Credit unions in Canada are an essential pillar in the country’s financial system, but they faced limitations earlier, like the inability to extend credit facilities to non-members, etc. However, the recent passage of Ontario’s Credit Unions and Caisses Populaires Act, 2020 (CUCPA 2020) created a dynamic and evolving operating environment full of opportunities and challenges.

But what should we know about CUCPA 2020? How does it affect credit unions, and how can they grow after this legislation? Let’s discuss this in this blog article.

What are credit unions in Canada?

A credit union is a financial cooperative that offers standard banking services. Major firms, organizations, and other entities can form credit unions for their employees and members. These credit unions can range from small, volunteer-only operations to large enterprises with thousands of participants across the country.

Its members create, own, and operate the credit union. As such, they are non-profit organizations with tax-exempt status.

While Canada’s big banks remain dominant, credit unions, Caisse Populaires, and online banks provide regular bank clients with a realistic alternative to meet their banking needs while keeping more money in their pockets.

In 2018, credit unions contributed over $6.5 billion directly and indirectly to Canada’s GDP.

Canadian Credit Union Association

Besides providing financial services, credit unions also focus on community building and development. They have a long history of giving back to their members and supporting the communities where they live and work.

Every credit union has a spirit and a determination to improve financial wellness for the communities they serve by providing professional guidance, world-class investment products, savings options for all income levels, and simply keeping money in their members’ pockets.

A brief overview of CUCPA 2020

The Credit Unions and Caisses Populaires Act, 2020 (CUCPA 2020) came into force on March 1, 2020, replacing the Credit Unions and Caisses Populaires Act, 1994 (CUCPA 1994). This reform was a welcome change for the industry, which includes 62 credit unions and over 1.7 million members in Ontario.

The Ontario government initiated public consultations on CUCPA 1994 in 2019 to modernize the framework, identify efficiencies, and reduce red tape so that credit unions may compete, grow, and better fulfill the needs of their members. CUCPA 2020 is the outcome of these public consultations and a subsequent legislative review that finished in 2020.

Ontario’s Financial Services Regulatory Authority’s (FSRA) three rules came into effect with CUCPA 2020:

| Sound Business and Financial Practices Rule | The Sound Business and Financial Practices Rule establishes outcomes to provide a principles-based approach to business and financial practices. |

| Capital Adequacy Requirements Rule | The Capital Adequacy Requirements for Credit Unions and Caisses Populaires Rule fosters a more robust credit union sector by assessing and maintaining adequate and acceptable internal capital types and improving alignment with international norms. |

| Liquidity Adequacy Requirements Rule | The Liquidity Adequacy Requirements for Credit Unions and Caisses Populaires Rule encourages a more vital credit union sector by assessing and maintaining adequate and acceptable sources of liquidity and improved compatibility with international standards. |

Key benefits CUCPA 2020 provides to credit unions in Canada

1. Reduced red tape

One of the public consultations’ pillars was to lessen the regulatory burden on credit unions. Many prescriptive provisions in CUCPA 1994 will be subject to or set out in rules adopted by Ontario’s Financial Services Regulatory Authority (FSRA) in CUCPA 2020. Although FSRA oversight may be essentially similar to the CUCPA 1994 regime, the change presents an opportunity to examine and simplify these regulations, which, given FSRA’s reputation as a principles-based regulator, may result in greater flexibility.

2. Increased competitiveness

CUCPA 2020 also increases business and capital-raising opportunities for the credit union sector.

- Increased business scope: The law no longer compels credit unions to operate in enterprises that are “reasonably ancillary” to providing financial services.

- Commodity transactions: Credit unions may transact in commodities or do business with the written approval of the Chief Executive Officer.

- Customer expansion: They can now lend money to non-members, which was previously disallowed.

- More capital raising options: Ontario credit unions will have greater access to financing since they can now offer securities without filing a prospectus under National Instrument 45-106 Prospectus Exemptions and National Instrument 45-108 Crowdfunding.

- Insurance sales: Credit unions will also be able to collaborate with certified insurance agents, brokers, and firms to offer more forms of insurance in their branches and online.

- Greater administrative flexibility: Meeting rules now have more technology-neutral language to provide alternatives to in-person meetings and voting, while the law liberalizes the record-keeping requirements to allow for storage outside Ontario.

Collectively, these reforms dramatically broaden the business prospects for credit unions and equip credit unions to be more competitive in the financial services sector.

3. Improved consumer experience

The last pillar of public consultations was to improve the consumer experience. As stated earlier, credit union services are more widely available since the implementation of CUCPA 2020, and non-member consumers can also obtain loans from credit unions.

Consumers now have access to more services, as credit unions can provide property and casualty insurance. As previously noted, consumers will profit from the availability of documents in electronic form.

However, the most significant change in terms of consumer protection is the new requirement for credit unions to develop and implement a market code of conduct, which is subject to FSRA inspection.

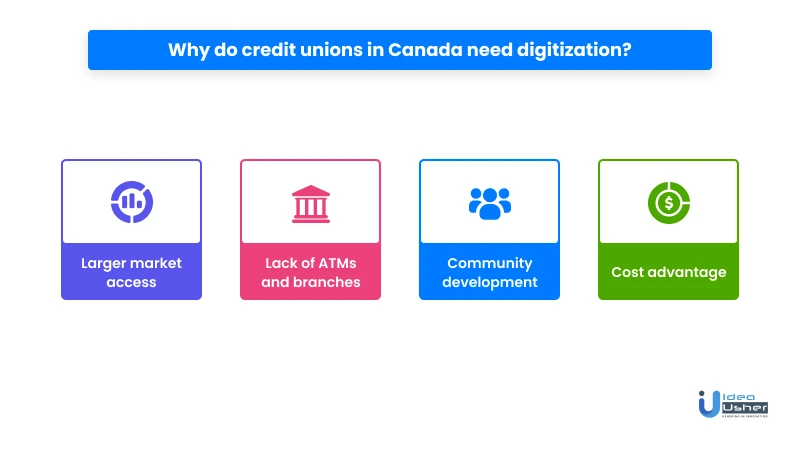

Why do credit unions in Canada need digitization?

The CUCPA 2020 has opened new opportunities for credit unions in Canada. Credit unions can cash in on these opportunities and switch to the digital mode of functioning to overcome their limitations. But why do credit unions need digitization? What are the pain points that digitization can help solve? How will digital solutions help credit unions? Let’s find out.

1. Access to a larger market

Previously, credit unions were limited to making transactions such as loan disbursement or investments with the members only. However, with the CUCPA 2020 in effect, credit unions can access a larger market, allowing them to deal with non-members and members.

Expanded market reach necessitates the integration of digital solutions into the functioning of credit unions, as the traditional modes of functioning would lead to delayed processes and inefficiency. The world is switching to online business methods, and with an online presence, credit unions can spread their word and provide customers with faster and better financial services.

2. Lack of ATMs and branches in multiple locations

Credit unions are smaller institutions than commercial banks and have vast differences from the banks. While banks have widespread branches and ATM networks spread across the country, credit unions lack geographical expansion. With a limited number of branches and ATMs, credit unions can operate within restricted limits only.

However, they can consider the geographical factor with digitization. Credit unions can provide their customers with online services right at their fingertips. Online banking facilities can streamline transactions and help reach remote locations where credit unions lack ATM or branch access. Thus, by focusing on digital expansion, the need for physical expansion can be controlled, if not eliminated.

3. Community development

As stated earlier, credit unions are community-driven and emphasize community building and development. They focus on giving back to the community through sponsorships, donations, grants, etc. According to Sunshine Coast Credit Union, every year, credit unions contribute an average of 5.4% of their pre-tax revenues to local community organizations. Moreover, in 2017, credit union staff volunteered 302,035 hours in their communities.

With a digital presence, credit unions can create a forum or a community platform for effective and efficient community building. The platform can help the credit unions channel efforts towards more community-driven projects and activities to foster a sense of trust and belongingness.

4. Cost advantage

Credit unions can get another advantage by digitizing their functions: reduced cost of operations. By switching to the digital mode, credit unions can take advantage of automation, cloud computing, and big data analytics, which can help lower the operational costs for the credit union.

Further, online services will help credit unions eliminate fixed costs related to property or machinery. It, in turn, helps to increase the return on investment.

What digital solutions do credit unions need?

We have understood why credit unions need to digitize and the benefits they’ll get by switching to the online mode of functioning. But which digital solutions do they need to reap those benefits? Let’s discuss this.

1. App/ website development

The primary digital solution that credit unions require is a robust and scalable mobile app for their business. A mobile app will provide an all-in-one solution to credit unions and their customers. The credit union can develop an app and upload it to the Google Play Store or the Apple App Store to reach a wider audience, specifically those who already rely on the online financial services of banks.

Further, credit unions need to include functionalities like loan disbursement, investment tracking, interest calculation, insurance disbursement, etc., in the mobile app. With the CUCPA 2020 in force, credit unions can capitalize on the revenue-generating opportunities using apps.

Additionally, the app can include portals and tabs for community engagement and interaction. Credit unions focus a lot on community development, so the community portal functionality cannot be ruled out. The credit union and the members can use the app to organize community events, hold discussions, and get updates about the community activities that the credit unions undertake.

Push notifications from the app can help users get timely updates about their financial activities. It will also help the credit union promote social activities and other initiatives.

In addition to mobile application development, the credit union can create a website (if not already created) or optimize the website (if already created). Website creation or optimization will ensure that the services also reach people without smartphones.

2. Digital marketing

In addition to app development, credit unions can employ digital marketing strategies to promote and spread the word about their services and activities. According to Smarter Loans research, social media largely impacts Canadians’ buying habits for Fintech products, with Facebook and YouTube standing out as the most popular platforms across all age groups and Instagram and TikTok emerging as significant sources of information for younger customers.

Credit unions can take advantage of various digital marketing strategies and channels to create awareness about their services:

- Content marketing

- Search Engine Optimization (SEO)

- Social Media Marketing

- Pay Per Click (PPC)

- E-mail Marketing

In 2021, 69% of marketers invested in SEO.

HubSpot

Wrapping up

The CUCPA 2020 is landmark legislation for the Fintech sector in Canada, specifically for credit unions. Fintech apps have been growing tremendously worldwide; however, Canadian credit unions have a comparatively lesser technological footprint. With the CUCPA 2020 in effect, credit unions have a greater chance of earning higher profits by expanding their reach and digitizing their services.

As already noted, credit unions can leverage app development, website development, and digital marketing to boost their business and reach new customers. These digital solutions are instrumental as they will help credit unions access a larger market, overcome the problem of lesser branches and ATMs, foster community engagement, and reduce costs.

However, integrating digital solutions into the existing business model is complicated, and it is better to consult experts for seamless digital integration.

Idea Usher is a leading technology company with years of experience in app development, web development, web 3.0 services, and digital marketing. Our ever-growing team is skilled in providing the best digital solutions for the growth and development of our client’s businesses.

Contact us to get digital solutions for your credit union to make the most of CUCPA 2020.

E-mail: [email protected]

Phone Numbers : (+91) 946 340 7140, (+91) 859 140 7140 and (+1) 732 962 4560

Frequently asked questions

Here are some exciting FAQs about Canadian credit unions.

1. How do credit unions work in Canada?

Credit unions commit to their members’ financial well-being and thus return profits to members via profit sharing, low/no fees, community investments, and a national network of surcharge-free ATMs. However, after the CUCPA 2020 came into effect, the credit unions could deal with non-members too.

2. Can credit unions sell insurance in Canada?

Yes, the CUCPA 2020 allows credit unions to partner with authorized insurance agents, brokers, and corporations to expand their insurance offerings in their branches and online.

3. Who regulates the credit unions in Ontario?

The Financial Services Regulatory Authority (FSRA) regulates credit unions in Ontario.