(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Every few months, a DeFi protocol faces an exploit, and people start wondering what could have protected their assets. Most users love the freedom and rewards of DeFi, but they rarely think about safety. This makes the space exciting yet sometimes risky. A DeFi insurance aggregator might bridge that gap by helping users explore protection without hassle. DeFi insurance should not only cover losses but also rebuild confidence in the system. OpenCover shows how this can work with features such as real-time premium tracking and multi-protocol coverage discovery. It also offers quick policy comparisons that make decisions easier for every user.

We’ve spent years working with fintech startups and Web3 enterprises, and have developed several decentralized insurance and risk management products powered by technologies such as smart contract engineering and DeFi protocol integration frameworks. As we have this expertise, we’re writing this blog to walk you through the steps to build a DeFi insurance aggregator like OpenCover. You will see how its architecture and protocols work and how you can design an experience that feels simple yet secure.

Key Market Takeaways for DeFi Insurance Aggregators

According to AlliedMarketResearch, the decentralized insurance market is expanding at a remarkable pace, surging from $1.4 billion in 2022 to a projected $135.6 billion by 2032. This rapid growth reflects rising adoption of DeFi platforms, wider use of smart contracts, and a stronger focus on managing protocol risk. Users are seeking insurance options that are transparent, cost-effective, and built to match the decentralized nature of the ecosystem.

Source: AlliedMarketResearch

DeFi insurance aggregators are stepping in to simplify this landscape by letting users compare and purchase coverage from multiple providers in one place. Bright Union and ArmorFi lead this charge.

Bright Union aggregates protection from over 150 protocols, offering coverage for hacks, de-pegs, and contract failures. ArmorFi’s arCORE aggregator, meanwhile, provides flexible, pay-as-you-go coverage that appeals to active traders who need adaptable protection.

A standout example of collaboration in the space is the Uno Re–Nexus Mutual partnership. Their 50% quota-share agreement combines risk capacity and premium sharing to strengthen decentralized underwriting. This partnership highlights a growing shift toward cooperative models that make DeFi insurance more scalable, liquid, and resilient for users and institutions alike.

Why DeFi’s $55B Locked Assets Need Insurance Aggregators?

DeFi has created one of the boldest financial systems ever built. It holds around $55 billion in digital value that moves freely without middlemen. Yet this freedom also makes it fragile because every transaction runs on code, and that code can fail. If DeFi wants to last, it must become stronger and more reliable. That is why it should now embrace insurance aggregators as the next layer of protection and trust.

The Protection Gap: DeFi’s Hidden Systemic Risk

Traditional finance runs on safety nets. The FDIC insures your bank deposits. Your investments are regulated. Even your credit card comes with fraud protection.

In DeFi, none of that exists. “Code is law,” and when that law breaks, users bear the loss.

Out of the $55 billion locked across DeFi platforms, only a few hundred million dollars are insured, leaving over 99% of total value unprotected.

This gap is not just a personal risk; it is a systemic threat. One major exploit without insurance could ripple through the ecosystem, destroy liquidity, and collapse confidence overnight.

Insurance aggregators can change this. By pooling coverage options across multiple providers and protocols, they make protection scalable, transparent, and accessible to every participant in the network.

Where the $55 Billion Is Most at Risk?

These vulnerabilities are not theoretical. They are chronic, documented, and expensive.

1. Smart Contract Risk

Bugs in smart contracts can turn into massive losses very quickly. Even a small coding error might open a door for hackers to steal millions within minutes. The Wormhole bridge exploit is one such case, where a vulnerability resulted in a $326 million loss.

2. Economic or Design Risk

Sometimes the danger lies in the system’s design rather than its code. When the economic model fails, the entire protocol can collapse. Terra’s UST meltdown showed this clearly as an algorithmic design flaw erased around $18 billion in value.

3. Oracle Manipulation

DeFi protocols often depend on oracles to provide price data, and when those feeds are manipulated, attackers can profit easily. The Mango Markets exploit is a clear example, where false price inputs allowed a user to drain $116 million.

4. Governance Attacks

In systems driven by governance tokens, control can shift into the wrong hands if someone gains enough voting power. Once that happens, they can alter rules or redirect funds, turning a community-driven project into a personal payout.

Why Insurance Aggregators Are the Safety Layer DeFi Needs?

For DeFi to grow from a niche experiment into a global financial system, it must earn trust, and trust comes from protection. Insurance aggregators make that protection possible at scale.

For Retail Users

Aggregators transform insurance from a luxury into a utility. Instead of manually comparing coverage across multiple protocols, users can access unified dashboards that quote, price, and manage all insurance in one place. This lowers friction and gives every participant the confidence to invest safely.

For Institutions

Institutional capital will not flow into uninsured ecosystems. Insurance aggregators create standardized, auditable coverage that meets fiduciary and compliance requirements, unlocking billions in potential inflows from funds, treasuries, and enterprises.

For the Ecosystem

Aggregators stabilize the market by spreading risk across diverse insurance pools. When an exploit hits, losses are absorbed collectively rather than devastating a single protocol. The result is systemic resilience, preserved confidence, and sustainable growth.

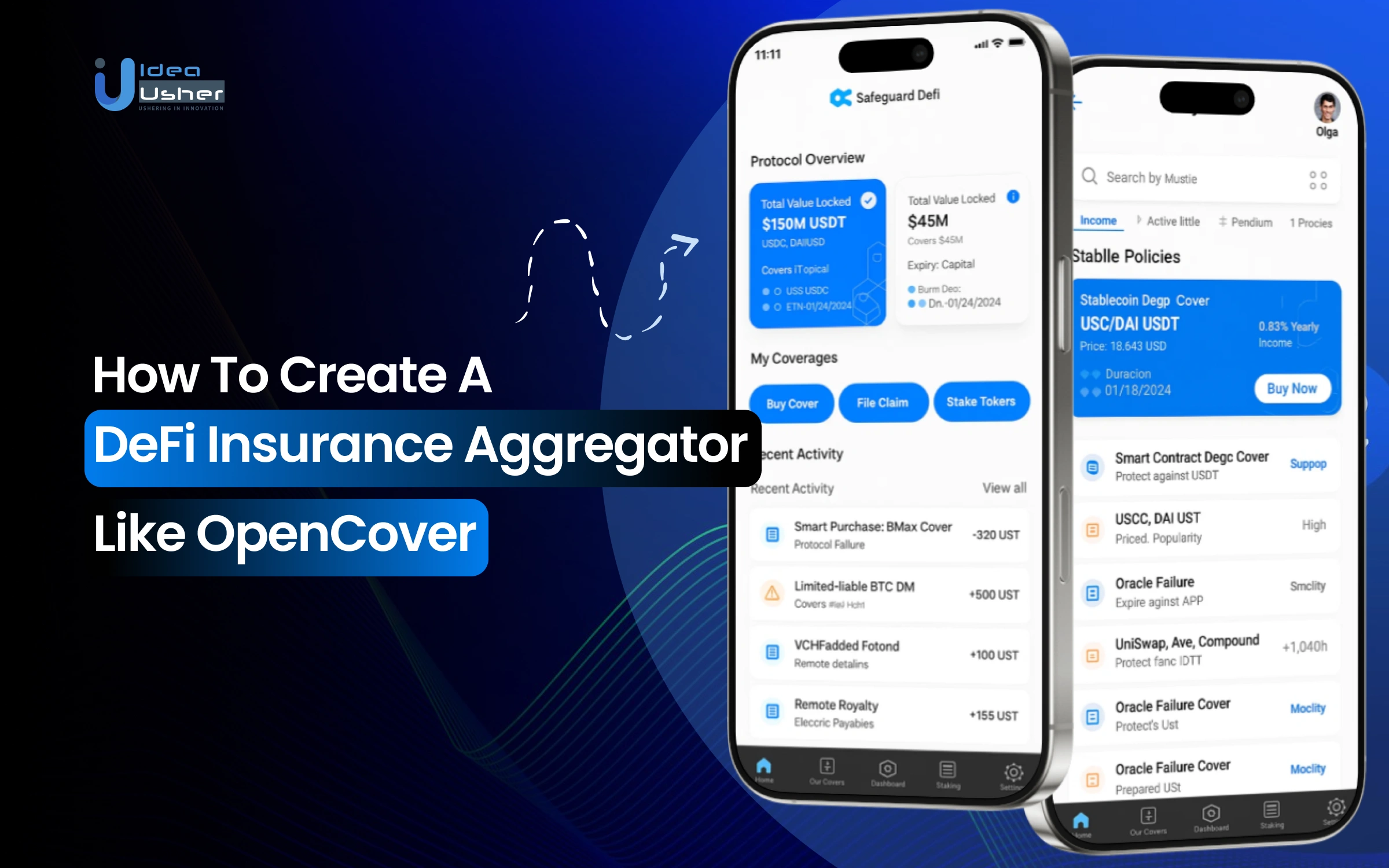

What is the OpenCover Platform?

OpenCover is a DeFi insurance platform designed to protect users’ on-chain portfolios against major risks, including protocol hacks, smart contract bugs, oracle failures, and governance exploits. It provides coverage across more than 100 DeFi protocols and multiple blockchains, giving both individual and institutional users a simple way to manage risk in an increasingly complex ecosystem.

By partnering with established underwriters, OpenCover offers affordable, transparent, and easily accessible protection. Coverage starts from just $2 per week for $5,000 in protection, making it one of the most approachable options for everyday DeFi participants.

Every policy is issued as an ERC-721 NFT, providing users with a verifiable, on-chain proof of coverage that they can easily manage, renew, or transfer.

Some of its standout features are.

Cross-Chain and Multi-Protocol Coverage

OpenCover protects assets across numerous protocols and blockchains, making it ideal for users with diversified DeFi portfolios. This cross-chain design ensures seamless protection even as users move between ecosystems.

Affordable Pricing

With entry-level policies starting at just $2 per week for $5,000 in coverage, OpenCover lowers the barrier to entry for risk management, making DeFi insurance accessible to a global audience.

ERC-721 Proof of Cover

Each policy is represented as an ERC-721 NFT, offering transparent ownership and easy on-chain management. Users can view, renew, or transfer their coverage without relying on intermediaries.

Extensive Protocol Support

The platform currently supports over 100 DeFi protocols, providing coverage for both well-established platforms and emerging ones. This broad scope helps users safeguard their assets wherever they participate in DeFi.

Simple User Experience

OpenCover’s interface is built for ease of use. Users can purchase, renew, or manage their coverage in a few clicks through the web app. For institutions and developers, OpenCover also provides API integrations to automate insurance purchases at scale.

Strong Backing and Ecosystem Integration

The platform is supported by leading crypto investors and integrated with major ecosystems such as Base. Its network of partners includes DeFi accelerators, venture firms, and ecosystem collaborators that help strengthen its reach and credibility.

How Does the OpenCover Platform Work?

OpenCover simplifies decentralized insurance by unifying a complex ecosystem into one intuitive interface. It allows users to discover, purchase, and manage on-chain insurance coverage across multiple protocols and blockchains, all in one place.

Here’s how it works.

Step 1: The Unified Quote Engine

When users visit OpenCover, they are greeted with a single, streamlined interface rather than a maze of separate insurance platforms.

User Input: Users choose what they want to protect, such as an Aave deposit on Arbitrum, along with the coverage amount and duration.

Behind the Scenes:

- Once users click “Get Quote”, OpenCover’s backend instantly begins aggregating data.

It queries several trusted on-chain insurance providers, including protocols like Nexus Mutual, across multiple blockchains. - It normalizes the diverse pricing models, terms, and parameters offered by these providers through a powerful data aggregation layer.

- Within milliseconds, OpenCover delivers a single, transparent quote or a set of options, ensuring users receive optimal coverage at the best available price.

The result is a seamless experience that hides the fragmented nature of DeFi insurance behind a unified interface.

Step 2: Policy Issuance as an NFT

OpenCover transforms the way users hold and interact with their coverage.

The Purchase: After users confirm their chosen policy and pay the premium, OpenCover processes the transaction on-chain.

The Innovation: Tokenized Coverage

Instead of issuing a receipt or a fungible token, OpenCover’s smart contracts mint a unique ERC-721 NFT and send it directly to the user’s wallet. This NFT functions as the Proof of Cover.

Why It Matters:

- Proof of Ownership: The NFT serves as a verifiable, on-chain record of the user’s insurance policy.

- Composability: As a standard NFT, it integrates seamlessly into the broader DeFi ecosystem. Users can display it alongside other assets, transfer it, sell it if coverage is no longer needed, or potentially use it as collateral in decentralized finance applications.

This approach turns a static insurance document into a flexible, living digital asset.

Step 3: The Claims Process

The claims process is where OpenCover’s design truly shines, removing the stress and confusion that usually accompany insurance claims.

Filing a Claim: If a covered event occurs, such as a protocol exploit, users can initiate a claim directly through OpenCover’s interface using their Policy NFT.

Behind the Scenes:

OpenCover itself does not adjudicate claims; it acts as a router.

- The system reads the NFT’s metadata to identify the underlying insurance protocol that issued the policy.

- It then forwards the claim to that protocol’s own claims process, such as Nexus Mutual’s assessment system.

- OpenCover provides a unified tracking dashboard, allowing users to monitor claim progress in one place rather than juggling multiple protocol interfaces.

Payout: Once the underlying provider approves the claim, the payout is released directly to the wallet holding the Policy NFT.

What is the Business Model of the OpenCover Platform?

OpenCover’s business model is built on recurring premium income, which serves as its primary and most predictable source of revenue. By leveraging a SaaS-style subscription infrastructure for premium collection, the platform generates steady and recurring cash flow that grows with user adoption.

Additional revenue sources include:

- Underwriter Partnerships: Revenue sharing or commission-based arrangements with insurance underwriters providing coverage capacity.

- B2B Integrations: Offering an insurance API and risk analytics tools for DeFi projects, centralized exchanges, and liquidity platforms that seek embedded protection features.

- Data Monetization: Potential use of anonymized policy and claims data to inform underwriters and institutional partners about market risk trends.

- Embedded Finance Products: Cross-chain premium payments and embedded coverage options for partner ecosystems such as Base and Optimism expand the platform’s monetization opportunities.

Financial Position and Growth

OpenCover has raised approximately $4 to $4.6 million in seed funding, with a major $4 million round completed in September 2023. Its backers include Jump Crypto, NFX, Alliance DAO, OrangeDAO, Village Global, and the Base Ecosystem Fund, which reflects strong investor confidence in decentralized risk markets.

Although FY 2023 revenue remained minimal, the company is still in its growth and network-building phase, which is typical for early-stage insurtech ventures. Recent performance indicators, such as a 3-point increase in its Mosaic Score, demonstrate improving investor sentiment and operational progress as the platform expands its premium pool and customer base.

How to Develop a DeFi Insurance Aggregator Like OpenCover?

We have developed numerous DeFi insurance aggregators like OpenCover that help users compare and manage decentralized coverage with ease. Our team focuses on building scalable systems that actually work across protocols. You will see how seamlessly our platforms connect users to real, transparent, and reliable DeFi protection.

1. Design Aggregator Architecture

We begin by defining the aggregation model, whether price-based, liquidity-based, or hybrid, to match client goals. Our team integrates leading protocols such as Nexus Mutual, InsurAce, and Neptune Mutual. Smart contracts are structured modularly, covering the risk engine, claims logic, and NFT minting, ensuring flexibility and scalability.

2. Build Policy Tokenization Framework

We develop ERC-721 “Proof of Cover” NFTs that represent each user’s policy on-chain. These tokens include standardized metadata with policy details, coverage terms, and claim records. Using IPFS or Arweave, we ensure that all policy data is stored immutably and transparently.

3. Cross-Chain Communication Layer

To support multi-chain coverage, we integrate LayerZero or Axelar for seamless interoperability. We implement state-sync modules that keep policies updated across chains. An off-chain indexer is also built to minimize gas costs and maintain consistency across networks.

4. Risk Scoring & Pricing Engine

We build a risk assessment engine that aggregates DeFi data from DefiLlama, Token Terminal, and other analytics providers. This data feeds into our pricing algorithm, which dynamically adjusts premiums based on real-time protocol risk and market volatility.

5. Claims Management & Arbitration System

Our platform includes a claims submission dashboard for easy user access. We integrate adapters for various claim-resolution protocols and use Oracle-based verification, such as Chainlink, to automate and validate parametric claims securely.

6. Integrate Frontend & Business Layer

Finally, we create a clean, responsive frontend dashboard where users can browse and manage their coverage. The platform supports MetaMask, WalletConnect, and Coinbase Wallet. We also build in monetization models like commissions and premium spreads to drive revenue for our clients.

The Revenue Potential of a DeFi Insurance Aggregator

The DeFi insurance market, while nascent, presents a compelling revenue opportunity for aggregator platforms. To build a realistic financial model, we must look beyond theoretical totals and analyze the actual performance and metrics of existing players

Let’s analyze the revenue streams and build a bottom-up financial model, justified by the competitive landscape.

Primary Revenue Streams

- Aggregator Fee (Commission): The core revenue driver, typically 5% to 15% of the premium paid.

- Protocol Incentives & Partnerships: Payments from underwriters for directing liquidity and users.

- Treasury Yield: Revenue generated by deploying fee-based stablecoins into low-risk yield protocols.

This model estimates potential annual revenue for a new DeFi insurance aggregator platform using a bottom-up approach, anchored in data from active industry peers.

1. Competitive Landscape and Market Benchmarks

To ground assumptions, we reference leading platforms operating across different models:

Nexus Mutual (Incumbent / Carrier)

This platform holds over $200 M in its capital pool and has paid more than $10 M in claims. Its annual premium volume is consistently in the multi-million-dollar range, setting the upper bound for the market.

InsurAce Protocol (Aggregator + Carrier)

InsurAce Protocol has facilitated over $300 M in total coverage, with Total Value Protected (TVP) often in the tens of millions. It earns protocol fees from underwriting and aggregation, making it one of the more diversified models in the sector.

Bright Union (Pure Aggregator)

Bright Union has aggregated more than $150 M in cumulative coverage. Its real-time dashboard shows active premiums, giving visibility into current premium flow and confirming that aggregator-based revenue is meaningful but modest compared to carriers.

2. Defining Key Market Metrics

Total Addressable Market

Aggregating data from Nexus Mutual, InsurAce, Unslashed, and Bright Union suggests an annualized DeFi insurance premium pool between $50 M – $100 M.

A midpoint of $75 M provides a balanced baseline for modeling.

Target Market Share: For a well-executed new entrant with strong UX, innovative tokenomics, and curated integrations, capturing 2.5% of this market is ambitious yet credible.

Bright Union’s current scale supports this assumption.

Aggregator Commission Fee:

Industry commissions typically range from 5–15% of premium volume.

We apply a 7.5% rate — conservative and realistic.

3. Core Revenue Calculation

| Metric | Value |

| Total DeFi Insurance TAM | $75,000,000 |

| Target Market Share | 2.5% |

| Processed Premium Volume | $1,875,000 |

| Commission Rate | 7.5% |

| Annual Commission Revenue | $140,625 |

4. Ancillary Revenue Opportunities

Beyond commissions, platforms commonly earn incremental income through yield strategies, staking incentives, or integrations with liquidity providers.

Assuming ancillary revenue equals 15% of commission income: $140,625 × 15% = $21,094

Total Projected Annual Revenue: $140,625 + $21,094 = $161,719

Validation Against Existing Players

- Bright Union Comparison: With over $150 M cumulative coverage, Bright Union’s annual processed premium is likely in the low-million range. A 7.5% fee on $3 M would generate roughly $225 K/year, meaning our $161 K projection for a 2.5% share is conservative and consistent with real-world performance.

- InsurAce Benchmark: By combining underwriting and aggregation, InsurAce captures a larger share of each premium. Its $300 M+ in coverage supports multi-million-dollar annual revenues, confirming the scalability of this model.

- Nexus Mutual Ceiling: As the sector’s benchmark, Nexus’s multi-million annual premium flow sets the aspirational upper limit of what’s achievable once network effects and governance maturity take hold.

Scaling Path to $1M+ Annual Revenue

Two realistic growth scenarios illustrate how the model can expand:

Scenario A: Market Growth

If the DeFi insurance market expands to $250 M annually and the aggregator captures 5%, then:

- Processed Premium: $250 M × 5% = $12.5 M

- Commission (7.5%): $937,500

→ Nearly $1 M/year in recurring revenue, achievable through organic market growth.

Scenario B: Value-Added Services

Introducing proprietary vaults or structured covers, keeping ~50% of premiums on 20% of volume, would lift effective revenue share and push annual income well beyond $1 M even without major market expansion.

Challenges for a DeFi Insurance Aggregator Like OpenCover

The idea of a DeFi insurance aggregator is powerful. A single platform where users can access multiple cover options, compare prices, and secure protection for their on-chain assets could redefine how risk is managed in Web3. But turning this concept into a functional, secure product is far from simple.

At Idea Usher, after architecting multiple solutions in the DeFi insurance space, we have seen the recurring challenges that define these projects. Below is a breakdown of the most critical ones and how to solve them strategically.

1. Integration Fragmentation

The DeFi insurance ecosystem includes many protocols such as Nexus Mutual and InsurAce. Each uses its own smart contract logic, pricing model, and cover token standard.

These differences make integration a complex technical challenge instead of a simple API task. Building a unified system that can interpret and compare multiple protocols is one of the toughest problems in the space.

Our Proven Solution

Rather than writing fragile code for each protocol, we design a middleware layer that works as a universal translator.

- Custom Adapters: We create smart contract adapters that communicate directly with every integrated protocol, handling actions such as purchasing cover, renewing policies, and checking claim status.

- Canonical Cover Model: We normalize all incoming data into one unified policy format that represents any cover type, regardless of origin. This consistent data model simplifies the entire system and ensures smooth scalability.

2. Cross-Chain Data Synchronization

Users and underwriters often operate across several blockchains. Policies may be purchased on Ethereum, collateral may sit on Arbitrum, and claims may be processed on Base.

Keeping data synchronized across chains is complex. Without proper design, it can lead to latency, mismatched information, and expensive transaction costs.

Our Proven Solution

We use proven cross-chain technologies to create a seamless multi-chain experience.

- Interoperability Protocols: By integrating systems like LayerZero or Axelar, our smart contracts can securely verify events and trigger actions across different networks without the need to move capital unnecessarily.

- Off-Chain Indexers: For fast and responsive user experiences, we employ indexing solutions such as The Graph. This allows us to present real-time policy and claims data across chains without relying on slow or costly on-chain queries.

3. Regulatory Compliance

To achieve meaningful scale, a DeFi aggregator must attract institutional users and liquidity providers. These participants operate under strict compliance requirements such as KYC and AML. Completely ignoring regulation limits your growth potential, while over-centralizing control defeats the purpose of DeFi.

Our Proven Solution

We build optional compliance pathways that allow both retail and institutional participation.

- Optional KYC and AML Modules: Retail users can access coverage freely, while institutional users can verify their identity through decentralized identity systems such as Polygon ID. Verification can unlock access to higher coverage limits and exclusive underwriting pools.

- Compliant Gateways: This hybrid design supports both open participation and regulated access, making the platform suitable for a wider audience while remaining true to its decentralized principles.

4. Claims Dispute Resolution

The credibility of an insurance platform depends on how it handles claims. Many aggregators rely solely on the claims processes of underlying protocols, which can be inconsistent, slow, or subjective. When users feel claims are unfairly rejected, trust and adoption decline.

Our Proven Solution

We introduce a fair, transparent, and efficient dispute resolution process that builds user confidence.

- Oracle-Based Resolution: For straightforward, parametric claims such as stablecoin depegs, we use decentralized oracles like Chainlink to automate and verify payouts instantly.

- Arbitration DAO: For complex or subjective claims, we establish a community-driven DAO composed of security experts and token holders. This group reviews evidence, votes transparently, and ensures accountability throughout the process.

Tools & APIs Needed for a DeFi Insurance Aggregator

Creating a DeFi insurance aggregator such as OpenCover is a sophisticated engineering challenge. It requires an architecture that balances transparency, composability, and cross-chain functionality while maintaining user trust and security. The following sections outline the essential technologies and frameworks that enable such a platform.

1. Smart Contract & Blockchain Frameworks

Smart contracts form the backbone of a DeFi aggregator. They handle policy creation, premium collection, claim validation, and payouts in a transparent and tamper-resistant way.

Languages & Frameworks:

- Solidity: The dominant language for writing smart contracts on Ethereum and EVM-compatible chains like Arbitrum, Base, and Polygon.

- Hardhat / Foundry: Development environments that simplify compiling, testing, debugging, and deploying contracts. They are critical for maintaining code quality and performing local simulations before going live.

Libraries:

OpenZeppelin Contracts: A secure library of reusable, audited smart contracts. For a DeFi insurance aggregator, implementations of ERC-721 (for “Proof of Cover” NFTs) and robust access control patterns are invaluable. They reduce both audit overhead and potential attack surfaces.

2. Cross-Chain & Interoperability Tools

To stand out in today’s DeFi space, your coverage should work across several chains. You will need a secure way for smart contracts on different networks to talk to each other. Tools like LayerZero, Axelar, and Wormhole can reliably move data and value between chains so a claim on Arbitrum could instantly trigger a payout on Ethereum.

3. Data Feeds & Oracles

DeFi insurance often depends on real-world or on-chain events, from a stablecoin losing its peg to a protocol suffering an exploit. Oracles bring this external data on-chain in a verifiable way.

Providers:

- Chainlink and Pyth: Offer decentralized price and event feeds used in parametric insurance models. For instance, if a stablecoin depegs beyond a threshold, a Chainlink oracle can automatically trigger claim payouts.

- UMA Oracle: Useful for complex or subjective data verification, such as determining whether a hack occurred or a protocol was exploited. UMA’s dispute resolution system adds an extra layer of decentralized governance to claims arbitration.

4. DeFi Analytics & Integration APIs

An aggregator’s competitive edge lies in how effectively it sources and compares coverage options across the ecosystem. That requires real-time analytics and access to protocol-level data.

APIs & Tools:

- DeFiLlama API: Provides reliable data on metrics like Total Value Locked, which is essential for evaluating protocol risk exposure.

- Dune Analytics: Enables custom dashboards and SQL-like queries for on-chain data. It is ideal for tracking exploit histories, coverage performance, and market share among competing insurers.

5. Storage & Indexing

Blockchains are not designed to store large or complex datasets efficiently. Decentralized storage and indexing layers fill this gap, allowing applications to remain fast, cost-effective, and composable.

Solutions:

- IPFS / Arweave: Perfect for storing immutable metadata for policy NFTs, such as coverage details, policy documents, and terms.

- The Graph: A decentralized indexing protocol that enables fast, complex queries like “show all active policies for this user” or “calculate total active coverage per protocol.” This greatly improves user experience and backend performance.

6. Frontend & Wallet Integration

The interface is where all the blockchain complexity must disappear. A well-built frontend with seamless wallet integration determines whether users stay or leave.

Frontend Stack:

- React: The go-to framework for building interactive, component-based web apps.

- Ethers.js / Web3.js: Enable your frontend to interact directly with blockchain data and send transactions securely.

- Web3Modal / RainbowKit: Simplify wallet onboarding. With one integration, users can connect MetaMask, Coinbase Wallet, or WalletConnect in seconds, making DeFi insurance accessible to non-technical users.

Conclusion

The DeFi ecosystem is full of innovation but also carries real risks. That is why insurance aggregation is quickly becoming the next big step in creating true financial security. Platforms like OpenCover have already shown how tokenized policies and cross-chain coverage can make decentralized insurance both safer and more scalable.

With the right setup, strong integrations, and a solid risk model, any business could build its own DeFi insurance aggregator and open a new stream of revenue in Web3’s fastest-growing space. At Idea Usher, we understand how to turn complex DeFi ideas into practical products. Our team builds everything from cross-chain smart contracts to NFT-based policy systems, helping companies confidently launch the next generation of financial solutions.

Looking to Develop a DeFi Insurance Aggregator Like OpenCover?

DeFi insurance can feel like a maze. Users struggle with scattered protocols, confusing claims, and locked-up capital. OpenCover proved that there is a smarter way to bring it all together. Now it is your chance to take the lead.

At Idea Usher, we turn complex challenges into clean and reliable code. With over 500,000 hours of hands-on development and a team of former MAANG engineers, we know how to build systems that perform, scale, and inspire trust.

Here is how we help you stand out:

- We integrate multiple insurance protocols into one seamless experience.

- We design gas-efficient multi-chain architectures that actually work in the real world.

- We simplify claims into one smooth process, even when the technology behind it is complex.

It is time to stop talking about what is broken and start building what works. Let us create your DeFi insurance aggregator that users will actually trust.

FAQs

A1: A DeFi insurance aggregator is a platform that brings together multiple decentralized insurance providers into one easy-to-use system. It helps users compare coverage options, purchase policies, and manage claims without having to switch between different protocols. This kind of platform makes decentralized insurance more accessible and helps users protect their digital assets with greater confidence.

A2: A good DeFi insurance aggregator should have seamless multi-protocol integration, a simple policy purchase flow, and transparent claim management. It should also support cross-chain access so users can explore multiple coverage options from one dashboard. Adding real-time analytics and NFT-based policy tracking can further improve trust and user experience.

A3: The cost can vary depending on the project’s complexity, the number of integrations, and the overall design requirements. A basic aggregator might cost less, but building a robust multi-chain system with advanced features could require a larger investment. Working with an experienced blockchain development team often helps optimize costs while ensuring reliability and security.

A4: To build a DeFi insurance aggregator, you would usually use Solidity or Rust for smart contracts and frameworks like Hardhat or Truffle for development and testing. The backend might run on Node.js or Python, while the frontend can be built with React or Next.js. Integrating APIs, oracles, and cross-chain bridges is also essential to make the platform scalable and efficient.