(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Dealing with unforeseen expenses such as medical bills or educational costs or the necessity to consolidate debt, the traditional loan process can feel overwhelming. However, the rise of money-lending apps like Avant has offered a quick and convenient solution to this problem. These apps provide rapid access to funds and have become a dependable and efficient resource for many individuals, instilling a sense of reassurance and confidence in their financial management.

The market size of money lending apps was valued at USD 3.36 billion in 2019 and can easily reach a valuation of USD 8.79 billion by 2031, growing from USD 3.7 billion in 2023. This shows that the market for money-lending apps is growing quickly because more and more people are using these apps. They provide fast access to money for emergencies or unexpected expenses. Also, for people who don’t have easy access to regular banks, these apps provide financial inclusion.

Because of these factors, it is evident that money-lending apps are gaining significant popularity in the US market. Therefore, in this blog, we aim to provide comprehensive information on developing a money-lending app similar to Avant.

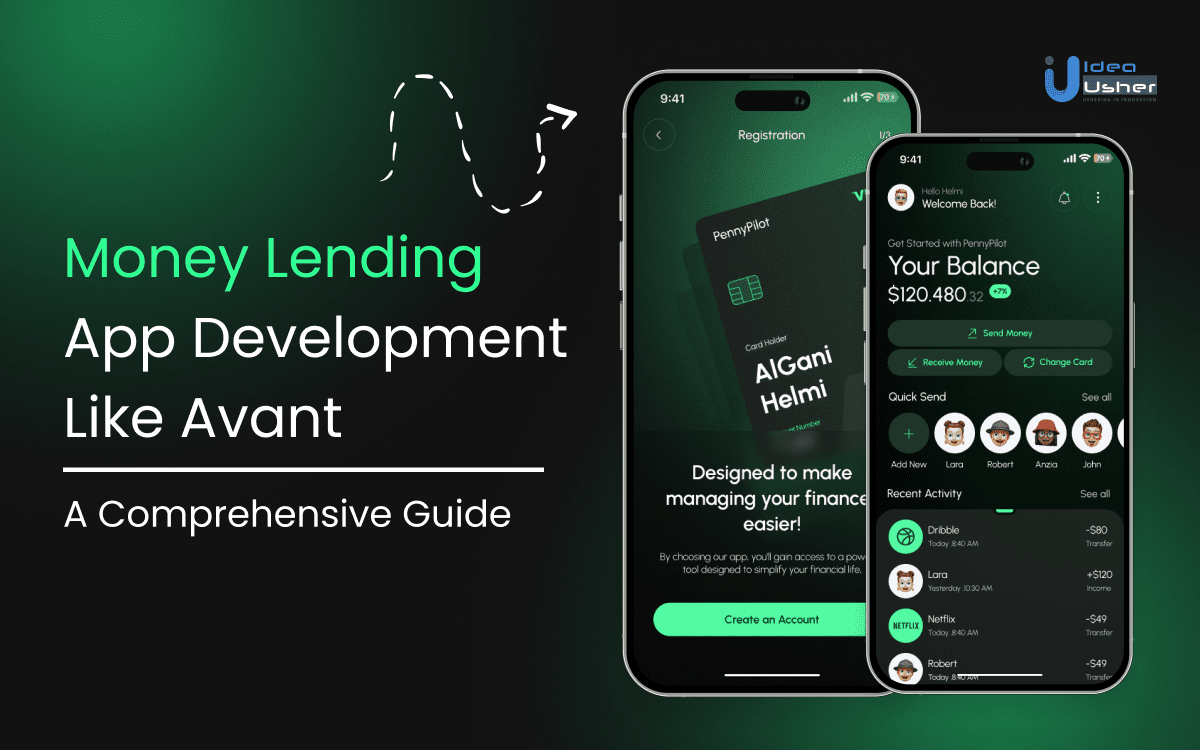

What is the Avant App?

The Avant money lending app is designed to simplify loan and credit card management, offering a user-friendly interface. With over 500K downloads and a 4.4-star rating on the Google Play Store, the app has become a popular tool for Avant customers. Users can easily view account balances, payment due dates, and transaction history. Features like secure payments, autopay enrollment, and push notifications ensure that managing financial obligations is not only convenient but also comfortable and easy to navigate.

What Makes the Avant App Unique?

The Avant app has capitalized on the growing trend of consumers seeking financial management tools that offer flexibility and transparency. By providing users with granular control over their accounts, Avant has positioned itself as a customer-centric fintech company.

The Avant app Empowers users to manage their cash flow effectively, reducing financial stress and instilling a sense of control.

- Features like ‘Schedule a Payment’ and ‘Cancel Payment’ put users in the driver’s seat, allowing them to make decisions that best effectively suit their financial situation.

- “Account Balance” and “Transaction History” provides essential financial information at users’ fingertips, facilitating informed decision-making.

- “Push Notifications” enhances the overall user experience by offering timely alerts and reminders.

Avant’s app offers a host of user-friendly features and an intuitive interface, all of which contribute to higher user satisfaction and loyalty. Through delivering a seamless and captivating digital experience, Avant has successfully expanded its customer base. Furthermore, the app’s data collection capabilities provide Avant with valuable insights into customer behavior and preferences. This data-driven strategy enables the company to fine-tune its product offerings, customize marketing initiatives, and identify potential new revenue streams.

Why do People Use the Avant App?

The Avant app has resonated with users due to its focus on control, transparency, and convenience. Key features contributing to its popularity include:

- Flexibility: Users appreciate the ability to manage their finances on their own terms, thanks to features like “Schedule a Payment” and “Cancel Payment.”

- Transparency: Real-time access to “Account Balance” and “Transaction History” empowers users to make informed financial decisions.

- Convenience: The intuitive interface and timely push notifications improve the overall user experience, making financial management effortless.

- Control: Users feel in charge of their finances and have the ability to proactively manage payments and track spending.

As the fintech industry continues to evolve, apps like Avant are at the forefront of innovation, shaping the future of financial services.

Key Market Takeaways for Money Lending Apps

Source: Strategic Market Research

This rapid expansion is driven by the numerous benefits offered by digital platforms to both lenders and borrowers. For lenders, automation, data-driven insights, and cost reductions are key advantages. For instance, Auxmoney, a prominent digital lending platform, secured a significant investment of USD 271.4 million in April 2021 to enhance its platform and expand its reach.

On the borrower side, digital lending platforms offer unparalleled convenience, speed, and personalization. By eliminating the traditional brick-and-mortar infrastructure, these platforms have made credit more accessible to a broader customer base. Moreover, the ability to tailor loan products to individual needs has fostered a new level of customer satisfaction and loyalty.

What Features Make the Avant App So Popular Among Its Users?

Avant’s app has garnered significant traction among users due to several key features that align with contemporary consumer needs.

1. Seamless Loan Application and Approval Process

The app’s streamlined interface and intuitive design expedite the loan application process. Users can quickly input the required information, receive real-time updates on application status, and often secure loan approval within minutes. This efficiency resonates with today’s fast-paced digital lifestyle.

2. Personalized Financial Insights

Avant’s app goes beyond basic loan management by offering personalized financial insights. Through data analysis, the app can provide users with tailored recommendations on budgeting, debt management, and credit improvement. Users are empowered to make informed financial decisions through this proactive approach.

3. Flexible Payment Options

Recognizing the diverse financial circumstances of its users, Avant offers flexible payment options through its app. Features like early payment, partial payment, and payment deferral provide users with control over their loan repayment schedule, enhancing financial flexibility.

4. Secure and Convenient Mobile Payments

The app’s integration of secure mobile payment options simplifies the loan repayment process. Users can easily make payments directly from their bank accounts or linked payment methods, eliminating the need for manual checks or online transfers.

5. Exceptional Customer Support

Avant’s commitment to customer satisfaction is evident in its robust in-app customer support features. Users can access a knowledge base, FAQ, and live chat support directly through the app. This accessibility ensures timely assistance and efficiently resolves user inquiries.

Innovative Features That Can Enhance a Money-Lending App Like Avant

To maintain a competitive edge, money-lending apps like Avant can benefit from incorporating highly innovative features that address evolving consumer needs and expectations.

1. AI-Powered Financial Wellness Coaching

Beyond basic financial advice, integrate an AI-powered coach capable of providing personalized, real-time financial wellness guidance. This coach could offer tailored recommendations based on individual spending habits, income, and goals, helping users achieve long-term financial stability.

2. Instant, Biometrically Secured Transactions

Leverage advanced biometric authentication (fingerprint, facial recognition, or voice) for lightning-fast, secure loan approvals and disbursements. This enhances user experience and significantly reduces fraud risks.

3. Predictive Financial Modeling

Employ advanced predictive analytics to develop personalized financial models for users. These models can predict future financial situations, assisting borrowers in making informed decisions about loan amounts, repayment terms, and potential financial consequences.

4. Blockchain-Secured Loan Contracts

Utilize blockchain technology to create immutable and transparent loan contracts. This enhances trust, security, and efficiency in the lending process while also providing borrowers with verifiable proof of their financial obligations.

5. Micro-Loan Options with Instant Payback

Offer small, short-term loans that can be repaid instantly through various digital channels (e.g., mobile payments, cryptocurrency). This caters to the growing demand for quick access to small amounts of cash and can be coupled with gamification elements to encourage responsible borrowing.

6. Rent-to-Own and Lease-to-Own Options

Expand the product offering to include rent-to-own and lease-to-own programs for high-ticket items. This can appeal to consumers who prefer alternative payment methods and can generate additional revenue streams for the lender.

How to Develop a Money Lending App like Avant?

Developing a money-lending app like Avant requires meticulous planning, sophisticated technology, and strategic partnerships. Let’s explore the crucial steps involved,

1. Market Research and User Persona Development

Developing a money lending app begins with thorough market research. This research aims to identify target demographics, analyze competitors, and understand industry trends. Creating detailed user personas helps in comprehending customer needs, pain points, and preferences, which are crucial for building a user-centric app.

2. Core Features and Functionality

Defining core features is essential. These features include loan application processes, eligibility checks, document upload capabilities, and secure payment options. Integration with credit bureaus and financial institutions ensures a seamless experience for users and enhances the app’s reliability and credibility.

3. Risk Assessment Model Development

Creating a sophisticated risk assessment model is vital. This model evaluates borrower creditworthiness accurately and efficiently. Incorporating alternative data sources beyond traditional credit scores can improve risk prediction, ensuring better decision-making in the lending process.

4. Pricing and Yield Curve Optimization

Establishing a dynamic pricing model requires considering factors like creditworthiness, loan amount, and term. Optimizing the yield curve helps in balancing risk and return while maintaining competitive interest rates. This approach ensures that the lending app remains attractive to both borrowers and investors.

5. Loan Origination and Underwriting Automation

Automating the loan origination process using AI and machine learning streamlines document verification and decision-making. Developing advanced underwriting algorithms allows for quick and accurate assessment of borrower eligibility, enhancing efficiency and user satisfaction.

6. Investor Relations and Funding Sources

Building relationships with investors and institutional lenders is crucial for securing funding for loan origination. Developing strategies for securitization and portfolio management ensures sustainable growth and stability. Effective communication and transparency with investors foster trust and long-term partnerships.

7. Collections and Recovery Strategies

Implementing efficient collection processes is essential. These processes include automated reminders, payment plans, and debt recovery strategies. Partnering with collection agencies can assist in recovering delinquent debts, ensuring minimal financial loss, and maintaining a healthy loan portfolio.

8. Partnerships with Financial Institutions

Collaborating with banks, credit unions, and other financial institutions aids in customer acquisition and loan servicing. Exploring partnerships for co-branded products or referral programs can enhance the app’s market presence and credibility, driving growth and customer trust.

Cost of Developing a Money Lending App like Avant

| Stage | Cost Range | Includes |

| Market Research and Planning | $1,000 – $5,000 | Competitor analysis, target market identification, feature definition, business model development, legal and compliance considerations. |

| Design and UI/UX | $2,000 – $10,000 | Wireframing, prototyping, user interface design, user experience design, visual design, branding. |

| App Development | $5,000 – $60,000 | Front-end development, back-end development, API integration, core features (user registration, loan application, disbursement, repayment, customer support, push notifications, security). |

| Testing and Quality Assurance | $1,000 – $10,000 | Functional testing, performance testing, security testing, usability testing, bug fixing. |

| Deployment and Launch | $1,000 – $10,000 | App store submission, marketing, user acquisition. |

Total Cost Range: $10,000 – $100,000

While several factors contribute to the overall cost of app development, certain aspects are particularly pronounced in the context of money-lending apps such as Avant.

Regulatory Compliance

The financial services industry is heavily regulated. Developing a money lending app necessitates stringent adherence to laws, regulations, and security standards. This involves legal counsel, compliance audits, and ongoing monitoring, significantly impacting development costs.

Integration with Financial Institutions

A money lending app must seamlessly integrate with banks, credit bureaus, and payment gateways. These integrations require specialized technical expertise and often involve fees or contractual obligations, contributing to development expenses.

Risk Assessment and Fraud Prevention

Mitigating financial risks and preventing fraud are paramount in lending. Implementing robust risk assessment models, fraud detection systems, and security measures demands significant investment in technology, personnel, and ongoing maintenance.

Credit Scoring and Risk Modeling

Accurately assessing borrowers’ creditworthiness is crucial for lending businesses. Developing sophisticated credit scoring models and risk assessment algorithms requires data scientists, specialized software, and continuous model refinement, increasing development costs.

Tech Stacks Required to Develop Money Lending Apps like Avant

Developing a money lending app like Avant requires a comprehensive tech stack covering front-end and back-end development, sophisticated risk assessment models, and robust security measures.

1. Front-End Development

Developing the user interface is crucial for a money-lending app. It involves creating an intuitive design that ensures a smooth user experience. Designing the user interface to adapt to various screen sizes ensures that the interface is easily accessible on all types of devices. Integrating with back-end services allows for seamless functionality, ensuring users can complete tasks efficiently.

2. Back-End Development

The back-end development involves server-side logic to handle loan applications, approvals, and disbursements. Managing databases for user data, loan information, and financial transactions is essential for smooth operation. Developing APIs facilitates communication between the front end and back end. Seamless integration with third-party services such as payment gateways and credit bureaus is essential to ensure comprehensive and robust functionality for our system.

3. Credit Scoring and Risk Assessment Models

Sophisticated algorithms are necessary for evaluating borrowers’ creditworthiness. Integrating various data sources, such as credit bureaus and bank statements, enhances the accuracy of these models. Utilizing machine learning allows for dynamic adjustments based on new data and market trends, ensuring up-to-date risk assessments.

4. Fraud Detection and Prevention Systems

Implementing real-time monitoring is essential for detecting fraudulent activities. Anomaly detection helps identify unusual patterns that may indicate fraud. Incorporating biometric authentication methods like fingerprints or facial recognition enhances security by providing an extra layer of protection.

5. Secure Data Management

Data encryption is critical for protecting sensitive financial information. Adhering to data privacy regulations like GDPR and CCPA ensures compliance and builds user trust. Implementing data loss prevention measures is crucial for protecting against unauthorized access and ensuring the security of the platform.

6. Payment Gateway Integration

Seamless transactions are fundamental for a money-lending app. Efficiently handling chargebacks and managing disputes and refunds are crucial for maintaining user satisfaction. Implementing robust security protocols protects payment data from unauthorized access and fraud.

7. Loan Origination and Management

Automating workflows streamlines the loan application process, reducing the time and effort required. Managing loan agreements and other paperwork electronically enhances efficiency. Effective loan servicing involves managing repayments, interest calculations, and handling delinquencies, ensuring smooth loan management.

8. Customer Relationship Management Systems

Storing and managing customer data effectively is vital for personalized service. Integrating communication channels like SMS, email, and in-app messaging facilitates efficient customer interactions. Ensuring that customers have access to strong support through multiple communication channels is essential for delivering timely and effective assistance.

How Do Money Lending Apps like Avant Generate Revenue?

Money lending apps, such as Avant, have revolutionized the financial landscape by offering accessible and convenient loan options to consumers. To sustain their operations and drive growth, these businesses employ several revenue-generating strategies.

1. Interest Income

The primary revenue source for money lending apps is interest charged on loans. Similar to traditional financial institutions, these companies lend money to borrowers at a specific interest rate. The difference between the interest earned and the cost of funds constitutes the interest income. Effective risk assessment and underwriting are crucial for maximizing this revenue stream while managing default risks. For example, Avant generates interest income on its AvantCard by charging a variable interest rate that typically ranges from 9.95% to 29.99% APR, depending on the borrower’s creditworthiness.

2. Fees and Charges

Beyond interest, money lending apps generate revenue through various fees and charges imposed on borrowers. These may include origination fees, late payment fees, and prepayment penalties. While these fees contribute to overall revenue, businesses must carefully balance fee structures to maintain customer satisfaction and avoid regulatory scrutiny. Avant, for instance, charges an annual membership fee of $95 for its AvantCard. Furthermore, when making a cash advance, users will incur a fee of either $10 or 3% of the transaction amount. Additionally, late payment charges can range from $25 to $35.

3. Loan Origination Fees

To cover operational costs associated with loan processing and underwriting, money lending apps often charge borrowers an origination fee. This fee is normally a percentage of the loan amount and is collected upfront. Streamlining the loan application process and leveraging technology can help businesses optimize origination fees while providing a seamless borrower experience.

4. Selling Loan Portfolios

In some cases, money lending apps may sell a portion of their loan portfolios to investors or other financial institutions. This process, known as securitization, allows businesses to generate immediate cash flow and reduce their exposure to credit risk. By carefully managing loan quality and diversifying their portfolio, companies can enhance the value of their loan assets.

5. Data Monetization

Money lending apps collect significant amounts of data on borrower behavior, creditworthiness, and repayment patterns. This data represents a valuable asset that can be monetized through various means. Businesses can leverage data analytics to refine their underwriting models, improve customer targeting, and develop new products. Additionally, anonymized and aggregated data can be sold to third-party companies for market research and other purposes.

Latest Technologies That Can Enhance a Money Lending App like Avant

To enhance the functionality and user experience of money lending applications like Avant, companies can leverage several innovative technologies.

1. Augmented Reality (AR) for Financial Education

By integrating AR features into money lending apps, companies can create immersive educational experiences that simplify complex topics such as loan products, interest rates, and repayment options. For example, users can visualize their loan repayment journey through AR simulations, allowing them to see how different payment schedules affect their finances over time.

A notable example is Fidelity Investments, which has launched an AR-based platform in the metaverse to enhance financial literacy. Their “Fidelity Stack” allows users to engage in gamified learning experiences, making financial education interactive and enjoyable. Research published in the Journal of Financial Services Marketing also supports the effectiveness of AR in enhancing financial literacy.

2. Internet of Things for Enhanced Data Collection

By integrating IoT devices, such as wearables or smart home systems, companies can collect real-time data on users’ financial behaviors and lifestyles. This data provides valuable insights into spending habits, income fluctuations, and overall financial health.

For instance, Lenddo, a fintech startup, utilizes IoT data to assess creditworthiness for underserved populations. By analyzing smartphone usage patterns and utility bill payments, Lenddo creates credit profiles for individuals with limited financial history. This innovative approach enables personalized loan products that align with users’ specific needs, enhancing user experience and positioning companies as proactive financial partners.

3. Blockchain Technology for Secure and Transparent Transactions

Companies can implement blockchain solutions to automate lending workflows, enhance security, and reduce operational costs. Smart contracts enable automatic execution of loan agreements, ensuring that terms are adhered to without the need for intermediaries.

A compelling example is CASHe, which uses blockchain technology to offer loans in the form of digital tokens. This approach ensures a higher level of transparency, speed, and security in transactions. By leveraging smart contracts, CASHe eliminates the need for paperwork and manual documentation, streamlining the lending process. The use of blockchain also provides an immutable record of all transactions, enhancing trust between borrowers and lenders

.

Conclusion

Money lending apps like Avant have changed the way people borrow money by making it easier and faster to get a loan. These apps get rid of the usual hassles of getting a loan, like loads of paperwork and having to go to a bank in person. They approve and give out loans quickly, which helps people handle unexpected expenses, combine debts, or finance personal projects more easily.

For financial technology companies, creating a similar money lending app is a great opportunity to reach more customers. By using technology and data analysis, these businesses can make new loan products, improve how they assess risk, and make the experience better for customers. Plus, they can make money from interest and fees and by selling loans to other companies. However, to do well in this competitive market, they need to focus on lending responsibly, following the rules, and making sure customers trust them.

Looking to Develop a Money Lending App like Avant?

Idea Usher can engineer a cutting-edge money-lending app mirroring Avant’s success. Our team, armed with over 500,000 hours of coding expertise, will construct a robust platform incorporating advanced features like predictive analytics for risk assessment, machine learning for streamlined underwriting, and robust cybersecurity measures. We’ll craft a user-centric app that accelerates loan processing, offers competitive rates, and ensures regulatory compliance, positioning your fintech venture for rapid growth and market dominance.

FAQs

Q1: How to create a money lending app?

A1: Creating a money lending app involves several key steps. First, thorough market research must be conducted to identify target users and competitors. Develop a comprehensive business plan outlining the app’s features, target market, and revenue model. Next, assemble a skilled development team to design and build the app. Integrate robust security measures and comply with relevant financial regulations. Implement effective marketing strategies to acquire users and build a strong brand identity.

Q2: How much does it cost to develop a loan lending app?

A2: The expense of developing a loan lending app is influenced by various factors. A basic app with limited features typically requires a lower investment compared to a complex platform with advanced functionalities. Additional costs may arise from design, technology choices, and the development team’s expertise.

Q3: How long does it take to develop a money-lending platform?

A3: Developing a money lending platform typically takes a few months. The exact timeline depends on various factors, including platform complexity, team size, and regulatory requirements. Key stages include planning, design, development, testing, and compliance. While a basic platform might be developed in a few months, incorporating advanced features and robust security measures can extend the development cycle.

Q4: How do money-lending apps make money?

A4: Money lending apps primarily generate revenue through interest charged on loans. They also earn fees from origination, late payments, and prepayment penalties. Additionally, some apps offer value-added services like credit monitoring or financial advice for a fee. By efficiently connecting borrowers with lenders and automating processes, these apps optimize operational costs, leading to higher profit margins.