(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

The BNPL finance sector is experiencing rapid growth, with a considerable user base of 380 million users already on board. This convenient and innovative approach is garnering attention from businesses and entrepreneurs globally. Wisetack is an exemplary app that has effectively capitalized on this demand by targeting in-person service businesses. Its success underscores the current opportunity to enter the market and develop a BNPL app similar to Wisetack.

This blog extensively explores the essential features that contribute to the success of an app like Wisetack and provides a detailed breakdown of the factors influencing development costs. Whether you’re an experienced fintech entrepreneur or just beginning your BNPL journey, this comprehensive guide equips you with the necessary information to make well-informed decisions and navigate the dynamic world of BNPL app development.

What is the BNPL Financing App?

BNPL stands for Buy Now, Pay Later. These financing apps are changing the way we shop by allowing you to split your purchases into manageable installments. Imagine that new gadget you’ve been eyeing – instead of paying the full price upfront, a BNPL app lets you break it down into smaller payments spread over weeks or months.

Using a BNPL app is generally quite straightforward. Download the app, sign up, and you’re ready to shop! Many online retailers and even some physical stores offer BNPL financing at checkout. Simply select the BNPL option during payment, and the app will handle the installment payments.

The key advantage of BNPL apps is their budgeting flexibility. By splitting your purchases, you can avoid straining your finances with a large one-time expense. It’s like having access to those desired items without depleting your savings or relying on high-interest credit cards.

Key Market Trends for BNPL

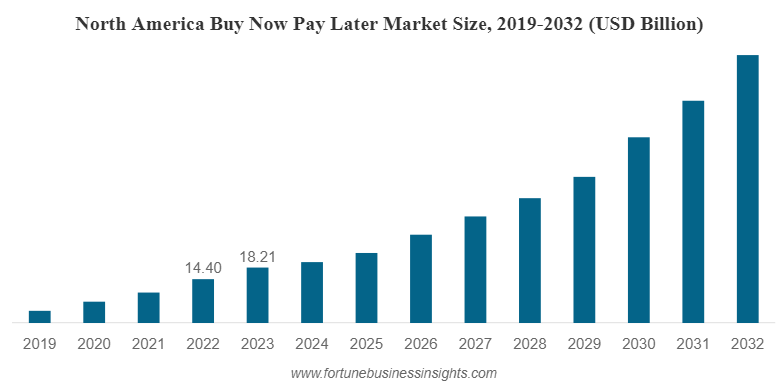

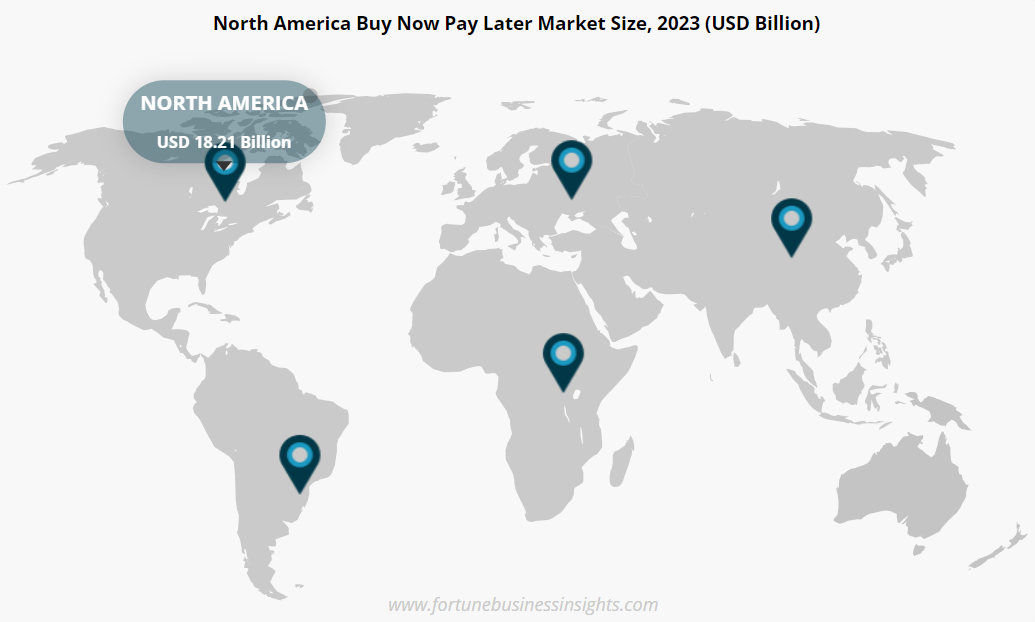

The “buy now, pay later” way of shopping is exploding in popularity. According to Fortune Business Insights, It’s expected to jump from a 30 billion dollar market in 2023 to a whopping 167 billion by 2032! That’s because more and more people are shopping online and want an easy way to pay.

BNPL is particularly appealing to millennials, a generation that has grown up with technology. It allows them to divide their purchases into manageable installments, facilitating better budget management. Moreover, it often comes with no interest, a stark contrast to credit cards that can impose hefty charges.

Right now, people in the US only use about 20% of their credit card limits. But if banks offered BNPL with their cards, they could raise those limits to a much bigger number by 2025. That means more money flowing through the banks!

The US is leading the way in BNPL, with lots of new companies starting up and banks getting involved. This is because people there are using BNPL more and more to buy things online. Basically, BNPL is changing how people pay. It’s convenient, affordable, and lets people be in control of their money.

Why Are BNPL Apps in High Demand?

Buy Now, Pay Later apps are financial solutions that allow consumers to make purchases and pay for them over time through installment payments. These apps are designed to provide an alternative to traditional credit cards, offering a more flexible and accessible way to manage finances.

BNPL apps typically split the total purchase amount into smaller, interest-free payments that are spread over a defined period, usually a few weeks or months. This payment model helps consumers manage their cash flow better and makes higher-priced items more affordable.

Financial Flexibility

BNPL apps empower consumers to manage their finances more effectively. Unlike credit cards with potentially high interest rates, BNPL allows them to spread out payments over time, often interest-free if paid on schedule. This predictability helps them stay within their budget and avoid debt spirals.

Enhanced Affordability

By segmenting expensive purchases into smaller installments, BNPL apps make them more attainable for many consumers. This can be particularly attractive for higher-priced items like electronics, furniture, or appliances. This expanded buying power translates to increased sales for businesses and potentially fuels a cycle of economic growth.

Streamlined User Experience

BNPL apps seamlessly integrate into the checkout process, eliminating the need for lengthy credit card applications or complex financial calculations. This creates a smoother and more convenient shopping experience, which can lead to higher consumer satisfaction and brand loyalty. Additionally, the transparent payment structure of BNPL apps fosters trust and reduces anxieties associated with traditional financing methods.

Inclusive Credit Access

BNPL apps often have less stringent eligibility requirements than traditional credit cards. This opens the door for a wider range of consumers to access financing options, including those with limited credit history or those who are rebuilding their credit score. This financial inclusion fosters a more equitable marketplace and empowers a broader demographic to participate in the consumer economy.

Benefits for Merchants

Businesses that embrace BNPL options can see significant advantages. Studies suggest that BNPL can reduce shopping cart abandonment numbers, as customers are more likely to complete purchases if they can spread out the cost. Additionally, BNPL can attract new customers who prefer the flexibility and control offered by installment payments. This translates to increased sales volume and potentially higher average order values for merchants who integrate BNPL into their payment ecosystem.

Why Should You Invest in Developing a BNPL App?

Here’s a closer look at the key benefits that make BNPL app development a strategic investment:

01 Exploding Market

The BNPL market is experiencing explosive growth. Consumers are increasingly seeking flexible payment solutions, and a BNPL app allows you to capitalize on this surging demand. By entering the market early, you can establish a strong foothold and get a significant share of potential customers.

02 Building a Loyal Customer Base

Offering BNPL options broadens your customer reach by attracting individuals who might not qualify for traditional credit cards. This flexibility fosters customer loyalty, as users appreciate the convenience and control of spreading out payments. They’re more likely to return for future purchases if BNPL is available.

03 Boosting Sales and Order Value

BNPL can be a powerful sales driver. When customers break down larger purchases into manageable installments, they’re more likely to complete transactions and spend more. This translates to increased sales volume and higher average order values, boosting your overall revenue potential.

04 Standing Out from the Crowd

In a crowded marketplace, offering BNPL services can be a major differentiator. It sets your business apart from competitors who lack flexible payment options. This can significantly enhance your brand’s appeal and attract new customers seeking convenient and budget-friendly shopping experiences.

05 Multiple Revenue Streams

BNPL apps offer diverse revenue generation opportunities. You can earn income through merchant fees, late payment penalties, and potentially interest on longer-term installment plans. This creates a sustainable and profitable business model that fuels long-term growth.

What Is Wisetack And How Does It Generate Revenue?

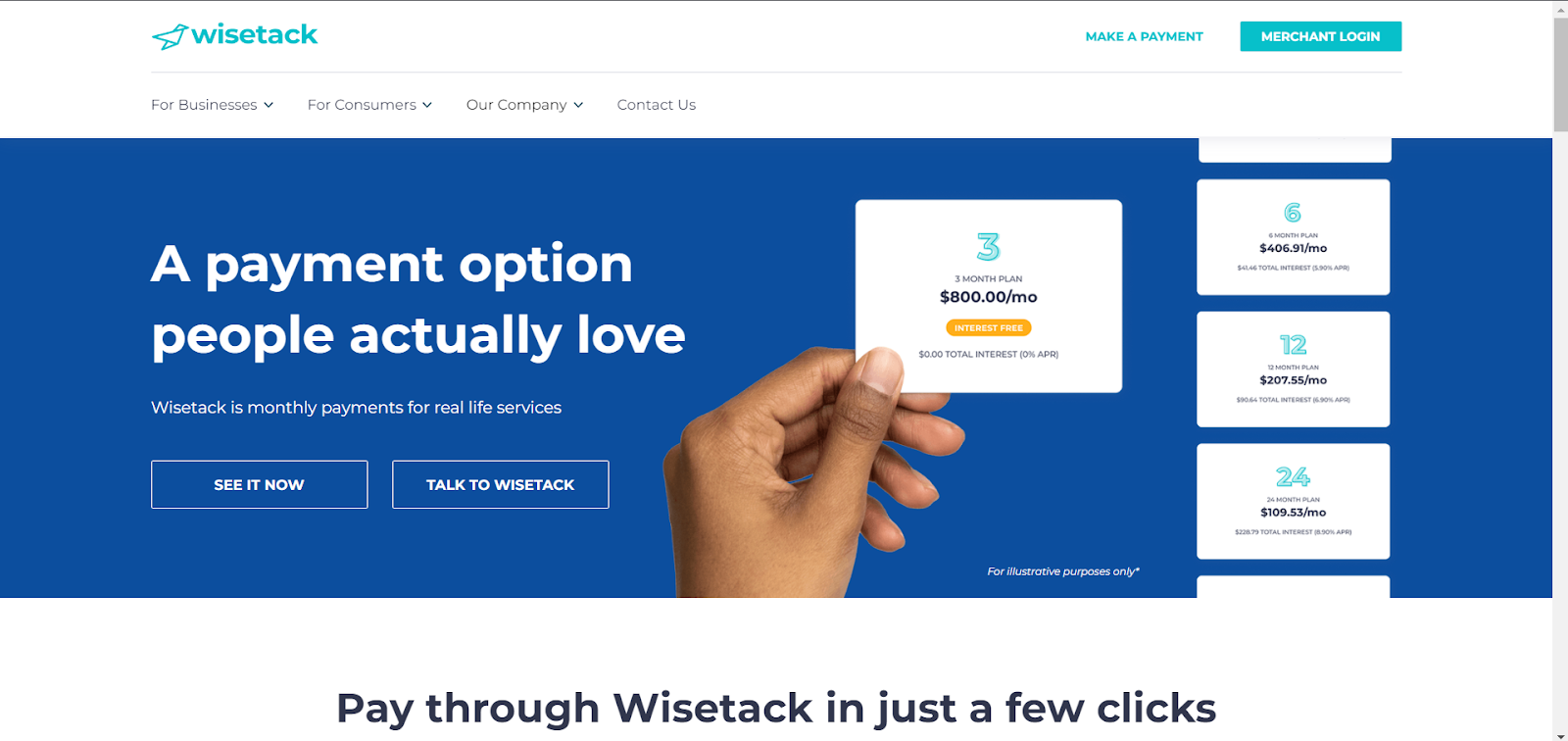

Wisetack is a financial technology company that offers Buy Now, Pay Later (BNPL) solutions tailored specifically for service-based businesses, such as home improvement, auto repair, and healthcare.

Unlike many BNPL providers that focus primarily on retail and e-commerce, Wisetack enables service providers (home improvement, auto repair, healthcare, and professional services) to offer their customers flexible financing options at the point of service. This allows customers to spread the cost of significant expenses over time, making it easier to manage their finances without the burden of immediate, large payments.

How Wisetack Generates Revenue

Wisetack generates revenue through several key streams:

Merchant Fees

One of the primary ways Wisetack earns revenue is by charging service providers (merchants) a fee for each transaction processed through their platform. These fees are usually a percentage of the transaction amount and compensate Wisetack for facilitating the financing option.

Interest Fees

Depending on the specific financing plan and the customer’s creditworthiness, Wisetack may charge interest on the installment payments. This interest is paid by the consumers who choose to finance their purchases over a longer period. The interest rates are competitive and tailored to the consumer’s credit profile.

Partnerships and Integrations

Wisetack partners with various platforms and service providers to integrate its financing solutions directly into their payment systems. These partnerships can generate additional revenue through integration fees or shared revenue agreements based on the volume of transactions processed through these integrated systems.

Late Fees and Penalties

While Wisetack emphasizes transparency and aims to minimize hidden fees, there might be instances where late fees or penalties are applied if customers fail to make their installment payments on time. However, this is usually a smaller portion of their revenue stream compared to merchant fees and interest charges.

What Are The Key Features That Make Wisestack Stand Out?

While general BNPL apps have paved the way for flexible financing, some limitations hinder their integration into specific sectors like in-person services. Here’s how Wisetack’s unique features address these shortcomings and sands out in the market:

Integration with Service-Based Businesses

Wisetack distinguishes itself in the Buy Now, Pay Later (BNPL) market by specializing in integration with service-based businesses in areas such as home improvement, auto repair, and healthcare. This focus allows service providers to offer financing options directly to their customers at the point of service, unlike many BNPL providers that primarily target retail and e-commerce.

Most BNPL platforms, such as Afterpay and Klarna, cater predominantly to online and in-store retail purchases, with a limited focus on service-based sectors. This specialization gives Wisetack a unique edge in the market.

Flexible Payment Plans

In addition to its service-oriented approach, Wisetack offers flexible payment plans which can be personalized to the needs of the service industry, with terms ranging from 3 to 60 months. This flexibility is crucial for consumers who need to manage larger expenses over time.

In contrast, many BNPL providers like Affirm and Sezzle typically offer shorter repayment periods, often up to 12 months, which might not be suitable for larger, service-based expenses. This extended flexibility makes Wisetack more appealing for financing for high-ticket items.

Transparent Pricing

Moreover, Wisetack emphasizes transparency with no hidden fees, late fees, or prepayment penalties. Customers are provided with clear terms and conditions upfront and have the option to view real-time financing options at the point of sale, making it user-friendly and enhancing trust and satisfaction.

While transparency is increasingly valued in the BNPL market, not all providers refrain from charging late fees or maintaining clear terms, which can result in unforeseen costs for consumers. Wisetack stands out by prioritizing clear and honest pricing, aiming to enhance customer awareness and financial transparency compared to competitors.

Easy Integration For Merchants

Furthermore, Wisetack offers a seamless integration process for merchants, supporting both online and in-person transactions. Their platform is designed to be easy for service providers to implement without extensive technical expertise. In comparison, the integration complexity can vary widely among BNPL providers.

For instance, while Klarna offers robust integration tools for e-commerce, they might be more complex to implement for smaller businesses or service providers. Wisetack’s user-friendly integration ensures broader accessibility and adoption among service-based merchants.

Focus on High-Ticket Items

Wisetack also specializes in financing high-ticket items and services, typically ranging from a few hundred to several thousand dollars. This focus helps consumers manage significant, one-time expenses.

On the other hand, many BNPL solutions are geared towards lower-cost consumer goods, with average transaction values typically under $1,000. By concentrating on high-ticket items, Wisetack addresses a niche market that other BNPL providers often overlook.

Merchant Support and Training

Additionally, Wisetack provides comprehensive support and training for merchants, helping them understand how to offer and manage financing options effectively. This support includes marketing materials and customer service training.

While some BNPL providers offer merchant support, the depth and focus on training and education can vary, with less emphasis on service-oriented businesses. Wisetack’s commitment to merchant support ensures that service providers can maximize the benefits of offering BNPL options to their customers.

Credit Options and Approvals

Finally, Wisetack utilizes a soft credit check process to assess consumer eligibility, which doesn’t impact credit scores and offers competitive APRs tailored to different credit profiles. This process aims to approve a wide range of consumers, making financing more accessible.

Other BNPL providers, like Affirm, also use soft credit checks, but approval rates and terms can vary significantly. Some may have stricter credit requirements or higher interest rates, affecting accessibility for consumers with varied credit histories. Wisetack’s balanced approach to credit options and approvals ensures inclusivity and broad appeal.

Essential Features To Consider in a BNPL Financing App Like Wisetack

By implementing these features and focusing on the specific needs of the in-person service industry, you can create a BNPL app that stands out from the competition.

User-Friendly Interface and Onboarding

First and foremost, a clean, intuitive UI is crucial for both consumers and service providers. The onboarding process should be quick and straightforward, minimizing friction for new users. This can involve features like clear navigation, one-click sign-ups, and pre-populated forms based on existing user data (where applicable, with consent).

Seamless Integration with Service Provider Systems

Moving on to functionality, the app should integrate smoothly with existing software used by service providers (e.g., appointment scheduling invoicing). This removes manual data entry and improves the BNPL experience. Consider offering pre-built integrations with popular platforms or an open API that allows for custom development by service providers with unique software needs.

Flexible Payment Plan Options

To serve a wider audience, offer a variety of BNPL plan options. This ensures you can accommodate different purchase sizes and consumer preferences. Consider interest-free installments for shorter terms and interest-bearing options for larger transactions. You can also explore features like early payment discounts or the ability to combine BNPL financing with loyalty programs or other promotions offered by service providers.

Secure Transactions and Data Protection

Security is paramount. Robust security features are essential to ensure user trust. Implement industry-standard encryption protocols and comply with relevant data privacy regulations. Additionally, consider offering features like two-factor authentication and in-app security settings to empower users to control their financial information.

Real-Time Credit Assessment and Approvals

Next, to ensure a smooth user experience, quick and efficient credit assessment allows for instant approvals or denials, minimizing wait times for both consumers and service providers. This can involve leveraging alternative data sources beyond conventional credit scores to provide a more holistic view of a consumer’s creditworthiness, particularly for those with limited credit history.

Transparent Fee Structure

Building trust is key. Clearly display all fees associated with BNPL transactions, including late payment penalties and potential interest charges. This fosters trust and avoids surprises for users. Consider offering fee calculators or simulations that allow users to see the total cost of financing before committing to a plan.

User Accounts and Transaction Management

Empower your users. They should have access to secure accounts where they can track spending, manage payment plans, and update personal information. Additional features like budgeting tools, spending notifications, and the ability to easily contact customer support can further enhance the user experience.

Communication and Customer Support

Excellent customer service is essential. Offer clear and accessible communication channels for both consumers and service providers. A multi-channel approach that includes in-app chat, email support, and phone helplines ensures users can get the assistance they need in their preferred format. Responsive customer support that resolves issues promptly is essential for building trust and user satisfaction.

Educational Resources

Inform your users. Integrate educational resources within the app to explain BNPL concepts, responsible credit use, and potential benefits and drawbacks. This can involve explainer videos, FAQs, or blog posts within the app that provide users with the information they need to make informed financial decisions.

Data Analytics and Reporting

Finally, empower your service providers. Provide them with insightful data and reports on BNPL transactions. This allows them to track trends, understand customer behavior (e.g., popular service categories financed through BNPL), and optimize their BNPL offerings. Consider features that allow for custom report generation and data visualization tools to empower service providers to make data-driven decisions about their BNPL strategy.

Steps to Develop a BNPL App Like Wisetack

Wisetack has carved a niche by focusing on in-person services. If you’re looking to develop a similar app, here’s a roadmap to guide you through the process:

01 Targeted Research & Competitive Analysis

Before you begin building, conduct thorough market research. Understand the current BNPL landscape, particularly within service industries. Identify your target audience (consumers and service providers) and their specific needs and challenges.

Next, carefully analyze existing BNPL apps, especially those like Wisetack. Learn from their successes and identify gaps in the market where your app can offer a unique value proposition.

02 Concept & Feature Prioritization

Once you have a clear understanding of the market, refine your app’s concept by clearly defining its niche. How will your app specifically address the needs of in-person service providers and their customers? Based on your research and target audience, prioritize the features your app will offer.

Use the ” Essential Features” list we explored previously as a foundation, but also consider features that enhance user experience, streamline BNPL integration for service providers, and provide valuable data insights.

03 User-Centric Design & Development

Moving into development, prioritize a user-friendly and intuitive interface (UI) for both consumers and service providers. The app should be easy to use and understand, minimizing friction during onboarding and transaction processes.

When selecting your tech stack, choose a robust set of technologies that can handle secure financial transactions, real-time data processing, and seamless integration with existing service provider software. Consider factors like scalability, security, and compliance with relevant regulations.

04 Rigorous Testing & Security

Before launch, rigorously test your app across various devices and operating systems to ensure functionality, security, and a smooth user experience. Conduct in-house testing and consider user testing with target audiences to gather valuable feedback.

Security is paramount. Enforce strict security measures to protect user data and financial information. This includes encryption protocols, secure authentication methods, and compliance with data privacy regulations.

05 Strategic Launch & Marketing

To gain traction, develop a comprehensive go-to-market strategy for launching your app. This includes establishing partnerships with service providers, marketing campaigns targeting consumers, and establishing a strong brand presence.

To build a user base, attract both consumers and service providers to your app. Consider offering incentives for early adopters and developing partnerships with industry associations or service provider platforms to reach a wider audience.

06 Regulatory Compliance & Payment Processing

Ensure your app operates within the legal regulations. Comply with all relevant financial regulations in your target markets. This may involve obtaining necessary licenses and adhering to data privacy laws. Partner with a reliable payment processor to handle BNPL transactions securely and efficiently. Consider factors like transaction fees, settlement times, and global reach.

07 Scalability for Future Growth

Design your app with the future in mind. As your user base rises, your app should be able to handle more transaction volumes and maintain performance. This means building with scalability in mind from the very beginning.

What Is the Cost of Developing a BNPL App Like Wisetack?

The exact cost of developing a BNPL app like Wisetack can vary depending on several factors, but here’s a breakdown to give you a ballpark estimate:

| Feature/Category | Basic App ($50,000 – $100,000) | Medium Complexity App ($100,000 – $200,000) | Advanced App ($200,000+) |

| Core Features | $15,000 – $30,000 | $30,000 – $60,000 | $60,000+ |

| User Interface (UI)/User Experience (UX) | $5,000 – $15,000 | $15,000 – $30,000 | $30,000+ |

| Security | $5,000 – $10,000 | $10,000 – $20,000 | $20,000+ |

| Integration | $5,000 – $10,000 | $10,000 – $20,000 | $20,000+ |

| Compliance | $5,000 – $10,000 | $10,000 – $20,000 | $20,000+ |

| Analytics and Reporting | $3,000 – $8,000 | $8,000 – $15,000 | $15,000+ |

| Scalability | $3,000 – $8,000 | $8,000 – $15,000 | $15,000+ |

| Support and Maintenance | $3,000 – $8,000 | $8,000 – $15,000 | $15,000+ |

| Additional Features | – | $5,000 – $10,000 | $10,000+ |

| Total Estimated Cost Range | $50,000 – $100,000 | $100,000 – $200,000 | $200,000+ |

Basic App

$50,000 to $100,000.

This would cover essential features such as user registration, payment gateway integration, basic loan management, repayment schedules, basic notifications, and customer support. The design would be functional but not highly customized.

Medium Complexity App

$100,000 to $200,000.

This level includes all basic features but with more advanced functionalities such as credit score assessment, enhanced security features, integration with third-party financial services or credit bureaus, more sophisticated notifications, and some basic analytics capabilities. The UI/UX design would be more refined to enhance user experience.

Advanced App

$200,000+

An advanced BNPL app would include all features from the previous levels but with additional complex features such as advanced analytics and reporting, comprehensive fraud detection systems, robust compliance with financial regulations (PCI-DSS, GDPR, etc.), highly customized UI/UX design for optimal user engagement, scalability for handling large volumes of transactions, and integration with multiple payment gateways or financial institutions.

Cost Affecting Factors

App Complexity

A basic BNPL app with core functionalities will cost less than a feature-rich app with functionalities like advanced fraud detection, creditworthiness assessments, or loyalty program integrations. Wisetack focuses on a specific niche (in-person services) but offers a variety of features to cater to both consumers and service providers. This complexity will likely place it on the higher end of the cost spectrum.

App Development Platform

Choosing between native app development (separate apps for iOS and Android) or a cross-platform approach (single codebase for both) impacts cost. Native development generally offers a more customized user experience but can be more expensive. Cross-platform development can be more cost-effective but might have constraints in terms of functionality and user experience.

Development Team Location

The location of your development team notably affects cost. Hiring developers in America or Western Europe typically commands higher rates compared to hiring teams in South Asia or Eastern Europe.

In-House vs. Outsourced Development

Developing the app in-house gives you more control but requires hiring and managing a development team. Outsourcing the project to a development agency can be more cost-effective but necessitates clear communication and project management to ensure your vision is realized.

How Does a BNPL App Generate Revenue?

BNPL apps like Wisetack generate revenue through several key channels:

Merchant Fees

This is the primary revenue stream for most BNPL apps. Businesses that offer BNPL options as a payment method pay a fee to the BNPL app provider for each transaction processed. This fee can be a fixed amount per transaction or a percentage of the purchase value. For example, Wisetack might charge service providers a fee of 3% for each BNPL transaction completed through their platform.

Late Payment Fees

Consumers who miss BNPL payment deadlines are typically charged late fees. These fees incentivize timely payments and generate additional revenue for the BNPL app. The specific late fee structure will vary depending on the app and regulations in the target market.

Interest on Longer-Term Plans

Some BNPL apps offer extended payment plans with interest charges. This can be particularly relevant for larger transactions financed through the app. Wisetack might offer interest-free financing for shorter terms but could potentially charge interest on longer-term BNPL loans for in-person services.

Premium Features

Some BNPL apps offer premium features to both consumers and businesses for an additional subscription fee. For consumers, this could include features like credit score monitoring or priority access to promotions. Businesses might pay for premium features like advanced analytics or marketing tools within the BNPL platform.

Data Insights

The data collected from user transactions can be valuable for businesses. BNPL apps might offer anonymized data insights or analytics tools (for a fee) to service providers, allowing them to understand customer behavior and optimize their BNPL offerings.

The specific revenue mix for a BNPL app like Wisetack will depend on its fee structure, target market, and the types of financing plans it offers. However, by focusing on these core revenue streams, BNPL apps can generate sustainable profits while providing a convenient payment solution for both consumers and businesses.

Innovative Trends in BNPL App Development

The BNPL market is growing rapidly, and developers are looking for ways to improve these apps. Here are five key technology trends that could impact BNPL apps in the future:

Open Banking Integration

This allows BNPL apps to access a user’s financial data from banks with the user’s permission. This data can be used to assess creditworthiness more fairly, create personalized payment plans, and even offer automated savings tools.

By looking at more than just credit scores, BNPL apps could reach more users and offer more inclusive financing options. Open Banking data can also be used to tailor payment plans to a user’s situation, with features like flexible repayment terms or automated savings to help users meet their obligations.

AI and Machine Learning

These technologies are changing BNPL. AI algorithms can interpret user behavior to identify and prevent fraud, making the system more secure. They can also personalize the experience by recommending relevant promotions or loyalty rewards based on spending habits. Additionally, AI-powered chatbots can provide customer support 24/7, answer user questions, and help users manage their accounts.

Biometric Authentication

Fingerprint or facial recognition can offer a secure and convenient way to access BNPL accounts and approve transactions. This eliminates the need for passwords, making it easier for users and easing the risk of unauthorized access.

Blockchain

This technology is still new in BNPL, but it has the potential to disrupt the industry. Blockchain can build a secure and transparent record of transactions, which could reduce fraud and make it easier to resolve disputes. It could also enable peer-to-peer BNPL financing models, bypassing traditional institutions and offering more competitive rates for consumers.

Embedded Finance

Integrating BNPL features within existing apps and platforms can significantly expand their reach. Imagine being able to access BNPL options directly within a service provider’s app, like financing a home repair without needing separate apps. This would streamline the purchase process for customers. Embedded finance also benefits businesses by allowing them to easily integrate BNPL options without developing their infrastructure, potentially boosting sales through wider adoption.

Conclusion

Developing a BNPL app like Wisetack requires careful planning and various considerations. The total cost can vary depending on the app’s complexity, development approach, and chosen team location. But by focusing on essential features like user-friendly interfaces, seamless service provider integrations, and security, you can create a competitive BNPL solution.

Remember that ongoing maintenance and updates are crucial for a successful app. Partnering with experienced BNPL app development companies can ensure you get a clear cost estimate and a solution tailored to your specific needs. By thoughtfully navigating the development process and keeping user experience a priority, you can create a BNPL app that thrives in this rapidly growing market.

How Can Idea Usher Assist You in Developing Your BNPL App?

Entering the BNPL market is exciting, but navigating development complexities can be daunting. Idea Usher is your one-stop shop for building a winning BNPL app.

We’ll collaborate to refine your concept, identify your niche, and prioritize features that cater to both consumers and service providers. Our team of experts tackles seamless integration with existing service provider systems while choosing a secure and scalable tech stack for future growth. Don’t compromise on user experience – our design team will craft an intuitive interface for a smooth journey.

Partner with Idea Usher and turn your BNPL vision into reality.

Contact Us today for a free consultation!

FAQs

Can BNPL be profitable?

BNPL platforms can be profitable through various revenue streams, including transaction fees charged to merchants, interest fees from customers choosing extended repayment plans, and partnerships with financial institutions. Profitability depends on efficient risk management, scalability, and customer acquisition strategies.

Is BNPL a good business model?

Buy Now, Pay Later (BNPL) has gained popularity due to its convenience and ease for consumers. It allows customers to make purchases and pay for them in installments over time, often without interest. For businesses, BNPL can increase sales by reducing customer upfront cost barriers. However, it requires careful management of credit risk and adherence to regulatory standards. Overall, BNPL can be a profitable business model if implemented effectively with a focus on customer experience and risk management.

How to build a BNPL platform?

Building a successful BNPL platform involves meticulous planning and execution. It begins with market research to understand consumer preferences and competitive landscapes. Developing a robust technology infrastructure is crucial, encompassing secure payment processing, user-friendly interfaces, and scalable backend systems to handle transaction volumes efficiently. Strategic partnerships with payment processors, financial institutions, and merchants are also essential to broaden service reach and ensure seamless integration into the shopping experience.

What is the future outlook for BNPL?

The future of BNPL looks promising as consumer requirements for flexible payment options continue to grow. However, the industry faces challenges such as regulatory scrutiny and competition. Innovations in technology, improved credit risk assessment, and expansion into new markets are expected to drive growth. Successful BNPL providers will likely focus on enhancing user experience, promoting financial literacy, and maintaining robust risk management practices.