(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Traditional insurance often faces issues like slow claims, unclear terms, and a lack of transparency. These problems can frustrate both businesses and customers. As people become more comfortable with digital solutions, blockchain is starting to change the way insurance operates. On-chain insurance platforms use smart contracts to automate coverage, verify claims right away, and keep all transactions safe on a public ledger. This helps reduce disputes and builds more trust between insurers and policyholders.

By bringing insurance processes on-chain, businesses can offer faster payouts, verifiable data, and globally accessible coverage models. From parametric insurance to DeFi-backed protection pools, this technology opens a new era of transparency and efficiency that legacy systems could never achieve.

In this blog, we’ll look at the main factors that affect the cost of building an on-chain insurance platform, covering core features, the technology stack, blockchain infrastructure, and what businesses should consider before launching their own blockchain-based insurance solution. With hands-on experience in delivering Web3 products, IdeaUsher helps businesses plan efficiently and invest in the right areas for scalable growth.

What is an On-Chain Insurance Platform?

An on-chain insurance platform is a decentralized system that runs fully on the blockchain. This setup allows for transparent, automated, and trustless insurance processes. Unlike traditional or hybrid models, all main tasks like issuing policies, handling premium payments, checking claims, and making payouts are managed by smart contracts instead of a central authority.

These platforms use oracles to fetch real-world data (like weather, flight statuses, or asset prices) that trigger insurance events automatically when conditions are met. This removes manual claim checks, reduces fraud, and ensures quicker, reliable settlements.

- Smart Contract Automation: Replaces manual claims handling with self-executing digital contracts.

- Data-Driven Triggers: Real-time data from trusted oracles activate payouts instantly upon event verification.

- Transparency & Immutability: All transactions and rules are publicly verifiable on the blockchain.

- Decentralized Governance: Policy terms, fund management, and updates are managed by DAOs or community consensus.

- Global Accessibility: Anyone can create or purchase insurance products without geographical or institutional barriers.

How On-Chain Insurance Platform Works?

An on-chain insurance platform uses blockchain to automate policy management and claims through transparent, tamper-proof smart contracts. It removes intermediaries, ensuring faster payouts, lower costs, and greater trust between insurers and users.

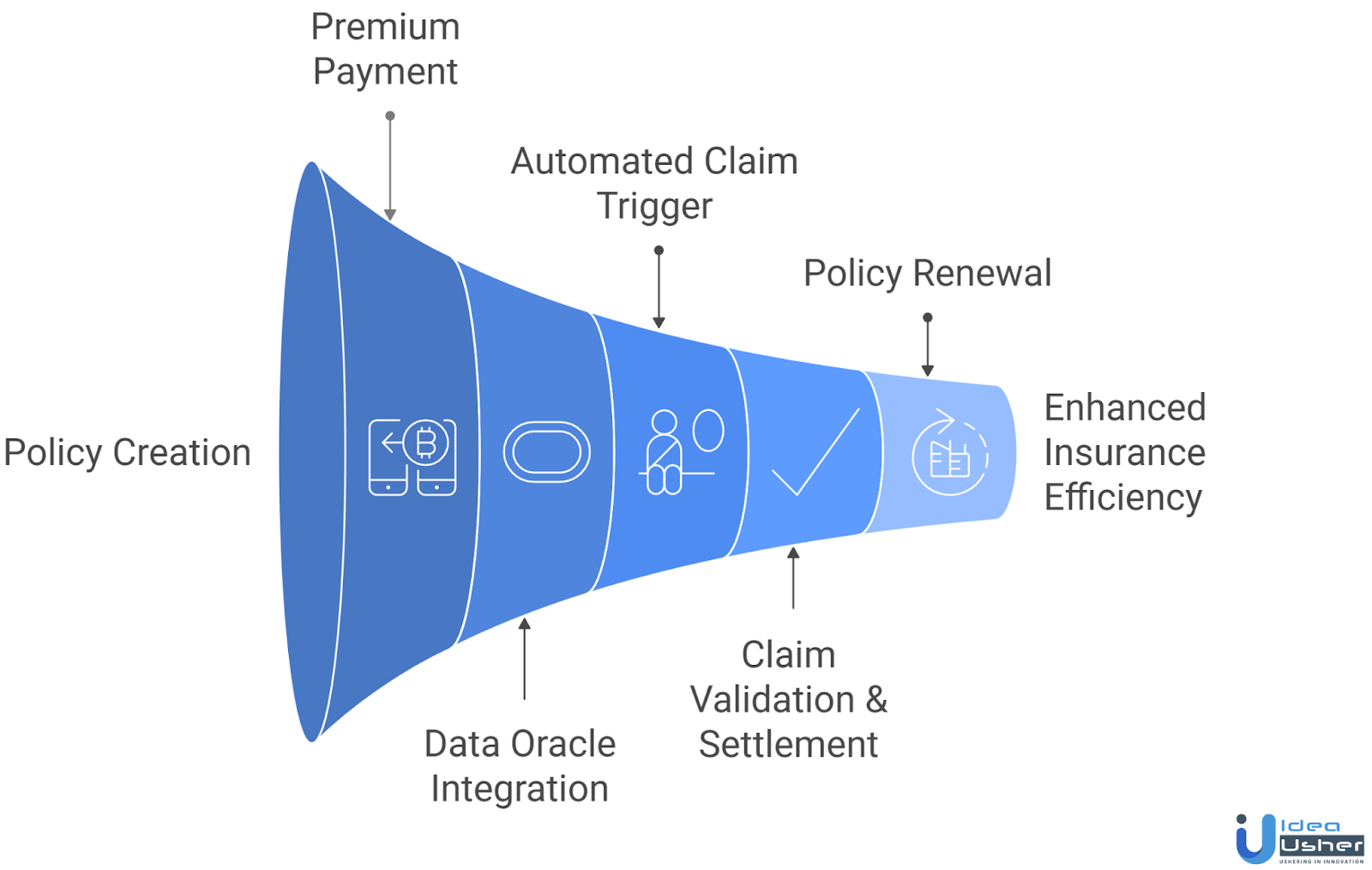

1. Policy Creation & Smart Contract Deployment

Insurance providers or users create policies directly on the blockchain. Each policy is encoded as a smart contract, defining parameters such as coverage type, premium, payout amount, and triggering conditions. Once deployed, the contract becomes immutable and self-executable.

2. Premium Payment & Policy Activation

Users purchase the policy by paying premiums in cryptocurrency or stablecoins. The payment automatically triggers the activation of the smart contract, storing proof of purchase and coverage details on-chain for full transparency.

3. Data Oracle Integration

External data oracles, such as Chainlink or API3, bring real-world information like weather, flight details, or asset prices into the blockchain. This helps contracts use accurate and secure data when evaluating claims.

4. Automated Claim Trigger

When predefined parameters (like rainfall threshold or flight delay duration) are met, the smart contract automatically recognizes the event. This eliminates the need for manual claim submission or investigation.

5. Claim Validation & Settlement

The smart contract instantly verifies data from the oracle. If the claim conditions are satisfied, the payout is automatically released to the policyholder’s crypto wallet. If not, the contract remains inactive until the condition occurs or the coverage period ends.

6. Reinsurance & Liquidity Management

The platform may integrate liquidity pools where investors stake funds to back insurance coverage. These pools ensure sufficient reserves for payouts and allow investors to earn yield from premium contributions.

7. Transparency & Auditability

Every transaction, from collecting premiums to making payouts, is recorded on the blockchain. This creates a secure audit trail that helps build trust among users, insurers, and investors.

8. Policy Renewal

After the policy term ends or a claim is settled, users can renew or modify their policies directly on-chain. Meanwhile, insurers analyze on-chain data and oracle feedback to improve smart contract logic, pricing models, and coverage efficiency for future policies.

Types of Blockchain-Based Insurance Platforms

Blockchain technology has given rise to several innovative insurance models, each tailored to specific user needs, business models, and automation levels. Below are the main types of blockchain-based insurance platforms:

1. Parametric Insurance Platforms

These platforms use triggers (weather, delays, crop yield) to automate payouts without manual claims. They rely on smart contracts and oracles for real-time tracking, ensuring faster, transparent settlements.

Example: Etherisc uses smart contracts and oracles to automate claim settlements for crop, flight delay, and hurricane insurance.

2. DeFi Insurance Protocols

These protocols utilize decentralized finance to let users pool funds and provide insurance through smart contracts. Governance tokens allow community participation, staking, and earning yields, ensuring a transparent, user-owned, and participant-focused system.

Example: Nexus Mutual is a member-owned DeFi insurance platform offering smart contract cover, custody cover, and yield protection.

3. On-Chain Insurance Platforms

Every step, from issuing a policy to settling a claim, occurs on the blockchain, providing transparency, preventing fraud, and enabling automation. On-chain insurance suits Web3 and digital assets.

Example: InsurAce is a multi-chain DeFi insurance protocol offering on-chain risk management and capital-efficient coverage.

4. Hybrid Insurance Platforms

These platforms combine on-chain automation with off-chain data validation. Smart contracts handle payouts and record-keeping, while traditional systems manage user verification and compliance. This balances new tech with real-world needs.

Example: B3i (Blockchain Insurance Industry Initiative), formed by global insurers like Allianz and Swiss Re, using blockchain to streamline reinsurance contracts.

5. Peer-to-Peer (P2P) Insurance Platforms

P2P models enable individuals to pool resources and insure each other, removing intermediaries and reducing administrative costs. Blockchain ensures trust and transparency among participants by maintaining a verifiable record of every contribution and claim.

Example: Teambrella is a P2P insurance model where members form teams, vote on claims, and share financial responsibility transparently.

Why is the On-Chain Insurance Platform Growing Now?

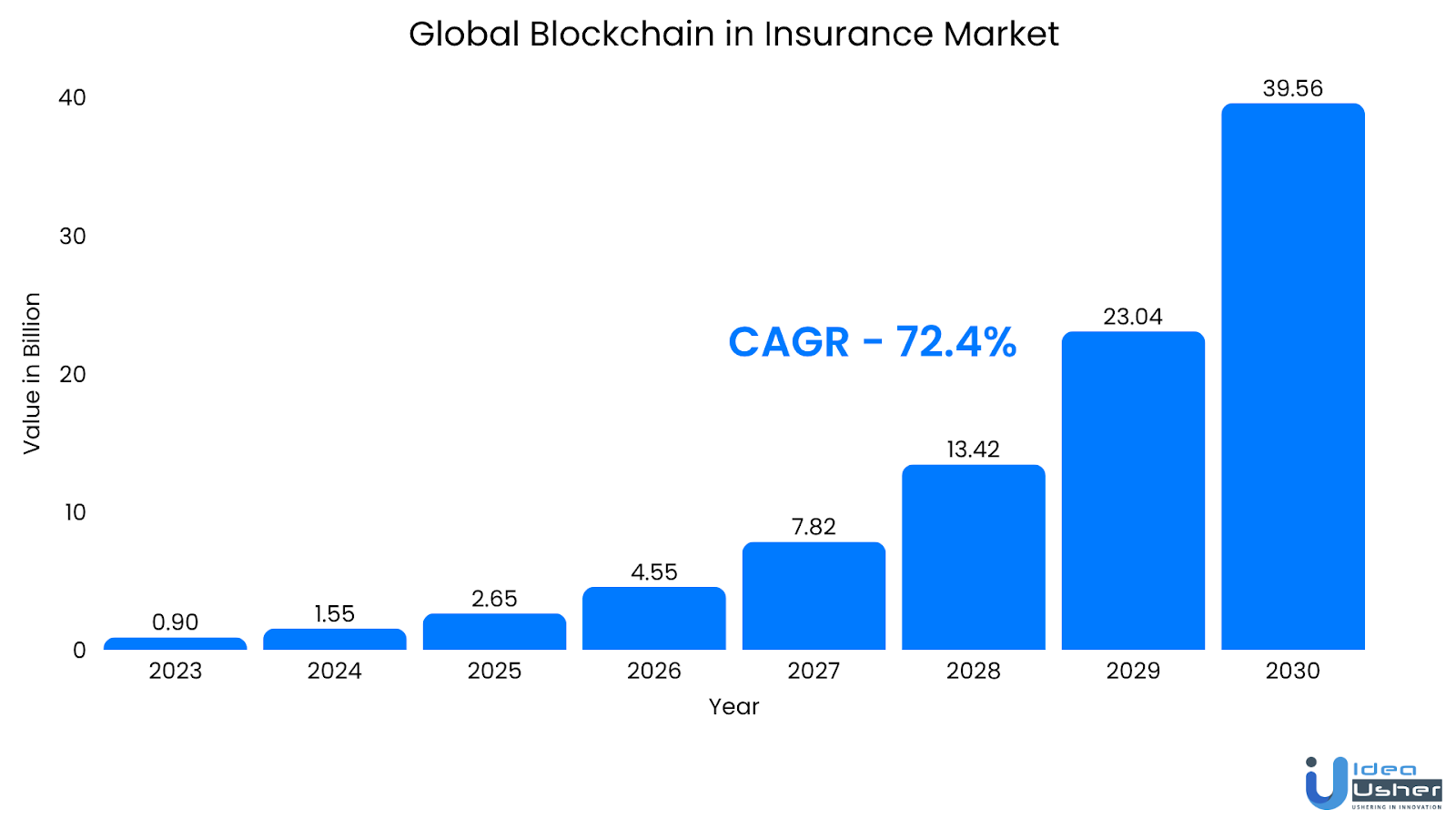

The Blockchain in Insurance Market was valued at $177.85 million in 2020 and is expected to reach $39.56 billion by 2030, growing at 72.4% CAGR. On-chain insurance platforms are emerging, using distributed ledger tech, smart contracts, tokenised risk pools, and real-time data to revolutionize insurance underwriting, distribution, and servicing.

Nayms is a regulated on-chain insurance marketplace for risk placement, capital raises, and tokenized risk pools and completed a private token sale in April at an $80 million valuation, with total funding of about $12 million.

Falcon Finance, a DeFi protocol, launched an on-chain insurance fund with an initial contribution of US$10 million (in stablecoin USD1) in August 2025, aimed at providing institutional-style protection for its ecosystem.

Why Businesses Are Investing in these Platforms?

Businesses are increasingly investing in on-chain insurance platforms because these systems deliver real, measurable benefits in efficiency, fraud reduction, customer experience, and access to new products.

- Significant cost-savings potential: According to PwC, the reinsurance sector alone could save US$5-10 billion via blockchain adoption, by reducing 15-20 % of expenses from duplication and manual reconciliation.

- Faster claims processing & automation: Market data suggests blockchain and smart contract automation can reduce claim processing time by ~41%. Another report says claims settlement time can drop from “weeks to days” or by ~40-50 % in some cases.

- Fraud reduction: One source notes that blockchain-based systems reduce fraudulent claims by ~25-30%, or reduce fraud application risk by up to ~65%.

- Reduced administration: Industry research shows potential operating cost reductions of 25-40% in policy administration and underwriting using smart contracts and ledger automation.

- Better transparency: Studies show that ~56% of insurers recognise blockchain’s importance, though ~57% still don’t know how to capitalise on it, indicating strong interest in business model change.

On-chain insurance is a rapidly growing market, projected to reach billions. Increased investment and incentives like cost savings, fraud prevention, and global capital access are fueling this growth. For insurers and businesses, adopting on-chain insurance means rethinking the value chain and gaining an edge through efficiency, innovation, and new risk models.

68% of DeFi Insurance Covers Smart Contract Risks

On-chain insurance is increasingly focused on smart-contract and protocol-failure coverage, which now accounts for over 68% of policies issued in 2025.

Most coverage in this area focuses on issues like code failures, exploits, or protocol bugs, rather than on traditional risks such as accidents or health problems.

Because of that focus, more than 65% of paid claims have been due to hacks and protocol exploits since 2020, underscoring how distinct this insurance niche is compared to legacy lines.

A. Capital Pools, Mutual Models & Scale

The peer-to-peer, capital-pool or mutual-model is central in on-chain insurance. For example, such mutual/pool-based models support over US$350 million in capital contributed by community policy-holders.

One leading platform, Nexus Mutual, by mid-2023, reported that its members had “sold more than US$4.3 billion in cover” and paid “over US$14 million in claims”.

These figures illustrate both the emerging scale of the model and the still relatively modest level of payouts relative to traditional insurance sectors.

B. Practical Platform Metrics & Underwriting Model

Diving into platform-specific metrics sheds light on operational realities:

- In Q2 2024, Nexus Mutual members purchased about US$167.9 million in coverage (≈ 223% quarter-over-quarter growth).

- In the same period, its underwriting fee income (cover-fee revenue) exceeded US$1.2 million, up ~236% from Q1 2024.

- On the platform side, some pools remain small: e.g., another protocol had peak TVL of only US$32 million+ covering 25+ DeFi protocols.

Overall, these figures show the sector is still developing but quickly shifting toward specialized, data-driven risk protection. On-chain insurance is establishing itself separately from traditional coverage by focusing on technical risks like smart contract failures and protocol exploits. As capital increases, claims become more automated, and underwriting clearer, decentralized insurance is likely to evolve from an experiment to a vital part of the DeFi ecosystem.

Why Blockchain Is the Future of Insurance Operations?

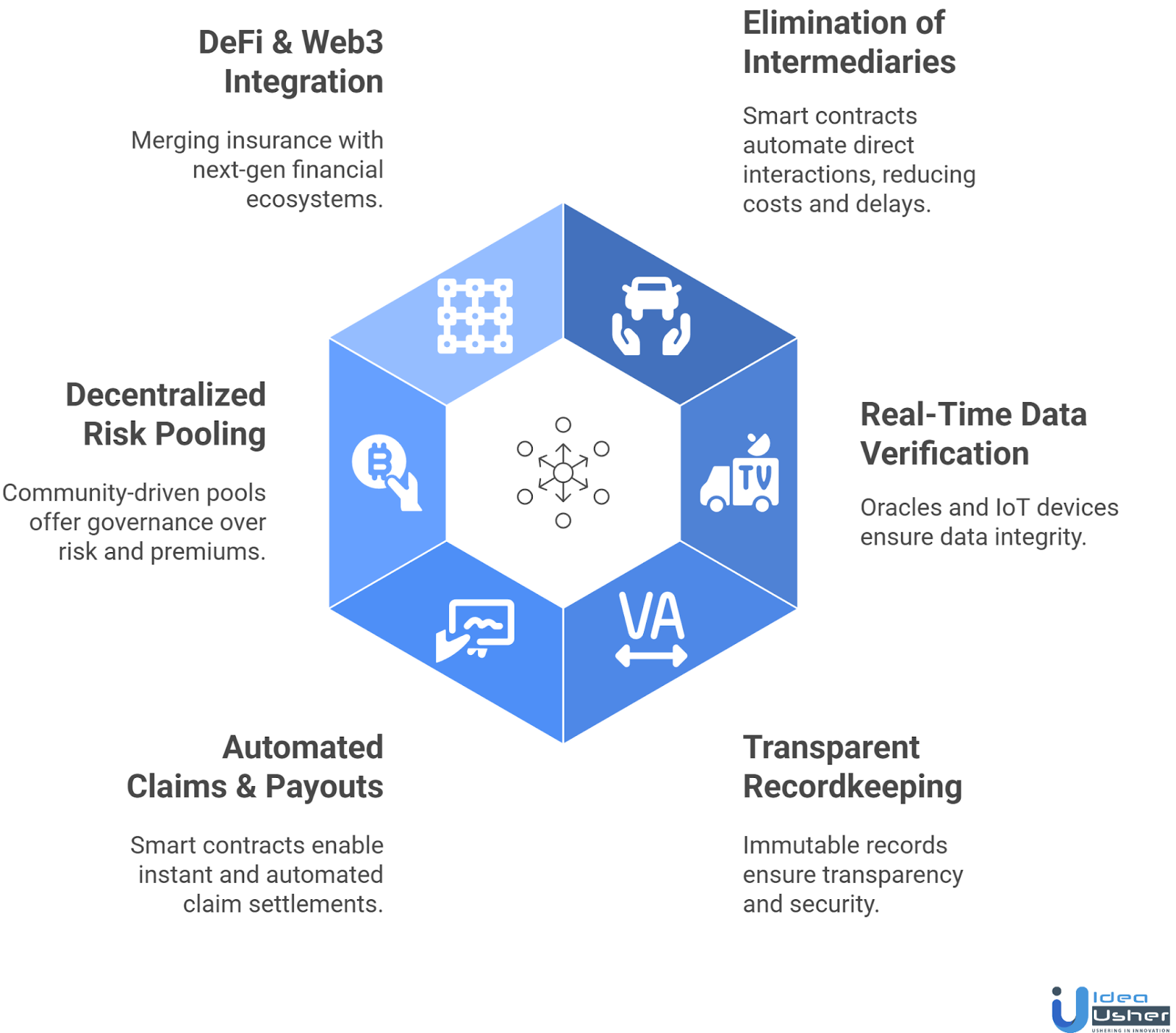

Blockchain is revolutionizing insurance by enhancing policy management, claims processing, and customer relations. Its decentralized and transparent system addresses fraud, inefficiency, trust, and speed, shaping the future of the industry.

1. Elimination of Intermediaries

Traditional insurance has many intermediaries, increasing costs and delays. Blockchain employs smart contracts to automate and connect insurers directly with policyholders, reducing costs, speeding transactions, and enhancing accuracy.

2. Real-Time Data Verification

Blockchain links with data oracles, IoT devices, and APIs, enabling insurers to verify claim-triggering events (like weather, flight delays, sensor data) in real time. This ensures data integrity, transparency, and trust, reducing fraud and disputes.

3. Transparent & Immutable Recordkeeping

Every transaction, from policy issuance to claim settlement, is permanently recorded on the blockchain. This creates an immutable audit trail that enables instant record verification, enhances transparency, and helps prevent data tampering.

4. Automated Claims & Payouts

With smart contracts, claim settlements are instant and automated. When a verified event occurs, the blockchain executes the payout without manual checks. This cuts processing times from days to minutes, improving user satisfaction and efficiency.

5. Decentralized Risk Pooling

Blockchain enables community-driven risk pools, allowing capital providers to stake funds to underwrite policies. This removes traditional intermediaries and gives users more governance over risk, premiums, and reinsurance, creating a more democratic and liquid insurance ecosystem.

6. Integration with DeFi & Web3 Ecosystems

DeFi insurance protocols and on-chain governance are merging insurance with next-gen financial ecosystems. With staking-based risk models and tokenized policy ownership, blockchain empowers insurers to create new products while maintaining security and decentralization.

On-Chain Insurance Platform Features & Estimated Cost

An on-chain insurance platform uses blockchain to automate and secure the insurance process, from policy issuance to claims. The table below shows key features, on-chain insurance costs, and how each helps build a transparent, decentralized ecosystem.

| Key Feature | Description | Estimated Cost |

| Smart Contract Policy Engine | Automates policy creation, validation, and claim execution through self-executing smart contracts, ensuring transparency and trustless operations. | $15,000 – $25,000 |

| Generic Insurance Framework (GIF) | A modular framework like Etherisc’s supports various insurance products (crop, flight delay, or property insurance) with shared smart contract logic. | $20,000 – $35,000 |

| Blockchain Oracle Integration | Connects the platform to real-world data sources like weather APIs or market feeds to trigger parametric events and payout conditions. | $10,000 – $20,000 |

| Payout & Trigger Engine | Automates event-based payouts using parametric triggers and predefined logic within smart contracts. | $8,000 – $14,000 |

| Decentralized Claims Management | Enables automated, on-chain claim assessment and settlement without intermediaries, reducing delays and fraud. | $18,000 – $30,000 |

| Risk Pooling & Liquidity Module | Enables decentralized capital pooling, fund allocation, and reinsurance across smart contracts. | $12,000 – $20,000 |

| Tokenization & Payment Layer | Facilitates premium payments, payouts, and staking in cryptocurrencies or stablecoins via on-chain wallets. | $12,000 – $22,000 |

| DAO Governance Module | Allows community-driven decision-making for premium rates, claim approvals, and protocol upgrades. | $15,000 – $28,000 |

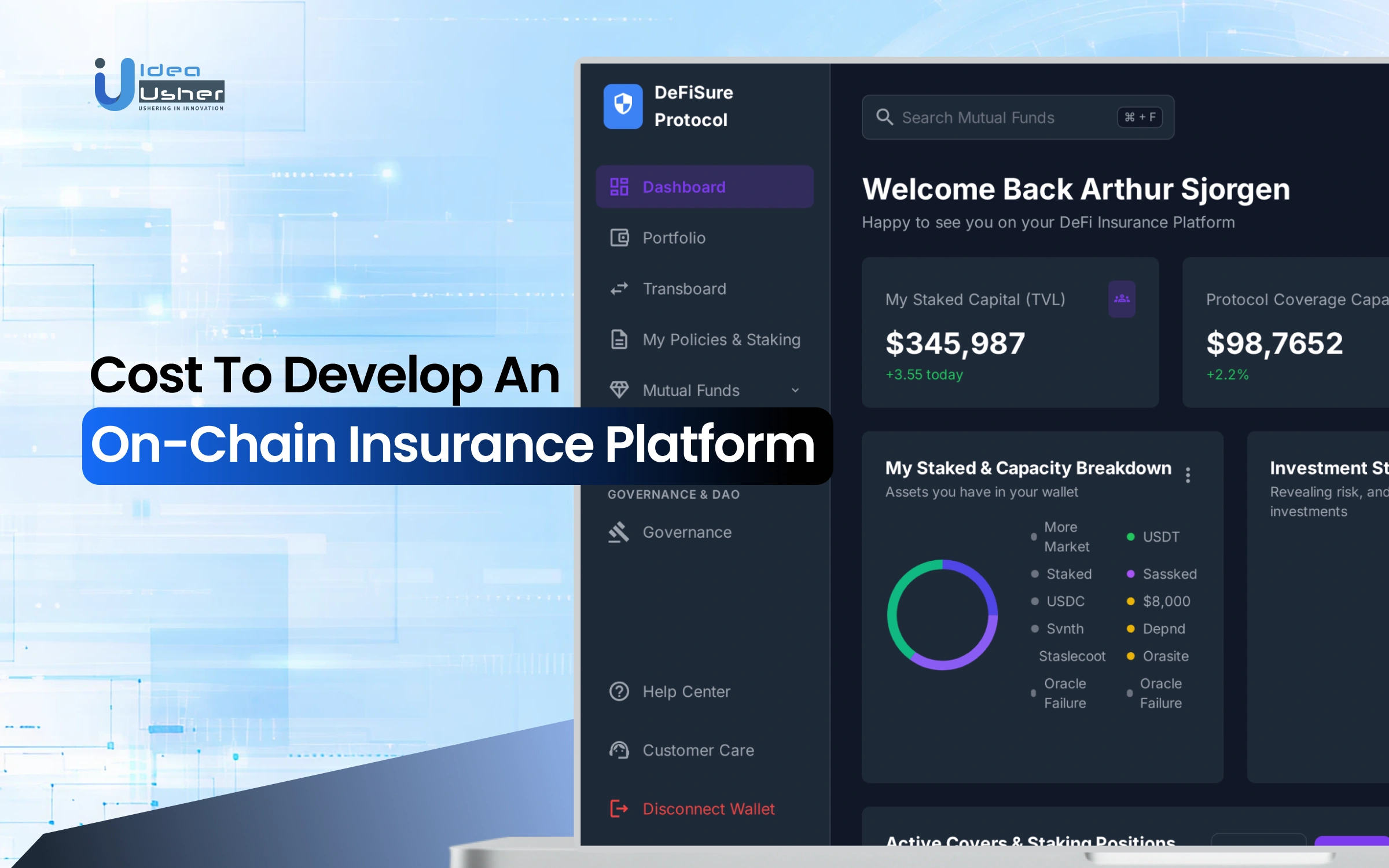

| User Dashboard (Web3 UI) | Gives users real-time policy tracking and claim updates through a blockchain interface. | $10,000 – $18,000 |

| Analytics & Reporting Module | Offers real-time analytics on policy sales, claims, and fund utilization using on-chain data visualization tools. | $7,000 – $12,000 |

Note: The actual on-chain insurance cost may vary based on project complexity, blockchain selection, smart contract sophistication, UI/UX design requirements, and integration with third-party APIs or oracle networks.

Consult IdeaUsher’s blockchain experts for a tailored cost estimate and guidance from conceptualization to deployment of your on-chain insurance platform.

Cost-Affecting Factors to Consider

Building an on-chain insurance platform involves several technical and operational variables that directly impact the total on-chain insurance cost. These factors determine the scalability, performance, and long-term sustainability of the platform.

1. Choice of Blockchain Network

The on-chain insurance cost varies based on whether you deploy on Ethereum, Polygon, BNB Chain, or a custom Layer 2 solution. While Ethereum offers higher security and developer support, Layer 2 and sidechains significantly reduce gas fees and transaction costs.

2. Complexity of Smart Contracts

Sophisticated policy logic like multi-trigger conditions, basis risk adjustments, or reinsurance pooling increases development and audit costs. Simple, single-event triggers are cheaper, but multi-layered contracts need expert Solidity development and testing.

3. Oracle & Data Integration Requirements

Integrating multiple oracles (for weather, IoT, or market feeds) increases cost but enhances data reliability and payout accuracy. Multi-source validation systems like Chainlink or DIA ensure trustworthy triggers but require additional configuration and API costs.

4. Governance & Compliance Modules

Adding DAO governance, KYC/AML checks, and smart compliance tools increases on-chain insurance costs, but these steps are crucial for meeting regulations and building trust, particularly when dealing with cross-border insurance.

5. Security Audits & Testing

End-to-end audits by reputed third-party firms (like CertiK or Quantstamp) are non-negotiable for production-grade protocols. Audit depth, manual code reviews, and continuous monitoring tools can account for 10–15% of the total budget.

6. Scalability & Infrastructure Setup

Deploying nodes, setting up cloud infrastructure, and enabling auto-scaling environments affect hosting and maintenance costs. Choosing decentralized hosting (like IPFS or Arweave) vs. hybrid models changes both operational efficiency and expenses.

7. Maintenance & Post-Launch Support

Ongoing smart contract upgrades, oracle maintenance, and user support ensure long-term stability. Post-launch improvements typically cost 15–20% annually of the initial development investment.

Estimated Cost for On-Chain Insurance Platform Development

The total on-chain insurance cost of building the platform depends on factors like project scope, required integrations, and the complexity of the blockchain. Here is a breakdown of costs for three different development levels, ranging from MVPs to enterprise solutions.

1. MVP / Small-Scale Platform

A Minimum Viable Product (MVP) is ideal for startups or small insurers testing decentralized insurance concepts. It focuses on automation, transparency, and basic oracle-driven claim triggers.

Estimated Cost: $60,000 – $85,000

Key Features:

- Smart Contract-Based Policy Execution: Automates policy creation, validation, and payouts, ensuring transparency and minimizing administrative tasks.

- Oracle Data Integration: Connects to external APIs (like weather or market data) for real-time event monitoring and trigger validation.

- Basic Web3 Dashboard: Allows users to view their policies, claim status, and transaction logs in a simple, wallet-connected interface.

- DAO Governance Lite: Enables basic voting on policy parameters or community decisions to maintain decentralized control.

- Basic Analytics Dashboard: Provides summary-level insights into active policies, claims processed, and pool utilization.

2. Mid-Scale Platform

A mid-scale platform is suited for growing organizations or consortiums launching a full-featured decentralized insurance ecosystem. It offers multi-product support, risk pooling, and advanced compliance modules.

Estimated Cost: $100,000 – $135,000

Key Features:

- Multi-Product Management: Supports different types of coverage, like crop, flight delay, or property insurance, all within a single framework.

- Advanced DAO Governance: Introduces weighted voting, multi-sig approvals, and dispute resolution for decentralized protocol upgrades.

- Enhanced Oracle Network Integration: Uses multiple oracle services (like Chainlink, API3) for high data reliability and trigger accuracy.

- Dynamic Premiums & Payouts: Adjusts premium rates and payout limits algorithmically based on risk levels and pool liquidity.

- Risk Pooling & Reinsurance Modules: Creates liquidity pools and reinsurance mechanisms to manage capital efficiently and scale coverage.

- Detailed Analytics & Audit Trail: Provides real-time visibility into claims, transactions, and pool health for stakeholders and auditors.

3. Enterprise-Grade Platform

This version is designed for large insurers, reinsurers, or institutional ecosystems aiming for scalability, interoperability, and global regulatory compliance.

Estimated Cost: $140,000 – $180,000+

Key Features:

- Modular Architecture (GIF Framework): Built on frameworks like Etherisc’s Generic Insurance Framework for modular and rapid insurance product deployment.

- Multi-Chain & Cross-Border Support: Enables policies and payouts across multiple blockchains, supporting international operations.

- Legacy System & API Integration: Connects with traditional insurance databases, CRMs, and regulatory systems for seamless transition.

- AI-Powered Risk Modeling: Utilizes predictive analytics and actuarial models to forecast risk exposure and optimize premium pricing.

- Institutional-Grade Security & Audits: Includes code audits, penetration testing, and SLA-backed infrastructure for compliance and trust.

- Real-Time Analytics & Liquidity Optimization: Provides deep data insights, performance tracking, and automated liquidity balancing for sustainable operations.

Revenue Models of an On-Chain Insurance Platform

An on-chain insurance platform can adopt various business and revenue models depending on its scale, target market, and operational design. Below are the most effective models used by modern decentralized insurance ecosystems.

1. Commission-Based Model

The platform earns a percentage commission on every policy purchase, claim settlement, or transaction executed on-chain.

Example: For every insurance policy worth $1,000, the platform charges a 2 – 5% commission.

Why It Works: Provides a steady revenue stream as transaction volume grows, making it ideal for startups or aggregators.

2. Subscription-Based Model

Users or institutions pay recurring fees (monthly or annually) for premium access, enhanced features, or governance participation.

Example: $20/month for extended coverage, faster claim validation, or access to staking pools.

Why It Works: Generates predictable income and encourages long-term customer retention.

3. Liquidity Pool / Staking Rewards

Participants can stake tokens into a liquidity pool that funds claims. In return, they earn a portion of premiums or interest from unused funds.

Example: Users stake native tokens (e.g., INSURE or DAI) and receive APY returns based on platform performance.

Why It Works: Incentivizes community participation while maintaining decentralized liquidity reserves.

4. DAO Governance & Tokenomics

A native token governs the platform’s decision-making, premium pricing, and claim approvals. Revenue is generated from token appreciation, trading fees, and DAO treasury growth.

Example: Token holders vote on new insurance products and earn a share of profits via staking or governance participation

Why It Works: Builds a transparent, community-driven business structure with scalable long-term value.

Why Choose IdeaUsher for On-Chain Insurance Platform Development?

At IdeaUsher, we combine blockchain expertise, insurance domain knowledge, and user-centric design to build scalable, compliant, and future-ready on-chain insurance platforms.

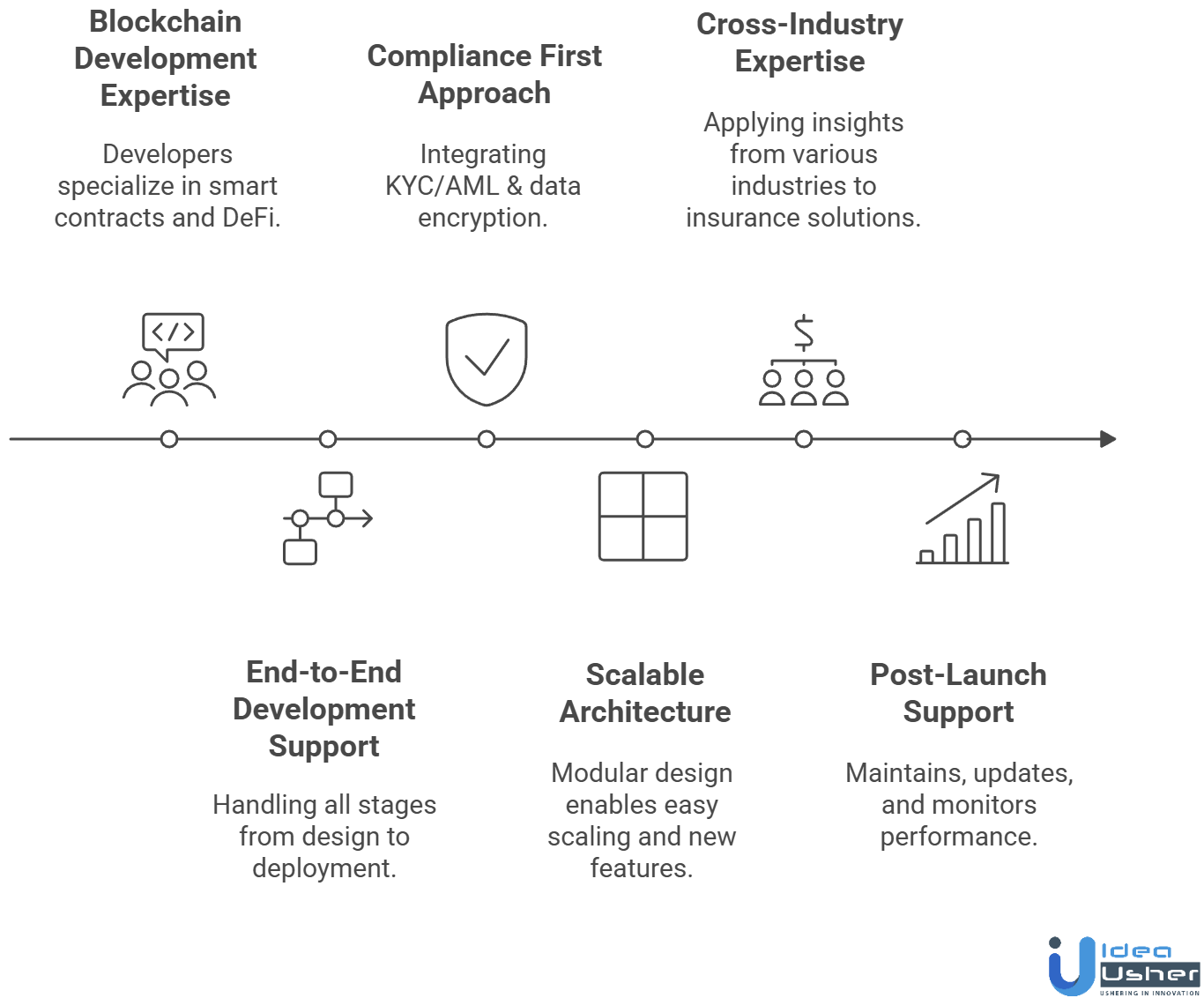

1. Proven Blockchain Development Expertise

Our developers specialize in smart contract creation, DeFi integrations, and decentralized architecture, ensuring your platform runs securely and autonomously with minimal manual intervention.

2. End-to-End Development Support

We handle every stage, from brainstorming and UI/UX design to deployment and ongoing improvements. At each step, we focus on smooth performance and meeting all requirements.

3. Compliance & Security First Approach

We integrate KYC/AML compliance, data encryption, and audited smart contracts, helping you build user trust while staying aligned with global insurance regulations.

4. Scalable & Customizable Architecture

Our modular development approach allows the platform to scale easily and integrate new features like AI risk assessment, oracle data feeds, or DAO governance as your business grows.

5. Cross-Industry Expertise

With successful blockchain projects across finance, healthcare, real estate, and supply chain, we bring multi-domain insights to design versatile, high-performance insurance solutions.

6. Post-Launch Support

Our partnership goes beyond deployment. We provide ongoing maintenance, regular feature updates, and performance monitoring to help your platform remain competitive and ready for the future.

Conclusion

Building an On-Chain Insurance Platform requires the right mix of blockchain infrastructure, smart contracts, real time data integration, and strong security practices. The on-chain insurance cost will vary based on features, automation level, and compliance requirements. However, the investment pays off with improved transparency, faster claims processing, and higher user trust. As more industries adopt decentralized solutions, on chain insurance continues to show strong market potential. If you are planning to innovate in the insurance sector, this model offers a scalable path toward efficiency and long term value.

FAQs

Costs depend on platform complexity, blockchain selection, smart contract development, security integrations, and regulatory compliance. The total investment increases as features like automation, oracle data, and advanced dashboards are added.

An MVP usually focuses on essential features such as policy creation, premium payments, and claims automation. Development prices typically fall in $60,000 – $135,000 range of the total estimate because only core modules and basic UI are included.

Insurance involves sensitive financial data, so additional audits, encryption layers, and fraud prevention tools are required. These security measures help ensure trust and reduce vulnerabilities within the decentralized ecosystem.

Yes. Ongoing upgrades, server operations, smart contract monitoring, and customer support contribute to yearly costs. These updates help enhance platform performance and keep it aligned with compliance and evolving user needs.