Key Takeaways

- Banks are replacing legacy systems with enterprise loan origination software to streamline approvals and improve efficiency.

- Platforms like nCino combine digital onboarding, AI underwriting, workflow automation, and cloud-native architecture to streamline enterprise lending.

- A successful platform requires AI-driven document processing, compliance automation, banking integrations, secure cloud infrastructure, and analytics dashboards.

- Cloud-native loan origination platforms deliver faster deployment, lower operating costs, greater scalability, and better enterprise collaboration than legacy systems.

- How Idea Usher can help businesses build enterprise loan origination software with AI automation, secure banking integrations, and scalable fintech solutions.

Enterprise lending has changed dramatically over the last few years. Financial institutions are handling more loan applications, stricter regulations, and borrowers who expect faster decisions. That’s why enterprise loan origination platforms like nCino are becoming the preferred choice. Instead of relying on disconnected systems and manual processes, banks can manage the entire lending journey from a single platform. The result is faster approvals, better operational efficiency, and a smoother experience for both lenders and borrowers.

We’ve developed numerous enterprise loan origination software solutions that streamline lending workflows using workflow automation and cloud-native architecture. As we have this expertise, we’re sharing this blog to discuss the steps to develop enterprise loan origination software like nCino.

Market Size of Enterprise Loan Origination Softwares

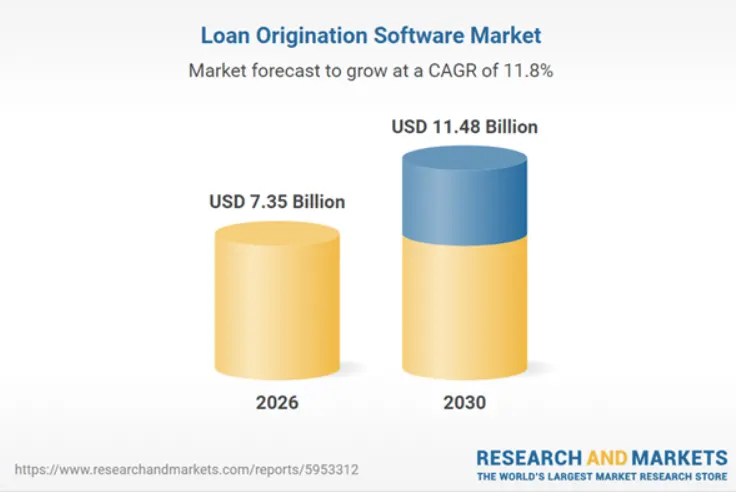

According to Research and Markets, the loan origination software market is expected to grow from $6.58 billion in 2025 to $7.35 billion in 2026, at a CAGR of 11.8%. This growth is driven by financial institutions replacing legacy lending systems with modern platforms that automate loan processing, speed up approvals, and improve the overall lending experience.

Source: Research and Markets

Consider the success of market giants like nCino. By building a cloud-based operating system that integrates seamlessly with commercial banking pipelines, they generated over $540 million in annual revenue. Allocating capital toward developing a proprietary enterprise LOS means entering a market backed by this exact type of institutional demand. As credit markets expand globally, the infrastructure supporting these transactions must scale accordingly. This shift turns a traditionally slow operational process into a highly lucrative tech stack opportunity.

Growth and CAGR Forecast

The global enterprise loan origination software market has moved past the early adoption phase and is now in a period of aggressive compounding growth. Valued comfortably at over $7 billion, the market is sustaining a compound annual growth rate of roughly 11%. This consistent CAGR indicates that spending on lending infrastructure is outpacing general IT budget increases across the financial sector.

Long-term industry forecasts show no signs of plateauing. The addressable market is expanding geographically as emerging economies modernize their banking systems, alongside developed markets upgrading to cloud-native solutions. For an investor, this represents a reliable macroeconomic tailwind where the target audience is well-funded and highly motivated to buy.

Why Banks Invest in Digital

Institutional lenders are not updating their software simply to stay modern. They are doing it because legacy infrastructure erodes their bottom line. The decision to purchase or upgrade an enterprise lending platform is driven by clear operational realities:

- Drastic Processing Speed: Traditional commercial loan origination can take weeks. Modern platforms cut this down to hours or days, directly impacting a bank’s quarterly loan volume.

- Predictive AI Underwriting: Advanced platforms use machine learning to evaluate risk. This allows institutions to approve more loans safely by analyzing unconventional data points alongside traditional credit scores.

- The Cloud Shift: Moving to cloud-native architecture reduces on-premise maintenance costs while giving financial institutions the elasticity to handle sudden spikes in loan applications.

- Automated Compliance: Financial regulations shift constantly. Modern software automates compliance checks, shielding banks from costly regulatory fines and audit failures.

A great real-world example of this value proposition in action is Blend Labs. By focusing heavily on streamlining the consumer and mortgage loan application journey, their platform model captures massive volume, driving over $120 million in annual revenue. Ultimately, customer expectations have changed. Institutional borrowers now demand the same smooth, digital experience they get from consumer fintech apps. Banks that fail to deliver this user experience lose market share to agile, digital-first competitors.

New B2B SaaS Opportunities

Large banks, credit unions, and financial institutions continue to invest heavily in modern lending technology. Since enterprise lending involves unique workflows, compliance requirements, and internal processes, many organizations prefer custom-built loan origination software over generic solutions. This creates a strong opportunity for technology companies to develop tailored enterprise lending platforms.

For founders and investors, an enterprise-grade loan origination platform can become a valuable long-term asset. A secure, scalable, and compliant solution not only attracts enterprise clients but also creates recurring SaaS revenue and the potential for strategic partnerships or acquisitions as demand for digital lending continues to grow.

nCino’s Growth into Enterprise Banking

nCino started as a commercial lending platform and has grown into a complete cloud banking solution for financial institutions. Today, it supports commercial, consumer, small business, and mortgage lending while also helping banks with customer onboarding and account opening. This evolution shows how a focused lending platform can expand into an enterprise banking system that simplifies operations and delivers a better customer experience.

Commercial Lending Automation

The initial success of the platform relied entirely on unseating outdated, manual processes within commercial and small business lending lines. Commercial loans are notoriously complex, requiring extensive document collection, financial spreading, risk rating, and multi-tier approval workflows. By digitizing these exact workflows, the platform allowed relationship managers and credit analysts to collaborate in a single cloud workspace.

This concentration on high-ticket commercial accounts proved to be highly lucrative. The core software engine was built to handle complex corporate balance sheets, legal entity structures, and compliance requirements that generic customer relationship management tools could not touch. This narrow, high-value problem focus allowed the vendor to capture early market share among regional and national banks, proving that financial institutions were willing to pay premium prices for highly specialized workflow tech.

Expansion and Onboarding

Once firmly embedded in the commercial departments of major banks, the development strategy shifted toward complete vertical expansion. The goal was to eliminate the need for banks to buy separate point solutions for different departments. The platform gradually added modules for:

- Retail consumer lending

- Residential mortgage origination

- Digital account opening

- Institutional onboarding and compliance

This end-to-end framework transformed the platform into a critical layer of modern banking infrastructure. The financials match the scale of this expansion. Total annual revenues reached $594.8 million, showing a steady 10% increase year over year. Subscription-based revenue drives the vast majority of this capital, bringing in $523.1 million annually.

The revenue model relies heavily on long-term enterprise commitments, netting an annual contract value of $602.4 million. B2B founders can learn a lot from their enterprise monetization strategy. Beyond standard software access fees, the total cost of ownership for a bank scales through mandatory Salesforce platform licensing, tiered pricing based on asset size or loan volume, and massive multi-million-dollar systems integration consulting fees.

AI-Powered Banking

Modern enterprise lending platforms are increasingly using AI to automate manual tasks and improve decision-making. Features like automated financial data extraction, portfolio monitoring, and real-time risk analysis help lenders work more efficiently and identify potential issues earlier. This shift shows that intelligent automation is becoming a key advantage for enterprise loan origination software.

How Does the nCino Bank Operating System Work?

The nCino platform functions as a single software-as-a-service architecture built entirely on top of the Salesforce platform. It acts as a unified digital layer that consolidates complex retail, commercial, and mortgage workflows. Rather than forcing a bank to jump between isolated legacy systems, it digitizes operations across the lifecycle of a financial product.

For software investors, this system serves as a prime case study in high-ticket enterprise business models. While smaller setups start at roughly $175 per user monthly, larger deployments scale through multi-year contracts ranging from three to five years. This contract structure secures highly predictable recurring cash flows.

1. A Unified Platform

Legacy banking systems fail because they isolate data within separate departments. Commercial loan origination, retail account opening, and compliance reporting frequently run on completely different software vendors. This tool solves that friction by pulling every single capability into a central hub.

The cloud platform handles loan creation, customer onboarding, deposit accounts, and deep portfolio analytics inside one shared dashboard. Employees work from a unified source of truth, removing data silos. This approach lowers IT maintenance costs while giving the front and back offices total visibility into every current transaction.

2. Connected Workflows

The software creates a continuous loop where a customer’s profile transfers smoothly from initial intake to underwriting and ongoing service.

- Intake & Onboarding: The journey begins with automated digital account opening, running integrated KYC and KYB compliance checks right at the start.

- Data Reusability: When that same client requests a commercial or mortgage loan, the platform pulls their verified credentials instantly into the origination pipeline.

- Underwriting & Management: Analysts review financial spreading, structure the credit terms, and pass the file to active portfolio monitoring without manual data re-entry.

This connectivity drastically reduces the expensive process friction that traditionally forces financial firms to spend thousands of dollars just to onboard a single corporate account.

3. AI and Automation

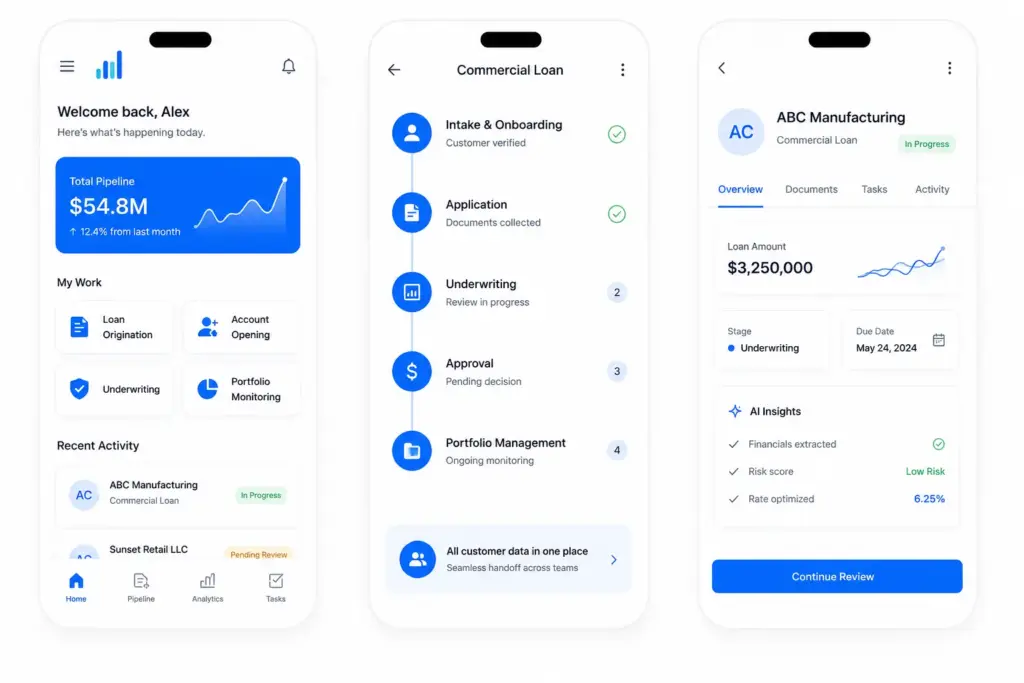

Embedded artificial intelligence acts as the core engine driving efficiency across the entire platform. Using integrated analytics and machine learning tools, the operating system automates document data extraction and handles complex pricing modeling. Advanced rate optimization modules instantly calculate loan profitability, confirming deals hit specific internal return metrics before final approval. This real-time automation allows banks to collaborate faster across remote departments and build hyper-personalized banking products.

Key Features of an Enterprise Loan Origination Software like nCino

Building an enterprise loan origination system starts with understanding how banks manage lending at scale. Platforms like nCino show that financial institutions value automation, faster workflows, and a unified lending process. Studying these capabilities can help businesses build software that meets enterprise needs and stands out in the B2B fintech market.

1. Digital Onboarding and KYC Automation

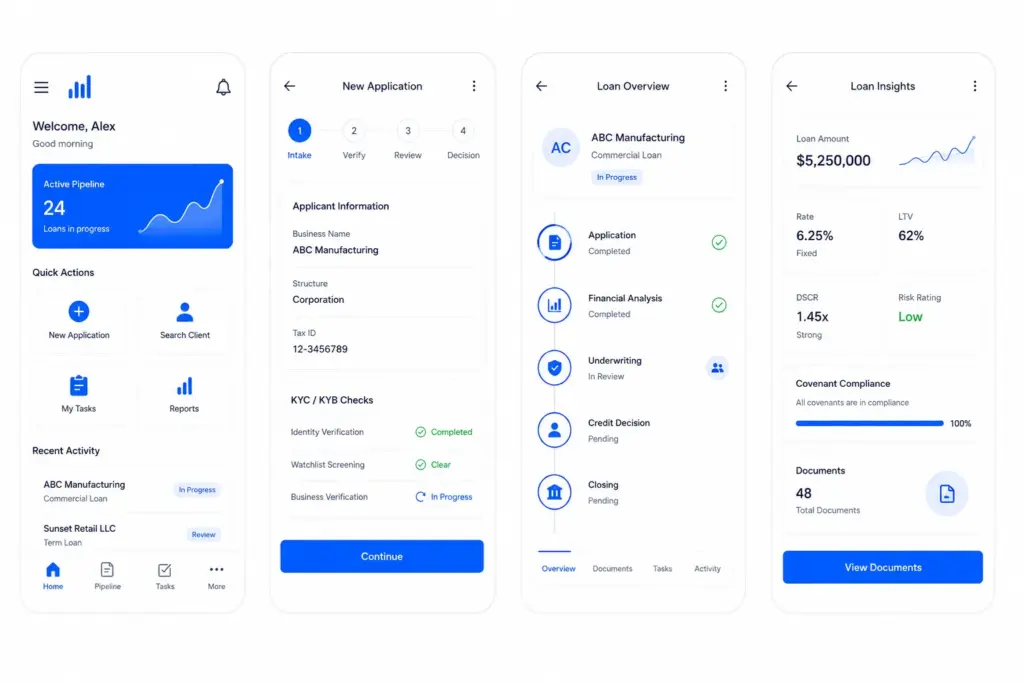

Front-line teams use nCino to capture new customer relationships through a fully white-labeled digital interface. The intake engine handles complex corporate structures alongside standard retail applicants, ensuring that no client data falls out of the pipeline during early data collection.

Behind the scenes, the platform connects directly with external identity verification bureaus. Compliance teams rely on this automated background check to process continuous Know Your Customer and Know Your Business checks in real time, moving applications from intake to verification with zero manual data entry.

2. End-to-End Loan Origination Workflows

Lending departments use nCino to manage every phase of the commercial and retail loan lifecycle from a single application interface. Relationship managers, credit analysts, and operations teams log into the same cloud workspace to progress deals through structural creation, financial spreading, risk rating, and closing documentation.

- Deal Management: Relationship managers use interactive pipelines to view ongoing loan files and track variable pricing metrics across corporate syndications.

- Structured Routing: Credit officers rely on integrated policy engines to pass files smoothly between multi-tiered department hierarchies for final sign-off.

- Post-Close Monitoring: Loan ops teams utilize active covenant tracking modules to track asset compliance indicators long after the funds deploy.

3. AI Underwriting and Credit Decisions

Underwriters use nCino to drastically cut down the time spent extracting numbers from tax returns, balance sheets, and complex corporate financial filings. The system leverages integrated machine learning models to read unstructured document uploads and populate financial analysis fields automatically.

Credit committees use these automated data flows to run complex sensitivity analysis models instantly. Lenders can quickly test portfolio exposure against variable interest rate changes and shifts in net operating income without manually building custom spreadsheets.

4. Intelligent Document and Data Management

nCino helps banks securely manage loan documents from a single platform. Teams can easily collaborate, maintain audit records, and reduce document errors. Some institutions have lowered loan document exceptions from around 11% to under 4% after implementing the system.

5. Workflow Automation

Risk officers use nCino to ensure every staff interaction aligns perfectly with the bank’s internal lending policies. The workflow engine enforces explicit rules, blocking a user from moving a deal forward if specific document requirements or credit checks are missing. Operations managers use the automated task router to distribute work based on team capacity and specific underwriting expertise.

This structural automation generates a permanent, clear audit trail that lets institutional compliance teams prove regulatory alignment without tracking down paper documentation.

6. Omnichannel Account Opening

Retail and commercial customers use nCino to start applications on one channel and finish them on another without losing their progress. A corporate treasurer can start a loan request on a desktop computer, upload documents via a mobile phone, and review final details with a branch agent.

Bank workers use the exact same dashboard layout as the borrower, viewing updates across physical locations and remote service centers in real time. This unified view removes communication friction, ensuring clients receive the same branding and service quality regardless of how they choose to connect with the institution.

7. Analytics, Dashboards, and Insights

Executive leaders use nCino to maintain continuous visual control over the bank’s collective credit exposure and deal pipeline. Real-time charts display live concentration metrics by industry sector, geographical location, and specific credit tier.

- Pipeline Tracking: Managers check interactive dashboards to spot bottlenecks in the underwriting queue before deal volumes back up.

- Staff Tracking: Executives use performance analytics to monitor processing speeds and review individual team output.

- Risk Intelligence: Analysts rely on automated alert trackers to highlight emerging defaults inside the portfolio early.

How to Develop an Enterprise Loan Origination Software like nCino?

Building an enterprise loan origination system requires secure technology that is easy for banking teams to use. We design scalable lending platforms that meet banking compliance requirements while delivering fast and efficient workflows. Our development approach helps businesses build enterprise-ready software that can grow with their needs.

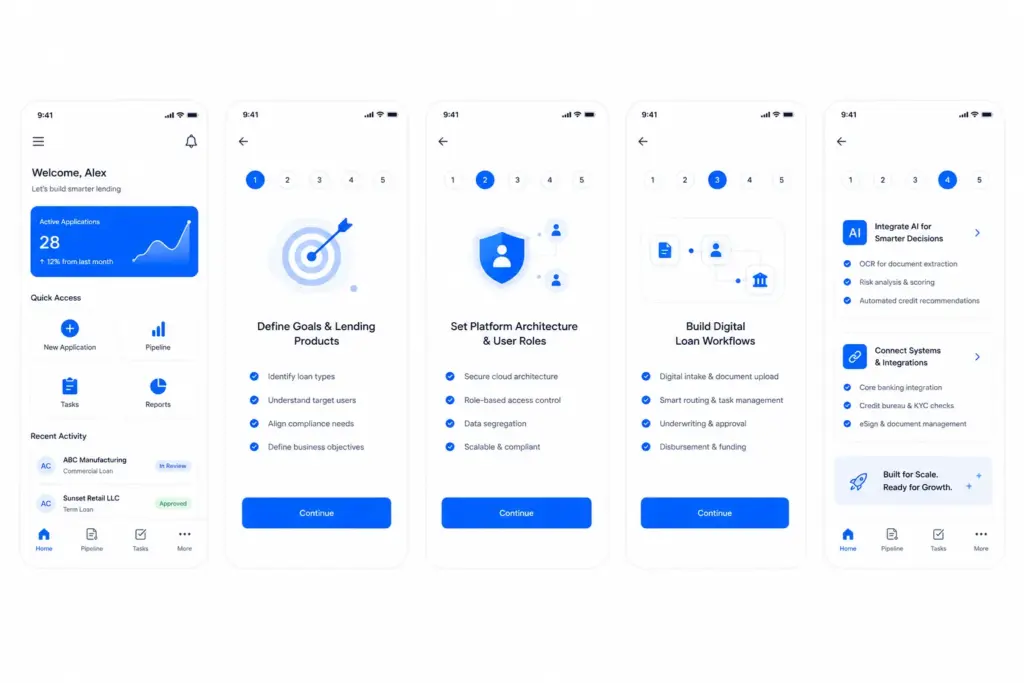

1. Lending Products and Business Goals

Before writing any code, we collaborate with you to define the exact scope of your digital platform. We isolate the specific loan types your software will process, whether you are targeting commercial real estate lenders, small business credit lines, or high-volume retail mortgages.

Different target buyers bring different internal workflows and strict compliance rulebooks. Our product engineering teams map these regulatory frameworks early in the discovery phase. This ensures that the base architecture naturally handles regional lending laws, giving your sales team a compliant, market-ready asset from day one.

2. Platform Architecture and User Roles

A strong enterprise lending platform starts with a secure and scalable cloud architecture. We build systems with role-based access controls so every user only sees the data and tools relevant to their role. This approach improves security, supports compliance, and allows financial institutions to scale their operations with confidence.

3. Build Digital Loan Workflows

A successful platform must turn messy document collection into an elegant, automated assembly line. We build responsive borrower application portals that allow clients to input records and upload financial histories without hitting structural errors.

- Intake Systems: Clean data fields capture corporate entity details and individual identification smoothly.

- Routing Logic: Smart task management engines move files automatically to the correct underwriting queue based on deal size.

- Funding Portals: Integrated disbursement pipelines push approved loan capitals directly into consumer checking accounts.

4. Integrate AI for Faster Lending Decisions

To compete with industry leaders, your platform needs intelligent automation. We implement advanced Optical Character Recognition tools to read messy uploaded tax returns and corporate balance sheets instantly. Our development teams train machine learning models to analyze this extracted financial data against custom risk parameters. The software spots suspicious balance sheet adjustments, calculates debt-to-income ratios, and serves up automated credit recommendations. This helps human underwriters approve complex loan files up to 60% faster.

5. Connect Banking and Third-Party Systems

An enterprise platform cannot operate in a vacuum. We build custom API pipelines that tie your loan origination software directly into legacy core banking architectures. We build pre-configured bridges to major credit bureaus, automated e-signature solutions, and global identity verification networks.

This deep connectivity enables immediate background checks and instant compliance validation. Borrowers execute binding contracts digitally without ever leaving your software ecosystem, maximizing conversion rates.

6. Ensure Security and Scalability

Financial software is a constant target for sophisticated cyber threats. We protect your platform using bank-grade encryption protocols for data moving across the cloud or resting inside your databases. Our engineers implement continuous tracking logs that record every single user interaction. This creates an unchangeable audit trail that lets institutional buyers easily prove policy compliance to regulatory officials during routine annual bank examinations.

7. Test and Continuously Improve

Enterprise lending platforms must remain reliable even under heavy transaction volumes. We thoroughly test performance, deploy updates in stages, and continuously monitor the platform to ensure stability. This approach helps us deliver secure, scalable lending software that financial institutions can depend on.

Cost to Develop an Enterprise Loan Origination Software like nCino

Allocating capital to build custom enterprise loan origination software requires a clear understanding of financial realities. For serious investors and tech entrepreneurs, engineering a proprietary lending platform means building an asset that can either scale a lending business or target banks as a high-margin B2B SaaS provider.

The overall budget depends entirely on the operational depth, target market scale, and structural complexity required. By working with dedicated product engineering groups like us at IdeaUsher, you can align your technical budget directly with long-term commercial goals.

Estimated Cost by Development Stage

The upfront engineering capital scales according to the complexity of the credit products and the level of internal process automation required. Launching a lean minimum viable product allows you to validate workflows in live markets before committing capital to a full-scale multi-product banking platform.

| Platform Tier | Technical Scope | Development Timeline | Estimated Investment |

| Minimum Viable Product (MVP) | Single loan product, basic borrower portal, automated KYC, rule-based scoring, e-signatures | 3 to 4 Months | $20,000 to $50,000 |

| Mid-Market Platform | Multi-product support, advanced AI underwriting, live portfolio analytics, third-party core integrations | 5 to 8 Months | $50,000 to $90,000 |

| Enterprise-Grade System | High-volume engines, custom predictive ML models, multi-market compliance, full multi-tenant white-label structures | 10 to 16 Months | $100,000 to $250,000+ |

How to Optimize Development Costs

Building an institutional-grade lending system does not mean overspending on unnecessary early-stage code. We focus heavily on clean product roadmaps to keep development capital highly efficient:

- Prioritize a Core Matrix: Avoid building engines for five distinct loan types at launch. Start by refining a single high-margin workflow, such as commercial lines or personal credit, before duplicating that code across other products.

- Modular Architecture Strategy: We structure your platform using containerized microservices. This design choice isolates distinct components like document intake and identity verification, allowing our squads to update specific modules without rebuilding the entire system.

- Cloud-Native Micro-Scaling: Utilizing cloud infrastructure keeps upfront server maintenance costs minimal. The backend resources scale down automatically during slow periods and ramp up during application spikes, avoiding expensive idle compute time.

- Phased Rollouts: Building a secure MVP allows you to generate live operational feedback using real loan applications. This live data ensures future development capital is spent exclusively on features that active credit teams value most.

Key Factors That Influence Development Cost

Every specialized API connection and automated logic branch added to your system directly shapes the final development timeline. Understanding these core financial drivers helps you maintain control over the product budget:

- AI and Data Processing Depth: Simple rule-based validation engines are inexpensive to implement. Integrating advanced machine learning models that automatically extract text from messy corporate financial uploads adds engineering hours.

- Third-Party API Integrations: Tying your code securely into regional credit bureaus, background check systems, and old core banking software requires extensive technical mapping and testing.

- Compliance Matrix: Building a platform that meets strict guidelines across multiple legal jurisdictions adds data isolation layers and complex logging tasks.

- Role-Based Access Complexity: Designing custom dashboards and strict data boundaries for relationship managers, underwriters, risk heads, and external audit teams requires more design resources.

Cloud-Based vs On-Premise Software: Which Has Better Business Value?

Choosing the right deployment model has a direct impact on the cost, scalability, and long-term success of an enterprise loan origination platform. We help businesses evaluate their requirements and build secure, high-performance lending solutions that align with enterprise needs and support future growth.

Cost, Scalability, and Deployment Speed

On-premise lending platforms require significant upfront investment in infrastructure and usually take longer to deploy. In contrast, cloud-based solutions reduce initial costs and allow businesses to launch much faster while scaling resources as demand grows. This flexibility makes cloud deployment a practical choice for organizations that want to expand their lending operations without investing in additional hardware.

To help evaluate the structural differences between these two models, the table below highlights key performance and financial metrics based on standard financial software deployments:

| Deployment Factor | On-Premise Architecture | Cloud-Native Infrastructure |

| Upfront Capital (CapEx) | High investment ($10,000+ per server array plus core software licensing) | Minimal initial setup (Subscription and usage-based access) |

| Launch Timeline | Typically 12 to 18 months due to hardware procurement and manual provisioning | Typically 3 to 6 months using pre-configured API systems |

| Scaling Capability | Limited by fixed physical server hardware limits | Elastic auto-scaling based on real-time transaction volume |

| System Maintenance | Maintained entirely by internal bank IT departments | Automatically managed and upgraded by the platform vendor |

| Operational Savings | Higher total cost of ownership over time due to hardware refreshes every 3–5 years | Typically 10% to 20% lower continuous operational overhead |

Security, Compliance, and Data Control

On-premise and cloud deployment each offer different advantages for enterprise lending platforms. Many traditional banks still choose on-premise infrastructure because it gives them full control over sensitive customer data. However, maintaining servers, applying security updates, and managing hardware also increases IT costs and operational effort.

Cloud-based platforms have become a popular choice because they provide strong security, easier scalability, and continuous updates without the same maintenance burden. This shift is reflected in the market, with Q2 Holdings reporting more than $802 million in annual recurring subscription revenue, showing the growing confidence financial institutions have in cloud-native banking software.

Which Deployment Model Delivers Better Value?

The best architecture choices depend on the specific business stage and operational goals of the target purchasing institution:

- Fintechs and Community Banks: Cloud deployment delivers rapid time-to-market advantages, lower entry costs, and flexible API pipelines that allow smaller firms to compete effectively with industry giants.

- Large Tier-1 Enterprises: Legacy institutions often protect their core systems by adopting hybrid cloud strategies, keeping sensitive credit accounting on internal servers while running borrower portals in the cloud.

- Alternative High-Yield Lenders: Niche lending providers choose specialized cloud setups like TurnKey Lender, an AI-powered system pulling in an estimated $19 million in annual revenue, to gain immediate access to plug-and-play alternative scoring models.

Build Enterprise Loan Origination Software with Idea Usher

Building enterprise fintech software requires experience with large-scale systems, security, and regulatory compliance. We help businesses turn their ideas into enterprise-ready lending platforms by combining strong engineering practices with scalable technology, reducing development risks and supporting long-term growth.

End-to-End Development

Building an enterprise loan origination platform requires expertise across every stage of product development. We manage the complete development lifecycle, from planning and UI/UX design to cloud architecture, AI integration, and secure deployment. This ensures your platform is scalable, reliable, and ready to support enterprise lending operations.

Launch a Future-Ready Platform

Enterprise lending platforms need to adapt as business and regulatory requirements evolve. Our team builds scalable solutions with a modular architecture that makes it easier to add new features, integrate third-party services, and support long-term growth. This approach helps businesses launch faster while keeping their platform flexible for future expansion.

Why Financial Institutions Choose Idea Usher

Deploying high-stakes financial technology requires an elite engineering foundation. Our development capabilities are built on deep enterprise software experience and rigorous execution:

- Elite Engineering Teams: With over 500,000 hours of combined coding experience, our team of ex-MAANG/FAANG developers applies premium product standards to every module we ship.

- Deep R&D Bench: A specialized workforce of 250+ technology experts focuses heavily on AI-first systems and modern database design.

- Proven Track Record: Over 1,000 successful digital projects delivered across highly regulated markets globally.

- Security Focus: Strategic data encryption and unchangeable transaction logs are built directly into the foundation of our systems.

Conclusion

Enterprise loan origination software like nCino is changing how financial institutions manage lending. Banks are investing in platforms that simplify operations, improve efficiency, and support future growth. If you’re planning to build a similar solution, focusing on scalability, security, and automation from the start will help you create a platform that delivers long-term value.

Things to Know About Enterprise Loan Origination Softwares

A1: Enterprise loan origination software is a platform that helps banks and lenders manage the entire lending journey in one place. Instead of relying on spreadsheets, emails, and disconnected systems, teams can onboard borrowers, review applications, approve loans, and track every stage through a single workflow. This not only speeds up lending but also creates a better experience for both employees and customers.

A2: Any organization that processes a high volume of loans can benefit from enterprise loan origination software. This includes banks, credit unions, mortgage lenders, commercial lenders, fintech companies, and NBFCs. If your lending team spends too much time on manual reviews or struggles with disconnected systems, an enterprise platform can significantly improve efficiency and consistency.

A3: A good enterprise platform should make lending easier rather than more complicated. It should allow borrowers to apply online, automate document collection, guide underwriters through the approval process, and keep all stakeholders updated in real time. Modern platforms also include AI-powered document processing, compliance checks, and integrations with banking systems so lenders can make faster and more informed decisions.

A4: Yes. AI is helping lenders reduce repetitive work while making decisions faster. It can extract information from financial documents, flag missing information, identify potential fraud, and assist underwriters with risk analysis. Rather than replacing lending professionals, AI gives them better insights so they can focus on complex cases instead of routine tasks.