Key Takeaways

- The demand for AI lending platforms is transforming digital lending with faster approvals, smarter underwriting, and data-driven credit decisions.

- Platforms like Upstart combine AI credit scoring, automated loan origination, risk-based pricing, and portfolio analytics to improve lending efficiency.

- A successful platform requires machine learning models, fraud detection, KYC/AML compliance, banking integrations, and secure cloud infrastructure.

- Development costs depend on AI complexity, regulatory compliance, third-party integrations, data engineering, and advanced automation features.

- How Idea Usher can help businesses build AI lending platforms with custom AI underwriting, secure banking integrations, and scalable fintech architecture.

The economics of digital lending are changing faster than ever. What used to give lenders a competitive edge has now become an expectation. Borrowers want quicker decisions, while financial institutions need better ways to evaluate risk without increasing defaults. That’s why AI lending platforms are gaining so much attention, because they don’t just make loan approvals faster. They also help lenders make better credit decisions by looking beyond traditional credit scores. By analyzing a wider range of financial and behavioral data, AI can identify creditworthy applicants who might otherwise be rejected

We’ve built numerous advanced AI lending solutions that leverage machine learning models and alternative data analytics to deliver faster, smarter credit decisions. As we have this expertise, we’re writing this blog to discuss the steps to develop an AI lending platform like Upstart.

Market Potential of AI Lending Platforms

According to Research Nester, the AI lending platform market is expected to grow from USD 156.53 billion in 2026 to over USD 1.16 trillion by 2035, expanding at a 24.7% CAGR. This rapid growth is driven by lenders looking for faster and smarter ways to approve loans. Unlike traditional systems that depend heavily on credit scores and manual reviews, AI analyzes a broader range of financial data to make more accurate lending decisions. This helps financial institutions approve more eligible borrowers, reduce risk, and offer a much smoother borrowing experience.

Source: Research Nester

A prominent real-world case is Upstart, a pioneer in this space that has validated the automated model on a massive scale. By leveraging machine learning to evaluate risk based on non-traditional variables, the company surpassed 1 billion dollars in total revenue for 2025. Upstart proves that replacing rigid, static credit metrics with dynamic data is highly profitable and scalable.

Why Banks are Investing in AI Lending

Traditional financial institutions face intense pressure to protect their margins while fending off agile fintech competitors. Legacy banks carry massive operational overhead due to manual underwriting processes and outdated software architecture. By investing heavily in automated lending infrastructure, these institutions can drastically lower their cost per loan acquisition while reducing human error in risk assessment.

Furthermore, these systems allow banks to dynamically adjust interest rates and credit limits based on real-time risk profiles. Instead of building these complex machine learning pipelines from scratch, many institutional players prefer to acquire or partner with established platforms. For entrepreneurs developing this technology, the exit opportunities are lucrative, as banks are actively looking to buy proven, compliant software that protects their balance sheets.

Market Size and Future Growth Outlook

The financial services industry is rapidly adopting AI to automate lending and improve credit decisions. As more freelancers, gig workers, and small businesses look for flexible financing, lenders need smarter ways to assess risk beyond traditional credit scoring. This growing demand is creating strong opportunities for AI-powered lending platforms.

A good example is Pagaya, which uses AI to evaluate credit applications and connect lenders with institutional investors. The company reported $1.3 billion in total revenue and other income in 2025, highlighting the commercial potential of AI-driven lending. For businesses entering this market, developing an AI lending platform is more than launching a software product; it’s an opportunity to build valuable financial infrastructure that can scale with the future of digital banking.

What Is Upstart and How Does It Work?

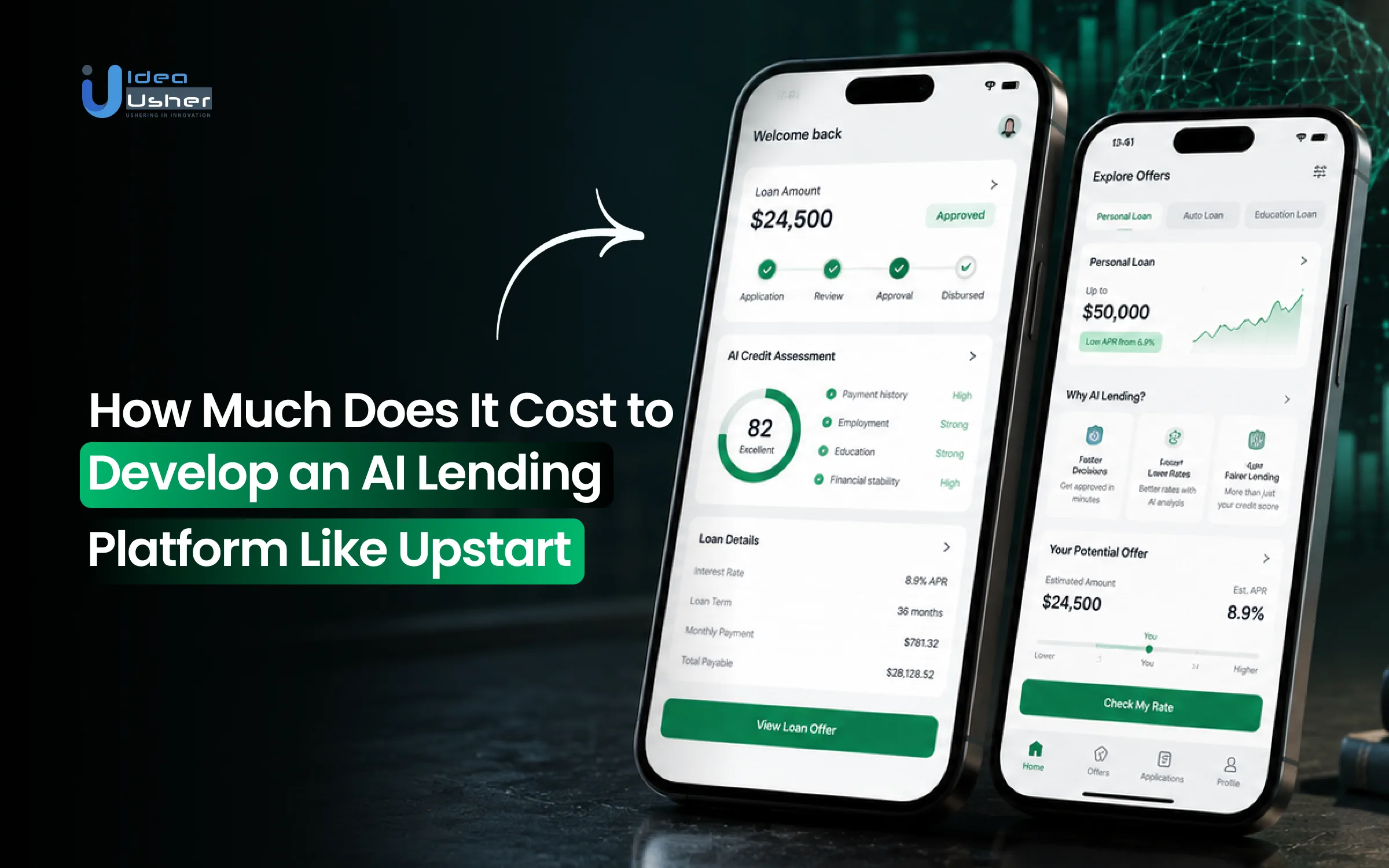

Upstart is an AI-powered lending platform that helps banks and credit unions automate loan approvals and make more accurate credit decisions. Instead of relying only on traditional credit scores, it uses AI to evaluate a wider range of borrower data, helping lenders approve more qualified applicants while reducing risk.

The platform’s success is reflected in its financial performance, generating $1.04 billion in total revenue for the full fiscal year. This shows how AI-driven lending platforms can create value for both financial institutions and borrowers by improving lending efficiency and expanding access to credit.

AI For Credit Decisions

Traditional credit underwriting relies heavily on static FICO scores and debt-to-income ratios. This approach often penalizes younger borrowers, immigrants, or gig-economy workers who possess strong earning potential but lack extensive credit histories. The core innovation of Upstart lies in expanding the underwriting data ecosystem from a handful of metrics to millions of data points.

The machine learning models evaluate complex relationships between non-standard financial variables. By predicting both default and prepayment likelihood across every month of a loan term, the algorithm builds a highly accurate risk map. This allows the platform to safely approve more applicants at a lower target loss rate than traditional banks using standard scoring methods.

The Borrower Journey

The modern financial consumer expects a friction-free digital experience similar to an e-commerce checkout. The platform delivers this speed by embedding automated verification checks directly into the front-end user experience.

- Rate Check: A user inputs basic personal and financial information to check their initial loan offers. This process relies on a soft credit check that does not lower the applicant’s credit score.

- Instant Processing: The machine learning pipeline processes the data in real time, granting fully automated approvals to over 70% of total applicants.

- Seamless Document Upload: If the system flags an anomaly requiring manual verification, the user simply uploads a photo of their paystub or bank statement through their mobile device.

- Capital Disbursal: Once the automated system clears the final fraud and identity checks, funds are transferred directly into the borrower’s account as soon as the next business day.

Institutional Adoption

For commercial banks and credit unions, building proprietary machine learning infrastructure from scratch is cost-prohibitive and presents immense regulatory compliance hurdles. Instead of trying to out-engineer tech startups, regional financial institutions license the infrastructure to optimize their existing balance sheets. Institutions deploy this software via two distinct pathways:

| Integration Model | Operational Mechanics | Core Business Value |

| Referral Network | Lenders purchase pre-vetted loans originated on the main marketplace. | Instantly scales loan volume using excess deposit liquidity. |

| Lender-Branded Software | The algorithm integrates directly into the bank’s own website and mobile apps. | Retains existing customers with a fast, modern digital interface. |

How Upstart Uses AI Instead of Traditional Credit Scores?

The massive differentiator for modern lending platforms is moving away from the static, outdated scoring models that have governed banking for decades. By replacing legacy assessment systems with multi-dimensional machine learning, the financial technology sector has fundamentally changed how risk is priced.

To turn this technology into a sustainable business, the monetization strategy relies primarily on software and marketplace transaction fees rather than taking direct credit risk on a balance sheet. The financial framework breaks down into a clear multi-tiered fee system:

- Platform Fees: Bank partners pay an upfront structural fee per loan origination to utilize the machine learning engine for underwriting and fraud detection.

- Referral Fees: A separate transactional fee is triggered when a borrower is sourced directly from the consumer-facing marketplace website.

- Servicing Fees: A recurring fee ranging from 0.5% to 1% of the outstanding loan volume is charged monthly for managing repayments and customer support throughout the lifetime of the credit asset.

Credit Score Limitations

Traditional credit scoring models like FICO rely heavily on a borrower’s past credit history, making them less effective in today’s digital economy. As a result, many financially responsible people, such as young professionals, freelancers, and recent immigrants, may struggle to qualify for loans despite having strong repayment potential. At the same time, these models can miss real-time financial changes, making it harder for lenders to accurately assess risk and leading to missed lending opportunities.

Smarter Risk Evaluation

Unlike traditional underwriting, AI lending platforms analyze thousands of data points to build a more complete picture of a borrower’s financial health. By evaluating factors such as income patterns, spending behavior, employment stability, and cash flow, AI can identify qualified borrowers more accurately and predict repayment risk with greater precision. This helps lenders make faster, more informed decisions while reducing the chances of defaults.

Key Underwriting Benefits

Transitioning to automated underwriting unlocks immediate capital efficiencies on both sides of the digital transaction marketplace. For institutional lenders, the biggest victory is a massive drop in loan loss rates without sacrificing total origination volume. Banks can confidently expand their target market into previously unserviceable segments, securely driving higher net interest margins.

Additionally, by automating roughly 90% of all credit approvals, institutions slash their manual processing overhead and eliminate human bias from the underwriting loop. For the everyday borrower, the platform offers an entirely modernized experience:

- Lower Cost of Capital: Access to highly competitive interest rates, often significantly lower than traditional options due to precise risk mapping.

- Instant Digital Fulfillment: A streamlined application journey that delivers fully automated approvals within minutes rather than days.

- Flexible Lending Limits: Personal credit opportunities ranging from 1,000 dollars up to 75,000 dollars, matching exact consumer needs without over-borrowing traps.

Ultimately, this structural optimization transforms lending from an expensive, slow chore into a highly scalable utility, turning risk management into a source of long-term competitive advantage.

Key Features of an AI Lending Platform Like Upstart

Building an AI lending platform involves much more than creating a simple loan application. To compete with platforms like Upstart, you need features that automate loan processing, improve credit decisions, and make borrowing easier for users. The right combination of AI, automation, and loan management tools creates a platform that is faster, more accurate, and built to scale.

1. AI Credit Decision Engine

Upstart uses AI and machine learning to help lenders make more accurate credit decisions by evaluating a much broader range of borrower information than traditional credit scoring models. Instead of relying mainly on FICO scores, the platform considers factors like income, employment, education, and financial behavior to better assess risk. This allows lenders to automate underwriting, approve more creditworthy applicants, and expand access to loans while maintaining responsible lending standards.

2. Automated Origination Workflow

Manual loan processing presents a massive cost bottleneck for traditional financial brands. Upstart eliminates this overhead through an end-to-end automated loan origination pipeline. Over 90% of all loans flowing through the platform are completed with zero human intervention by the company.

Borrowers use this feature by completing a streamlined digital questionnaire on their smartphones or laptops. The system instantly scans the inputs, runs automated fraud detection patterns, and renders a binding credit decision in minutes. Because the platform handles backend verification automatically, capital providers can scale up their total loan volume without hiring additional customer support staff or operations teams.

3. Digital Onboarding And Verification

Friction during onboarding is the leading cause of abandoned loan applications. Upstart minimizes this drop-off by implementing a modern web-based interface that requests data in logical, easy-to-digest stages.

- Soft Inquiry Initial Checks: Borrowers input their personal identification details to check custom rates without lowering their credit scores.

- No-Stipulation Approvals: In more than 70% of auto loan applications, Upstart approves users without requiring income verification documents like paystubs or tax forms.

- Mobile Document Uploads: When the system flags an anomaly that requires secondary verification, the user simply snaps a quick picture of their bank statement with their phone and uploads it straight into the portal.

This structured digital pathway eliminates the need for physical branch visits, keeping the completion rate high.

4. Risk-Based Pricing Infrastructure

Traditional lenders charge uniform interest rates to broad credit tiers, often overcharging low-risk borrowers while mispricing high-risk applicants. Upstart solves this by implementing highly precise, individualized pricing models based on exact default probabilities. Lenders utilize this feature to remain highly competitive across market cycles.

Bank partners set their desired return targets, and the Upstart platform automatically shifts interest rates dynamically to cover the exact risk of each borrower pool. This means creditworthy applicants get access to lower rates than legacy banks offer, while capital providers achieve predictable, highly optimized interest margins.

5. Multi-Product Asset Management

Upstart has expanded beyond personal loans by building a flexible lending platform that supports multiple financial products. Its software helps lenders manage different loan types through a single system, including auto financing used by dealerships to offer and process loans digitally. This diversified approach gives the platform greater stability, allowing it to adapt to changing market conditions while continuing to create lending opportunities across different segments.

| Product Segment | Target Audience | Core Platform Functionality |

| Personal Loans | General consumers | Handles unsecured debt consolidation up to 50,000 dollars. |

| Auto Financing | Car buyers and dealerships | Powers mobile desking tools and remote signature options on-site. |

| Home Equity (HELOC) | Suburban homeowners | Evaluates property valuation metrics for lines of credit. |

| Small-Dollar Relief | Underbanked individuals | Automates micro-loans spanning 3 to 18 months for urgent bills. |

6. Portfolio Analytics And Insights

A strong analytics dashboard is essential for any AI lending platform because it gives lenders and funding partners a clear view of loan performance. By tracking repayment trends, portfolio health, and key risk metrics in real time, the platform helps financial institutions make informed decisions and build confidence in their lending strategy.

7. Acquisition And Cross-Sell Tools

Acquiring new users through paid search ads is an expensive, recurring business drain. Upstart mitigates this by embedding automated marketing and cross-selling mechanics directly into the core platform architecture. The platform operates via a dual-track acquisition strategy:

- The Marketplace Referral Network: Upstart captures organic consumer traffic on its primary web domain, vets the applications via AI, and passes pre-approved borrowers over to regional banks looking to deploy excess deposits.

- Lender-Branded Portals: Regional credit unions place the white-labeled software directly onto their own corporate websites to modernize their digital interface.

What is the Cost to Develop an AI Lending Platform Like Upstart?

Investing in an intelligent lending marketplace requires an analytical understanding of software capital expenditure. Building a system that replaces human underwriting with machine learning involves specific engineering tiers, data integration pipelines, and stringent compliance frameworks.

When we architect these platforms at IdeaUsher, we focus on helping businesses balance upfront development costs with technical longevity. This ensures your capital builds an asset that is ready to scale securely.

Estimated Costs By Platform Tier

The capital required to launch an AI lending solution scales directly with architectural complexity and the depth of the machine learning decision models. A clear understanding of these budget boundaries allows you to plan your funding tranches strategically. Our engineering approach at IdeaUsher prioritizes structural optimization.

We often guide clients to start with a robust MVP to securely validate data models before deploying large-scale capital into enterprise features.

| Platform Tier | Technical Scope | Target Deployment | Cost Range |

| Minimum Viable Product (MVP) | Core AI scoring engine, basic KYC onboarding, single credit product. | Initial market validation and seed-stage investor presentations. | $50,000 to $120,000 |

| Mid-Scale Platform | Automated document verification, advanced risk-pricing dashboards, multi-bank system routing. | Growth-stage startups expanding loan origination volumes. | $120,000 to $250,000 |

| Enterprise Platform | Custom multi-layered neural networks, automated auto/HELOC lending, full regulatory reporting audits. | Established financial brands or heavily funded fintech institutions. | $250,000 to $500,000+ |

Primary Development Cost Drivers

Unplanned expenses in fintech engineering typically surface when infrastructure demands are miscalculated. Managing these primary cost drivers helps keep your development budget predictable:

- Data Engineering and Model Training: Machine learning algorithms require massive amounts of clean, labeled historical transaction data to train accurately. If your target niche utilizes highly unstructured alternative data, the engineering hours required to clean and format those data sets will significantly increase the initial build cost.

- Regulatory Compliance and Security: Banking regulations require strict security protocols, including real-time fraud monitoring, bank-grade encryption, and adherence to regional financial guidelines. Building these compliance filters into the backend architecture from day one prevents expensive security redesigns or legal penalties later.

- Third-Party API Integrations: Connecting your core platform to external credit bureaus, biometric identity verifiers, and open banking systems requires custom API development. The complexity of mapping data flows securely across multiple institutional endpoints directly drives up core engineering hours.

Advanced Features That Can Affect The Costs of an AI Lending Platform

When scaling a digital lending asset past basic market validation, incorporating advanced feature sets becomes necessary to remain competitive against entrenched players. These capabilities go beyond standard matching algorithms to address complex issues like fair-lending compliance, document fraud, and channel fragmentation.

When we engineer these premium capabilities at IdeaUsher, we carefully balance high-tier functionality with technical capital efficiency. This structured development approach ensures that every added line of code directly drives automation and expands your platform’s margins.

1. Explainable AI Transparency

Regulators require extreme transparency in automated lending decisions to protect against algorithmic bias. Implementing Explainable AI (XAI) ensures that whenever the machine learning engine denies an applicant, it generates an accurate mathematical audit trail explaining exactly why.

- Industry Reference: Zest AI uses proprietary explainability math to provide deep documentation for fair lending compliance.

- Development Cost Impact: Adds $25,000 to $45,000 to the baseline build.

- Engineering Reality: This cost reflects building post-hoc interpretation layers like SHAP (Shapley Additive exPlanations) or LIME (Local Interpretable Model-agnostic Explanations) over your neural networks. It also requires coding automated Adverse Action notice builders that convert data weights into clear, user-facing text.

2. Automated Document Processing

Many creditworthy borrowers lack structured bank APIs, requiring them to upload traditional paperwork like tax returns, handwritten invoices, or PDF paystubs. This feature automates the reading and validation of these files.

- Industry Reference: Ocrolus specializes in unstructured financial document extraction with high precision.

- Development Cost Impact: Adds $20,000 to $40,000 to your budget.

- Engineering Reality: The expense stems from building custom layout-parser models and pairing them with Large Language Model (LLM) prompts to categorize varied financial documents. We also build Human-in-the-Loop verification queues so that low-confidence scans are securely routed to manual reviewers without breaking the main software pipeline.

3. Omnichannel API Gateway

Borrowers rarely complete their application journeys on a single device or network. An omnichannel gateway synchronizes application states smoothly across mobile apps, desktop browsers, and physical dealer kiosks.

- Industry Reference: nCino connects diverse point-of-sale workflows into a unified cloud-based system.

- Development Cost Impact: Adds $35,000 to $65,000 to the architectural scope.

- Engineering Reality: This architecture requires building a centralized Integration Platform as a Service (iPaaS). The development hours are spent writing webhooks and low-latency state machines that synchronize real-time applicant data across point-of-sale frontends and legacy banking databases without data loss.

4. Real-Time Fraud Intelligence

Automated approval platforms are prime targets for sophisticated digital fraud, including synthetic identities and coordinated device-spoofing attacks. This security layer flags bad actors before they can access funds.

- Industry Reference: Zest AI Fraud Detection incorporates deep pattern recognition across diverse applicant metrics to stop application fraud.

- Development Cost Impact: Adds $20,000 to $35,000 to development costs.

- Engineering Reality: Our team implements this by creating behavioral telemetry trackers that monitor user interaction speed, paired with fraud API integrations like Sift or Socure. The system evaluates device fingerprints and cross-references external identity graphs instantly during the onboarding phase.

5. Dynamic Portfolio Insights

Managing risk does not end once a loan is funded. Continuous portfolio analytics allow institutional funding sources to actively track the financial health of outstanding credit assets over time.

| Analytics Focus | Data Points Tracked | Strategic Value |

| Prepayment Velocity | Early principal payoffs | Predicts shifts in total net interest margin returns. |

| Macro Volatility Filters | Local employment changes | Shifts credit limits before delinquencies spike. |

| Vintage Analysis | Delinquency rates by cohort | Isolates underperforming underwriting rules. |

- Industry Reference: Zest AI uses its automated portfolio tools to give lenders proactive data reporting on active asset risk.

- Development Cost Impact: Adds $30,000 to $55,000 to the project scope.

- Engineering Reality: This involves setting up data warehouses like Snowflake and deploying automated ETL (Extract, Transform, Load) pipelines. These pipelines clean daily loan repayment streams and feed them into interactive dashboard engines for your bank partners.

6. Predictive Offer Personalization

To maximize marketplace conversion rates, a platform cannot show generic loan packages. Predictive algorithms analyze user historical patterns to present custom loan amounts, terms, and repayment schedules that fit the applicant’s exact cash flow.

- Industry Reference: Upstart utilizes personalized data mapping to present customized personal and auto credit packages to marketplace users.

- Development Cost Impact: Adds $25,000 to $50,000 to the system architecture.

- Engineering Reality: The budget goes toward building machine learning recommendation engines, such as collaborative filtering algorithms and regression models. These models test multiple loan structures simultaneously against a borrower’s profile to display the option with the highest conversion probability.

7. Modular Multi-Product Engine

A single-product platform limits a business’s total addressable market. A modular, multi-product framework allows the marketplace to support personal loans, auto financing, and home equity lines of credit on a single infrastructure stack.

- Industry Reference: nCino Consumer Lending uses modular software blocks to process multiple consumer credit profiles from one hub.

- Development Cost Impact: Adds $45,000 to $90,000+ depending on product variety.

- Engineering Reality: This requires designing a highly modular microservices architecture. While the foundational modules for identity verification and fraud detection remain shared, our engineers build specialized validation pipelines for each specific product line, such as integrating vehicle appraisal data for auto loans or real estate valuations for HELOCs.

What Makes Upstart a Successful AI Lending Business Model?

Traditional credit scoring often leaves creditworthy people out because it relies on outdated metrics. Upstart changes this dynamic by acting as an intermediary, using artificial intelligence to connect borrowers with banks and institutional investors. Here is how its business model drives commercial success.

AI Underwriting Creates A Competitive Edge

The core of the business relies on its proprietary AI underwriting models. Instead of looking only at standard FICO credit scores, Upstart analyzes over 1600 non-traditional variables. These include employment history, area of study, and academic performance. By looking at a broader picture, the system approves more borrowers at lower interest rates without increasing risk. This automation streamlines the process, allowing more than 80% of loans on the platform to be approved instantly and with zero manual paperwork.

Marketplace Model Connects Partners

Upstart does not operate like a traditional bank. Instead of using its own money to fund loans, it runs a marketplace. This model connects consumers who need capital with over 100 bank and credit union partners who have the funds.

- Lower balance sheet risk: The company rarely holds loans on its own books, meaning it avoids the credit risk that hurts typical banks during downturns.

- Network effects: As more borrowers apply, the AI gains more repayment data to train its models. This accuracy attracts more bank partners, which brings more capital to the platform.

Multiple Revenue Streams Drive Growth

This marketplace relies on several fee-based revenue streams rather than collecting interest on outstanding loans. This structure protects the business from rate fluctuations and generates steady cash flow. The company also charges borrowers a one-time origination fee of up to 12% of the total loan amount, which is deducted before the cash is sent out. Late payments incur a fee of 5% of the overdue balance or $15, depending on which amount is higher.

These fees make up the vast majority of the company’s financial performance.

| Metric | Financial Result |

| Annual Total Revenue | $1.0 billion |

| Revenue from Fees | $950 million |

| Annual Origination Volume | Roughly $11.0 billion across 1.5 million loans |

| Net Income | $53.6 million |

This fee-heavy system makes the platform highly scalable. By focusing on software and platform matching instead of loan holding, Upstart remains agile while expanding its reach into auto and home lending markets.

Build an AI Lending Platform with Idea Usher

Building a competitive financial technology asset requires a deliberate mix of secure code, responsive design, and compliant data practices. If you want to scale beyond basic legacy systems, choosing a development team with deep engineering experience is the most important decision you will make.

With over 500,000 hours of coding experience, our team of ex-MAANG/FAANG developers at Idea Usher brings elite technical knowledge to your fintech project. We know how to construct high-performance backend systems, scale data-heavy pipelines, and keep transaction logic operating safely at volume.

Tailored Underwriting Models

Every lender targets a different risk profile and audience. Instead of using generic tools, we build custom machine learning models designed around your specific credit criteria. By utilizing variables like employment tenure, cash flow consistency, and educational backgrounds, our algorithms construct multi-dimensional risk profiles. This approach allows your platform to approve thin-file borrowers safely. The system maps out highly accurate default and prepayment timelines, helping you expand credit limits securely.

Secure Banking Integrations

Fintech security is non-negotiable. Connecting modern applications to traditional banking networks requires secure, seamless data routing. We integrate automated Know Your Customer and Anti-Money Laundering checks directly into your onboarding flow. By utilizing secure bank aggregation tools, borrowers can link their accounts instantly. This setup automates cash flow verification while blocking fraudulent applications before they can proceed.

Scalable Platform Support

Lending engines must run flawlessly during high-volume spikes. We build your platform using a highly modular microservices architecture, ensuring each feature can scale independently.

- Optimized database setups: Keep transaction speeds fast as your user count grows.

- Continuous drift monitoring: Tracks model performance over time to catch any changes in underwriting accuracy.

- Proactive maintenance support: Updates secure payment APIs and handles operating system upgrades smoothly.

This clean architecture keeps your technical infrastructure healthy. Our engineering support allows your team to focus entirely on borrower acquisition and portfolio growth.

Conclusion

Building an AI lending platform like Upstart is about creating a smarter way to evaluate borrowers and deliver faster loan decisions. The overall cost depends on the features you need, the complexity of the AI, and the systems you want to integrate. If you’re planning to enter the AI lending market, it’s worth focusing on a platform that can scale with your business from day one. Working with an experienced development partner can help you launch faster and avoid costly rebuilds as your platform grows.

Things to Know About AI Lending Platforms

A1: Traditional lending often depends on credit scores and manual underwriting, which can overlook borrowers with limited credit history. AI lending takes a broader approach by evaluating factors such as income stability, employment history, spending patterns, and other financial signals. This allows lenders to approve more qualified applicants, improve risk assessment, and deliver loan decisions much faster.

A2: The cost varies based on the scope of the platform and the level of AI functionality you want to include. A basic MVP with digital loan applications and automated underwriting costs much less than an enterprise solution with explainable AI, fraud detection, portfolio analytics, and multiple banking integrations. Compliance requirements, cloud infrastructure, and third-party APIs also play a major role in the overall budget.

A3: Modern AI lending platforms combine several technologies to automate credit decisions and improve accuracy. Common technologies include machine learning for risk scoring, OCR for extracting information from financial documents, natural language processing for document understanding, predictive analytics for default forecasting, and AI models for fraud detection and identity verification. Together, these technologies help lenders process applications more efficiently while reducing operational costs.

A4: Yes. Enterprise AI lending platforms are designed to integrate with core banking systems, credit bureaus, open banking providers, payment gateways, KYC and AML services, identity verification platforms, and digital signature solutions. These integrations create a seamless lending workflow and reduce the need for manual data entry.