The digital payments landscape is changing as businesses look for alternatives to traditional card-based transactions. Rising processing fees, settlement delays, and increasing fraud concerns are pushing the demand for better payment solutions. Creating a Pay-by-Bank checkout app is a direct response to these issues. It allows for direct bank-to-bank transfers that completely avoid card networks.

This change is especially noticeable in areas where Open Banking regulations are well established, like Europe and the UK. Companies such as Trustly have shown how powerful this method can be, allowing for instant payments while cutting down transaction costs.

Our hands-on experience in transforming complex financial technology into smooth, user-friendly solutions means we’re uniquely positioned to help you develop a Pay-by-Bank checkout system, one that supports instant payments, minimizes fraud, and gives you the competitive edge with seamless bank transfers. Having worked with clients to bring this vision to life, IdeaUsher understands the intricacies, and we’re putting together this blog to walk you through the process of launching your own successful platform.

Key Market Takeaways for Pay-by-Bank Checkout Apps

According to GrandViewResearch, the global digital payment market is set for rapid growth, expected to rise from $114.41 billion in 2024 to $361.30 billion by 2030, with a CAGR of 21.4%. A key driver of this growth is the increasing popularity of Pay-by-Bank checkout apps. These apps are becoming a go-to option for consumers seeking secure, easy, and low-cost payment solutions, especially as traditional payment methods become more cumbersome and expensive for merchants.

Source: GrandViewResearch

Pay-by-Bank apps facilitate direct transfers from bank accounts, bypassing card networks and reducing transaction costs. By using open banking and instant payment systems, they offer quick, secure payments without intermediaries.

As concerns about privacy and data security grow, many consumers are gravitating towards these apps because they reduce the risk of data breaches and simplify authentication, often using biometrics or secure logins.

Platforms like Trustly, Vyne, Plaid, and Tink are leading the charge, forging partnerships with e-commerce platforms, banks, and fintech companies to expand their reach.

For example, Trustly collaborates with PayPal and Stripe, while Plaid integrates Pay-by-Bank features with Shopify and Square, enabling merchants in diverse industries to offer this streamlined payment option. These partnerships are helping position Pay-by-Bank as a mainstream solution for global online commerce.

What is a Pay-by-Bank Checkout App?

A Pay-by-Bank Checkout App is a payment solution that allows customers to make payments directly from their bank accounts, bypassing traditional credit or debit cards. Essentially, it acts as a digital bridge between the merchant’s checkout page and the customer’s online banking system.

These apps rely on Open Banking regulations and secure APIs to facilitate direct payments from bank accounts. With this setup, there are several key benefits:

- No card networks involved: Transactions are made directly from the customer’s bank account, eliminating the need for credit/debit card networks like Visa or Mastercard.

- No sensitive financial details shared with merchants: Since the payment is initiated and processed by the bank, merchants do not receive any sensitive financial information, reducing the risk of data breaches.

- Payments authenticated through the customer’s own bank: The bank authenticates the payment, ensuring security and trust.

- Real-time transaction confirmation: Payments are confirmed instantly, allowing for quick and seamless transactions.

The Regulatory Landscape: Is It Legal?

Yes, Pay-by-Bank apps operate within a legal framework that prioritizes security and consumer protection. Some of the key regulations include:

- PSD2 (Payment Services Directive 2) in Europe: This regulation requires strong customer authentication and sets rules for third-party payment providers, ensuring secure transactions.

- Open Banking Standards in the UK: These standards define the technical specifications for securely connecting banks and payment providers.

- Local Equivalents: Countries like Brazil, Australia, and Canada have their own regulations in place to ensure security and transparency in financial transactions.

- GDPR Compliance: Pay-by-Bank apps must also comply with data protection laws, such as the General Data Protection Regulation (GDPR) in Europe, to safeguard personal data.

These regulations provide essential safeguards, ensuring that Pay-by-Bank providers maintain the highest security standards and protect both consumers and businesses.

Types of Pay-by-Bank Applications

Checkout Integrations

Pay-by-Bank apps are making checkout easier across different industries. For e-commerce, customers can pay with just one click. In travel bookings, instant payments for flights and hotels are now a breeze. And in retail, QR codes or mobile banking apps let you pay contactlessly at the counter. Simple, fast, and secure!

Industry-Specialized Solutions

Pay-by-Bank apps also cater to specific industries. In gaming and betting, they handle instant deposits and withdrawals. Marketplaces can split payments across multiple sellers, while bill payments make recurring utilities and subscriptions seamless. Plus, B2B payments simplify high-value transactions between businesses.

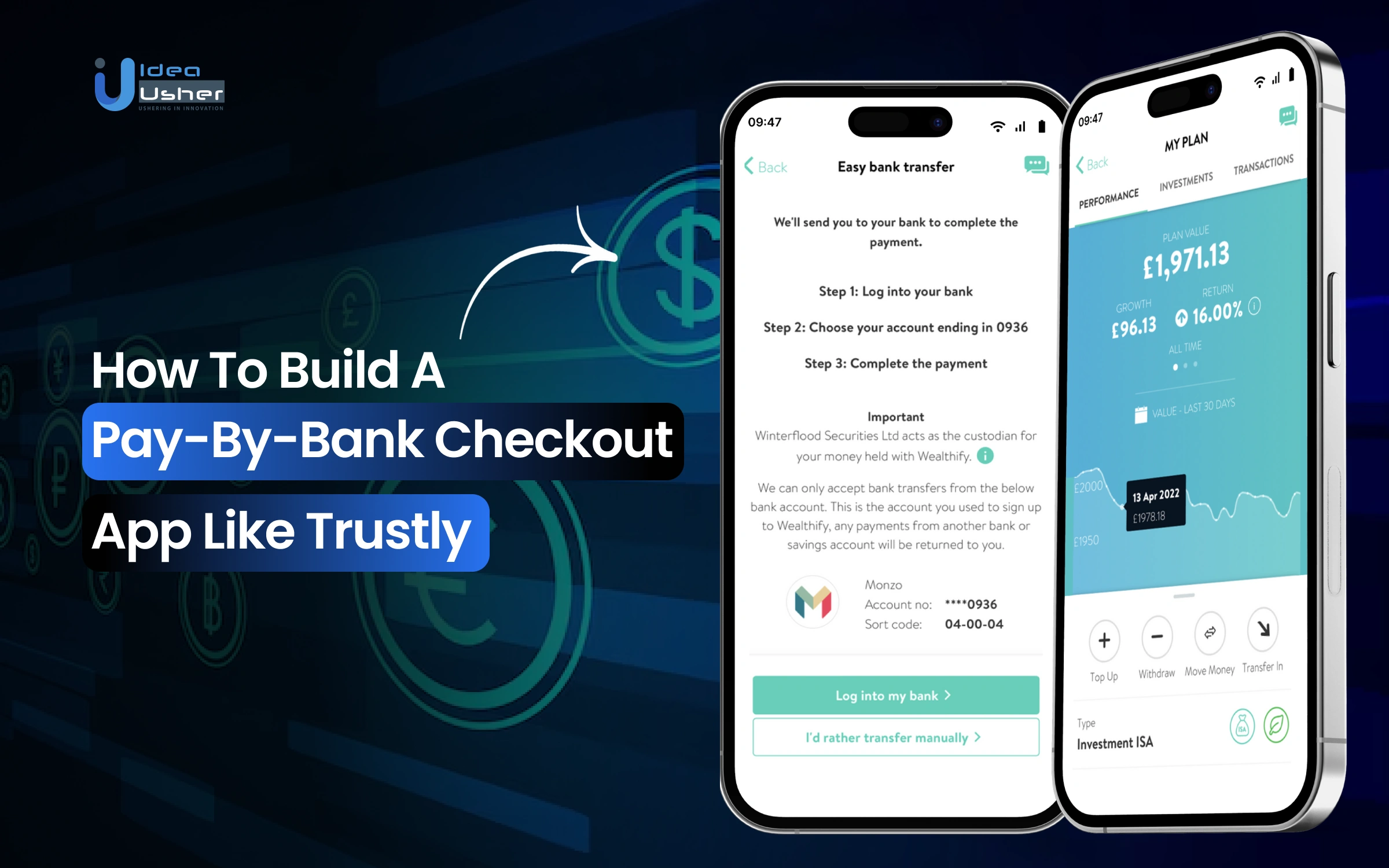

How Does the Trustly App Work?

Trustly makes payments simple by connecting directly with users’ bank during checkout, so they don’t need to enter card details. Users just select their bank, log in securely, and approve the payment. It’s quick, safe, and keeps banking info private.

The Key Players:

- Users (The Payers): The individuals ready to make a purchase.

- The Online Merchant: The website or service users are buying from, such as an e-commerce store, a travel platform, or even an online casino.

- The Bank: The institution holding the user’s funds, equipped with its own secure app and authentication methods.

- Trustly: The intermediary that makes the connection happen securely and efficiently.

Act 1: The Checkout – Choosing a Smarter Way to Pay

While shopping online, users will notice Trustly as a payment option on checkout. This might appear as “Pay by Bank” or with the Trustly logo. Often, merchants highlight benefits like “No card details required” or “Instant payment” to make it clear that users can skip entering credit card information.

Act 2: The Connection – Secure and Instant Recognition

Once users select Trustly, they’ll choose their country and bank. Trustly presents a list of supported banks in their country, and they pick the one they use. At this point, instead of entering sensitive data on the merchant’s site, users are securely redirected to their bank’s online environment. This is made possible through Open Banking APIs, ensuring that the connection is both secure and reliable.

Act 3: The Authentication – Users Are in Control

Now, users log into their bank’s online banking system using their usual credentials, like their username and password. Trustly uses Strong Customer Authentication for an extra layer of security. This often involves confirming the payment using a code from a mobile token or verifying their identity with a biometric scan (e.g., fingerprint or Face ID) through their banking app. This process is far more secure than typing in a credit card number.

Act 4: The Confirmation – Instant Results for Everyone

After logging in and authenticating, users will see the payment details pre-filled. They simply confirm the payment. Behind the scenes, Trustly gets instant confirmation from the bank that the payment has been authorized. This confirmation is sent to the merchant in real-time, and the purchase is finalized. Typically, this whole process takes less than 30 seconds.

Users are then redirected back to the merchant’s website or app with an order confirmation message, completing the transaction quickly and efficiently.

Why Merchants Love Trustly?

For merchants, Trustly is more than just another payment method—it’s a strategic tool that provides:

- Reduced Costs: Eliminates the fees typically associated with credit card transactions.

- Higher Conversion Rates: By streamlining the checkout process, Trustly reduces cart abandonment and boosts sales.

- Minimized Fraud: Trustly’s bank-level authentication drastically reduces the risk of chargebacks and fraud.

What is the Business Model of the Trustly App?

Trustly makes payments faster and safer by connecting merchants and consumers directly to their bank accounts, cutting out card-based systems. This helps businesses in e-commerce, gaming, and travel reduce fees, boost conversions, and lower fraud risks. With its smart data engine, Azura, Trustly ensures seamless transactions and has grown through global partnerships with banks.

Revenue Streams & Financial Performance

- Transaction Fees: Trustly’s primary source of revenue comes from transaction fees charged to merchants each time a customer completes a pay-by-bank transaction.

- AI-powered Recurring Payments: In June 2024, Trustly introduced a recurring payments service, offering merchants an easy way to facilitate repeat payments. This product enhances merchant retention and generates additional revenue.

- Data Engine Monetization: The Azura data engine indirectly contributes to Trustly’s revenue by improving payment conversion, making the service more valuable to merchants.

- Partnerships & Contract Wins: Strategic partnerships, particularly in North America and contracts with government entities like HMRC in the UK, provide a consistent and reliable source of revenue for Trustly.

In 2024, Trustly processed $87 billion in payments, marking a 54% increase year-over-year. This surge led to net revenue of $239 million, up 32% from the previous year. The company also posted an impressive adjusted EBITDA of $73.2 million, reflecting a 50% increase compared to 2023.

Trustly’s growth was supported by large-scale contract renewals and its expansion into new sectors, such as gaming and government payments.

Funding and Valuation

Trustly has raised over $30 million across five funding rounds, attracting notable investors such as BlackRock, Aberdeen Standard Investments, and the Investment Corporation of Dubai. As of June 2020, Trustly was valued at over $1 billion, with analysts projecting a potential IPO valuation between $7.3 billion and $11 billion in 2021.

The company remains privately held but has strong growth prospects driven by its expanding revenue base and increasing profitability, positioning it well for an eventual public offering.

Benefits of Pay-by-Bank Checkout Apps

Pay-by-Bank checkout apps make payments faster and more secure by connecting directly to customers’ bank accounts. With no card details involved, they reduce the risk of fraud and make checkout smoother for customers, cutting down on cart abandonment. Plus, businesses benefit from lower fees and quicker access to funds, helping to boost efficiency and cash flow.

For Businesses: Beyond Cost Savings to Strategic Advantage

1. Significant Reduction in Transaction Fees

Pay-by-Bank eliminates those pesky credit card interchange fees, cutting out the middlemen. By connecting payments directly from bank to bank, businesses save up to 2-3% per transaction—money that can be reinvested into growing your business or enhancing customer experiences.

2. Instant Settlement for Unprecedented Liquidity

With Pay-by-Bank, businesses enjoy near-instant settlement, drastically improving cash flow. You get faster access to funds, enabling better management of working capital and the flexibility to act on opportunities immediately, without being stuck waiting for traditional payment processing times.

3. Drastic Reduction in Fraud Liability

Fraud risks are significantly reduced with Pay-by-Bank, thanks to bank-level security features like biometric verification. Since transactions are authenticated within the customer’s own bank app, your business is protected from chargebacks and fraud liability, giving you more time to focus on growth.

For Customers: Checkout Should Feel Secure, Not Stressful

1. A Truly Frictionless Checkout Experience

Pay-by-Bank makes checkout a breeze, letting customers pay with just a few taps—often using fingerprint or face ID verification. No need to dig for a wallet or remember card details, making the shopping experience smoother and reducing cart abandonment.

2. Enhanced Security Through Data Minimization

Customers can shop with peace of mind, knowing their sensitive payment data is never shared or stored with merchants. By using direct bank transfers, Pay-by-Bank significantly reduces the risk of data breaches, strengthening trust between the customer and your brand.

3. Real-Time Transparency and Control

Pay-by-Bank keeps customers in the loop with real-time updates on transaction status. They see exactly how much is being deducted from their account and receive instant confirmation, providing transparency and putting them in full control of their financial decisions.

How to Build a Pay-by-Bank Checkout App?

We specialize in developing custom Pay-by-Bank checkout solutions for our clients. We focus on creating secure, seamless, and scalable payment experiences that comply with global regulations and meet user expectations.

1. Regulatory Readiness & Licensing

We ensure your Pay-by-Bank app complies with regulations like PSD2 and GDPR. We help decide whether to partner with a licensed provider or obtain licenses ourselves to meet the regulatory requirements for your business.

2. Secure Bank Connectivity

We integrate Payment Initiation Services and Account Information Services through Open Banking APIs, ensuring seamless bank connectivity. Our scalable architecture supports multiple banks, payment methods, and regional needs for smooth transactions.

3. Seamless Checkout Flow

We design a user-friendly checkout flow that minimizes friction. From the merchant’s checkout to bank redirects, biometric authentication, and instant payment approval, every step is streamlined for a fast, effortless experience.

4. Implement Advanced Security

Security is a top priority. We use tokenization, encryption, and multi-factor authentication to protect transactions. Real-time fraud detection powered by machine learning ensures continuous monitoring and protection from fraud.

5. Add Analytics & Merchant Tools

We provide merchants with dashboards for tracking settlements and real-time reconciliation. With customer consent, we offer valuable insights into customer behavior, helping merchants optimize operations and boost revenue.

6. Testing & Scaling

We conduct thorough sandbox testing with partner banks to ensure everything works smoothly. After initial rollout, we gradually expand to more geographies and continuously optimize for API variations, ensuring scalability and global reach.

Tools & APIs for a Checkout App like Trustly

When creating a Pay-by-Bank application, you’re essentially building a secure, high-speed bridge between merchants and customers’ banks. To ensure it’s strong, safe, and efficient, you need the right tools, APIs, and frameworks. Here’s a breakdown of the critical components that will power your solution:

1. The Foundation: Open Banking APIs

Open Banking regulations have reshaped the financial landscape, requiring banks to offer secure APIs for third-party providers to initiate payments and access account data with user consent. These APIs are the essential building blocks of any Pay-by-Bank application.

- Payment Initiation Services (PIS): This is the core API for moving money. It enables your application to instruct the customer’s bank to transfer funds directly to the merchant’s account. When the user approves a payment, the PIS API is triggered to complete the transaction.

- Account Information Services (AIS): These APIs are used to securely retrieve account details, such as account holder name and balance. AIS enables features like pre-filling forms or verifying available funds, creating a smoother experience for users.

2. The Guardian: Fraud & Risk Engines

Fraud prevention is paramount in payments. A strong risk engine acts as the safeguard for each transaction, analyzing patterns and identifying potential fraud before it can occur.

- Third-Party Solutions: You can integrate with established fraud-prevention providers like LexisNexis, Riskified, or Sift. These platforms use machine learning algorithms trained on vast datasets to detect suspicious transactions in real time.

- Custom-Built Engines: For businesses with unique needs, creating a custom risk engine can provide a competitive advantage. By using machine learning models tailored to your transaction data, you can pinpoint fraud patterns that are specific to your customer base or industry.

3. The Vault: Security Tools

Security isn’t just an add-on; it’s part of the foundation. Every interaction must be protected from end to end.

- Encryption: All data, both in transit (using TLS 1.3) and at rest, must be encrypted to ensure that sensitive information remains unreadable, even if intercepted.

- Tokenization: Instead of storing sensitive bank account information, use tokenization to replace it with a unique, random string of characters. If your system is compromised, attackers will only encounter useless tokens.

- Multi-Factor Authentication (MFA): While banks handle user authentication, your system should incorporate MFA (e.g., using Auth0 or Okta) for internal systems and admin panels. This adds an extra layer of protection against unauthorized access.

4. The Air Traffic Controller: Payment Orchestration Platforms

As you scale and connect with more banks, managing those integrations can get tricky. A payment orchestration platform simplifies this by offering a single API that links you to multiple banks and payment methods. It boosts reliability, reduces costs by picking the best payment route, and helps you expand faster into new regions.

5. The Workshop: Developer Tools

Behind every smooth application is a team of developers using the right tools to build, test, and manage the infrastructure.

- API Development & Testing (Postman, Swagger): Tools like Postman are indispensable for testing API calls during development, while Swagger (or OpenAPI) helps you design, document, and maintain clear and consistent APIs.

- API Gateways (Kong, AWS API Gateway): An API gateway serves as the main entry point for API requests. It handles critical tasks such as rate limiting, caching, authorization, and routing, ensuring the system remains secure and manageable.

Use Case: E-Commerce Checkout with Pay-by-Bank

Our client came to us struggling with a high cart abandonment rate, shoppers loved their items but bailed at checkout. The reason? Digging for wallets, typing in long card numbers, and security worries made the process feel frustrating and outdated. They needed a simpler, smoother solution to match their brand’s modern vibe, and that’s exactly what we set out to create.

Our Solution: Simplifying Payment with a Single Tap

Instead of adding another payment method and calling it a day, we decided to rethink the entire checkout experience. We integrated a Pay-by-Bank feature, designed to streamline the final step of the customer journey. Here’s how it works for Sarah, a typical shopper:

Finding the Perfect Item: Sarah spots a beautiful handcrafted item and adds it to her cart. She’s ready to make a purchase.

Choosing a Better Way to Pay: At checkout, instead of seeing the usual credit card fields, Sarah is presented with a clean, secure option: “Pay directly from your bank.” She selects it.

Instant, Secure Approval: With a tap, her phone prompts her to open her banking app—the same one she uses for daily transactions. Sarah quickly authenticates the payment with her fingerprint. No typing, no sharing of sensitive details.

Instant Confirmation for All Parties:

- For Sarah: The website instantly confirms the transaction with a simple message: “Payment Approved! Your order is confirmed.” She receives her receipt right away, completing the transaction in seconds.

- For the Business: The system sends an instant settlement confirmation, guaranteeing the funds. This eliminates the risk of fraud or chargebacks, offering a faster, more reliable cash flow.

The Result: A Checkout Process That Converts

By removing the friction from the checkout process and addressing the anxiety associated with traditional payment methods, we helped the marketplace achieve meaningful results:

- 22% reduction in cart abandonment at the payment stage.

- Instant settlement led to faster, more reliable cash flow.

- Enhanced customer trust by leveraging the security of the bank customers already use.

The success of the project wasn’t just about the technology we built; it was about understanding the psychology of a shopper. By creating a seamless, frictionless payment experience, we empowered Sarah and others like her to feel confident and secure in completing their purchases, every time.

Conclusion

Pay-by-Bank is revolutionizing online checkout by offering businesses a more efficient, cost-effective, and secure alternative to traditional payment methods. Early adoption of this solution allows companies to reduce transaction fees, streamline their cash flow, and enhance the customer experience with faster, frictionless payments. Idea Usher is equipped to help enterprises and platform owners integrate Pay-by-Bank solutions seamlessly, ensuring robust security and compliance every step of the way.

Looking to Develop a Pay-by-Bank Checkout App?

It’s time to move past outdated payment systems. Partner with Idea Usher to create a cutting-edge Pay-by-Bank app that keeps you ahead of the competition. We combine technical expertise with a proven track record to turn your vision into reality.

- Elite Technical Expertise: Tap into over 500,000 hours of coding experience from ex-MAANG/FAANG engineers who know how to build robust, scalable solutions.

- Secure by Design: Security is our top priority. We ensure your app is fully compliant, building both user trust and peace of mind.

- Proven Results: Don’t just take our word for it—check out our portfolio to see how we’ve turned innovative ideas into industry-leading applications.

Ready to build the future of payments? Let’s get started!

FAQs

A1: Pay-by-Bank operates on a direct A2A model, eliminating the need for card networks. Unlike traditional card payments, which rely on intermediaries like card issuers and processors, Pay-by-Bank transactions occur directly between the payer’s bank account and the merchant’s, offering faster processing and reduced fees.

A2: Pay-by-Bank apps prioritize security by using bank-grade authentication methods, such as biometrics and multi-factor authentication, ensuring a high level of protection. These apps do not store payment credentials, minimizing the risk of data breaches and fraud.

A3: Yes, Pay-by-Bank can be used for recurring payments through consent-based mandates and seamless API integrations. This allows businesses to set up automatic payments while maintaining full transparency and security for both parties.

A4: The licensing requirements for launching a Pay-by-Bank app vary depending on your jurisdiction. Typically, you may need a Payment Initiation Service license, or you can integrate with a licensed partner to ensure compliance with local regulations.