulations.

3. Lack of experts

Businesses find it hard to develop blockchain applications and struggle to implement this technology as experienced blockchain developers are rarely available in the market.

As blockchain technology is growing continuously, there is a high possibility that more blockchain developers will be available in the future.

4. High energy consumption

Blockchain consuming high energy consumption is another challenge on a global level. Many blockchain platforms, such as Bitcoin, use a proof-of-work consensus algorithm that demands high computational power, which can be fulfilled by the process known as blockchain mining.

Nearly 2.0% of the total electricity is used by blockchain miners worldwide. However, other consensus algorithms, such as proof of stack and proof of weight, consume less energy than proof of work.

5. Slow processing

Blockchain uses a complex mechanism that takes more time to process transactions, encryption, and decryption. Since all the participants compete on crypto coins by solving complex problems through different consensus algorithms, it becomes hard for blockchain developers to process any transaction quickly compared to a centralized server.

How do we make the team for blockchain implementation?

The key to successfully implementing blockchain technology into your team is to create a team that works together on your business purpose. Your team must be familiar with blockchain technology before implementing it in your business.

Here’s a list of checkpoints that need to be considered before forming a blockchain team:

- Programmers must be well versed in programming languages like JavaScript, Java, C++, C Python, and Node.JS and have experience with blockchain-based programming languages such as Golang and Solidity

- They must have excellent knowledge of cybersecurity concepts such as secure algorithms and have proficiency in algorithms and data structure.

- The blockchain developer should be able to write code in solidity, be familiar with creating blockchain API, and work effectively to solve blockchain scalability problems such as Hyper Ledger, where the developer can create a private blockchain.

- They are proficient in maintaining client and server-side blockchain applications.

Skilled blockchain developers are hard to find, but here is the best way to hire a perfect candidate to implement blockchain technology in your business.

Hire blockchain developers for your business

Mastering blockchain technology is hard, and more work experience is needed to become proficient in implementing blockchain technology.

Also, you may find it hard to train new employees to work in the role of blockchain developer, which may take years and is unsuitable for your business as your competitor can take this opportunity to get ahead of you.

The best thing you can do is to hire experienced blockchain developers for your team who can help you quickly with blockchain implementation in your business.

You can contact Idea Usher, as their team has experienced blockchain developers who have already worked on many decentralized projects related to smart contracts, NFTs, dApps, etc.

Contact Idea Usher:

Email:

Phone:

FAQ

Q. How do you implement blockchain in business?

Implementing blockchain involves a strategic approach. Here’s a simplified breakdown:

- Identify a need: Can blockchain solve a specific challenge in your business (e.g., secure transactions and improve traceability)?

- Proof of Concept (POC): Develop a small-scale project to test the feasibility of blockchain for your use case.

- Platform Selection: Choose a suitable blockchain platform (e.g., Ethereum, Hyperledger Fabric) based on your needs.

- Develop Smart Contracts (optional): If needed, create self-executing contracts to automate specific processes on the blockchain.

- Integrate and Pilot: Integrate the blockchain solution with your existing systems and run a pilot test before full deployment.

Q. How does blockchain improve business?

Blockchain offers several advantages for businesses:

- Enhanced Security: A decentralized ledger ensures tamper-proof data and secure transactions.

- Increased Transparency: All participants share a single view of the data, fostering trust and traceability.

- Improved Efficiency: Automates processes with smart contracts, streamlining operations.

- Reduced Costs: Eliminates intermediaries in certain transactions, potentially lowering costs.

- New Business Models: Unlocks innovative business models based on secure data and collaboration.

Q. How do I implement my own blockchain?

While possible, building your own blockchain requires significant technical expertise and resources. It’s often more practical to consider:

- Existing Blockchain Platforms: Utilize established platforms like Ethereum or Hyperledger Fabric for your business needs.

- Consortium Blockchains: Collaborate with other businesses in your industry to develop a shared blockchain infrastructure.

Q. How could blockchain shape your future and your business?

Blockchain has the potential to revolutionize various aspects of business:

- Supply Chain Management: Track goods movement transparently, ensuring authenticity and origin traceability.

- Financial Services: Enable secure and efficient cross-border payments and smart contracts for automated financial processes.

- Data Security: Provide a secure and tamper-proof platform for storing and managing sensitive data.

- Customer Engagement: Build stronger customer relationships through transparency and trust in data ownership.

These are just a few examples. As blockchain technology continues to evolve, it’s likely to play an increasingly important role in shaping the future of businesses and how they operate.