Frequent system downtimes, higher processing fees, and long settlement times are pushing merchants to look for new options that offer cost savings and better customer experiences. This change has led to a growing interest in pay-by-bank merchant apps. This app allows direct bank-to-bank transfers, cutting out middlemen and enabling real-time transaction processing.

Unlike traditional payment methods that use card networks, pay-by-bank solutions like Banked connect customers straight to their banks. This creates a smooth link between consumer accounts and merchant systems. Businesses that can adopt this pay-by-bank technology early on can place themselves at the front of the digital commerce shift. They become ready to meet changing market needs while improving their profits.

We’ve helped several businesses transition to seamless bank-to-bank transactions, integrating features like instant settlements and bank-level security that enhance both merchant and customer experience. IdeaUsher has facilitated such transitions for multiple clients, ensuring that the shift to pay-by-bank is as smooth as possible. This blog is our way of passing on valuable information on how you can get started with a platform like this.

Key Market Takeaways for Pay-by-Bank Merchant Apps

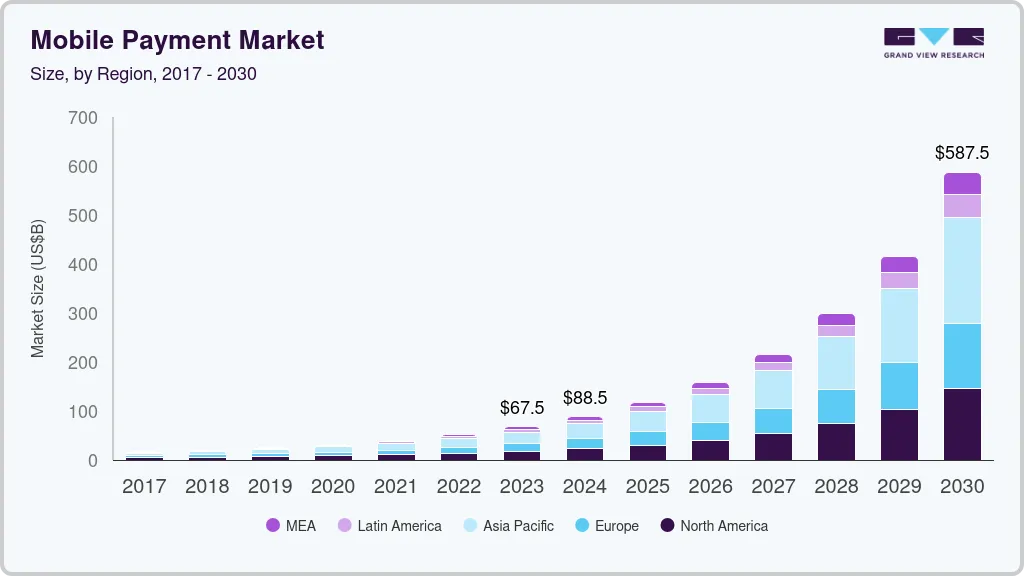

According to GrandViewResearch, the global mobile payment market is set for explosive growth, expected to rise from USD 88.50 billion in 2024 to USD 587.52 billion by 2030. A significant driver of this surge is the increasing adoption of Pay-by-Bank merchant apps, which allow direct payments from one bank account to another, bypassing traditional card systems. This not only reduces transaction fees for merchants but also makes these apps an essential tool for e-commerce, retail, and subscription-based businesses.

Source: GrandViewResearch

These apps rely on open banking APIs and real-time payment systems, ensuring secure and seamless transfers. Leading platforms like Trustly, GoCardless, Plaid, and Tink are at the forefront of this trend, expanding their services through partnerships with major banks and payment processors.

For instance, Trustly has partnered with global brands like PayPal and DraftKings, offering frictionless bank payments worldwide, while GoCardless supports subscription businesses with direct bank payments.

Strategic partnerships are further accelerating the adoption of Pay-by-Bank services. In 2024, Mastercard teamed up with Trustly to expand these payment options for U.S. merchants, while Plaid deepened its collaboration with JPMorgan Chase to streamline the process for merchants adopting Pay-by-Bank solutions. These partnerships are helping to pave the way for a more efficient and cost-effective payment landscape.

What is a Pay-by-Bank Merchant App?

A Pay-by-Bank Merchant App is a digital payment solution that enables businesses to accept payments directly from a customer’s bank account to the business’s account, bypassing traditional credit card networks. This streamlines the payment process and often reduces costs associated with third-party intermediaries like Visa or Mastercard.

Here’s how it works in practice:

- Open Banking APIs: These are secure channels that allow regulated apps to initiate payments directly from a customer’s bank account, but only with the customer’s explicit consent. This bypasses traditional card networks entirely.

- Instant Payment Networks: These networks, such as PayTo in Australia, SEPA Instant in Europe, or FedNow in the US, enable payments to be settled in real-time, making the entire transaction much faster than traditional card-based systems. Essentially, it’s like building a direct, high-speed connection between the customer’s bank and the business’s treasury, bypassing the usual delays and fees of card networks.

The Three Main Archetypes of Pay-by-Bank Apps

While the idea of Pay-by-Bank is innovative, there are different ways this technology is being applied. Most providers fall into three key categories, and choosing the right one depends on your business goals.

| Type | What They Are | Best For |

| Domestic Specialist (e.g., PayTo in Australia) | Payment solutions for a single country’s instant payment network. | Businesses operating in one region seeking a cost-effective, localized solution. |

| Global Aggregator (e.g., Banked) | Single API connecting multiple global payment networks. | Growing businesses with international customers or ambitions, like e-commerce or SaaS. |

| Sector-Specific Solution | Tailored for industries with unique payment needs (e.g., travel, B2B). | Businesses with specialized payment needs, such as recurring billing or large transactions. |

How Does the Banked App Work?

The Banked app is designed to make payments feel effortless, ensuring a quick and secure transaction for both customers and merchants, in a world where speed and security matter, the Banked app transforms the way payments are made, creating a smooth, trusted, and efficient experience.

With strategic acquisitions, such as the recent purchase of the Australian “Pay by Bank” provider, Waave, and the UK-based VibePay, Banked is setting the stage for a global payments network that can rival credit card systems. The core of this service is Pay by B, which connects customers directly to their bank accounts for secure, immediate payments.

The Customer’s Journey: Simplicity in Three Clicks

For the customer, Pay by B is the fastest, most secure way to pay online. The entire experience is built on familiarity and trust.

Step 1: Choose Pay by B at Checkout

The journey begins at the most critical point: your checkout page. Alongside traditional payment options, the customer selects the Pay by B button. This single click signals their intent to pay directly from their bank account, bypassing cards altogether.

Step 2: Seamless Redirect to a Trusted Environment

Instead of being asked to type in cumbersome card details, the customer is instantly and securely redirected to a place they know and trust: their own banking app or internet banking portal.

This is the core of the security model. Pay by B never asks for or stores your customer’s online banking credentials. The authentication happens entirely within the secure walls of their financial institution.

Step 3: Authorize with a Touch or a Glance

Inside their banking app, the customer sees the payment details—merchant name and amount. To approve, they simply use the biometric authentication they use every day: a fingerprint (Touch ID) or facial recognition (Face ID). Alternatively, they might use their bank PIN or MFA. This step leverages the immense security infrastructure the banks have already built.

Step 4: Instant Confirmation and Return

The moment they authorize the payment, they are automatically redirected back to the merchant’s website or app with a confirmation message: “Payment Successful.” The experience is frictionless, fast, and secure.

The Merchant’s Experience

While the customer enjoys simplicity, the merchant reaps the benefits of a powerful financial engine. Here’s what happens on your end.

Step A: The Secure Payment Initiation

When the customer clicks the Pay by B button, your system sends a secure, encrypted API call to the Pay by B platform. This request contains the payment amount and a unique reference ID.

Step B: Orchestration via the PayTo Network

The Pay by B platform acts as an intelligent orchestrator. It takes the payment request and routes it through Australia’s real-time payment rail, the PayTo network. PayTo is the modern standard designed specifically for these kinds of pre-authorized, account-to-account payments.

Step C: Real-Time Authentication and Settlement

This is where the magic happens simultaneously:

- The customer authenticates in their banking app.

- The bank sends an approval signal back through the PayTo network.

- The funds are instantly transferred from the customer’s bank account and settled directly into your merchant account. The delay of 1-3 business days associated with card payments is completely eliminated.

Step D: Instant Notification and Fulfillment

As soon as the payment is confirmed, the Pay by B platform sends an instant notification (a webhook) to your system. This automation allows you to:

- Immediately update the order status to “paid.”

- Trigger a fulfillment process (e.g., send a download link, confirm a booking).

- Update your inventory in real-time.

This creates a completely seamless, automated operational flow.

Why is This a Game-Changer?

Unlike traditional card payments, Banked offers instant payment authorization and settlement, significantly lowering fees by bypassing intermediaries and shifting liability for sensitive data security to the bank. This streamlined, automated system helps merchants boost conversion rates and operational efficiency.

| Aspect | Traditional Card Payment | Banked (via Pay by B) |

| Authentication | Typing 16-digit numbers, CVV, expiry dates. | Biometrics in your banking app. Secure and familiar. |

| Speed | Authorization in seconds, but settlement takes days. | Instant authorization and settlement. |

| Cost | High interchange fees (1.5% – 3%). | Drastically lower fees by cutting out intermediaries. |

| Security | Merchant stores sensitive card data, liable for breaches. | No sensitive data stored. Liability shifts to the bank. |

| Experience | Friction-filled forms lead to cart abandonment. | One-click flow after first use increases conversion. |

What is the Business Model of the Banked App?

Banked earns revenue by charging merchants a fee for each transaction processed through its Pay by Bank system, enabling instant bank payments without relying on card networks. As more merchants and customers adopt this method, transaction volume grows, boosting revenue. Strategic acquisitions like Waave and VibePay also help Banked expand globally, strengthening its market presence and technical capabilities.

Revenue Streams:

- Transaction Fees: The primary source of revenue comes from the fees Banked charges merchants each time a customer completes a Pay by Bank transaction at checkout.

- Volume Growth: As more merchants and consumers adopt the Pay by Bank system, Banked benefits from increased transaction volume, which scales the company’s revenue.

- Strategic Acquisitions: By acquiring companies like Waave and VibePay, Banked strengthens its technical capabilities and expands its market reach, which enhances its ability to generate revenue globally.

Financial Performance and Market Impact

Banked has recently focused on growing its presence both locally and internationally, with significant strides made through the acquisition of Waave.

Although specific financial figures are not available, the increasing transaction volumes and positive feedback from clients such as Eva and Oz Hair & Beauty suggest strong growth. Merchants report reduced fees and greater flexibility at checkout, driving Banked’s continued success in the competitive payments sector.

Funding and Growth Strategy

Banked raised $20 million in Series A funding, showing strong investor confidence in its ability to challenge traditional card payments. With offices in key global cities, the company is primed for international growth. Its strategic acquisitions and innovative payment solutions are setting it up for success in the global payments market.

Benefits of Pay-by-Bank Merchant Apps for Businesses

Pay-by-Bank merchant apps simplify payments by directly linking to customers’ bank accounts, reducing transaction fees. They offer faster, secure transactions and lower fraud risks, which is great for businesses looking to improve efficiency.

1. Drastically Reduced Transaction Fees

Card payments come with high transaction fees, often ranging from 1.5% to 3.5%, eating into your profits. Pay-by-Bank cuts out the middlemen, enabling direct A2A transfers. This can reduce transaction costs by up to 80%, allowing you to reinvest those savings into your business for growth.

2. Instant Settlement & Cash Flow

Traditional card payments can take 3-5 business days to settle, creating uncertainty around cash flow. Pay-by-Bank enables near-instant settlement, meaning funds are available as soon as a customer approves payment. This allows you to better manage your working capital and operate with financial agility.

3. Elimination of Fraud & Chargebacks

With card payments, fraud and chargebacks are often a merchant’s responsibility, leading to costly disputes. Pay-by-Bank shifts the fraud liability to the customer’s bank by using biometric or multi-factor authentication, virtually eliminating the risk of chargebacks and fraud, saving both time and money.

4. Enhanced Security

Storing card details exposes businesses to security risks and compliance burdens. Pay-by-Bank eliminates this by allowing payments through a secure channel with the bank, using tokenization. This reduces the risk of data breaches, builds trust with customers, and simplifies compliance.

5. Frictionless Customer Experience

Lengthy checkout forms are a major cause of cart abandonment. With Pay-by-Bank, once a customer links their bank account, future purchases are made in a single click with biometric approval. This streamlined process leads to higher conversion rates and a better overall shopping experience.

6. Easy Global Expansion

Expanding into new markets often requires dealing with different payment systems and complex integrations. Pay-by-Bank simplifies this by offering a single API that connects you to global payment networks. This reduces the time and cost of expansion, letting you quickly serve new markets with local payment methods.

How to Develop a Pay-by-Bank Merchant App?

We specialize in developing secure and seamless Pay-by-Bank merchant apps for businesses. Our end-to-end approach ensures that we handle every step, from compliance to final deployment, helping clients provide customers with fast, secure, and easy payment solutions.

1. Regulatory & Banking Ecosystems

We start by ensuring compliance with open banking regulations such as PSD2 and CDR. We also identify and integrate instant payment networks like PayTo, SEPA Instant, and FedNow, enabling fast and secure transactions across regions.

2. Core Payment Infrastructure

Our team builds a reliable core payment system with an event-driven architecture to support instant A2A transfers. We also ensure secure and efficient clearing mechanisms to maintain settlement integrity, providing seamless transactions.

3. Bank Connectivity & APIs

We integrate open banking APIs to securely link bank accounts and authorize transactions. Our scalable middleware connects with multiple global banks, ensuring flexibility and easy payments for customers worldwide.

4. Security & Authentication

Security is a priority. We implement biometric or multi-factor authentication (MFA) through bank apps. Tokenization and end-to-end encryption further protect sensitive data, ensuring transactions are secure at all stages.

5. Merchant & Customer Dashboards

We create easy-to-use dashboards for merchants and customers. Merchants get tools for real-time transaction tracking, reporting, and analytics. Customers enjoy one-click payments and access to their transaction history for better financial oversight.

6. Testing & Global Scaling

We rigorously test the app with partner banks in sandbox environments and certify it against regional compliance frameworks. After passing all tests, we scale the app globally, ensuring smooth performance and compliance across multiple markets.

Tools & APIs for Pay-by-Bank Merchant Apps

To build a cutting-edge Pay-by-Bank app, a combination of essential tools, APIs, and frameworks is required to deliver seamless integration, robust performance, and security. Below are the core components of the system:

1. The Connectors: APIs That Bridge Worlds

The success of a Pay-by-Bank app depends on its ability to communicate effectively with banks and payment networks. Here’s how we do it:

Aggregator APIs (TrueLayer, Plaid, Tink)

These are pre-built services that provide quick access to hundreds of banks, allowing rapid market entry. They abstract the complexities of individual bank APIs and offer consistent connectivity, speeding up MVP validation and initial development.

Direct Bank APIs (PSD2, PayTo)

For clients needing low-latency, high-performance integration, we directly interface with bank APIs. This approach ensures control over performance and cost optimization, especially when targeting regional markets like Australia’s PayTo network.

2. The Payment Highways

The API triggers payments, but the real magic lies in the network that moves funds quickly and reliably. Here’s how we leverage the best payment rails:

| Payment Network | Region | Description |

| PayTo | Australia | A real-time, data-rich payment standard ensuring seamless transactions in the Australian market. |

| SEPA Instant | European Union | Enables instant euro payments across Europe, offering real-time transfers. |

| Faster Payments | United Kingdom | Powers real-time sterling payments in the UK, facilitating lightning-fast transactions. |

| FedNow | United States | Emerging real-time payment network in the U.S., designed to handle rapid, secure payments. |

3. The Fortress: Security That Builds Trust

Security isn’t just an add-on; it’s the cornerstone of every financial transaction.

- OAuth 2.0 & FAPI (Financial Grade API): We employ the highest standard of authentication for financial transactions, ensuring robust protection against sophisticated attacks through FAPI, a gold-standard protocol.

- Tokenization: To protect sensitive data, we use tokenization, replacing actual bank account details with non-sensitive tokens. This minimizes PCI DSS compliance scope and virtually eliminates the risk of data breaches.

4. The Engine Room: Frameworks That Scale

The backend and frontend systems are the backbone of the application’s performance and scalability.

Frontend (React Native, Flutter): These frameworks are chosen for their ability to create high-performance, cross-platform mobile apps. They enable rapid development, maintainability, and consistent user experiences across both iOS and Android.

Backend (Node.js, Python/Django, Java/Spring Boot)

- Node.js: Ideal for real-time applications requiring high I/O operations.

- Python/Django: Chosen for rapid development and clean, scalable code.

- Java/Spring Boot: The go-to framework for large-scale, enterprise systems demanding maximum robustness.

Database (PostgreSQL, MongoDB): We usually prefer PostgreSQL for its ACID compliance and support for complex queries, crucial for financial reporting and operations. However, we are flexible and choose the database that best fits the client’s data needs and architecture.

5. The Intelligence: Analytics That Drive Growth

To transform a payment system into a strategic asset, data-driven insights are key.

Snowflake & BigQuery

For large-scale enterprises, we integrate with powerful cloud platforms like Snowflake and BigQuery. This allows for extensive analysis of transaction trends, customer behavior, and operational performance.

Custom Dashboards

We create real-time dashboards that provide a clear view of financial performance, such as conversion rates, payment method preferences, and settlement times. This turns raw data into actionable insights, helping businesses make more informed decisions.

Use Case: Enterprise Merchant Integration

Our client, a global e-commerce leader, was facing a tough situation, growing fast but losing millions to interchange fees and a slow payment system. Their cash flow was stuck in a 3-5 day cycle, fraud costs were eating away at profits, and their checkout process was losing customers. They came to us looking for a fresh approach to fix these issues and reimagine how payments worked.

Our Solution: A Strategic Pivot, Not a Quick Fix

When they came to us, the challenge wasn’t just about adding a payment method—it was about completely rethinking how money moved between them and their customers. We introduced Pay-by-Bank technology through Banked’s API, aiming for a seamless, unified payment network across all regions. With our experience in global integrations, we knew how to customize this solution to fit their exact needs.

Phase 1: The Architecture of Autonomy

We started by building a custom integration layer, which acted as a smart router to connect their regional platforms to Banked’s single API. This streamlined everything into one global payment endpoint, eliminating the need for multiple systems. It was a simple, efficient way to link to local payment systems like PayTo and Open Banking.

Phase 2: Frictionless by Design

Next, we revamped the checkout flow. We made Pay-by-Bank the preferred payment option, guiding customers through a seamless, secure experience. The design focused on simplicity: customers could authenticate payments directly through their banking app using biometrics, a method they were already familiar with and trusted.

Phase 3: Data as a Deliverable

We didn’t stop at just payments. We built a custom analytics dashboard that transformed raw payment data into valuable insights. This allowed our client to better understand customer behavior and make informed decisions about their global operations.

The Results: A Payment Transformation

The transformation was immediate and undeniable. Within the first quarter of operation, the impact was clear:

- Eliminating the Fee Drain: By bypassing card networks, we cut payment processing fees by over 80%. Millions of dollars previously lost to fees were redirected into the client’s innovation fund.

- Cash Flow Transformed: With instant settlements, funds were available as soon as customers approved payments. This new dynamic unlocked the ability to reinvest quickly, improving cash flow and operational flexibility.

- Fighting Fraud with Confidence: Fraud-related costs dropped by 60%. By authenticating payments directly with the customer’s bank, we shifted the fraud liability away from our client and into the bank, drastically reducing chargebacks.

- Breaking the Checkout Ceiling: The frictionless, one-click payment option led to a 20% increase in checkout conversion rates. We didn’t just save them money, we made them money by improving their conversion process.

Conclusion

Pay-by-Bank merchant apps are the future of digital payments, offering businesses the benefits of instant settlements, lower fees, and enhanced security. By adopting these solutions, companies can see a higher return on investment while building greater trust with their customers. As open banking adoption grows, platform owners and enterprises must act quickly to stay ahead of the curve. Idea Usher is ready to support businesses in integrating secure, scalable, and future-ready Pay-by-Bank solutions that drive long-term success.

Looking to Develop a Pay-by-Bank Merchant App?

Traditional payment systems are bogged down by high fees, fraud risks, and unnecessary friction. It’s time for a direct connection to your customers’ wallets. At Idea Usher, we help forward-thinking businesses launch their own Pay-by-Bank Merchant Apps, offering reduced transaction costs, instant settlements, and top-tier security. We don’t just write code; we create competitive advantages that push your business forward.

Why Build with Us?

- Elite Technical Expertise: With over 500,000 hours of coding experience, our team of ex-MAANG/FAANG developers designs solutions that are not only functional but also game-changing.

- Proven Excellence: Don’t just take our word for it—explore our latest projects to see the high-caliber work we consistently deliver.

Ready to leave behind the old payment system and start building your future?

Let’s create something innovative together.

FAQs

A1: Pay-by-Bank apps cut out card networks, offering direct account-to-account transfers that result in lower transaction costs and enhanced security. This streamlined process eliminates intermediaries, reducing fees, speeding up transactions, and providing a safer payment experience.

A2: Banked stands out with its global reach, strong partnerships, and innovative merchant incentives. Their scalable APIs empower businesses to integrate Pay-by-Bank seamlessly, creating a more efficient, cost-effective payment system with international capabilities.

A3: Pay-by-Bank transactions are highly secure, using multi-layered authentication through banking apps, including biometrics, tokenization, and encryption. These measures ensure that sensitive payment information remains protected throughout the transaction process.

A4: Pay-by-Bank apps are particularly beneficial for industries like e-commerce, travel, SaaS platforms, marketplaces, and subscription-based businesses. These sectors can leverage the speed, security, and reduced costs of Pay-by-Bank to improve customer experience and streamline payment processes.