(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Paying and getting paid should be simple but for many merchants and users, it can be slow, complicated, and frustrating. Delays, transaction fees, failed payments, and complicated checkout processes often create frustration on both sides. That’s why pay-by-bank apps are gaining traction and promise a faster, more secure way to move money directly between accounts, without the friction of cards or intermediaries.

These apps leverage bank-to-bank connections and modern security protocols to streamline payments. For users, this means instant, convenient transactions. For merchants, it reduces fees, improves cash flow, and enhances the checkout experience. By combining simplicity with reliability, pay-by-bank solutions make digital payments smoother for everyone involved.

In this blog, we’ll explore the key benefits of pay-by-bank apps for both merchants and users, highlight how these platforms work, and show why businesses and consumers are increasingly adopting them in today’s digital economy. With experience in building secure and scalable payment solutions, IdeaUsher provides the expertise to help companies implement pay-by-bank apps that enhance user trust, operational efficiency, and long-term value for investors.

What is a Pay-by-Bank App?

A Pay-by-Bank app is a digital payment solution that allows users to make transactions directly from their bank account without the need for cards or third-party wallets. Instead of entering card details, users authorize payments securely through their banking app, using methods such as two-factor authentication or biometric verification.

These apps streamline payments, cut fees, and boost security by using existing bank infrastructure. Connecting merchants directly to customer accounts allows faster, safer, more transparent payments than traditional card or wallet systems.

Pay-by-Bank Apps vs. Card Payments and Digital Wallets

Pay-by-Bank apps are emerging as a seamless alternative to traditional card payments and digital wallets, allowing direct transfers from a user’s bank account. They offer enhanced security, faster transactions, and reduced reliance on intermediaries like cards or wallet balances.

| Feature | Pay-by-Bank App | Traditional Card Payments | Digital Wallets |

| Security | Transactions authorized directly through the bank using biometrics or 2FA, reducing fraud. | Relies on card networks and PINs; susceptible to theft or skimming. | Security depends on wallet provider; compromised credentials can lead to unauthorized access. |

| Transaction Speed & Settlement | Real-time fund transfer between accounts; instant checkout. | May involve delayed settlement due to multiple intermediaries. | Usually instant payments, but withdrawing to bank can take time. |

| Cost & Fees | Lower fees; no card network or wallet charges. | Includes merchant processing fees; sometimes customer charges apply. | Fees may apply for transfers, top-ups, or international payments. |

| Transparency & Control | Direct visibility of funds; bank provides detailed reporting. | Limited tracking; depends on bank statements and card network reporting. | Wallet provider maintains records; full account-level transparency may be missing. |

| User Experience | Simple checkout; no card entry or wallet top-up needed; integrated with bank app. | Requires entering card details, can be cumbersome or error-prone. | Easy for frequent wallet users, but requires setup and balance management. |

How a Pay-by-Bank App Works?

A Pay-by-Bank app enables secure, direct payments from a user’s bank account, removing the need for cards or third-party wallets. It leverages bank APIs and authentication protocols to ensure fast, safe, and transparent transactions.

1. Payment Initiation

The user selects Pay-by-Bank at checkout, either online or in-store. The app identifies the user’s bank and prepares a secure payment request, simplifying the process and reducing manual input errors.

2. User Authentication

The app redirects the user to their banking interface, where they authorize the payment using two-factor authentication, biometrics, or OTPs. This step ensures high security and builds trust in the payment system.

3. Transaction Processing

Once authenticated, the bank transfers funds directly to the merchant’s account. Real-time APIs ensure instant processing, lower transaction fees, and elimination of intermediaries, making payments faster and more cost-efficient.

4. Confirmation & Record Keeping

Both the user and merchant receive instant confirmation of the payment. The app maintains a secure, auditable record for transparency, dispute resolution, and regulatory compliance, enhancing accountability across all transactions.

Why You Should Invest in Launching a Pay by Bank App?

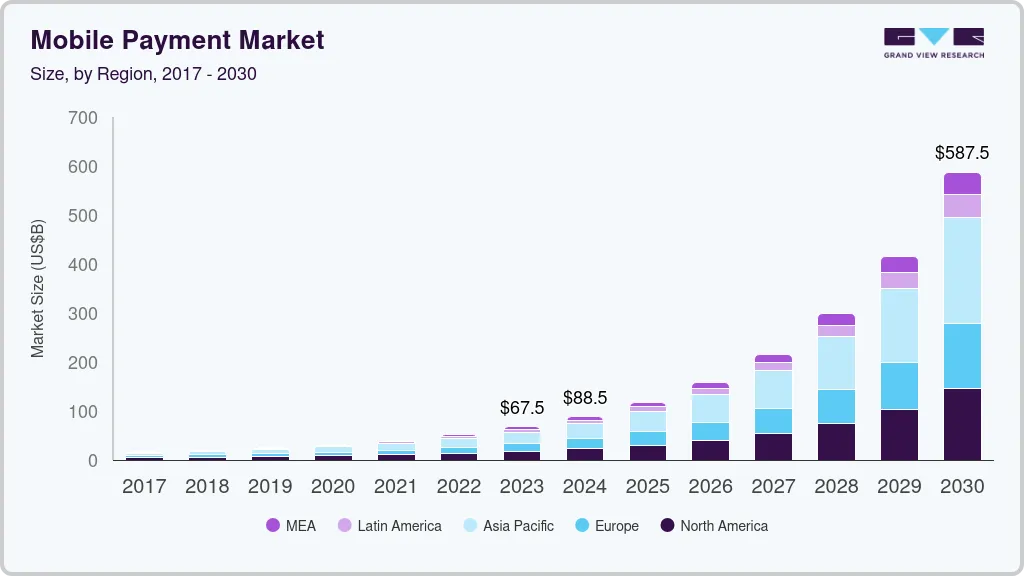

Pay by Bank is an emerging, convenient payment method linking directly to your bank account, part of the growing mobile payment market valued at USD 88.5 billion in 2024 and projected to reach USD 587.5 billion by 2030 at a 38% CAGR. This reflects how quickly consumers are adopting digital payment solutions globally.

The Pay by Bank sector is attracting significant investment, underscoring its potential for growth and innovation. Notable funding rounds include:

- Banked Ltd raised a $20 million Series A round led by Bank of America and Edenred Capital Partners, with participation from investors like Acrew and Force Over Mass.

- Fortis, a UAE-based fintech firm, secured $20 million in Series A funding to enhance customer-centric services and expand partnerships.

- Stitch, a South African payments startup, raised $21 million in Series A funding to develop its Pay by Bank solution, LinkPay.

These investments highlight the growing confidence in Pay by Bank solutions and their scalability across various markets.

Strategic Advantages of Pay by Bank

Investing in a Pay by Bank app offers several strategic benefits:

- Cost Efficiency: Merchants can reduce transaction fees significantly compared to traditional card payments. For instance, partnerships like Spire and Discover aim to save merchants up to 90% on processing fees by integrating Pay by Bank at the point of sale.

- Enhanced Security: Direct bank-to-bank transactions minimize fraud risks and provide consumers with a secure payment method.

- Consumer Preference: A growing number of consumers prefer Pay by Bank options for their speed and convenience, as evidenced by collaborations like MoneyGram’s partnership with Plaid to enable faster, secure bank account authentication.

- Global Expansion: Countries are increasingly adopting open banking frameworks, paving the way for Pay by Bank solutions to become mainstream. The UK’s Faster Payments network and Saudi Arabia’s Vision 2030 initiative are examples of such developments.

The growing mobile payment market and the emergence of Pay by Bank solutions present a strong investment opportunity. With increasing consumer demand for secure payments and favorable regulations, launching a Pay by Bank app places you at the forefront of digital payments and offers significant potential for returns.

Benefits of Pay-by-Bank Apps for Merchants

Pay-by-Bank apps enable merchants to accept payments directly from customers’ bank accounts, improving efficiency, security, and profitability. By removing intermediaries, merchants can enjoy multiple pay-by-bank app benefits that enhance both operations and customer trust.

1. Lower Transaction Fees

Traditional payment methods like credit cards or digital wallets charge merchants high processing fees per transaction. Pay-by-Bank apps eliminate card networks by linking customer bank accounts directly with merchants, reducing transaction costs, especially for high-volume or low-margin sales. These savings allow merchants to reinvest in growth, offer discounts, or improve competitiveness.

2. Faster Settlements

Merchants face delays of 2–3 days in settling card payments. Pay-by-Bank apps enable instant or near-instant transfers from customers’ banks to merchants, boosting cash flow. Faster access helps cover payroll, stock, and expenses, vital for small and medium businesses’ survival and growth.

3. Enhanced Security

Security concerns, chargebacks, and fraud are costly for merchants. Pay-by-Bank apps use the bank’s security, including biometrics, encryption, and two-factor verification. Since transactions are authorized directly by the bank, the risk of fraud is reduced. Merchants also face fewer disputes and chargebacks, saving time and money.

4. Increased Customer Trust

Customers paying directly from their bank see the checkout as more trustworthy and transparent than using third-party wallets or cards, reducing hesitations and cart abandonment. This builds stronger customer relationships, boosting repeat purchases and loyalty. In competitive sectors like e-commerce, trust becomes a key differentiator.

5. Simplified Reconciliation

Handling multiple payment methods causes reconciliation issues, leading to errors and wasted time. Pay-by-Bank apps simplify this with clear transaction trails, reference numbers, timestamps, and account details. This makes audits easier, improves accuracy, and offers real-time financial visibility.

6. Reduced Dependency on Intermediaries

By using Pay-by-Bank, merchants reduce reliance on third-party payment providers that can impose changing fees, terms, or technical issues. This greater autonomy gives merchants more control over their payment systems and reduces risks tied to external disruptions.

7. Better Compliance and Transparency

Since Pay-by-Bank transactions are routed through regulated banks, merchants automatically operate within strict compliance frameworks. This reduces regulatory risks and provides better transparency to both customers and regulators. For global merchants, this also helps in handling cross-border transactions with fewer compliance headaches.

Benefits of Pay-by-Bank Apps for Users/Consumers

Pay-by-Bank apps allow users to make direct payments from their bank accounts without needing cards or third-party wallets. By connecting securely to their bank, users enjoy faster, safer, and more transparent transactions while gaining access to key pay-by-bank app benefits that enhance convenience and trust.

1. Enhanced Security

Pay-by-Bank apps leverage bank-grade authentication methods such as biometric verification (fingerprint or facial recognition), secure PINs, and two-factor authentication. Transactions happen directly between the bank and merchant, so sensitive card data isn’t stored. This minimizes exposure to fraud or phishing attacks and ensures users have greater confidence when paying online or in-store.

2. Faster and Seamless Payments

These apps enable instant transactions, instead of traditional card payments that require entering long card numbers or topping up digital wallets. Users simply authorize the payment, and funds move directly to the merchant. This reduces checkout friction, particularly in e-commerce, ride-hailing, or food delivery apps, making everyday purchases quicker and hassle-free.

3. Lower or No Transaction Fees

Since Pay-by-Bank apps cut out intermediaries like card processors or wallet providers, users often avoid additional transaction charges. This is especially beneficial for frequent or small-value payments where card fees can add up over time. By lowering costs, these apps make digital payments more accessible and economical for regular users.

4. Transparency and Control

Every transaction made through the app is recorded in real-time and accessible through detailed transaction histories. Users can track exact amounts, timestamps, and merchants, which improves budgeting and financial management. This transparency also prevents hidden charges, giving users clear control over their money.

5. Improved Trust and Reliability

Because payments flow directly from the user’s bank to the merchant’s bank, transactions are instant and verifiable. There’s no risk of funds being “stuck” in an intermediary system. This reliability encourages users to trust Pay-by-Bank apps as a consistent and dependable alternative to cards or wallets for both online and offline purchases.

6. Wider Accessibility

Unlike digital wallets that require topping up or credit cards that need approval, Pay-by-Bank apps can be used by anyone with a bank account. This inclusivity makes digital payments accessible to a larger population, including users who don’t want or qualify for a credit card but still seek safe, modern payment options.

Key Features of a Pay-by-Bank App

Pay-by-Bank apps combine convenience, security, and speed to simplify direct bank-to-merchant transactions. Understanding their key features and the pay-by-bank app benefits helps users and businesses maximize efficiency and trust in digital payments.

A. Key Features for Merchants

For merchants, payment solutions go beyond convenience as they directly impact sales, customer experience, and operational efficiency. Understanding the key features and pay-by-bank app benefits helps businesses choose the right option to streamline transactions and boost profitability.

1. Direct Bank Settlements

The app enables merchants to receive funds directly into their bank accounts in real time, bypassing card networks and third-party payment processors. This not only eliminates high transaction fees but also improves cash flow, ensuring businesses have immediate access to working capital without waiting days for settlements.

2. Real-Time Transaction Dashboard

Merchants need visibility over their incoming payments, and the dashboard offers live transaction tracking, automated reconciliation, and detailed financial analytics. By reducing manual accounting errors and giving a clear overview of business performance, merchants gain better financial control and planning ability.

3. Multi-Bank Support for Payouts

Businesses often operate across multiple accounts or entities, and the app supports linking several bank accounts for payouts, refunds, or revenue sharing. This flexibility helps merchants manage operations more efficiently while avoiding delays caused by limited banking options.

4. QR Code and POS Integration

The Pay-by-Bank app integrates seamlessly with QR codes and point-of-sale systems, enabling businesses to accept payments both online and in-store without investing in extra hardware. Faster checkouts improve the customer experience, while merchants reduce dependency on costly POS infrastructure.

5. Seamless Refund Management

Refunds and reversals are processed directly through connected bank accounts, making it a smooth experience for customers and reducing disputes. For merchants, this strengthens customer trust, encourages repeat business, and reduces friction in post-purchase interactions.

6. AI-Powered Fraud Detection

The app integrates AI-driven fraud monitoring tools that analyze payment patterns, flag unusual activities, and block suspicious transactions in real time. This reduces financial risks for merchants and protects their businesses from fraudulent chargebacks while ensuring smoother transactions.

B. Key Features for Users/Consumers

For users, the value of a payment method lies in its ease, speed, and security. The right features ensure a smooth checkout experience while building trust and confidence in every transaction.

1. Direct Bank Payments

Users can pay directly from their bank account without the need for cards or e-wallets. This reduces hidden charges, makes payments faster, and offers a straightforward, low-cost alternative to traditional payment methods.

2. Multi-Factor Authentication

To ensure security, every transaction is protected with biometric verification, OTPs, or PINs, making it nearly impossible for unauthorized payments to go through. This strengthens user confidence in the app and reduces fraud risks significantly.

3. Instant Payment Confirmation

Once a payment is made, users receive immediate confirmation and real-time notifications, eliminating the uncertainty often seen with delayed payment updates. This builds trust in the system and creates a seamless checkout experience.

4. Spending Insights & History

The app provides users with detailed transaction histories and spending insights, enabling better personal finance management. This feature helps users stay in control of their money while also improving transparency across all payments.

5. Refund Tracking

Refunds are deposited directly into the user’s linked bank account, often within hours rather than days. This eliminates the frustration of waiting for money to return and enhances the overall shopping experience.

6. Recurring & Scheduled Payments

Users can set up automatic recurring payments or scheduled transfers (e.g., subscriptions, utility bills, or rent). This feature removes the hassle of remembering due dates and ensures timely payments directly from their bank accounts, boosting convenience and reliability.

Revenue Models for Pay-by-Bank Platforms

Pay-by-Bank platforms generate income by bridging direct bank-to-bank transactions while adding value for both merchants and users. Below are the key revenue models these platforms adopt:

1. Transaction Fees (Merchant-Paid)

Merchants are charged a small fee per transaction for using the Pay-by-Bank service. Even though fees are lower compared to card networks, this model ensures steady revenue for the platform with each payment processed.

2. Subscription Plans for Merchants

Some platforms offer tiered subscription models where merchants pay a monthly or annual fee for advanced services, such as fraud detection, analytics dashboards, API access, or faster settlement options.

3. Value-Added Services

Platforms monetize by offering additional services like currency conversion, reconciliation support, invoicing tools, or integration with ERP systems. Merchants pay for these features to simplify operations and improve efficiency.

4. Data Insights & Analytics

Aggregated and anonymized transaction data can be used to provide merchants with insights into customer behavior, spending patterns, and business performance. Merchants may pay for access to these detailed analytics to improve decision-making.

5. Partnerships with Banks & Financial Institutions

Platforms often partner with banks to earn referral commissions or shared revenue from payments processed. Banks benefit from increased transaction volumes and customer engagement, while platforms earn a share of the fees.

6. White-Label Solutions

Some Pay-by-Bank providers license their technology to banks, fintechs, or eCommerce platforms under a white-label model. This generates revenue through licensing fees or long-term contracts.

7. Premium User Features

For consumers, platforms can introduce paid premium features such as budgeting tools, instant refund options, cross-border payments, or credit score monitoring. These add-ons can become a secondary revenue stream.

How IdeaUsher Helps Develop Your Pay-by-Bank App?

IdeaUsher specializes in building secure, seamless, and scalable financial applications. Our developers ensure your Pay-by-Bank app integrates directly with banking networks, provides real-time payments, and delivers a user-friendly experience for consumers and merchants alike.

1. Consultation

We conduct a detailed consultation with our clients to understand business objectives, regulatory requirements, and target user needs. Our developers use this insight to define the app’s core features, workflows, and compliance strategy.

2. UI/UX Design & Feature Planning

Our developers design intuitive interfaces for both merchants and consumers, focusing on frictionless payment flows, dashboard clarity, and feature accessibility. We also plan essential modules such as instant payments, transaction history, and authentication.

3. Banking Network Integration

We integrate the app directly with banking APIs and payment gateways, enabling secure, instant bank-to-bank transactions. Our developers ensure seamless connectivity, real-time fund verification, and compliance with open banking standards.

4. Security & Compliance Implementation

Our team implements advanced encryption, two-factor authentication, and fraud detection mechanisms. We also ensure compliance with regulatory standards like PSD2, GDPR, and local banking regulations to protect users and maintain trust.

5. Testing, Deployment & Maintenance

We perform rigorous testing for performance, security, and usability. Post-launch, our developers provide continuous support, updates, and feature enhancements to keep the platform secure, scalable, and market-ready.

Conclusion

A pay by bank app provides clear benefits for both merchants and users. It simplifies transactions, reduces reliance on traditional card payments, and improves security. Merchants see faster settlements, lower transaction fees, and increased customer trust. Users appreciate convenience, real-time payments, and an easy checkout experience. By offering direct bank-to-bank transfers, these apps lower the risk of fraud and make financial management simpler. Using a pay by bank app modernizes payment processes and builds stronger relationships between businesses and their customers through reliability and efficiency.

FAQs

Merchants benefit from faster payment settlements, reduced transaction fees, and improved cash flow. These apps also minimize fraud risks and enhance customer trust, making business operations more efficient and reliable.

Users enjoy seamless and secure transactions, real-time payments, and direct bank-to-bank transfers. The convenience of avoiding cards and digital wallets makes purchases faster, simpler, and more transparent.

Yes, pay by bank apps use encryption, authentication protocols, and direct bank connections to ensure payments are secure. This reduces fraud risks and provides users and merchants with peace of mind.

These apps streamline expense tracking by recording real-time transactions. Users and businesses can monitor cash flow more efficiently, reduce errors, and make informed financial decisions.