(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

In traditional insurance, trust has always been fragile, and people often feel disconnected from the process. Many wait for weeks to get a claim approved and never really know how decisions are made. Centralized systems give institutions power, while users can only hope for fair treatment. Blockchain might finally change that by bringing ownership and clarity back to the people.

On-chain mutual insurance platforms allow members to pool their funds and share risk with complete visibility. They can include features like tokenized capital pools and automated claim settlements that work without middlemen. A DAO-based structure could allow every member to vote on important changes and to manage governance openly. Smart contracts would verify data instantly and release payouts only when conditions are met.

We’ve built multiple DeFi insurance solutions over the years that use advanced technologies such as blockchain architecture and smart contract automation. So, we’re putting together this blog to share our insights on the key steps to build an on-chain mutual insurance platform and see how decentralized technology can truly reshape trust and transparency.

Key Market Takeaways for an On-Chain Insurance Platform

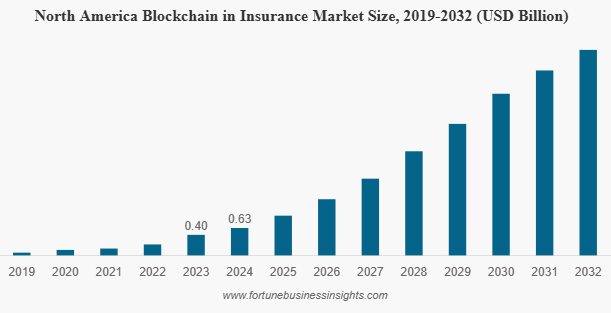

According to FortuneBusinessInsights, the blockchain insurance industry is gaining serious traction, valued at $1.86 billion in 2024 and expected to climb to nearly $60 billion by 2032. This surge, driven by a 53% CAGR, reflects insurers’ growing trust in blockchain’s ability to automate claims, reduce fraud, and create transparent risk pools. North America remains the key driver, accounting for over a third of the market, supported by regulatory clarity and a strong appetite for digital transformation.

Source: FortuneBusinessInsights

On-chain mutual platforms are leading this shift by reinventing how insurance capital is managed and distributed. Nayms (rebranded as OnRe) exemplifies this model, creating a regulated smart contract ecosystem that connects insurers, brokers, and investors. Built on tokenized capital pools and automated oracle-based claims, it blends institutional standards with decentralized efficiency.

Similarly, Nexus Mutual empowers users to collectively fund and share risk, offering flexible, transparent coverage options that evolve alongside DeFi and institutional demand.

Partnerships are fueling further growth in this space. Ensuro stands out for linking DeFi liquidity to real-world insurance providers, allowing decentralized capital to back traditional coverage. Through collaborations with networks like Polygon, Ensuro is proving that blockchain isn’t just a tool for innovation; it’s a bridge between financial ecosystems, expanding access to secure, efficient, and inclusive insurance solutions worldwide.

What are On-Chain Mutual Insurance Platforms?

On-chain mutual insurance platforms are blockchain-based systems that bring the entire insurance process onto decentralized infrastructure. Every step, including policy creation, capital pooling, claim assessment, and payout, is handled through smart contracts on the blockchain.

This model eliminates traditional intermediaries, automates complex administrative tasks, and provides transparent, tamper-proof records of all activities. It allows both individuals and enterprises to participate in and manage insurance coverage in a more efficient, auditable, and resilient way than traditional insurance models.

Here are some of their key features,

1. Smart Contract Automation

All insurance operations, including policy issuance, premium collection, and claims management, are executed by smart contracts. This automation ensures instant claim processing, removes manual errors, and significantly reduces administrative overhead.

2. Tokenized Capital Pools

Investor contributions are pooled and represented through digital tokens, allowing transparent and fractional ownership of risk. These tokenized pools create a tradable and auditable structure for capital participation and returns.

3. Automated Oracle-Based Claims

External data feeds, known as oracles, verify real-world events such as cyberattacks, weather incidents, or market movements. Once an event is confirmed, the system automatically triggers payouts, ensuring fairness, speed, and objectivity in claims handling.

4. Ring-Fenced Risk Pools

Each insurance program operates within its own smart contract cell, segregating capital and liabilities. This ring-fenced design maintains financial integrity and provides clear solvency boundaries, which are essential for regulatory compliance and institutional participation.

5. Secondary Market Liquidity

Some platforms enable users to trade their insurance positions on secondary markets. This feature introduces liquidity into the system, allowing investors to exit positions early or reallocate capital into new risk pools with minimal friction.

6. Regulatory and Compliance Integration

Platforms such as Nayms (OnRe) operate under recognized insurance jurisdictions like Bermuda, combining blockchain automation with traditional compliance standards. This alignment makes on-chain mutuals accessible to regulated and institutional clients.

7. Transparency and Auditability

Every policy, premium payment, and claim is permanently recorded on the blockchain. This immutable audit trail reduces fraud, increases accountability, and allows open verification of all financial activity.

8. Real-Time Settlement and Capital Release

At the end of each insurance cycle, capital is automatically released according to predefined contract terms. All distributions, including returns, fees, and premiums, are recorded transparently, ensuring a clear and permanent record of financial outcomes.

Important Types of On-Chain Mutual Insurance

The rise of on-chain mutual insurance is transforming how we think about risk and protection in the digital economy. By combining blockchain technology with cooperative risk sharing, these systems deliver new levels of transparency, automation, and community governance.

Not all risks are created equal, and neither are all insurance models. Two distinct structures have emerged as the foundation of this new landscape: Parametric Insurance and Discretionary Mutual Insurance. Understanding how each works is key to matching the right model with the right type of risk.

1. Parametric Insurance

Parametric insurance is a fully automated insurance model where payouts are triggered by specific, predefined events. There are no claim forms, no adjusters, and no back-and-forth negotiations. If the conditions of the policy are met, the payout happens automatically.

Here’s how it works,

Objective Parameters Are Defined:

Each policy is built around a clear, measurable condition. Examples include:

- “Pay $500 if Flight AB123 is delayed by more than four hours.”

- “Pay $10,000 if hurricane wind speeds exceed 100 mph at a specified weather station.”

- “Pay the policy limit if ETH drops below $2,000 during the coverage period.”

Data Comes from Oracles

The smart contract relies on decentralized oracles such as Chainlink to feed it real-world data. These oracles serve as trustworthy data bridges that report on flight delays, weather readings, or asset prices.

Automatic Execution:

The smart contract constantly monitors the oracle feed. The moment the data confirms that the event occurred, the contract executes the payout directly to the policyholder’s wallet, with no human intervention.

Best For: High-frequency, low-severity risks that can be objectively verified with reliable data. Common examples include flight delays, crop damage due to weather, price volatility in crypto markets, and smart contract failures.

2. Discretionary Mutual Insurance

Discretionary mutual insurance takes a very different approach. Instead of automated triggers, claims are evaluated by the collective judgment of the mutual’s members. This model revives the traditional idea of a shared risk pool, but now it operates transparently through blockchain governance.

It is designed for scenarios that are too complex or subjective for simple parametric conditions.

Here’s how it works,

A Claim Is Submitted

The policyholder files a claim for a loss that cannot be reduced to a yes-or-no data point. Examples include:

- “My NFT was stolen through a phishing attack.”

- “A DeFi protocol was exploited, and the loss may or may not fall within the coverage scope.”

- “A business dispute caused financial loss that could be covered.”

Community Governance Is Triggered

The claim is submitted to the protocol’s governance system. Token holders, who often also serve as capital providers, review the evidence and deliberate.

Voting and Payout

Token holders vote on whether the claim is valid. Many protocols use a staked voting model, where participants are rewarded for aligning with the majority and penalized for poor or biased voting. If the claim receives enough support, the smart contract releases the payout.

Best For: Complicated or subjective risks such as digital asset theft, contested smart contract exploits, professional indemnity coverage, or other long-tail risks where context and judgment matter.

Why 70% of On-Chain Coverage Protects Code, Not People?

If you look at the total value locked in on-chain insurance today, something interesting shows up. More than 70 percent of all capital sits in coverage for smart-contract and DeFi protocol failures. People are basically insuring their crypto with crypto. It might sound strange but it actually makes sense when you think about how these users see risk. This focus shows that on-chain insurance is both growing and still figuring out where it can go next.

Why the Obsession with Smart-Contract Risk?

This concentration didn’t happen by accident. It’s a textbook case of product–market fit in a new financial ecosystem.

1. The Existential Need

For anyone active in DeFi, whether staking, lending, or yield farming, the biggest threat isn’t a car crash or a flood; it’s a bug in the code. A single exploit can erase millions in seconds. Traditional insurers don’t touch that kind of risk, leaving a vacuum that only blockchain-native solutions can fill.

2. The Perfect Parametric Match

Smart-contract failure is tailor-made for parametric coverage.

The triggers are objective:

- Did a protocol suffer a specific exploit?

- Did an asset in a liquidity pool collapse to zero?

These events are verifiable on-chain. Oracles can detect them and trigger automatic payouts with no paperwork, no adjusters, and no delays.

3. The Aligned Community

The people buying these policies are the ecosystem itself. They understand staking, governance, DAOs, and smart contracts. They don’t just use the mutual; they are the mutual.

The Untapped Trillion-Dollar Market

Securing the DeFi ecosystem is no small feat, but it’s only a fraction of what’s possible. The next frontier is the real world, where billions of people remain uninsured or underinsured.

Here’s where on-chain mutual insurance could rewrite the rulebook:

- The Gig Economy: Freelancers, delivery drivers, and ride-share workers often lack disability or income protection. A blockchain-based mutual could offer parametric coverage triggered by verified downtime due to accident or illness.

- Travel and Events: Flight delay insurance shouldn’t be an overpriced afterthought. A transparent, low-cost, parametric policy triggered automatically by public flight data is a natural fit for on-chain models.

- Agriculture in Developing Regions: Smallholder farmers face devastating losses from droughts or floods. An on-chain mutual could use satellite or weather oracle data to trigger instant payouts, preventing hardship before it spirals into debt or famine.

- Personal Asset Protection: From phone theft to laptop damage to rental disputes, a mix of automated and community-assessed claims could provide accessible, transparent coverage without traditional bureaucracy.

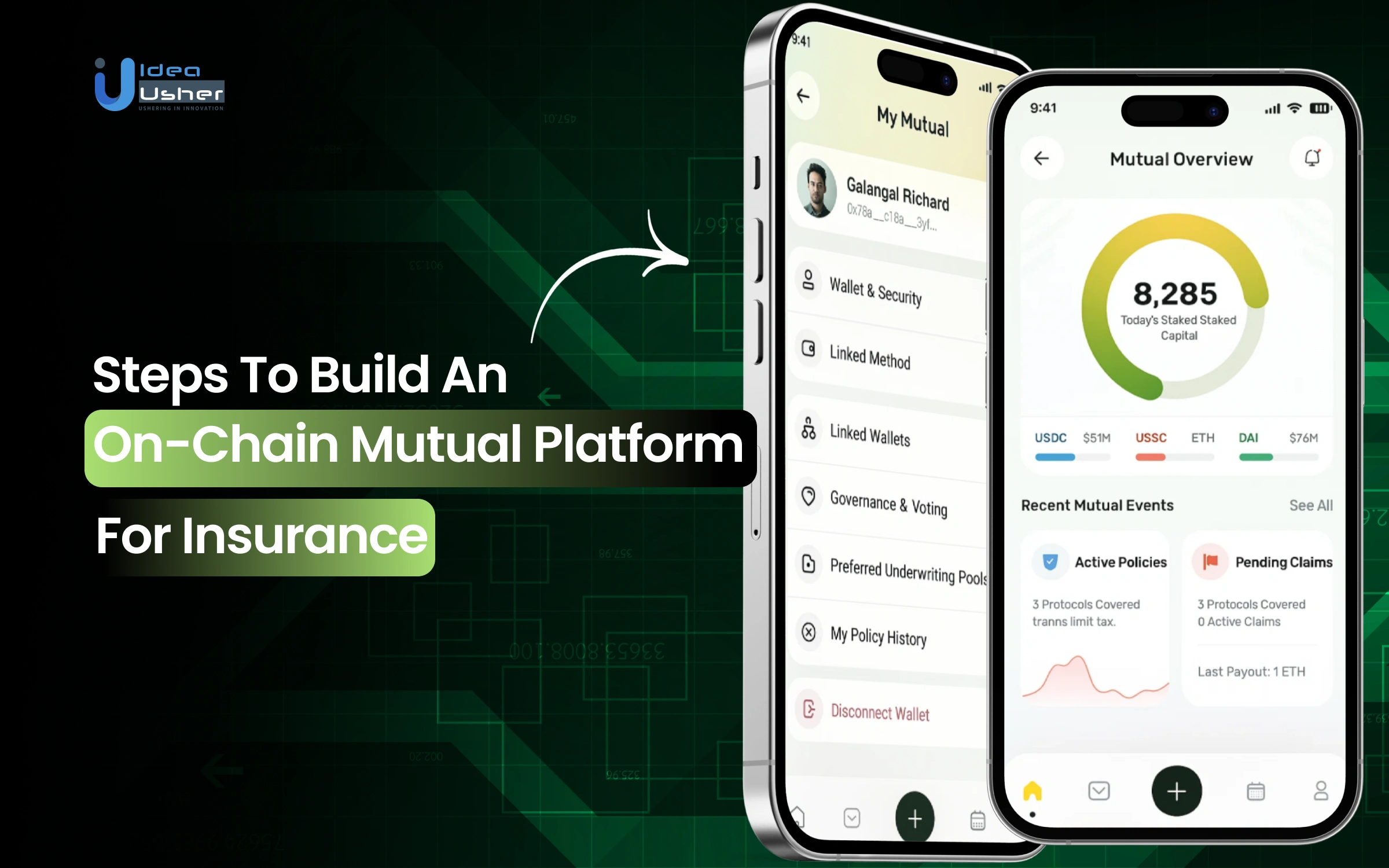

How to Build an On-Chain Mutual Platform for Insurance?

We design and develop on-chain mutual insurance platforms that let communities pool capital, share risk, and manage claims transparently through blockchain technology. We have built several of these platforms for our clients, and each one solves real challenges in decentralized coverage. Here’s how we usually approach and deliver them with clarity and purpose.

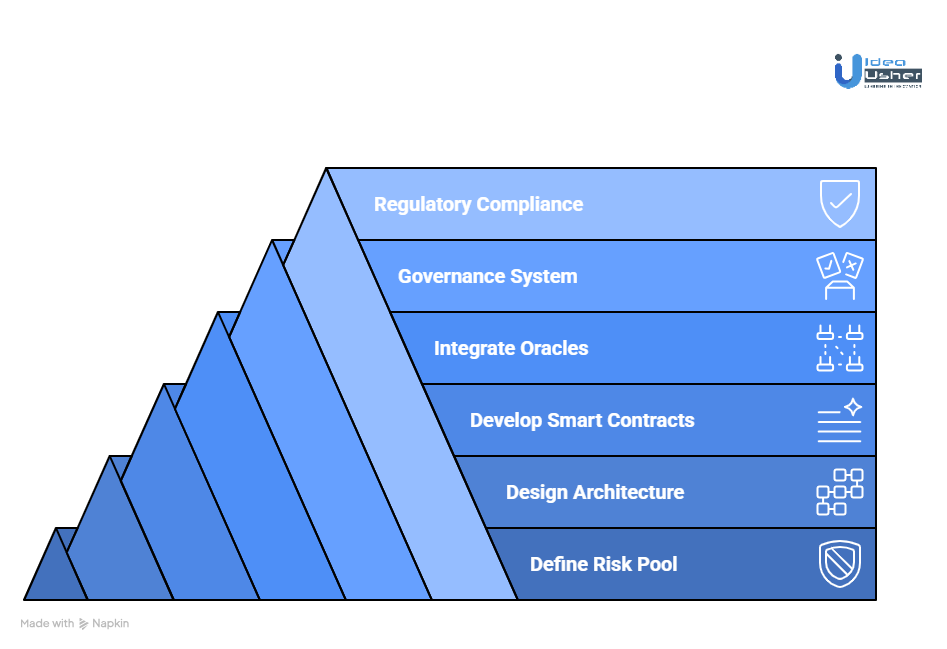

1. Define Risk Pool & Coverage Niche

We start by helping clients identify a focused coverage area such as DeFi protocol exploits, agricultural yield loss, or stablecoin de-pegging. Together, we define parametric coverage conditions that oracles can verify to ensure trustless payouts. Our team also establishes clear coverage limits, premium structures, and risk-scoring models to create a sustainable, transparent mutual risk pool.

2. Design Blockchain Architecture

Next, we design the technical foundation of the mutual platform. Depending on scalability and transaction needs, we deploy on Ethereum, Polygon, Arbitrum, or Optimism. The architecture connects users, smart contracts, oracles, and DAO governance through a secure and efficient data flow. We build separate modules for capital pooling, governance operations, and claims management to ensure system reliability and modular growth.

3. Develop & Audit Smart Contracts

Our blockchain engineers develop robust self-executing smart contracts that automate policy issuance, premium collection, and claim approvals. Policies are tokenized using NFT-based policy tokens for full transparency and traceability. Before deployment, we conduct comprehensive audits with independent blockchain security firms to ensure the contracts are safe, reliable, and production-ready.

4. Integrate Decentralized Oracles

We integrate oracle networks such as Chainlink, Pyth, or API3 to pull real-world event data into the blockchain securely. To ensure data accuracy, we implement redundant oracle sources and fallback mechanisms, maintaining consistent, reliable coverage verification even under adverse conditions.

5. Governance and Tokenomics System

We help clients design their governance framework powered by a native token such as $GOV. Token holders can stake, vote, and participate in claim decisions through a user-friendly DAO interface. This system empowers members to propose updates, allocate funds, and manage risk pools collaboratively, ensuring that the platform remains truly community-driven.

6. Regulatory and Compliance Layers

Finally, we integrate on-chain compliance systems to align with global regulations. Using Civic, Polygon ID, or other identity verification APIs, we enable secure KYC/AML verification directly on-chain. Our RegTech smart contracts automatically enforce compliance limits, while transparency logs provide verifiable audit trails for regulators and stakeholders.

Key Challenges of an On-Chain Mutual Platform for Insurance

After helping several businesses build on-chain mutual platforms, we have seen the same core challenges recur. The good news is that each one has a clear and practical solution when approached with the right architecture and mindset.

1. The Oracle Problem

The Challenge: Smart contracts are only as reliable as the data they consume. If a flight-delay oracle goes offline or a price feed is manipulated, claims can fail or, worse, drain the capital pool through false triggers.

Our Solution: Redundancy and Decentralization.

We never rely on a single oracle. Our systems use multiple data sources such as Chainlink, Band Protocol, and API3 to cross-check information. If one feed fails or shows an anomaly, the system automatically falls back to others. We also use time-weighted average price data and backup nodes to protect against flash manipulation attacks, keeping claim triggers both accurate and reliable.

2. The Governance Trap

A mutual should reflect collective decision-making, yet the traditional one-token-one-vote model can lead to dominance by large holders. When a few whales control proposals, trust erodes and community participation drops.

Our Solution: Fair and Transparent Voting.

We design governance systems that balance influence with fairness. Quadratic voting makes it progressively more expensive for one entity to control the outcome, encouraging wider participation. We also use weighted reputation models that factor in user contributions, such as claim validations or governance engagement, ensuring active members have meaningful influence.

3. Building and Sustaining the Capital Pool

The Challenge: Without liquidity, the pool cannot offer meaningful coverage. Early-stage insurance protocols often struggle to attract and retain enough capital to back policies, leading to low limits and weak user confidence.

Our Solution: Incentivized Liquidity and Market Design.

We create incentive models that reward users for providing liquidity and participating in governance. Staking programs allow members to earn from premium revenue and native token rewards. Policy NFTs add flexibility by letting users trade or resell their coverage, creating a secondary market and improving liquidity from day one.

4. Smart Contract Vulnerabilities

One vulnerability in a smart contract can result in irreversible loss of funds. In a trustless system, there is no customer support line, only code, and code must be airtight.

Our Solution: A Multi-Layered Security Process.

We treat security as an ongoing commitment. Every deployment goes through a full third-party audit by leading firms such as CertiK or PeckShield. We also run continuous bug bounty programs that invite ethical hackers to identify risks before attackers can. Extensive testnet simulations allow us to stress-test the system against both normal operations and potential economic exploits.

5. Staying Ahead of Compliance

Regulations for on-chain insurance and DeFi are still evolving. Without a clear framework, projects risk compliance issues or limitations on where they can operate.

Our Solution: Proactive Compliance and Transparent Operations.

We integrate decentralized KYC and AML solutions such as Polygon ID to meet legal standards without compromising user privacy. Every transaction, claim, and governance action is immutably recorded on-chain, giving regulators and partners a transparent and verifiable audit trail. This approach builds long-term credibility while keeping the system open and accountable.

Successful Business Models for On-Chain Mutual Insurance Platforms

The intersection of decentralized finance and insurance has sparked a new generation of on-chain mutuals. These platforms use blockchain technology to reimagine how risk is shared and managed, introducing transparency, automation, and community-driven governance to a traditionally opaque industry.

The strength of these platforms lies in their ability to align incentives among three key stakeholders: capital providers, policyholders, and the protocol itself. Here are the four business models that have proven most effective in achieving that balance.

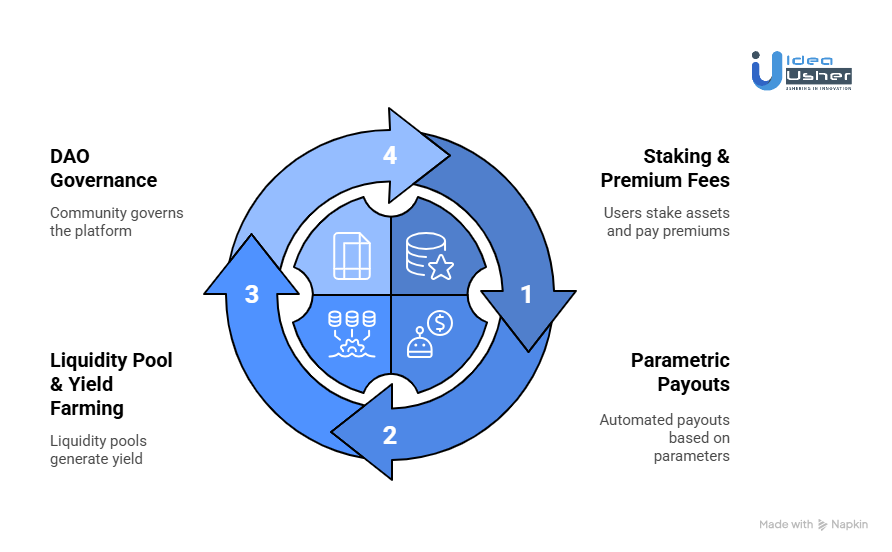

1. The Staking & Premium Fee Model

This is the backbone of most decentralized insurance platforms. It mirrors the traditional mutual insurance model but introduces blockchain efficiency and composability.

How It Works: The protocol acts as a two-sided marketplace. On one side, capital providers (stakers) deposit crypto assets such as ETH or USDC into a shared capital pool that backs policies. On the other side, users purchase coverage by paying premiums. The protocol charges a small fee from each premium before distributing the remainder to the stakers.

Revenue Stream: A protocol fee, typically 10% to 20% of collected premiums.

Value Proposition:

- For Stakers: A yield-generating opportunity tied to real insurance demand, often outperforming traditional bond yields.

- For Policyholders: Tailored, blockchain-native coverage with faster and more transparent claim resolutions.

Real-World Example: Nexus Mutual

Nexus Mutual pioneered this model by offering smart contract failure coverage. Members stake NXM tokens to back the pool, and policyholders pay premiums in ETH or DAI.

Over its lifetime, Nexus Mutual has generated more than $376 million in total premiums. During the 2021–2022 bull market alone, premiums exceeded $270 million. Assuming a 10% protocol fee, that represents roughly $27 million in annual treasury revenue, underscoring the power of this model in active DeFi markets.

2. The Parametric & Automated Payout Model

This model is built for efficiency and automation, removing human discretion from the claims process altogether.

How It Works: Policies are written around clear, objective conditions. When a predefined event occurs, such as a flight delay or extreme weather, a decentralized oracle automatically triggers a payout.

Revenue Stream: A small fee on each premium, with profitability driven by high policy volume rather than high margins.

Value Proposition:

- Speed and Certainty: Payouts are instant and trustless once conditions are met.

- Low Overhead: There is no need for manual claims management or adjusters.

Real-World Example: Etherisc

Etherisc focuses on parametric insurance frameworks. One of its products, Flight Delay Insurance, automatically compensates users when a flight delay exceeds a preset threshold, using oracle-fed flight data.

3. The Liquidity Pool & Yield Farming Model

This approach merges insurance economics with DeFi liquidity incentives, helping protocols overcome the “cold start” challenge of attracting initial capital.

How It Works: Users deposit assets into liquidity pools in exchange for LP tokens that represent their share of the pool. These LP tokens can then be staked to earn additional rewards, typically in the form of the protocol’s native governance tokens.

Revenue Stream: The protocol still earns fees on premiums but temporarily issues token rewards to bootstrap growth.

Value Proposition:

- For Liquidity Providers: Dual incentives consisting of a share of premiums plus token rewards with high APY potential.

- For the Protocol: Rapid growth of capital reserves, enabling meaningful coverage capacity early on.

Real-World Example: InsurAce

InsurAce adopted a yield-farming-based mutual model across multiple chains. Users can stake USDC or other stable assets to back policies and earn both premium yield and $INSUR token rewards.

4. The DAO-Governed Subscription Model

Aimed at complex or high-value risks, this model operates like a decentralized Lloyd’s of London, relying on expert-driven governance rather than full automation.

How It Works: A DAO oversees underwriting and claims. Governance token holders vote on which policies to underwrite and how to price risk. Coverage is often offered through recurring subscription premiums, ensuring predictable revenue streams.

Revenue Stream: A protocol fee on recurring premiums, often substantial due to high policy values.

Value Proposition:

- Customization: Tailors coverage for nuanced, hard-to-model risks such as smart contract exploits or cross-chain vulnerabilities.

- Community Expertise: Uses decentralized, incentivized governance to assess and validate claims.

Real-World Example: Sherlock

Sherlock provides audit-backed smart contract coverage for DeFi projects. Clients pay subscription fees in USDC for continuous protection. A panel of expert judges and UMA’s optimistic oracle handles claim validation, with $SHER token holders governing the process.

Tools & APIs For an On-Chain Mutual Insurance Platform

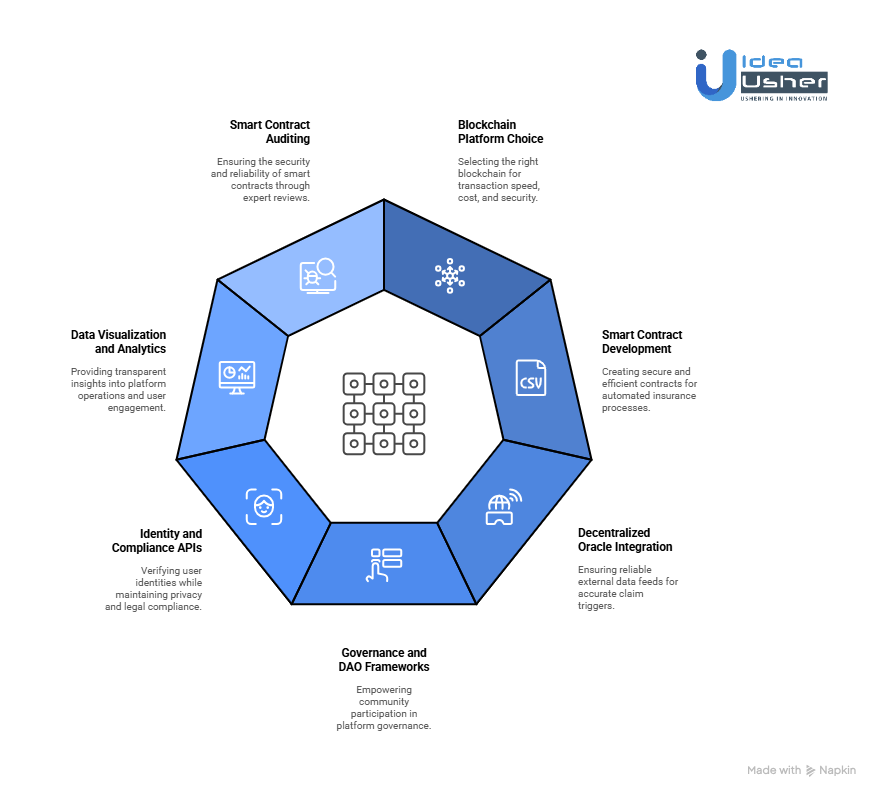

The idea of an on-chain mutual insurance platform is a powerful one. It offers a transparent, community-driven alternative to a system often weighed down by opacity, delays, and mistrust. But a strong vision needs a strong foundation. The right mix of tools, APIs, and frameworks does more than make development easier. It determines how secure, scalable, and future-proof your platform will be.

1. Choosing Your Blockchain Platform

Your blockchain choice shapes everything that follows. It defines your transaction speed, costs, and security model.

Ethereum

The long-standing leader in smart contract platforms. It provides unmatched security and deep liquidity, making it a safe choice for storing governance assets or high-value capital pools. The downside is its higher gas fees, which can make smaller and frequent transactions more expensive.

Polygon and Arbitrum

These scaling solutions are ideal for insurance platforms that need low fees and high speed. They process transactions efficiently while still benefiting from Ethereum’s base layer security. This balance makes them perfect for high-frequency activities such as micro-premiums and claim submissions.

Avalanche

Another strong, EVM-compatible option. It is fast, cost-effective, and supports creating subnets for specialized use cases such as private mutual pools or dedicated claim chains.

Our Take: A hybrid model often works best. Launching on a Layer 2 like Polygon or Arbitrum for affordability and user access, while anchoring governance and treasury contracts on Ethereum, delivers both reach and resilience.

2. Smart Contract Development

Your smart contracts hold your business logic. They enforce how premiums are collected, policies are issued, and claims are processed without human intervention.

- Solidity: The standard language for Ethereum and its compatible chains. It offers extensive resources, documentation, and a large developer community.

- Hardhat and Truffle: These are your go-to environments for writing, testing, and deploying contracts. Hardhat’s plugin ecosystem and flexible configuration make it a favorite for modern development workflows.

- OpenZeppelin Libraries: Building from scratch is risky when security is at stake. OpenZeppelin offers audited implementations of core standards like ERC-20 and ERC-721, along with modules for access control, pausing, and safe arithmetic.

3. Decentralized Oracle Integration

Smart contracts cannot see the real world, so they depend on oracles for trusted external data. For insurance, oracles determine when an event such as a hack, depeg, or weather incident actually happens.

- Chainlink: The industry benchmark for decentralized data feeds. It delivers accurate, tamper-resistant information to trigger parametric insurance claims automatically.

- Band Protocol and API3: Reliable alternatives that approach data aggregation differently. They allow greater customization and can suit use cases where you need specific data sources or governance structures.

- Our Take: In insurance, Oracle security is non-negotiable. Chainlink’s decentralized network remains the minimum standard for ensuring fairness and accuracy in claim triggers.

4. Governance and DAO Frameworks

A mutual insurance model lives and dies by its community. These frameworks give members the power to guide the platform’s evolution transparently.

- Snapshot: A simple, gasless voting system that records governance proposals and decisions off-chain. It is perfect for community engagement without burdening users with transaction costs.

- Aragon: A robust framework for launching on-chain DAOs. It offers built-in governance, treasury control, and access management tools that help your mutual operate like a transparent digital cooperative.

5. Identity and Compliance APIs

Even in decentralized finance, compliance matters. Proper identity verification keeps your platform credible and legally sound.

- Polygon ID and Civic: These decentralized identity tools let users prove who they are without revealing personal information. They are ideal for compliance scenarios that require user verification but still value privacy.

- Veriff: A centralized yet effective option for verifying user identities through government-issued documents. It is often used during onboarding to ensure your user base meets jurisdictional standards.

6. Data Visualization and Analytics

Transparency builds trust faster than any marketing campaign. When users can see exactly how capital pools, claims, and governance decisions evolve, they believe in the system.

- The Graph: A decentralized indexing protocol that allows fast querying of blockchain data. It powers dashboards that show users their policies, claim statuses, and live platform metrics.

- Dune Analytics: A public analytics platform where anyone can create dashboards tracking metrics such as Total Value Locked, claim payouts, and premium flows. Adopting Dune promotes openness and strengthens community confidence.

7. Smart Contract Auditing Tools and Firms

In DeFi, one bug can undo years of work. Continuous auditing and automated security checks are essential, not optional.

- MythX: A tool that scans smart contracts for vulnerabilities before deployment. It integrates directly with development environments like Hardhat to catch issues early.

- CertiK and PeckShield: Two of the most respected names in blockchain security. A full audit by either firm is a crucial step before going live. It assures users that your contracts have been reviewed and tested by top-tier professionals.

Top 5 On-Chain Insurance Mutual Platforms in the USA

We did a deep dive into the on-chain insurance space and found some really interesting mutual platforms that are changing how people share risk. You might actually find it surprising how transparent and community-driven these projects are. They could easily become a major part of how insurance works in the future.

1. Nexus Mutual

Nexus Mutual is one of the most established decentralized mutual insurance protocols. It operates as a member-owned risk-sharing pool on Ethereum, offering coverage for smart contract failures, exchange hacks, and custody risks. All governance, claims, and capital are managed transparently on-chain.

2. Bridge Mutual

Bridge Mutual is a decentralized insurance marketplace that lets users provide liquidity to earn yields while offering coverage against smart contract exploits, stablecoin de-pegs, and exchange hacks. It emphasizes a fully on-chain, community-driven claims process and dynamic pricing.

3. Tidal Finance

Tidal Finance provides a decentralized mutual-style cover protocol where users can create customizable insurance pools for different DeFi projects. It focuses on risk diversification, flexible pool creation, and yield optimization through shared capital.

4. Dynamis

Dynamis was one of the earliest Ethereum-based P2P insurance DAOs, originally built for unemployment and income protection coverage. It explored a true mutual insurance structure in which members verified claims and shared risk directly via smart contracts.

5. Nayms

Nayms is an on-chain insurance marketplace designed for professional and commercial risk transfer. It tokenizes insurance contracts and risk pools, enabling investors, underwriters, and brokers to participate transparently in fully auditable on-chain insurance markets.

Conclusion

We are entering a new era where insurance becomes transparent, fair, and community-driven. On-chain mutual platforms are reshaping how people view protection by replacing hidden processes with openness and shared ownership. Businesses adopting this approach can gain both trust and profitability through decentralization while building stronger relationships with their users.

With sound architecture, thoughtful tokenomics, and proper compliance, they can launch scalable, community-owned insurance models that truly empower their members. At Idea Usher, we help enterprises make this shift by integrating blockchain, smart contracts, and DAO governance into real-world insurance systems that are built to last and ready to inspire trust.

Looking to Develop an On-Chain Mutual Platform for Insurance?

Creating a decentralized insurance platform takes more than just blockchain know-how. It demands precision, security, and deep technical experience.

At Idea Usher, we have invested over 500,000 hours of development into blockchain, Web3, and DeFi systems. Our team includes former MAANG engineers who understand what it takes to turn ambitious ideas into reliable, user-friendly products.

- We help you design and launch an on-chain mutual insurance platform built on solid architecture, audited smart contracts, and a frictionless user experience.

- Every project we build is engineered for trust, performance, and scalability. The results speak for themselves. Explore our latest work to see how we deliver innovation that lasts.

Let’s redefine the insurance industry, secured by code and powered by vision.

FAQs

A1: An on-chain mutual platform for insurance is a decentralized system where people come together to pool funds and share risk using blockchain technology. Instead of relying on traditional insurers, members manage the platform through smart contracts and community voting. This setup makes the process transparent and fair while giving users real ownership of the coverage model. It creates a community-driven approach where everyone has a say and benefits from collective trust.

A2: An on-chain mutual insurance platform makes money mainly through membership fees, cover premiums, and returns on the pooled capital that members provide. It may also earn yield by staking or investing idle funds in low-risk DeFi protocols. Since these platforms are member-owned, profits are often redistributed to participants or used to strengthen the capital pool for future claims.

A3: An on-chain mutual platform usually includes automated claim settlements, tokenized capital pools, DAO-based governance, and transparent fund tracking. It may also support staking and yield features to make capital more productive. The platform offers flexibility in creating insurance products for different risks, such as smart contract failures or market volatility. Every transaction is recorded on-chain, giving users full visibility and confidence in how funds are managed.

A4: The cost depends on several factors such as the platform’s scale, feature complexity, security requirements, and blockchain infrastructure. A basic version might cost less, while a full-featured solution with advanced smart contracts and DAO governance will require more investment. Development can start from a modest budget but may grow as the platform expands and integrates more services. It is always best to consult with a blockchain development team to get a detailed estimate based on your goals and technical needs.