(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Digital asset banking demands a higher security standard than most crypto products. Custody, transaction integrity, access control, and regulatory oversight must operate reliably under real financial risk. These expectations shape how a digital asset bank platform is designed, with security embedded into the core infrastructure rather than added later.

Asset protection depends on how systems perform across routine operations and edge cases alike. Key management, transaction authorization, monitoring, audit trails, and recovery mechanisms need to work together without exposing sensitive data or creating gaps in control. Platform resilience comes from enforcing these safeguards consistently across both on-chain and off-chain components.

In this blog, we explain how to build a secure digital asset bank platform by breaking down core security principles, architectural decisions, and practical considerations involved in delivering institutional-grade custody and financial services for digital assets.

What is a Digital Asset Bank Platform?

A Digital Asset Bank Platform is a specialized financial infrastructure that enables regulated institutions to provide banking services for non-traditional assets, such as cryptocurrencies (e.g., Bitcoin, Ethereum), stablecoins, and tokenized real-world assets (e.g., stocks, bonds, or real estate). These platforms bridge the gap between traditional fiat-based finance and the decentralized blockchain economy, allowing users to manage both digital and traditional holdings in a single, secure environment.

The Core Pillars

The core pillars of a Digital Asset Bank platform ensure secure custody, regulatory compliance, seamless fiat integration, and scalable financial infrastructure.

- Institutional-Grade Security & Custody: Protects digital assets with Multi-Party Computation (MPC) and cold storage, ensuring no single party controls private keys and assets stay safe from online threats.

- Regulatory Compliance & Licensing: Operates under legal frameworks, follows KYC/AML rules, and secures required licenses to ensure full legal compliance in relevant jurisdictions.

- Trading & Deep Liquidity: Enables seamless asset trading with minimal slippage by connecting to global exchanges, OTC desks, and market makers for fair pricing and round-the-clock execution.

- Fiat On/Off-Ramps: Bridges traditional and digital finance, enabling fast and secure conversion between fiat currencies and digital assets via reliable deposit and withdrawal options.

- Financial Service Innovation (Yield & Lending): Provides services like staking, lending, and DeFi access, letting users earn passive income from digital assets within a regulated environment.

- Operational Connectivity (APIs & Integration): Delivers robust APIs for seamless integration with accounting, portfolio management, and banking systems, streamlining reporting and transaction tracking for institutions.

How a Digital Asset Bank Differs from Crypto Wallets & Exchanges?

A Digital Asset Bank differs from crypto wallets and exchanges by combining regulated banking infrastructure, secure custody, and compliance-driven services with seamless crypto and fiat integration under one platform.

| Criteria | Digital Asset Bank Platform | Crypto Wallet | Crypto Exchange |

| Core Role in Finance | Provides regulated digital banking infrastructure for custody, accounting, compliance, and financial controls | Acts as a key-management and asset storage tool | Functions as a trading venue and liquidity aggregator |

| Custody & Key Security | Institutional custody using MPC or HSM, segregated wallets, enforced signing policies, and zero single-point control | User fully controls private keys and recovery responsibility | Centralized custody managed by exchange infrastructure |

| Compliance & Regulatory Readiness | Designed for licensing, audits, transaction reporting, and jurisdiction-specific regulatory enforcement | Generally non-compliant and user-regulated | Compliance focused mainly on trading and withdrawals |

| Financial System of Record | Internal banking-grade ledger synchronized with blockchain and fiat systems | Blockchain is the only record of ownership | Exchange-maintained internal balances for trading |

| Transaction Governance & Risk Control | Policy-based approvals, velocity limits, jurisdiction rules, and real-time risk scoring before execution | No transaction controls beyond user confirmation | Exchange-defined withdrawal rules and limits |

| Enterprise Support | Multi-user accounts, role-based permissions, approval workflows, and immutable audit trails | Not designed for corporate asset management | Limited enterprise features, trading-centric |

How does Digital Asset Bank work?

A Digital Asset Bank integrates regulated banking systems with blockchain infrastructure to securely manage custody, trading, lending, and fiat on-off ramps within a single compliant financial platform.

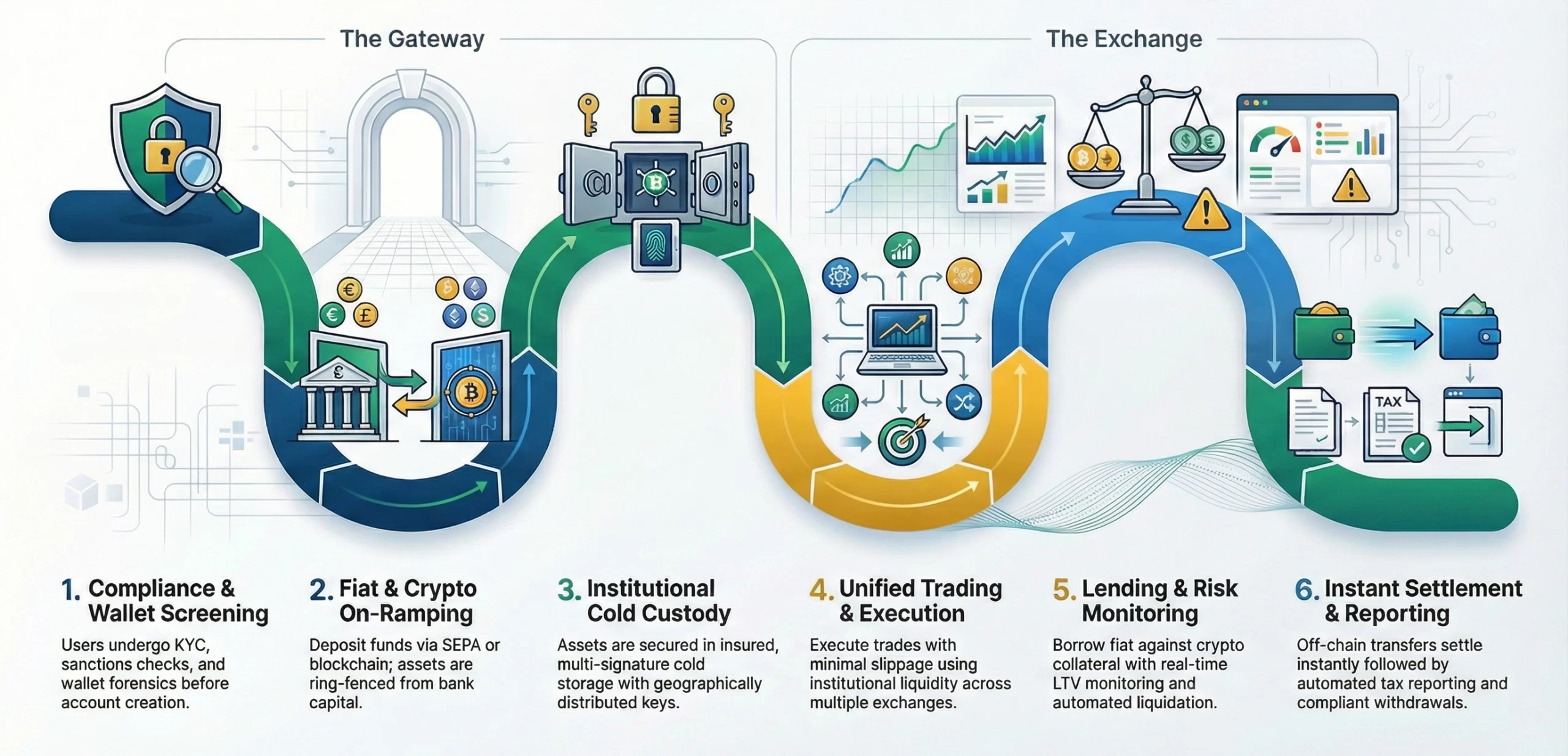

1. Onboarding & Compliance (The Gateway)

Users complete KYC/KYB, identity verification, sanctions screening, and wallet address checks. Upon approval, the bank creates segregated fiat and digital asset wallets aligned with regulatory requirements.

Example: Alice uploads her passport and completes a liveness check in 90 seconds. The bank screens her identity against 50+ global sanctions listsand evaluates jurisdictional and PEP risk. Her external wallet addresses are analyzed via Chainalysisfor exposure to darknet markets, mixers, or sanctioned entities. Once cleared, segregated fiat and digital asset wallets are created instantly.

2. Banking the Fiat Ramp (On/Off Ramps)

Users deposit fiat or crypto, which the bank credits to internal ledgers after settlement, confirmation, and AML checks, enabling seamless movement between traditional and digital financial systems.

Example: Alice deposits €15,000 via SEPA; funds clear in under two hours. Client fiat is held in ring-fenced accounts at Deutsche Bank, fully segregated from operational capital. She then deposits 2.5 BTC from cold storage. The bank requires three Bitcoin confirmations (~30 minutes), traces coin ancestry back to genesis, and credits her digital asset wallet.

3. Custody & Asset Servicing

The bank safeguards assets using institutional-grade cold custody, distributed key management, and optional staking services, while maintaining strict security and insurance coverage.

Example: Alice’s 2.5 BTC is swept into Fireblocks-powered MPC custody, requiring a 5-of-7 quorum across geographically distributed key shards in Switzerland, Singapore, and Delaware. Assets are insured up to $380M via Lloyd’s syndicates. Alice stakes 32 ETH and the bank operates the validator at 99.9% uptime, pays 4.2% APY, and retains a 15% service fee.

4. Trading & Execution

Users place trades through a unified interface. The system verifies balances, sources liquidity, executes trades with minimal slippage, and updates internal ledgers instantly while assets remain in secure custody.

Example: Alice buys $12,000 of ETHand verifies her fiat balance and executes the trade via an institutional liquidity aggregator sourcing prices from 12 exchanges, achieving 2 bps slippage. Alice’s ETH balance updates immediately, while the underlying ETH remains in the bank’s omnibus cold wallet under beneficial ownership.

5. Lending & Borrowing

Users can earn yield by lending assets or borrow fiat against crypto collateral. The bank manages credit risk, monitors collateral in real time, and enforces margin and liquidation rules automatically.

Example: Alice pledges 1.8 BTC at a 50% LTV to borrow $72,000 in fiat for business expansion at 8.9% APR. The system monitors BTC prices across seven oracles every 15 seconds. At 70% LTV, Alice receives a margin warning; at 75%, the auto-liquidation engine executes market sell orders and maintains compliance throughout.

6. Settlement & Reconciliation

Internal transfers settle instantly off-chain via ledger updates. External withdrawals trigger on-chain transactions. The bank reconciles internal liabilities against on-chain and fiat balances daily.

Example: Alice sends 5,000 USDC to Bob within the bank. The ledger debits Alice and credits Bob instantly no gas fees. She later withdraws 0.5 BTC externally and the bank signs the transaction using an HSM-backed 3-of-5 key shard policy. End-of-day reconciliation shows 18,450 BTC in client liabilities and 18,452.3 BTC held in custody, reflecting a controlled surplus.

7. Reporting & Exit (Off-Ramp)

The bank provides automated tax reporting, regulatory disclosures, and compliant fiat withdrawals, maintaining a complete and auditable transaction history.

Example: Alice generates her 2025 tax report. The system categorizes 847 transactions, applies the HIFO accounting method, and calculates a $23,400 realized capital gain. She sells 1.2 BTC at $94,000 and initiates a €98,000 SEPA withdrawal. After liquidity checks, the transfer settles within 45 minutes. All records are retained for seven years.

Why Digital Asset Bank Platforms are Gaining Popularity?

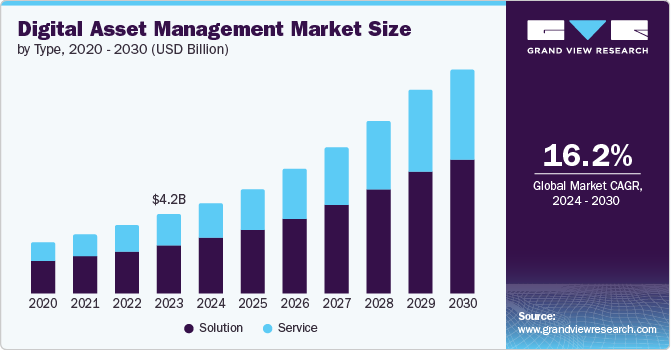

The global digital asset management market size was valued at USD 4.22 billion in 2023 and is projected to reach USD 11.94 billion by 2030, growing at a CAGR of 16.2% from 2024 to 2030. This growth reflects measurable adoption across institutions, infrastructure, and users rather than early-stage experimentation.

This growth is supported by both institutional adoption and changing user behavior, with over 76% of global consumers now using some form of digital banking, reinforcing long-term demand for digital-first financial platforms.

- Institutional Adoption at Scale: 45% of banks issued a digital asset in the past 12 months, while 50% of North American firms now run live DLT projects, a 72% year-over-year increase. Industry participation has grown 800% since 2020.

- Operational Efficiency Gains: 85% of firms identify intraday liquidity as the primary benefit, reporting 79% lower transaction costs and a 71% reduction in failed payments compared to traditional banking rails.

- Sustained Capital Investment: Funding for digital asset infrastructure has tripled since 2020, with average annual spend reaching $2.2 million per firm. Banks and technology providers invest up to 10× more than other market participants.

- Platform and Asset Growth: On-chain asset management AUM increased 118% to $35 billion, while regulated digital asset platforms report multi-fold revenue growth and rapidly expanding user bases.

- Stablecoins as Financial Rails: The stablecoin market reached $250 billion with $26.1 trillion in transaction volume, with projections of $500–750 billion, reinforcing stablecoins as core settlement and treasury instruments.

Digital asset bank platforms are gaining popularity not because of hype, but because capital, institutions, infrastructure, and users are already aligned. The market has moved into an execution phase where secure, compliant platforms can be built, launched, and scaled with real demand behind them.

Industry Use Cases of Digital Asset Bank Platforms

Digital Asset Bank Platforms (DABPs) have evolved from experimental pilots to core infrastructure for global industries, primarily by bridging traditional finance with blockchain-based efficiency.

1. Finance and Capital Markets

The most direct use case is the tokenization of financial instruments to enable 24/7 trading and near-instant settlement.

Real-World Example:

- Goldman Sachs uses its GS DAP™ platform to facilitate the issuance, registration, and settlement of tokenized assets.

- BlackRock launched the BUIDL fund in 2024, an institutional-grade tokenized fund invested in US Treasury bonds that provides daily dividends on-chain.

2. Supply Chain and Global Trade

DABPs streamline trade finance by digitizing paper-heavy documents and providing real-time payment traceability.

Real-World Example:

- Spydra enabled the brand Raymond to tokenize supply chain invoices, accelerating invoice discounting and improving cash flow through real-time payment tracking.

- Standard Chartered and Northern Trust launched Zodia Custody, a platform that provides institutional safekeeping for digital assets, supporting the complex needs of global trade participants.

3. Real Estate and High-Value Assets

Tokenization allows for fractional ownership, lowering entry barriers for investors and providing liquidity to traditionally illiquid assets.

Real-World Example:

- Propy utilizes blockchain to facilitate cross-border real estate transactions, simplifying international property buying.

- Masterworks tokenizes high-value blue-chip paintings, allowing investors to buy “shares” in artwork rather than the entire piece.

4. Corporate Treasury and Global Payments

Enterprises use DABPs to manage stablecoins for cross-border B2B payments, bypassing slow and expensive traditional correspondent banking.

Real-World Example:

- Uber partnered with Green Dot Bank and Barclays to provide debit cards to drivers, allowing them to access daily earnings instantly via a digital banking layer.

- Platforms like CoinsPaid provide infrastructure for businesses to accept stablecoins (like USDC) for global invoicing and payroll, reducing currency conversion fees.

5. Institutional Custody and Staking

Regulated banks now offer secure “safekeeping” services and yield-generating options like staking for institutional clients.

- BNY Mellon and Fidelity provide institutional-grade custody platforms that store private keys in secure, multi-layered environments.

- SEBA Bank (now AMINA) offers an institutional-grade Ethereum staking service, allowing clients to earn rewards on their holdings while maintaining them in a regulated bank.

Key Features of a Secure Digital Asset Bank Platform

A secure Digital Asset Bank platform combines identity, payments, custody, and on-chain services with strong security and scalability, delivering compliant, user-friendly financial infrastructure beyond traditional crypto wallets and exchanges.

1. User Onboarding & Identity Verification

The platform embeds KYC, KYB, AML, and sanctions screening directly into account creation, assigning dynamic risk profiles that determine transaction limits, asset access, and approval rules before any wallet or balance is activated.

2. Bank-Grade Digital Asset Custody

User assets are protected through multi-party computation (MPC) or HSM-based custody, with hot, warm, and cold wallet segregation, policy-driven signing, and zero private-key exposure, ensuring institutional-level protection against external attacks and internal misuse.

3. Internal Ledger & Balance Management

A real-time internal ledger functions as the system of record, synchronizing fiat and digital asset balances, handling instant transfers, and continuously reconciling on-chain activity to guarantee financial accuracy, auditability, and regulatory compliance.

4. Policy-Based Transaction Controls

Every transaction is governed by programmable rules covering amount thresholds, velocity limits, jurisdiction restrictions, asset risk levels, and user behavior, allowing the platform to automatically approve, delay, flag, or block transactions before execution.

5. Secure Transaction Authorization & Approval

Transactions pass through multi-layer authorization flows including multi-factor confirmation, role-based approvals, and time-locked execution, preventing single-point fund movement and aligning asset transfers with enterprise governance and compliance requirements.

6. Fiat On-Ramp & Off-Ramp Integration

The platform connects regulated banking rails with blockchain infrastructure, enabling users to deposit, withdraw, and convert fiat and digital assets while maintaining clear settlement visibility, ledger consistency, and compliance across both financial systems.

7. Risk Monitoring & Fraud Prevention

An always-on risk engine analyzes transaction patterns, wallet behavior, and blockchain intelligence in real time, automatically triggering alerts, transaction freezes, or manual reviews to stop fraud, laundering, or abnormal activity before losses occur.

8. Enterprise Accounts & Role-Based Access

Business users operate through multi-user accounts with granular permissions, approval hierarchies, and immutable audit trails, allowing organizations to manage digital assets securely while maintaining internal controls and accountability across teams.

9. User-Controlled Security

Users can define withdrawal allowlists, transaction limits, device restrictions, and real-time alerts, giving them direct control over account security while the platform enforces institutional safeguards in the background.

10. Transaction History & Compliance Records

The platform provides detailed transaction logs, downloadable statements, and compliance-ready reports that align internal ledger data with on-chain activity, enabling users to meet accounting, tax, audit, and regulatory reporting requirements confidently.

How to Build a Secure Digital Asset Bank Platform?

Building a secure Digital Asset Bank platform requires strong architecture, regulatory compliance, and institutional-grade security across fiat and blockchain systems. Our developers follow best practices and compliance-first frameworks to deliver scalable, secure digital banking solutions.

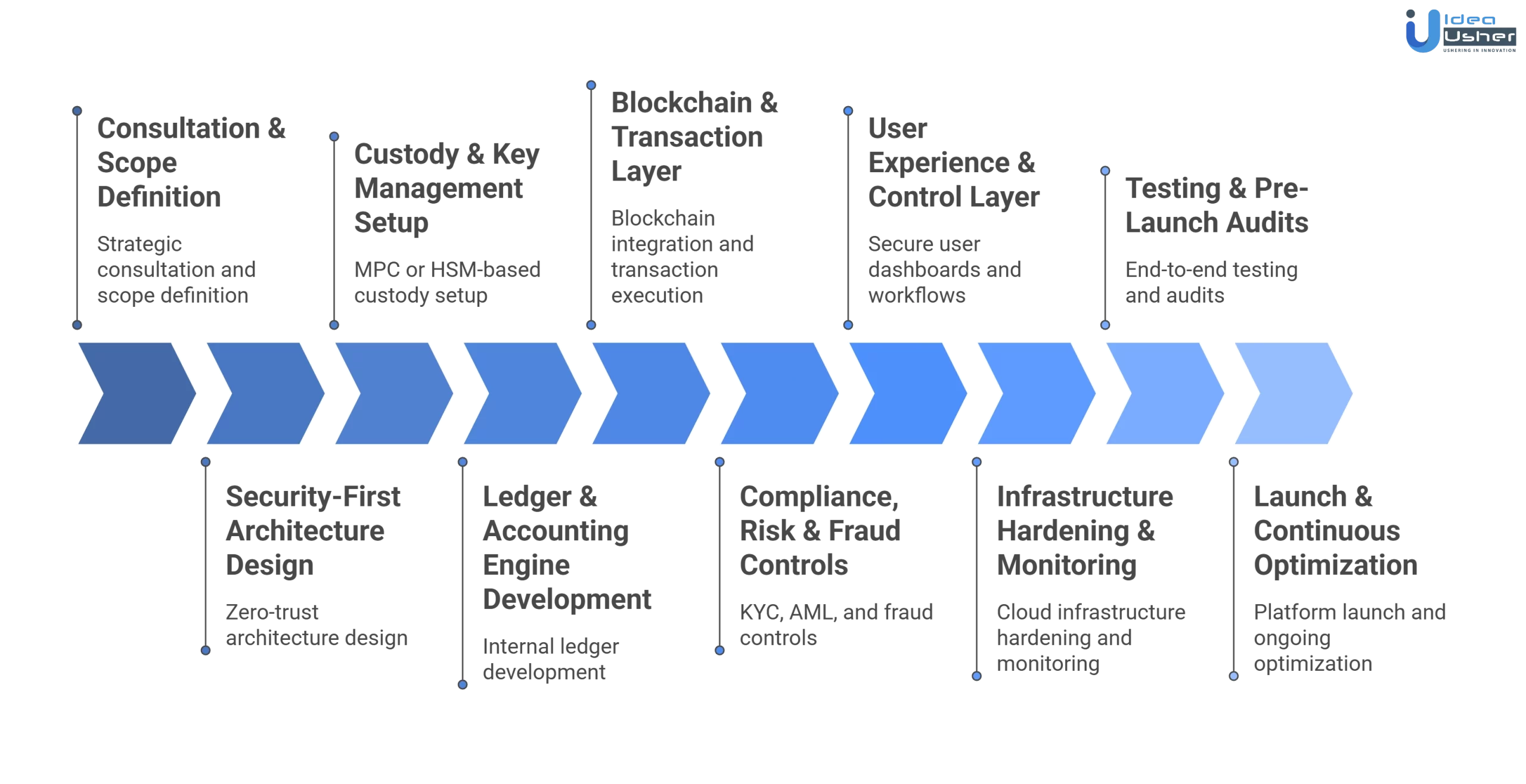

1. Consultation & Scope Definition

We start with a strategic consultation to understand the client’s business model, target users, and outcomes. Based on this, we define jurisdictions, licensing needs, custody obligations, and compliance scope while advising on architecture and risk decisions to ensure long-term scalability and regulatory readiness from day one.

2. Security-First Architecture Design

Our developers design a zero-trust architecture, separating custody, ledger, risk, and application layers. We conduct threat modeling early to eliminate single points of failure and insider-risk exposure before development starts.

3. Custody & Key Management Setup

We implement MPC or HSM-based custody with hot, warm, and cold wallet segregation. Transaction signing policies, approval thresholds, and recovery mechanisms are enforced at the infrastructure level, not just application logic.

4. Ledger & Accounting Engine Development

We build an internal ledger as the system of record to manage balances, asset movements, fees, and reconciliations. This layer ensures real-time accuracy across fiat and digital assets while supporting audits and regulatory reporting.

5. Blockchain & Transaction Execution Layer

Our developers integrate blockchain nodes, indexers, and transaction relayers to track deposits, validate confirmations, and broadcast signed transactions securely. Multi-chain logic is isolated to minimize systemic risk.

6. Compliance, Risk & Fraud Controls

We embed KYC, AML, sanctions screening, and transaction monitoring directly into user actions and transaction flows. Risk scoring and behavioral analysis determine whether transactions are approved, delayed, flagged, or blocked in real time.

7. User Experience & Control Layer

We develop secure user dashboards, enterprise approval workflows, and account control settings that balance transparency with safety. Every action is logged and mapped to backend policies for full auditability.

8. Infrastructure Hardening & Monitoring

Our team deploys the platform on hardened cloud infrastructure with encryption, network segmentation, continuous monitoring, and automated incident response. Disaster recovery and failover scenarios are validated before launch.

9. Testing & Pre-Launch Audits

We perform end-to-end testing across custody, ledger accuracy, compliance enforcement, and failure handling. Security audits and controlled simulations ensure the platform meets bank-grade security and operational standards.

10. Launch & Continuous Optimization

We launch the platform with real-time monitoring enabled, then continuously optimize security rules, infrastructure performance, and user experience based on live usage, risk signals, and regulatory updates.

Digital Asset Platform Development Cost

Digital asset platform development cost depends on security requirements, regulatory scope, and feature complexity, including custody, compliance, and integrations. Understanding these factors helps businesses plan budgets and build scalable, compliant digital asset platforms efficiently.

| Development Phase | What We Deliver | Estimated Cost |

| Consultation | Business consultation, jurisdiction analysis, compliance scope, custody model recommendation, platform architecture blueprint | $8,000 – $12,000 |

| Security-First Architecture Design | Zero-trust system design, component separation, threat modeling, infrastructure planning | $10,000 – $15,000 |

| Custody & Key Management Setup | MPC or HSM integration, wallet segregation (hot/warm/cold), signing policies | $25,000 – $35,000 |

| Ledger & Accounting Engine | Internal ledger, balance tracking, reconciliation logic, fee handling | $18,000 – $25,000 |

| Blockchain & Transaction Layer | Blockchain node integration, deposit tracking, transaction broadcasting, confirmations | $15,000 – $22,000 |

| Compliance & Fraud Controls | KYC/KYB integration, AML rules, transaction monitoring, risk scoring | $12,000 – $18,000 |

| User Experience & Control Layer | Secure dashboards, transaction flows, approval workflows, security settings | $10,000 – $15,000 |

| Infrastructure Monitoring | Secure cloud setup, logging, monitoring, access controls, backups | $8,000 – $12,000 |

| Testing & Pre-Launch Hardening | End-to-end testing, security reviews, failure simulations | $7,000 – $10,000 |

| Launch & Initial Optimization | Production launch, monitoring calibration, post-launch fixes | $5,000 – $8,000 |

Total Estimated Cost: $65,000 – $128,000+

Note: Actual development costs may vary based on regulatory scope, custody complexity, supported assets, integrations, and security requirements.

Consult with IdeaUsher to evaluate your requirements and get a tailored cost estimate for your digital asset bank platform.

What Increases the Cost of a Digital Asset Bank Platform?

Development complexity, security requirements, regulatory compliance, integrations, scalability, and maintenance increase digital asset banking costs.

1. Multi-Jurisdiction Regulatory Coverage

Supporting multiple countries increases costs due to separate compliance rules, reporting logic, data residency requirements, and jurisdiction-specific transaction controls built into the platform.

2. Advanced Custody & Management Models

Implementing MPC, HSM clusters, cold storage automation, and complex signing policies significantly raises infrastructure, integration, and ongoing security engineering costs.

3. Enterprise-Grade Approval & Governance Workflows

Multi-user accounts, hierarchical approvals, custom permissions, and immutable audit trails require additional backend logic, UI complexity, and extensive testing.

4. Real-Time Risk, AML & Chain Analytics

Continuous transaction monitoring, behavioral analysis, blockchain intelligence, and automated enforcement engines increase cost due to third-party tools and custom rule engines.

5. Multi-Chain & Tokenized Asset Support

Supporting multiple blockchains and token standards requires separate indexers, node management, reconciliation logic, and risk models, increasing both development and maintenance effort.

6. Disaster Recovery & Compliance Audits

Active-active infrastructure, failover systems, incident simulations, and external security audits add substantial cost but are essential for bank-grade reliability and trust.

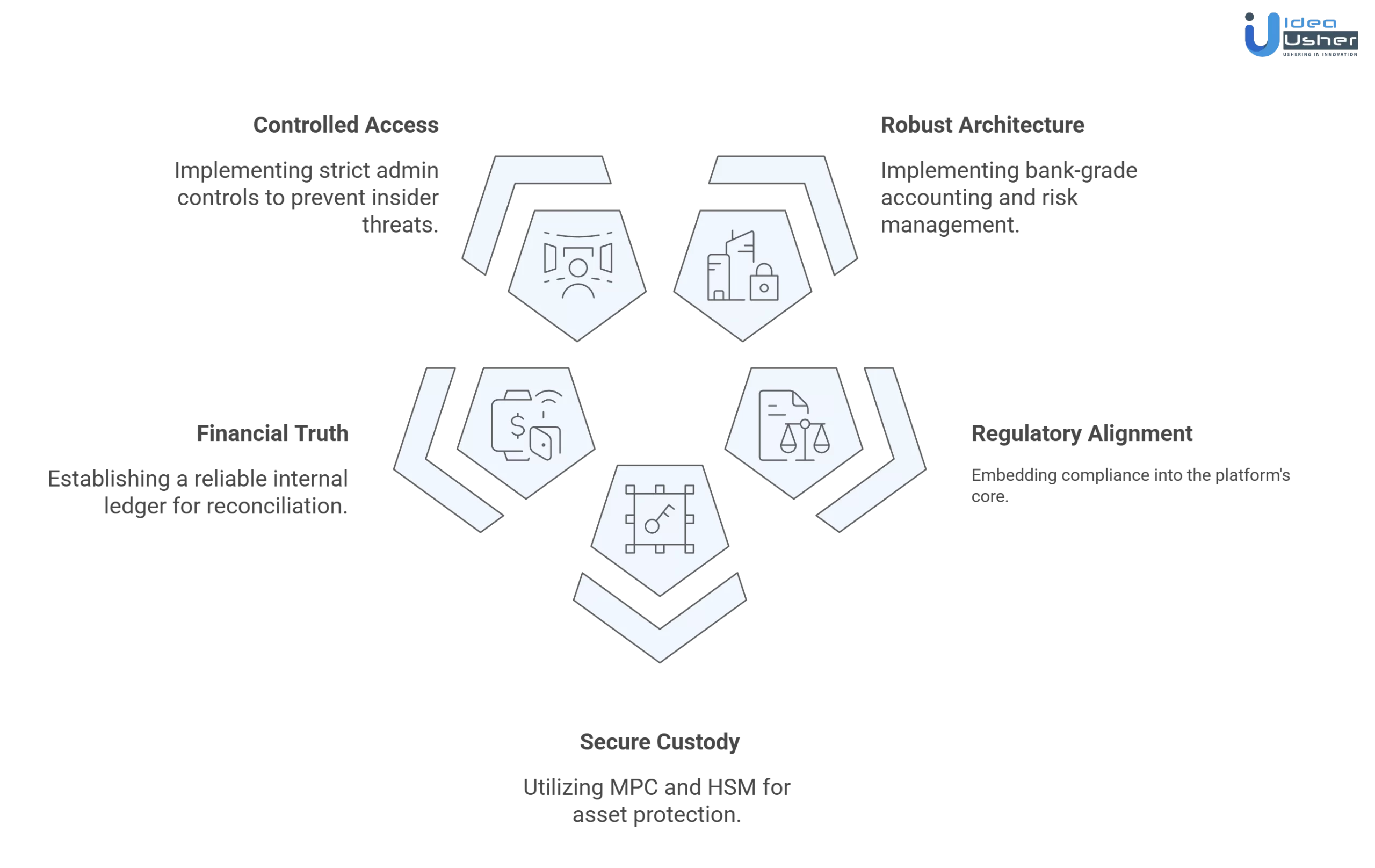

Common Mistakes That Break Digital Asset Bank Platforms

Digital asset bank platforms often fail due to security gaps, scalability issues, and poor compliance planning. Our experienced developers prevent these pitfalls with robust architecture, regulatory alignment, and future-ready engineering.

1. Digital Asset Bank Like a Crypto App

The Mistake: Platforms are built like wallets or exchanges, ignoring bank-grade accounting, controls, auditability, and operational risk management requirements.

How our developers handle it: We architect the platform as a financial system first, implementing internal ledgers, reconciliation, approval workflows, and compliance-driven transaction logic from the foundation layer.

2. Bolting Compliance On After Development

The Mistake: Compliance tools are added post-development, forcing architectural rework, delayed launches, and increased regulatory exposure across user onboarding and transactions.

How our developers handle it: We embed KYC, AML, sanctions screening, and risk checks directly into onboarding, wallet creation, and transaction flows so compliance shapes architecture, not patches it.

3. Weak or Over-Centralized Custody Design

The Mistake: Single-key custody, poor wallet segregation, or excessive admin access creates catastrophic exposure to hacks, insider misuse, and irreversible asset loss.

How our developers handle it: We implement MPC or HSM-based custody with hot, warm, and cold wallet segregation, strict signing policies, and zero single-point control over asset movement.

4. No True Source of Financial Truth

The Mistake: Relying only on blockchain balances causes reconciliation errors, reporting gaps, and audit failures when transactions, fees, or reversals occur.

How our developers handle it: We build a banking-grade internal ledger as the system of record, continuously reconciling on-chain activity with user balances and compliance reporting requirements.

5. Uncontrolled Admin & Internal Access

The Mistake: Overpowered admin panels and shared credentials expose platforms to insider threats, unauthorized actions, and untraceable operational changes.

How our developers handle it: We enforce role-based access control, approval hierarchies, action logging, and immutable audit trails across all internal systems and administrative operations.

Does a Digital Asset Bank Require a Banking License?

Digital asset banks face complex licensing requirements depending on jurisdiction, custody models, and services offered. Understanding when a banking, payments, or crypto license is required ensures compliant, scalable, and legally sound operations.

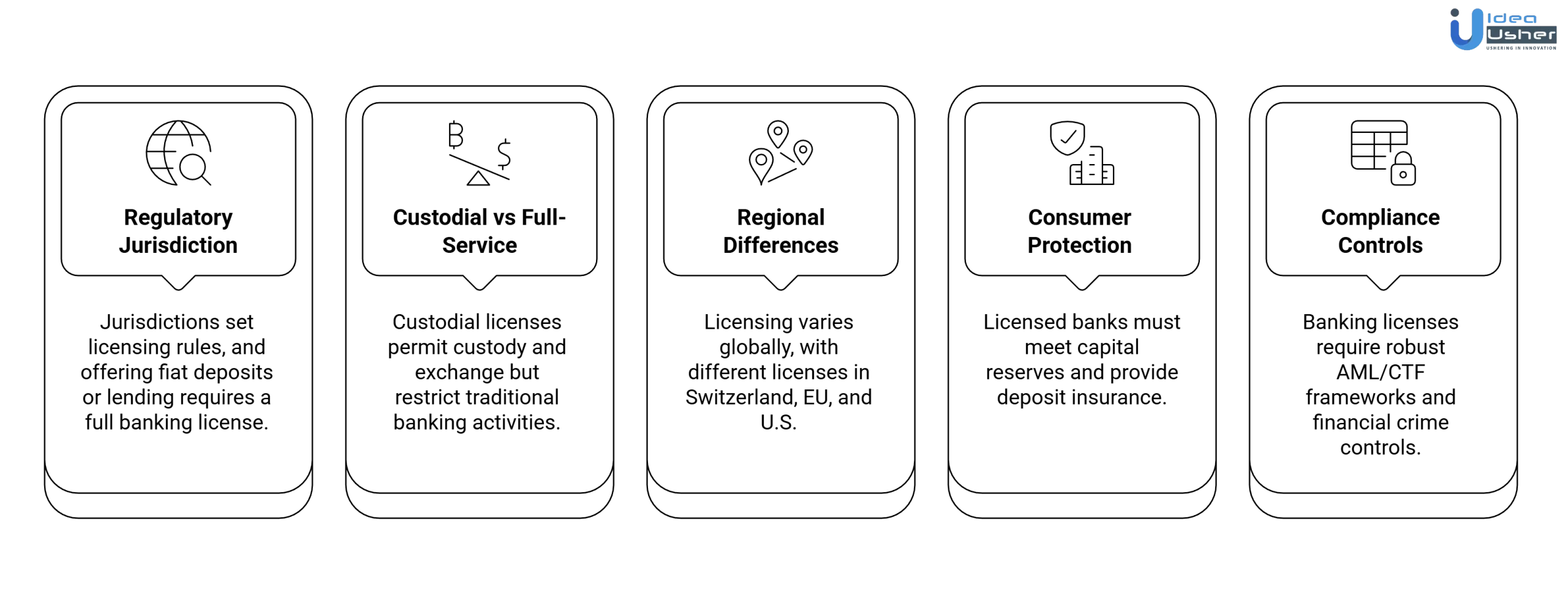

1. Regulatory Jurisdiction and Service Scope

Licensing requirements depend on jurisdiction and the platform’s functional scope. If the entity accepts fiat deposits, issues loans, or presents itself as a bank, a full national banking license is typically mandatory to remain legally compliant.

2. Custodial vs Full-Service Banking Licenses

Many digital asset platforms operate under “Trust” or “VASP” (Virtual Asset Service Provider), or custodial licenses. These frameworks permit secure digital asset custody and exchange but explicitly restrict traditional banking activities such as deposit-taking and fractional reserve lending.

3. Regional Differences in Regulation

Licensing requirements vary globally, for example, Switzerland offers a Fintech License, the EU follows MiCAR, while the U.S. requires state-level BitLicenses or federal OCC charters. Operating without appropriate authorization can trigger enforcement actions and shutdowns.

4. Consumer Protection and Deposit Safeguards

Licensed digital asset banks must meet capital reserve requirements and, where applicable, provide deposit insurance. These protections safeguard client funds against insolvency that unlicensed or lightly regulated platforms cannot legally offer.

5. Compliance and Financial Crime Controls

Holding a banking license requires robust Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) frameworks, including transaction monitoring, sanctions screening, and blockchain analytics. These controls ensure digital asset flows meet global financial transparency and reporting standards.

Top Example of Digital Asset Bank Platforms

Leading digital asset bank platforms demonstrate secure custody, regulatory compliance, and seamless user experiences. These examples highlight how modern infrastructure enables trusted crypto banking, institutional adoption, and scalable financial services.

1. Anchorage Digital

A U.S.-based regulated digital asset bank and infrastructure platform, Anchorage Digital Bank holds the first federally chartered crypto bank charter, offering institutional-grade custody, trading, staking, settlement, and stablecoin services, blending traditional cash and crypto rails under strict compliance.

2. Sygnum Bank

A pioneer Swiss and Singaporean regulated digital asset bank, Sygnum delivers bank-grade trading, custody, staking, tokenization, and compliance services worldwide, supporting institutional clients with deep liquidity, multi-asset settlement, and modular B2B banking tools in a fully compliant ecosystem.

3. Kinexys Digital Assets

Kinexys by J.P. Morgan is a bank-led blockchain platform powering digital payments, asset tokenization, and programmable rails; it enables institutional tokenized assets and bank-issued deposit tokens like JPM Coin, transforming cross-border payments and financial information flows.

4. AMINA Bank (formerly SEBA)

A Swiss FINMA-regulated crypto and fiat bank, AMINA Bank integrates everyday banking with digital asset custody, trading, staking, lending, and multi-currency services, offering secure crypto-native and traditional finance products under Swiss banking regulation.

5. Xapo Bank

A Gibraltar-based crypto-focused private bank and virtual asset provider, Xapo Bank combines secure Bitcoin and USDC holding accounts with global banking functions such as debit cards, interest-bearing accounts, and secure vault storage, bridging traditional finance with digital asset services.

Conclusion

Building a secure digital asset bank platform requires more than strong technology choices. It demands clarity on regulation, disciplined security practices, and a deep respect for user trust. From custody architecture to transaction controls, every decision shapes resilience and credibility. Successful digital asset bank platform development balances innovation with governance, aligning blockchain capabilities with proven banking standards. When security, compliance, and user experience are designed together, the platform can scale responsibly. This approach supports long term confidence for institutions and customers navigating digital assets with shared accountability and operational transparency.

Build a Secure Digital Asset Bank Platform with IdeaUsher

We bring deep experience in blockchain engineering, crypto platforms, and regulated financial systems. Our ex-FAANG and MAANG developers have built secure blockchain solutions for global enterprises. Using this practical knowledge, we design digital asset bank platforms aligned with security, compliance, scalability, and real business objectives, not just technical requirements.

Why Work With Us?

- Bank-Grade Security Architecture: We implement custody, key management, and risk controls aligned with financial regulations.

- Regulatory-First Design: Our platforms integrate KYC, AML, and reporting frameworks from day one.

- Scalable Platform Engineering: We build modular systems that support growth without weakening security.

- Institutional-Ready Infrastructure: Our solutions are designed for reliability, audits, and long-term operations.

Explore our portfolio to see how blockchain solutions and crypto applications are delivered for diverse enterprise and financial use cases.

FAQs

A.1. Security audits typically include smart contract reviews, infrastructure penetration testing, custody process audits, and compliance assessments. Auditors validate that systems, controls, and policies meet regulatory standards and withstand real-world threats.

A.2. Multi–layer controls such as cold storage, hardware security modules, encryption, access management, and continuous monitoring ensure security. These measures reduce attack surfaces and protect private keys, transactions, and sensitive customer data.

A.3. A digital asset bank platform must follow KYC, AML, transaction monitoring, data protection, and reporting obligations. Teams should embed compliance frameworks into workflows to meet regulatory standards without disrupting user experience or operational efficiency.

A.4. Modular architecture, secure APIs, and automated monitoring enable scalability. Teams separate core systems and apply consistent security controls so the platform can grow transaction volumes and users while maintaining stability and risk oversight.