The availability of fast and convenient access to money is essential. Unforeseen expenses such as medical emergencies, unexpected bills, or home repairs can disrupt an individual’s monthly budget. During such difficult times, personal loan apps like OneMain Financial can provide a comforting and user-friendly solution, offering much-needed financial relief.

The personal loan app market is not just growing, it’s booming. With a projected annual growth rate of 25.4% from 2022 to 2030, it’s clear that more and more people are turning to personal loan apps for their financial needs. This rapid growth presents exciting opportunities for entrepreneurs and developers in the fintech industry, igniting a sense of excitement about the potential in this market.

Given all these considerations, it’s clear that loan apps are gaining significant traction in the US market.

Therefore, in this blog, we will discuss all the necessary steps to develop a personal loan app similar to OneMain Financial, from conceptualization to design, development (including the use of specific programming languages and frameworks), testing, and launch!

What is the OneMain Financial App?

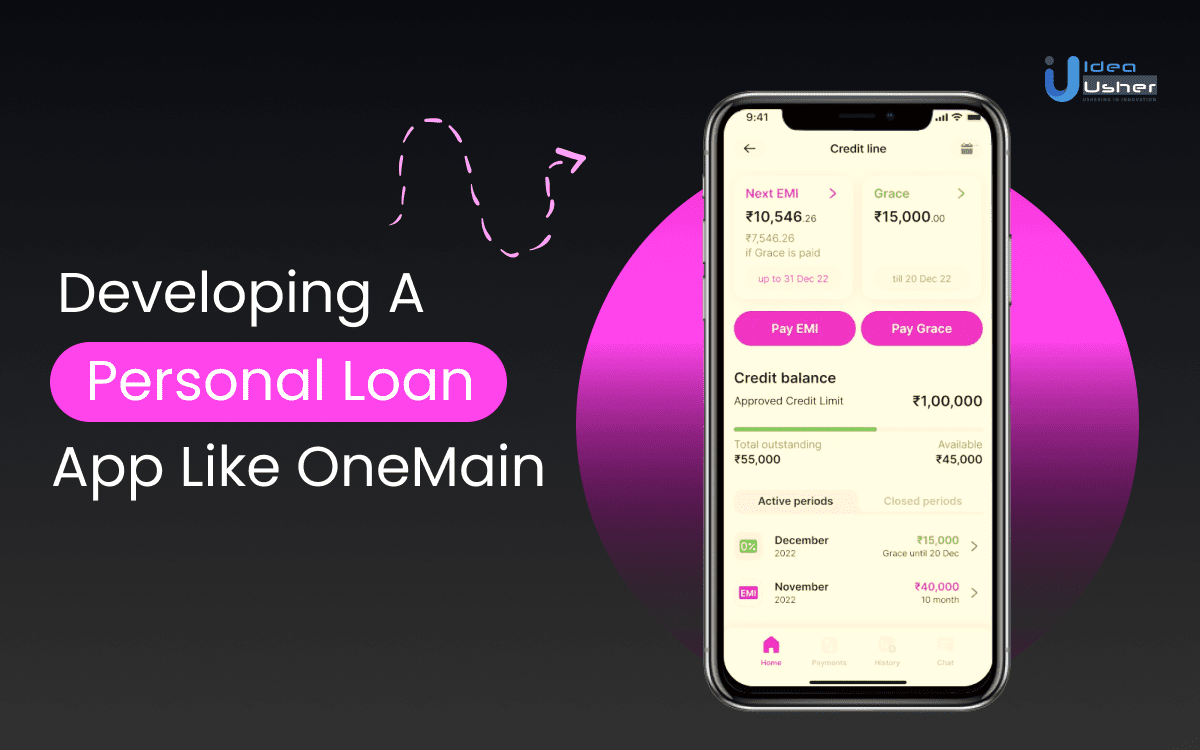

The OneMain Financial, a personal loan app, launched in 2016, offers convenient management of personal loans. With over 1 million downloads and a solid 4.5-star rating on the Google Play Store, the app has become a trusted tool for many borrowers. Users can easily view account details, make payments, set up autopay, and check loan balances. Push notifications provide timely reminders for payments and account updates. Additionally, the app allows users to explore prequalified offers for refinancing or additional borrowing, simplifying the process for those seeking financial flexibility.

What Makes the OneMain Financial App Unique?

The rapid adoption of mobile app technology and the growing demand for accessibility to financial services have fueled the growth of fintech apps like OneMain Financial. By offering a digital platform for loan management, these apps cater to the preferences of tech-savvy consumers who prioritize convenience and efficiency.

- “Loan Summary”: Provides users with a clear overview of their financial obligations, empowering them to make informed decisions.

- “Make a Payment”: Simplifies the payment process, reducing friction and increasing customer satisfaction.

- “Autopay”: Eliminates the risk of missed payments, building trust and loyalty among customers.

- “PreQualified Offers”: Enables cross-selling opportunities and increases revenue by offering tailored financial products.

- “Push Notifications”: Improves customer engagement by providing timely reminders and updates.

By incorporating these features, fintech companies like OneMain Financial can enhance customer experience, reduce operational costs, and generate additional revenue streams through cross-selling and upselling. The app’s ability to provide a seamless and personalized user experience fosters customer loyalty and advocacy, ultimately driving business growth.

Key Market Takeaways for Personal Loan Apps

Source: MarketResearchFuture

Consumers are increasingly drawn to personal loans as a flexible and accessible financing option. The appeal of personal loans stems from their versatility and potential financial benefits. Unlike secured loans, personal loans typically do not require collateral, making them more accessible to a wider range of borrowers.

The collaboration between fintech firms and traditional financial institutions has also significantly boosted the expansion of the personal loan market. These collaborations allow for the integration of innovative technologies into established lending platforms, resulting in improved customer experiences and expanded reach. For instance, the partnership between LendingClub and Wells Fargo has led to the development of joint personal loan products that combine the speed and convenience of digital lending with the trust and security associated with traditional banks.

Moreover, the increasing popularity of smartphones and mobile apps has revolutionized the way consumers engage with financial services. Personal loan apps provide convenience, speed, and a tailored borrowing experience. For example, the SoFi app allows users to apply for loans, track payments, and access financial tools all in one place.

What Features Make the OneMain Financial App So Popular Among Its Users?

OneMain Financial’s app has garnered significant user adoption due to several key features that address the needs of its target audience.

1. User-Friendly Loan Management

The app’s “Loan Summary” and “Payment Schedule” features enable users to effortlessly track loan balances, due dates, and payment history. This simplicity empowers users to maintain control over their financial obligations.

2. Secure and Convenient Mobile Payments

OneMain Financial’s app prioritizes security while offering convenient mobile payment options through its “Quick Pay” feature. Users can securely make payments directly from their bank accounts, eliminating the hassle of traditional payment methods.

3. Real-Time Account Updates

The app’s “Account Overview” feature provides users with real-time updates on account balances, payment confirmations, and any changes to loan terms. This transparency fosters trust and keeps users informed about their financial situation.

4. Personalized Financial Tools

OneMain Financial offers personalized financial tools within the app, such as the “Budget Planner” and “Debt Management Calculator,” to meet diverse financial needs.These attributes enable individuals to make well-informed choices about their finances.

5. Exceptional Customer Support Integration

The app seamlessly integrates with OneMain Financial’s customer support channels through the “Help & Support” feature. Users can access live chat, contact information, and frequently asked questions directly within the app, ensuring timely assistance when needed.

Innovative Features That Can Enhance a Personal Loan App like OneMain Financial

In order to remain competitive and effectively cater to changing consumer demands, personal loan apps like OneMain Financial need to integrate cutting-edge features.

1. AI-Powered Loan Compare Models

Leverage AI algorithms to develop sophisticated loan comparison models that analyze a user’s financial profile, loan needs, and market trends in real time. This allows the app to offer personalized suggestions, highlighting the best loan options from different lenders.

2. Cryptocurrency-Backed Loans

Tech-savvy borrowers should consider offering loans secured by cryptocurrency holdings. This opportunity allows the company to enter a new market and broaden its range of products and services.

3. Real-Time Financial Coaching Chatbots

Implement advanced chatbots capable of providing real-time financial advice, answering questions, and assisting with loan applications. This enhances customer support and accessibility.

4. Loan-Based Rewards Programs

Offer loyalty programs where borrowers can earn points or rewards for on-time payments, referrals, or other actions. This can incentivize responsible borrowing and increase customer engagement.

5. Financial Literacy Curriculum

Develop comprehensive financial literacy courses that are accessible through the app. This can help users improve their financial knowledge and make informed decisions.

6. Marketplace for Financial Products

Expand the app to include a marketplace for other financial products, such as insurance, investments, or credit cards. This creates additional revenue streams and enhances the app’s value proposition.

7. Loan Consolidation and Refinancing Tools

Offer tools to help users consolidate multiple debts into a single loan or refinance existing loans for better terms. This can simplify financial management and potentially save borrowers money.

Development Steps For a Personal Loan App like OneMain Financial

Developing a personal loan app like OneMain Financial requires a strategic approach that can include market research, robust underwriting models, and seamless branch network integration.

1. Market Research and Competitive Analysis

The initial phase of creating a personal loan app involves undertaking comprehensive market research. Identifying target customer segments and understanding their specific needs is crucial. Analyzing competitor offerings helps to identify gaps in the market and potential differentiators, providing a foundation for a unique and competitive product.

2. Underwriting Model Development

Creating a robust underwriting model is essential. This model should consider various factors beyond traditional credit scores, such as income verification, employment stability, and debt-to-income ratio. Incorporating alternative data sources enhances the accuracy of borrower risk assessments, leading to better loan decisions and reduced default rates.

3. Branch Network Integration

Seamless integration between the app and physical branch locations enhances customer support and loan disbursement. Ensuring data synchronization between digital and physical channels provides a consistent user experience. This integration allows customers to receive support and complete transactions both online and in person.

4. Customer Segmentation and Product Customization

Identifying distinct customer segments based on demographics, financial behavior, and creditworthiness enables tailored loan products and interest rates. Customizing products to meet the unique requirements of each segment enhances customer satisfaction and engagement, leading to higher retention rates.

5. Compliance and Regulatory Adherence

Developing a comprehensive compliance framework is crucial for meeting federal, state, and local regulations for consumer lending. Implementing robust anti-money laundering (AML) and KYC procedures ensures legal compliance and reduces the risk of fraudulent activities. This adherence to regulations builds trust and credibility with customers and regulatory bodies.

6. Partnerships with Dealers and Retailers

Establishing partnerships with auto dealers and retailers offers point-of-sale financing options. Integrating loan application processes into dealer management systems streamlines the application process for customers. These partnerships expand the app’s reach and provide additional revenue streams.

7. Customer Relationship Management System

Implementing a CRM system is vital for managing customer interactions, tracking loan performance, and identifying cross-selling opportunities. Utilizing data analytics to personalize customer communications enhances engagement and satisfaction. A robust CRM system supports targeted marketing efforts and improves overall customer service.

8. Debt Collection and Recovery Strategies

Developing effective debt collection processes is essential for minimizing charge-offs and maximizing recovery rates. Implementing both in-house collections and partnerships with collection agencies ensures a comprehensive approach to debt recovery. Effective strategies reduce financial losses and maintain a healthy loan portfolio.

Cost of Developing a Personal Loan App like OneMain Financial

ere’s the adjusted cost breakdown for developing a money lending app like Avant, with a total cost range of $10,000 – $100,000:

| Stage | Description | Cost Range |

| Research and Planning | Market Analysis, Feature Identification, Business Model Development, Legal and Compliance | $1,000 – $5,000 |

| Design | UI/UX Design, Wireframing and Prototyping | $5,000 – $15,000 |

| Front-End Development | User Interface, User Experience, Platform Compatibility (iOS and Android) | $10,000 – $30,000 |

| Back-End Development | Loan Application and Processing, Credit Score Integration, Payment Processing, Data Management | $15,000 – $40,000 |

| App Features | User Registration and Login, Loan Eligibility Calculator, Loan Application Form, Document Upload, Push Notifications, In-App Chat Support, Loan Repayment Options, Financial Dashboard | Varies (See below) |

| – User Registration and Login | $2,000 – $5,000 | |

| – Loan Eligibility Calculator | $3,000 – $8,000 | |

| – Loan Application Form | $4,000 – $12,000 | |

| – Document Upload | $1,000 – $3,000 | |

| – Push Notifications | $1,000 – $2,500 | |

| – In-App Chat Support | $2,000 – $5,000 | |

| – Loan Repayment Options | $4,000 – $12,000 | |

| – Financial Dashboard | $4,000 – $12,000 | |

| Testing | Functional Testing, Performance Testing, Security Testing, User Acceptance Testing | $5,000 – $10,000 |

Total Cost Range: $10,000 – $100,000

The cost of building a personal loan app, similar to OneMain Financial, is subject to numerous variables. While some factors are common across software development projects, others are specific to the financial services industry.

Loan Calculation and Repayment Scheduling

Determining accurate interest rates and fees and constructing detailed repayment plans necessitates specialized financial expertise. This often involves complex calculations and algorithms.

Credit Risk Assessment

Implementing robust models to evaluate borrower creditworthiness and determine loan eligibility requires advanced data analysis and statistical modeling. These processes contribute significantly to development time and costs.

Customer Support and Collections

Providing comprehensive customer support, including handling loan inquiries, payment issues, and collections, demands additional resources such as customer service personnel, technology infrastructure, and training.

Compliance Auditing and Reporting

Regularly auditing systems and generating reports to adhere to financial regulations incurs ongoing costs for personnel, software, and processes.

Essential Tech Stacks to Develop Personal Loan Apps like OneMain Financial

Developing a personal loan app like OneMain Financial requires a comprehensive tech stack. Let’s explore them in detail,

1. Front-End Development

Creating a user-friendly interface is crucial for a personal loan app. The design must ensure a seamless user experience, allowing users to navigate the app effortlessly. Responsive design is essential to optimize viewing across different devices, ensuring accessibility and functionality on smartphones, tablets, and desktops. Integration with payment gateways and biometric authentication enhances security and simplifies the user experience.

2. Back-End Development

Robust API development is necessary to facilitate communication between the front-end and back-end systems. This ensures smooth data flow and efficient processing of user requests. Integration with financial institutions and data providers allows for real-time account verification and fund transfers. Effective database management is essential for securely storing user data, loan information, and financial transactions.

3. Robust Risk Assessment Engine

A robust risk assessment engine is vital for evaluating borrower creditworthiness. Advanced statistical modeling and machine learning algorithms are used for credit scoring. Integrating alternative data sources provides a comprehensive risk assessment, enhancing the accuracy of credit evaluations. Real-time risk evaluation capabilities enable dynamic pricing and underwriting, adapting to market trends and individual borrower profiles.

4. Secure Data Management and Encryption

Ensuring secure data management is critical. End-to-end encryption protects sensitive customer data, such as social security numbers and financial information. Secure data storage and transmission protocols, including HTTPS and TLS, safeguard data integrity. Compliance with data privacy regulations like GDPR and CCPA builds user trust and ensures legal adherence.

5. Integration with Financial Institutions

Seamless integration with financial institutions is essential for efficient operations. APIs facilitate real-time data exchange with banks, credit bureaus, and payment processors. Secure authentication mechanisms ensure the safe sharing of sensitive information. This integration supports accurate account verification and prompt fund transfers, enhancing user trust and app reliability.

6. Scalable Cloud Infrastructure

A cloud-based architecture is necessary to handle fluctuating workloads and user traffic. Auto-scaling capabilities accommodate growth and seasonal variations, ensuring consistent performance. High availability and disaster recovery plans are essential to maintain uninterrupted service, ensuring users can access the app reliably at all times.

7. Fraud Detection and Prevention Systems

Implementing advanced fraud detection systems is crucial for maintaining security. Machine learning models and sophisticated algorithms detect fraudulent activities. Real-time monitoring of user behavior and transaction patterns helps identify potential threats. Integration with fraud prevention services, including chargeback management, ensures comprehensive protection against fraud.

8. Customer Relationship Management Platform

A robust CRM system manages customer interactions, tracks loan performance, and identifies cross-selling opportunities. Integration with marketing automation tools enables personalized campaigns, enhancing user engagement. Data analytics capabilities support customer segmentation and behavior analysis, providing insights for targeted marketing and improved customer service.

How Does a Personal Loan App like OneMain Financial Generate Revenue?

Personal loan apps like OneMain Financial primarily generate revenue through a combination of interest charges and fees.

1. Loan Amounts and Fees

OneMain Financial, a prominent company in the personal loan business, offers loan amounts ranging from $1,500 to $20,000. These loans can be either personal or auto loans, depending on the applicant’s qualifications and collateral availability. Larger loan amounts might need a first lien on a motor vehicle that meets specific value and age requirements, and the vehicle must be titled in the applicant’s name with valid insurance. Loan approval and terms depend on the borrower’s credit history, income, and state of residence. Notably, APRs are typically higher for unsecured loans compared to those secured by a vehicle.

2. Loan Origination Fees

OneMain Financial generates a significant portion of its revenue through loan origination fees. These fees are either a flat amount or a percentage of the loan amount, varying by state. Flat fees can range from $25 to $500, while percentage-based fees can range from 1% to 10% of the loan amount, subject to state-imposed limits. These fees are usually disclosed in the Loan Agreement and Disclosure Statement under “Prepaid Finance Charges,” and they may be labeled differently in each state, such as Loan Processing Fee, Document Preparation Fee, or Credit Investigation Fee.

3. Late Payment Fees

Late payment fees are another revenue stream for OneMain Financial. When borrowers fail to make payments on time, OneMain charges late fees, which vary by state. These fees can be around $5 to $30 per late payment or a percentage of the monthly payment amount, typically between 1.5% and 15%, depending on state regulations. The late fees are disclosed in the Loan Agreement and Disclosure Statement under “Truth in Lending Disclosures” in the row titled “Late Charge.”

4. Non-Sufficient Funds Fees

OneMain Financial charges non-sufficient funds fees when payment by check or electronic ACH debit is returned due to insufficient funds. These fees vary by state, ranging from $10 to $50 per returned payment. This fee structure allows the business to mitigate the risk associated with payment defaults and maintain its revenue flow.

Note: OneMain Financial also adheres to state-specific loan limits. For instance, in Alabama, the minimum loan size is $2,100, while in California, it is $3,000. Maximum loan sizes also vary, with North Carolina capping unsecured loans at $11,000 and Maine at $7,000. These limits ensure that the business operates within the legal frameworks of different states, providing a tailored approach to loan offerings based on regional regulations.

Innovative Technologies That Can Enhance a Personal Loan App like OneMain Financial

To enhance a personal loan application like OneMain Financial, integrating unique and innovative technologies can significantly improve user experience and operational efficiency.

1. Voice Recognition Technology

Voice recognition technology can simplify the loan application process by allowing users to interact with the app through voice commands. This technology can enhance accessibility for users who may have difficulty navigating traditional interfaces. By enabling voice-activated features, companies can offer a more user-friendly experience.

For instance, the integration of voice recognition in personal loan apps can allow users to complete tasks such as checking loan status, making payments, or asking questions about loan terms just by speaking. A notable example is the financial app Cleo, which uses AI and voice recognition to help users manage their finances through conversational interactions. This approach not only streamlines the process but also creates a more engaging experience for users.

2. Peer-to-Peer Lending Integration

P2P lending platforms can provide an alternative funding source for personal loans, connecting borrowers directly with individual lenders. This model has the potential to lower costs for borrowers and provide investors with attractive returns.

A successful example is Upstart, which connects borrowers with lenders using an AI-driven platform to assess creditworthiness. Upstart’s model allows individuals with limited credit history to access loans, demonstrating how P2P lending can democratize access to credit. By incorporating P2P lending into their platforms, companies like OneMain Financial can diversify their funding sources and potentially lower interest rates for borrowers.

3. Gamification for Financial Engagement

By integrating gamification into personal loan apps, companies can encourage users to improve their financial literacy and manage their loans more effectively.

For example, CASHe, a fintech startup, has successfully utilized gamification to engage young professionals. The app offers rewards for completing financial education modules and achieving savings goals, which not only helps users learn but also fosters a sense of accomplishment. This approach can lead to better financial habits among users, ultimately resulting in lower default rates for the lending company.

Conclusion

Apps like OneMain Financial have changed the way people borrow money. They make it easy and fast to get a loan, and you can do it all from your phone. This is really helpful for people who don’t have good credit or who live in areas where it’s hard to get financial help. For companies in the finance and technology industry, creating a similar app is a big chance to make money and grow their business. Using technology and data, they can make the loan process faster, save money, and offer different kinds of loans to fit what people need. They can also learn a lot about their customers to improve their products and services. But to do this well, they need to understand how people use money, manage risks, and make sure they are lending money in a responsible way.

Looking to Develop a Personal Loan App like OneMain Financial?

Idea Usher can engineer your vision of a robust personal loan app similar to OneMain Financial. Leveraging our 500,000+ hours of coding expertise, we’ll architect a secure, scalable platform incorporating advanced features like AI-driven credit underwriting, blockchain for transparent transactions, and real-time fraud detection, ensuring your app delivers speed, accuracy, and trust, propelling your fintech venture to new heights.

FAQs

Q1: How to make a personal loan app?

A1: To create a personal loan app, start by conducting thorough market research to identify target users and competitors. Develop a comprehensive business plan outlining the app’s features, target market, and revenue model. Assemble a skilled development team to design and build the app, incorporating robust security measures and complying with relevant financial regulations. Integrate features such as loan application, approval, disbursement, and repayment. Implement effective marketing strategies to acquire users and build a strong brand identity. Continuously monitor user feedback and iterate on the app to enhance user experience and drive growth.

Q2: How long does it take to create a mobile loan app?

A2: The time required to create a mobile loan app varies depending on its complexity and desired features. A basic app with core functionalities might take several months to develop, while a sophisticated platform with advanced features and integrations could take a year or more. Factors such as team size, development methodology, and regulatory compliance also influence the development timeline.

Q3: How much does it cost to develop a loan lending app?

A3: The expense to develop a loan lending app varies significantly based on several factors. These include the app’s complexity, desired features, technology stack, team size, and location. A basic app with limited functionalities might require a lower investment compared to a sophisticated platform with advanced features. Additionally, ongoing maintenance and updates should be factored into the overall cost.

Q4: What are the features of an Ioan lending platform?

A4: Loan lending platforms typically offer features such as user registration and profile creation, loan application and approval processes, integration with credit bureaus, secure payment gateways, loan management tools, customer support channels, and analytics dashboards. Advanced platforms may incorporate AI-powered underwriting, fraud detection systems, and personalized loan recommendations.