(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Fintech companies manage sensitive financial data every day, and even small monitoring gaps can create serious risks. With identity fraud, money laundering attempts, and shifting regulations, teams often struggle to stay compliant while maintaining a smooth user experience. These challenges make it crucial to adopt a reliable fintech compliance tool that automates checks, flags suspicious activity, and keeps operations aligned with global standards.

Modern compliance and AML systems bring structure and speed to processes that were once manual and error-prone. With real-time monitoring, AI-driven risk scoring, automated KYC and AML workflows, and secure data integrations, fintech apps can detect threats earlier and lower compliance workloads. This not only strengthens trust and security but also allows businesses to scale without being slowed by regulatory complexity.

In this guide, we’ll explain how to build effective compliance and AML systems for fintech applications, the core features they require, and the technology that powers them. This blog will give you a clear understanding of the tools, architecture, and strategy needed to create a secure and regulation-ready fintech solution.

What is a Compliance & AML Platform?

A Compliance & AML Platform is a specialized system designed to help fintech companies detect, prevent, and manage financial crimes while meeting regulatory requirements. It centralizes identity verification, transaction monitoring, sanctions screening, and risk assessment to ensure users, transactions, and business activities remain compliant and fraud-free.

By combining automated checks, real-time analytics, and structured workflows, the platform enables organizations to identify suspicious behavior early, reduce compliance burdens, and maintain trust with regulators and customers.

- Identity verification (KYC) ensures users are legitimate through document checks, biometrics, and database validation, preventing fraudulent or high-risk individuals from entering the platform.

- Transaction monitoring analyzes user activity in real time to detect suspicious patterns, unusual behavior, or potential money-laundering attempts.

- Risk scoring evaluates customers and transactions using rules, historical data, and behavioral insights to assign dynamic risk levels for better decision-making.

- Reporting automates regulatory submissions, audit logs, and compliance documentation, reducing manual workload and ensuring transparency with authorities.

- Alerting notifies compliance teams immediately when high-risk events, anomalies, or threshold breaches occur, enabling faster investigation and response.

Importance of Compliance & AML in Fintech

Compliance and AML are vital for fintechs to operate safely, prevent crime, and uphold trust. They safeguard the platform, customers, and the financial system from fraud, sanctions breaches, and money laundering.

1. Protecting Customers and Preventing Fraud

Compliance and AML systems safeguard users from identity theft, account takeovers, and fraud by verifying identities, monitoring transactions, and blocking suspicious activity, ensuring a secure environment for digital financial services.

2. Meeting Regulatory Requirements & Avoiding Penalties

Fintech companies face strict regulations, and non-compliance risks fines, license suspension, or shutdowns. Strong AML practices help platforms meet legal rules, ensuring smooth operations and regulatory trust.

3. Platform Security and Risk Management

Robust AML controls lower risks of money laundering, terrorism, and illicit activities. They improve the platform’s risk management, helping fintech firms detect threats early, maintain system integrity, and safeguard financial data.

4. Building Customer Trust & Brand Credibility

Users trust fintech apps with strong compliance and transparent security. Effective AML processes boost credibility, attract quality customers, and reinforce the brand as a safe, reliable financial partner.

5. Enabling Scalable & Sustainable Growth

As fintech firms expand into new markets and customer segments, compliance is crucial for sustainable growth. A strong AML foundation enables smooth cross-border operations, onboarding, and new product launches without regulatory problems.

How Compliance & AML Platforms Work in Fintech Apps?

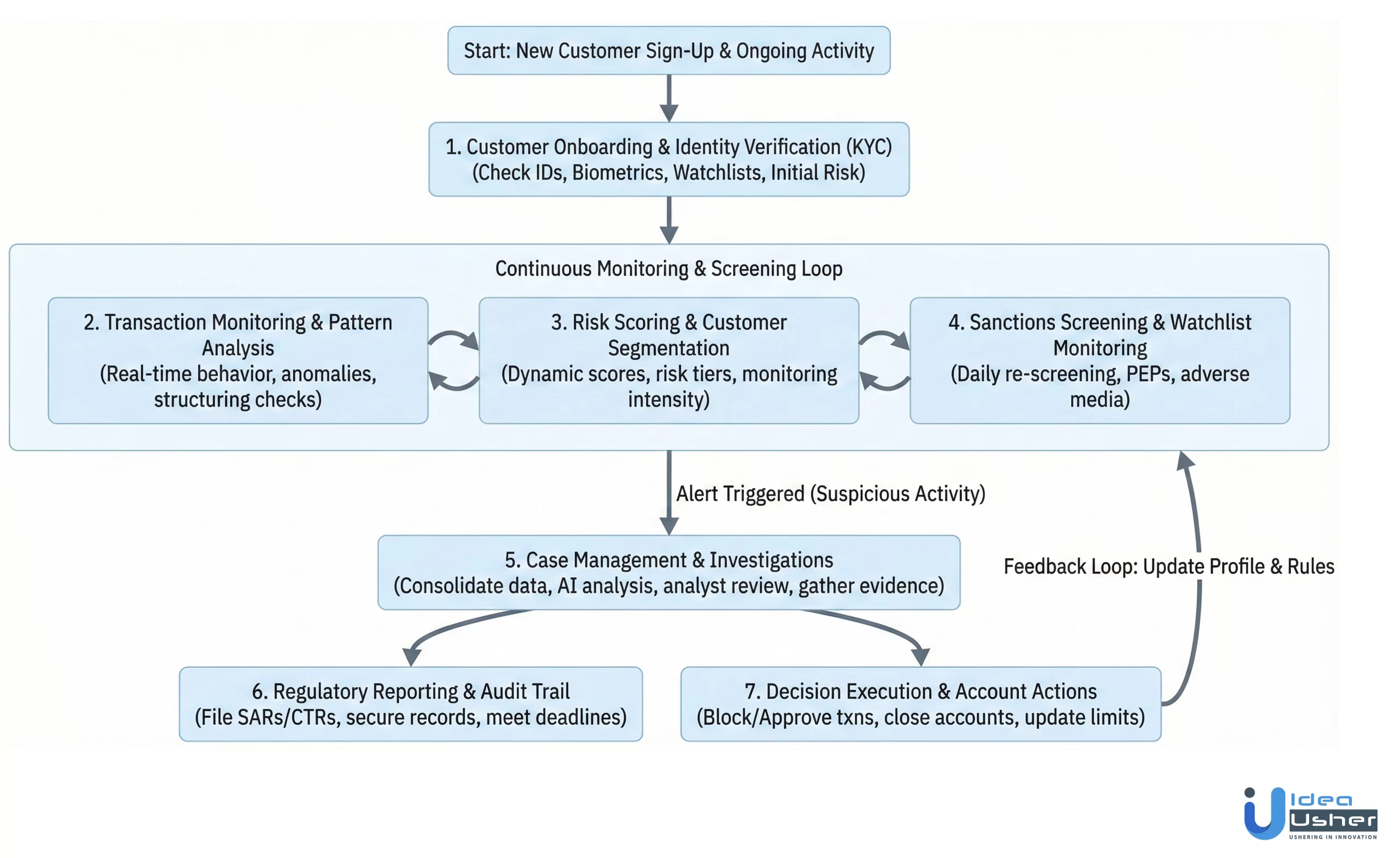

Compliance and Anti-Money Laundering (AML) platforms are critical systems that help fintech companies detect financial crimes, meet regulatory requirements, and protect their business from illicit activities. Here’s the complete working process:

1. Customer Onboarding & Identity Verification (KYC)

When a new fintech customer signs up, the compliance platform runs KYC checks, collecting personal and biometric data, verifying it against databases, and using AI to detect fake IDs or deepfake documents.

Example:

When Sarah uploads her driver’s license to FinSecure Compliance, the system verifies it in 8 seconds, checking authenticity, matching her selfie, and cross-referencing 200+ global sanction and PEP (Politically Exposed Persons) lists. She receives a risk rating of 12 (Low Risk) and is approved instantly.

However, when John applies, the platform flags that his ID photo looks digitally altered, the shadows don’t match and the document number format is incorrect. His application is automatically queued for manual review before approval, preventing potential identity fraud from entering the system.

2. Transaction Monitoring & Pattern Analysis

After onboarding, the platform monitors all transactions in real-time, analyzing amounts, frequency, counterparties, locations, and timing. Machine learning detects deviations, unusual transfers, structuring, rapid fund movements, and inconsistent behavior.

Example:

FinSecure monitors Sarah’s usual pattern: $3,200 bi-weekly salary, 15–20 retail purchases averaging $45, and $1,400 monthly rent. One Tuesday at 2:00 AM, she suddenly receives $9,500 from Romania and transfers $9,000 to recipients in Malaysia, Nigeria, and Ukraine within 18 minutes.

The platform assigns an anomaly score of 94/100, flags it as “Possible Money Mule Activity”, freezes outgoing transactions within 3 minutes, and routes the case to an AML analyst. It also notes her account was accessed from Nevada instead of her usual New York, adding another red flag to prevent cross-border money laundering.

3. Risk Scoring & Customer Segmentation

The platform continuously updates dynamic risk scores for each customer, segmenting them into Low, Medium, High, or Critical tiers. It considers hundreds of factors, including behavior, transactions, geography, occupation, and links to flagged entities.

Example:

FinSecure classifies 500,000 customers into four risk tiers. Sarah (risk score 12, Tier 1 – Low Risk, 78% of users) gets instant transfers up to $5,000 with monthly reviews. Marcus (risk score 58, Tier 2 – Medium Risk, 18% of users), a cash-heavy used car dealer, needs extra verification for transactions over $3,000 and weekly reviews (higher scrutiny due to statistical risk, not illegal activity).

Customers from FATF high-risk jurisdictions like Myanmar are automatically placed in “High Risk – Tier 3”, requiring enhanced due diligence, source of funds documentation, and daily monitoring. The “Critical Risk – Tier 4” segment gets real-time, transaction-by-transaction human review for direct watchlist matches or proven suspicious activity.

4. Sanctions Screening & Watchlist Monitoring

The platform continuously screens customers against global sanctions, law enforcement, adverse media, and PEP lists. Daily rescreening and real-time transaction checks, including intermediaries and indirect relationships, ensure ongoing compliance.

Example:

FinSecure runs automated screenings against 47 global watchlists every night at 2:00 AM. When the US Treasury adds “Viktor Kozlov” to the OFAC sanctions list, FinSecure’s next screening cycle flags customer “Victor Kozlov” as an 82% match probability and immediately freezes his account.

By 9:00 AM, a compliance analyst confirms Victor, a 23-year-old Boston college student, is a false positive and unfreezes the account within 2 hours. Meanwhile, Jennifer Wu receives $4,500 from Shanghai Import Export Ltd, 60% owned by a sanctioned entity. The platform blocks the transaction, files a SAR, and alerts the compliance team, demonstrating how relationship-based screening catches risks one-time checks would miss.

5. Case Management & Investigations

When suspicious activity is detected, the platform automatically creates cases, routes them by severity, and consolidates data, transactions, related entities, and AI summaries, enabling investigation, network visualization, fund flow analysis, and compliance tracking.

Example:

When analyst Michael opens Case #2847 (Sarah’s suspicious 2 AM transactions), he sees a full investigation package: a visual transaction timeline, a network graph linking her to 6 flagged accounts, device fingerprint changes, and an AI summary stating “High probability money mule – account likely compromised.”

The platform pulled IP logs, device info, and flagged her email password in a recent breach. Michael confirms suspicious activity, and FinSecure auto-generates a pre-filled SAR per FinCEN rules. The entire process from alert to filing takes 35 minutes versus 4 – 6 hours manually, while also notifying Sarah, forcing a password reset, and adding extra security measures.

6. Regulatory Reporting & Audit Trail

The platform automatically generates and files regulatory reports like SARs and CTRs, ensuring proper formatting and timely submission. It maintains encrypted audit trails of all actions and stores data for 5–7 years for compliance.

Example:

After Michael confirmed Case #2847, FinSecure had 30 days to file a SAR with FinCEN. The platform auto-formats it in BSA E-Filing, populates 42 fields, and submits it on day 12. It also automatically generates and files monthly CTRs for customers exceeding $10,000 in cumulative cash transactions.

For UK operations, FinSecure also generates SARs in UK format and submits them to the NCA. Annual audits access a complete audit trail showing who reviewed cases, data accessed, and exact timestamps, e.g., “Michael accessed Sarah’s transactions on March 15 at 10:47 AM for 8 minutes”, demonstrating full compliance.

7. Decision Execution & Account Actions

After investigations, the platform executes final actions like approving or rejecting transactions, closing high-risk accounts, adjusting limits, or clearing false positives. All decisions are logged and communicated, ensuring compliance and smooth service for legitimate customers.

Example:

After Michael’s investigation, FinSecure executes multiple actions: Sarah’s compromised account is permanently closed and she’s guided to open a new secure account; the 6 connected money mule accounts are automatically terminated within 2 hours; the $9,500 in suspicious funds is held and reported to law enforcement.

For false positive Victor Kozlov (the college student), the platform clears the alert, unfreezes his account, restores full functionality, and allowlists him. It also upgrades 3 medium-risk customers to low-risk after 6 months of clean activity, automatically upgrading them to low-risk tier with higher limits. Every decision is logged, communicated, and recorded in a full audit trail.

Why a Jump to 95% Detection Accuracy Signals a Major Opportunity for Modern Compliance & AML Platforms?

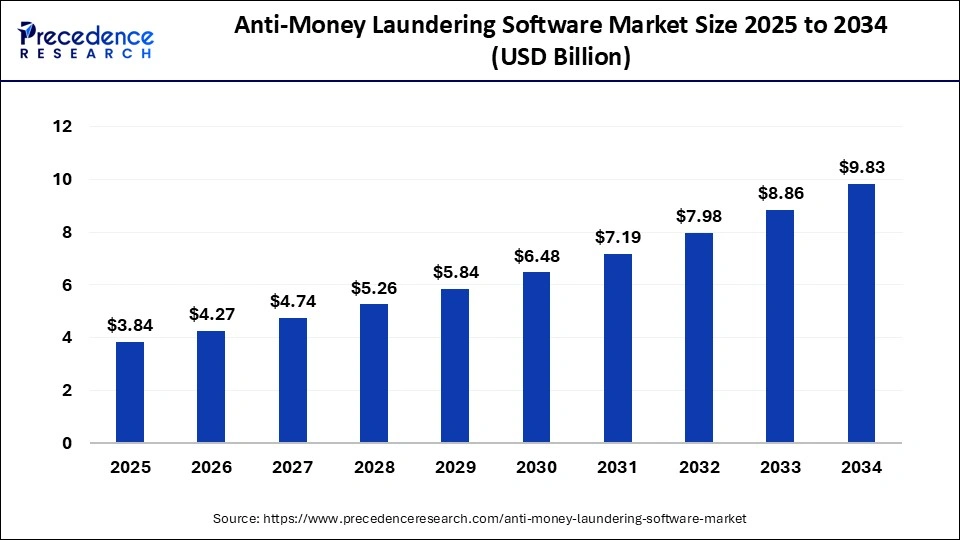

The global anti-money laundering (AML) software market is estimated at USD 3.46 billion in 2024 and is anticipated to reach around USD 9.83 billion by 2034, expanding at a CAGR of 11% from 2025 to 2034, driven by increasing regulatory scrutiny, rising financial crime, and broader fintech adoption worldwide.

AI-powered real-time fraud detection now achieves 95% accuracy in financial institutions, up from around 80% with traditional methods. This improvement highlights the value a robust Compliance & AML Platform brings to fintechs, banks, and financial service providers.

Higher Detection Accuracy Changes Compliance & AML Outcomes

For fintech apps, regulators expect strong controls, but users expect instant, frictionless experiences. Boosting detection accuracy into the mid-90s range means platforms can catch more suspicious activity while putting fewer legitimate users through unnecessary friction. That balance is where a modern Compliance & AML Platform wins.

- The problem is enormous, with 2–5% of global GDP laundered yearly, about USD 800 billion to USD 2 trillion in illicit funds flowing through the financial system annually.

- Most institutions are already facing money-laundering risk. Around 77% of financial institutions report that they have detected or suspected money-laundering activity in their operations, underscoring how widespread the issue is.

- Yet only a small fraction of alerts result in actual follow-up. Globally, about 1% of suspicious transaction reports (STRs) generated lead to further investigation, meaning most compliance effort goes into triaging low-value alerts.

- Manual work dominates fraud-related costs, according to Feedzai data, with about 25% from manual reconciliations, showing that a significant budget goes to human-heavy processes.

- Capgemini reports that machine-learning and analytics fraud-detection solutions can increase detection accuracy by up to 90% and reduce fraud-investigation time by 70%, outperforming manual or rule-based methods.

These Numbers Show a Big Market Opportunity for Compliance & AML Platforms

Combining financial crime costs, compliance expenses, and AI gains highlights a major business opportunity. Fintechs, banks, and payment firms face pressure to enhance compliance and efficiency, already investing heavily.

- Compliance spend is massive and rising. A LexisNexis study estimates financial institutions spend USD 206.1 billion annually on financial-crime compliance, about USD 3.33 per person monthly worldwide.

- Regional compliance costs highlight the urgency of efficiency. In EMEA, annual financial-crime compliance costs hit USD 85 billion, with 98% of institutions facing higher costs and 81% prioritizing cost reduction.

- According to a report, 71% of compliance professionals say their organizations are advancing data use with analytics, and 72% use analytics and AI to improve compliance.

- Financial crime causes damages surpassing compliance costs, with fraud losses exceeding USD 4.7 trillion annually. Improved detection helps meet regulations, prevent losses, and secure revenue.

Key Features of a Compliance & AML Platform for Fintech Apps

A Compliance and AML platform for fintech apps ensures regulatory adherence, monitors suspicious activities, and prevents fraud. It provides real-time insights and automated controls to safeguard both the business and its users.

1. Customer Identity Verification (KYC)

A strong AML platform begins with reliable Know Your Customer (KYC) verification. This includes ID document scanning, biometric checks, database validation, and fraud signal detection. Accurate onboarding reduces risk exposure and ensures only verified, legitimate users gain access to financial services.

2. Risk-Based Customer Profiling

The platform must automatically classify customers using a risk-based approach, evaluating factors such as geography, behavior, transaction history, and financial patterns. Dynamic profiling enables continuous risk scoring and helps fintech companies adapt controls based on evolving user activity.

3. Real-Time Transaction Monitoring

A core AML capability is real-time monitoring of all transactions to detect suspicious patterns instantly. The system evaluates behavior against predefined rules, anomaly thresholds, velocity checks, and AML typologies, allowing teams to intervene before illicit activities escalate.

4. Sanctions, Watchlist & PEP Screening

The platform should continuously screen users against global sanctions lists, watchlists, and PEP (Politically Exposed Person) databases. Automated screening ensures fintech apps remain compliant with international regulations and quickly flag high-risk individuals or entities.

5. Automated Alerting and Case Management

When unusual transactions or risk signals are detected, the system should generate automated alerts and route them into a structured case management workflow. This allows compliance teams to review, escalate, document, and resolve issues with full visibility and audit trails.

6. Machine Learning–Driven Fraud and AML Detection

To stay competitive, the platform must incorporate ML models capable of detecting complex, hidden, or emerging fraud patterns. Machine learning enhances detection accuracy, reduces false positives, and helps fintech teams stay ahead of rapidly evolving financial crime tactics.

7. Comprehensive Reporting & Regulatory Compliance

Fintech apps must support seamless reporting for regulators through automated SAR/STR filing, activity logs, evidential data export, and compliance dashboards. This ensures organizations stay aligned with AML laws, maintain transparency, and reduce manual reporting workloads.

8. Ongoing Customer Monitoring

Compliance doesn’t end after onboarding. The platform needs continuous monitoring to detect changes in customer behavior, updated sanctions data, or newly emerging risks. This ensures long-term compliance and helps fintech companies adjust controls proactively.

9. Secure Data Management & Access Control

A robust compliance platform must include encrypted storage, role-based access control, MFA, and strict data governance. Protecting sensitive customer and financial data strengthens trust and ensures compliance with privacy and security standards like GDPR or PCI DSS.

10. Integration with Fintech Ecosystem

The platform should integrate seamlessly with payment gateways, banking APIs, CRMs, data providers, fraud tools, and core fintech systems. Smooth integration reduces operational friction, improves data consistency, and accelerates compliance automation across the entire app ecosystem.

How to Build Compliance & AML Systems for Fintech Apps?

Building Compliance and AML systems for fintech apps requires embedding regulatory rules, real-time monitoring, and automated alerts. This ensures fraud detection, legal compliance, and protection for both the business and its users.

1. Consultation

We begin with a focused consultation phase to understand your regulatory obligations, customer verification needs, transaction workflows, and risk appetite. This alignment helps us define a compliance strategy tailored to your fintech model rather than relying on generic AML templates or assumptions.

2. Regulatory Requirements Analysis

Our team evaluates the specific regulatory frameworks that apply to your market such as FATF, AMLD, FinCEN, or local KYC laws. We map mandatory controls, reporting standards, and screening rules to ensure the platform’s architecture supports full, long-term compliance from day one.

3. Use Case & Risk Scenario Definition

We identify key compliance use cases, including onboarding checks, transaction monitoring, sanctions screening, and fraud detection. By defining high-risk scenarios early, we ensure the platform is engineered to detect real-world patterns rather than relying solely on predefined AML rules.

4. Data Architecture & Integration Planning

Our developers design a secure data architecture that supports live ingestion of customer, transaction, and third-party compliance data. We plan integrations with identity providers, sanctions databases, banking APIs, and internal systems to ensure seamless, accurate data flow across the platform.

5. KYC & Identity Verification Engine Development

We build or integrate a KYC engine capable of document verification, biometrics, liveness checks, and risk-based profiling. This module ensures only legitimate users enter your fintech ecosystem and establishes a strong foundation for downstream AML monitoring.

6. Sanctions, Watchlist & PEP Screening Module

Our team develops automated screening pipelines connected to sanctions lists, watchlists, and PEP databases. This module runs continuous checks, handles list updates, and flags high-risk individuals instantly, eliminating manual screening delays and reducing compliance risk.

7. Real-Time Transaction Monitoring System

We design a monitoring engine that evaluates transactions using rules, anomaly detection, velocity checks, and behavioral patterns. This real-time AML system ensures suspicious activities are detected immediately, supporting both regulatory requirements and operational fraud prevention.

8. ML-Based Risk Scoring & Fraud Detection

Our engineers implement machine learning models that enhance detection accuracy, reduce false positives, and adapt to new criminal tactics. These models analyze customer behavior, transaction sequences, and historical data to generate dynamic, context-rich risk scores.

9. Alerting & Case Management Workflow

We build structured workflows that automatically create alerts and case files for suspicious activities. Compliance teams can review evidence, assign tasks, escalate decisions, and maintain a complete audit trail ensuring every investigation meets regulatory scrutiny.

10. Testing & Launching

We rigorously test the platform through simulated fraud patterns, sanctions hits, onboarding failures, and data-edge cases. After validating regulatory accuracy and system stability, we deploy the solution with monitoring tools, ensuring a smooth launch and reliable compliance performance from day one.

Cost Breakdown for Building a Compliance & AML Platform

Before estimating the budget, it’s important to note that AML and compliance systems require multiple technical layers like data architecture, identity verification, ML models, and real-time monitoring. Each phase adds unique value and contributes differently to the overall cost.

| Development Phase | Description | Estimated Cost |

| Consultation | Understanding requirements, mapping regulations, and defining key compliance scenarios. | $6,000 – $10,000 |

| Architecture & Integration Planning | Designing data pipelines, system architecture, and integration strategy. | $14,000 – $25,000 |

| KYC & Identity Verification Module | Implementing document checks, biometrics, and risk-based customer verification. | $12,000 – $18,000 |

| Sanctions, Watchlist & PEP Screening | Adding automated screening against global sanctions, watchlists, and PEP databases. | $14,000 – $26,000 |

| Transaction Monitoring & AML Engine | Building rule-based monitoring, anomaly detection, and suspicious activity triggers. | $15,000 – $29,000 |

| ML-Based Risk Scoring & Fraud Detection | Developing models for dynamic scoring, fraud detection, and reducing false positives. | $18,000 – $32,000 |

| Alerting, Case Management & Reporting | Creating alert workflows, investigation tools, and compliance reporting features. | $7,000 – $13,000 |

| Testing & Launching | Performing simulations, audits, deployment, and post-launch monitoring setup. | $9,000 – $20,000 |

Total Estimated Cost: $70,000 – $130,000

Note: Actual costs may vary based on regulatory jurisdiction, integration needs, data providers, and the complexity of ML-driven detection. Additional customization, UI design, and continuous optimization can also affect the overall budget.

Consult with IdeaUsher for a precise estimate and a tailored development roadmap for your Compliance & AML platform. Our team builds secure, scalable, and regulation-ready systems designed specifically for fintech growth.

Tech Stack Recommendation: Compliance & AML Platform Development

Here’s the ideal tech foundation to build a secure, scalable, and regulation-ready compliance and AML platform.

1. Backend Technologies

Node.js, Python (Django/FastAPI), or Java enable scalable API development, real-time processing, and secure handling of compliance workflows, transaction monitoring, and AML logic.

2. Frontend Frameworks

React or Angular offer responsive dashboards, case management interfaces, and real-time alert views for compliance teams.

3. Database & Storage

PostgreSQL, MongoDB, and Redis support structured customer data, unstructured logs, sanctions lists, and fast retrieval for monitoring and scoring.

4. Identity Verification & KYC Tools

Solutions like Onfido, Veriff, or Jumio provide document verification, biometrics, and liveness checks to validate customer identities securely.

5. Sanctions & Watchlist Screening APIs

Integration with ComplyAdvantage, Refinitiv World-Check, or Dow Jones ensures up-to-date sanctions, PEP, and watchlist data for continuous screening.

6. AML & Fraud Detection Engines

Custom ML models built with TensorFlow or PyTorch analyze behavioral patterns, reduce false positives, and adapt to emerging fraud tactics.

Monetization Model of a Compliance & AML Platform

A successful compliance and AML platform relies on a monetization model that reflects the value it delivers in accuracy, automation, and risk reduction. By aligning pricing with usage, features, and regulatory demands, these platforms can scale sustainably while meeting the needs of fintech businesses.

1. Subscription-Based Pricing (SaaS Model)

Fintech companies pay a recurring monthly or annual subscription fee to access the platform. Pricing tiers typically vary based on features, user seats, data volume, and level of automation, allowing startups and enterprises to choose plans suited to their scale.

2. Pay-Per-Verification (KYC Charges)

Platforms charge for each identity verification, document check, biometric scan, or liveness test performed. This model aligns revenue with onboarding volume, making it ideal for fintechs that scale rapidly or experience fluctuating user activity.

3. Custom Enterprise Licensing

Large financial institutions often require custom modules, advanced reporting, complex integrations, and high-volume capacity. Enterprise licensing offers tailored pricing, dedicated support, and long-term contracts, providing predictable multi-year revenue.

4. API Usage Fees

Fintech apps integrating deeply through APIs may be charged based on API call volume. This usage-based model ensures fintechs pay only for what they consume while incentivizing efficient integration.

Top Compliance & AML Platforms for Fintech Apps

Top Compliance and AML platforms for fintech apps help businesses meet regulatory requirements, detect suspicious activity, and prevent fraud. They provide real-time monitoring, automated reporting, and risk management tools tailored for financial services.

1. Unit21

Unit21 is a flexible compliance and fraud platform with configurable KYC, transaction monitoring, case management, and AML workflows. Its no-code rule engine and extensive API support suit fintechs needing quick, scalable compliance automation without heavy engineering.

2. ComplyAdvantage

ComplyAdvantage provides real-time AML screening, sanctions monitoring, and risk intelligence powered by machine learning. It helps fintechs quickly detect PEPs, high-risk entities, and suspicious behavior through global data coverage, making it one of the most trusted platforms for automated AML and financial crime prevention.

3. Trulioo

Trulioo is a global identity verification platform offering KYC, KYB, AML screening, and document verification across hundreds of countries. Fintechs use it to streamline customer onboarding, verify businesses, and meet regulatory requirements through a single API designed for scalability and international compliance.

4. Sumsub

Sumsub delivers end-to-end identity verification, KYC/AML checks, biometric authentication, liveness detection, and fraud prevention. Its unified compliance platform helps fintech apps onboard users securely, reduce fraud risks, and maintain global regulatory compliance while offering onboarding flows optimized for speed and user experience.

5. Sardine

Sardine is a modern fraud, compliance, and risk platform built specifically for fintechs, neobanks, and crypto companies. It provides transaction monitoring, behavioral analytics, KYC/AML checks, and real-time fraud prevention, helping fintech apps identify risky users, prevent account abuse, and streamline compliance workflows through a unified API.

Conclusion

A Compliance & AML Platform for Fintech Apps ensures that financial applications meet regulatory standards while detecting and preventing fraudulent activities. By integrating real-time monitoring, automated reporting, and advanced verification tools, fintechs can safeguard customer assets and maintain trust. Such a platform not only minimizes legal and financial risks but also streamlines operational efficiency, allowing teams to focus on innovation. Prioritizing compliance and anti-money laundering measures strengthens credibility, supports sustainable growth, and provides a secure foundation for both users and business operations in the competitive fintech landscape.

Why Choose IdeaUsher for Your Compliance & AML Platform for Fintech Apps?

IdeaUsher designs robust compliance and AML systems that support fintech applications with secure onboarding, transaction monitoring, and regulatory reporting. Our experience ensures your app meets global standards while providing smooth user experiences.

Why Work with Us?

- Fintech Development Track Record: We built solutions like JABA PAY, a secure digital payment app that required strong compliance and data security.

- Tailored Compliance Architecture: From KYC/KYB flows to AML screening and reporting, we customize every module to fit your regulatory scope.

- Security & Privacy First: Our implementations leverage encryption, secure authentication, and compliance-ready data handling practices.

- Scalable & Maintainable: Solutions are built to accommodate growth, regulatory changes, and evolving threat landscapes.

Explore our portfolio to see how we helped businesses launch their product in the market.

Reach out today for a consultation to build your Compliance & AML platform.

FAQs

A compliance and AML system ensures fintech apps follow regulatory standards and detect suspicious activity. It monitors user behavior, verifies identities, and automates reporting to prevent fraud and financial crimes while maintaining trust with regulators and customers.

Key features include KYC verification, risk scoring, transaction monitoring, sanctions screening, and automated reporting. These capabilities help fintech apps identify potential fraud, reduce manual oversight, and maintain regulatory accuracy across all user and transaction flows.

AML tools analyze user data, transactions, and behavior patterns to detect irregular activity. They flag suspicious actions, generate alerts, and support investigations. This proactive monitoring helps fintech companies reduce exposure to fraud while enhancing customer security.

AML systems utilize AI models, rule based screening engines, secure databases, and cloud infrastructure. These technologies help process high volumes of data, deliver accurate results, and maintain compliance across changing regulations without affecting app performance.