Global trade moves fast, but trust still lags behind. Banks face constant uncertainty regarding ownership status approvals and exposure to duplicate financing. This is why trade finance tokenization platforms are gaining momentum, as they replace document checks with verifiable asset states.

Tokenization allows trade instruments to exist as digitally native records that may be validated in real time. It can also enable programmable controls such as usage restrictions, expiry enforcement, and conditional transfer rules. Settlement may occur faster, while audit trails remain continuously available to regulators and counterparties.

We’ve developed numerous bank-grade trade finance tokenization solutions that use permissioned distributed ledgers and compliance rule enforcement layers. As IdeaUsher has this expertise, we’re sharing this blog to discuss the steps to develop a trade finance tokenization platform for banks.

Key Market Takeaways for Trade Finance Tokenization Platforms

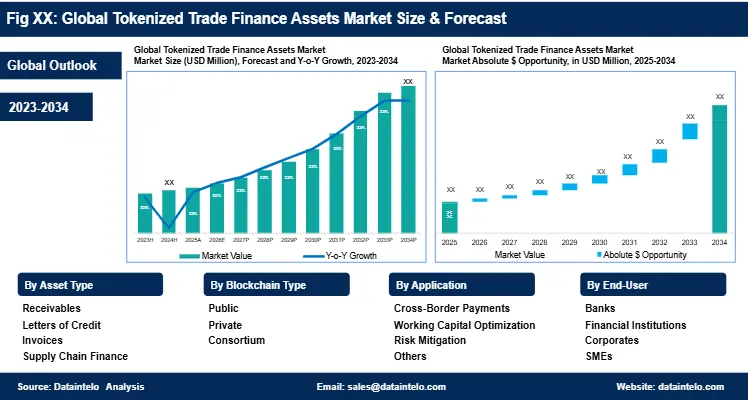

According to DataIntelo, the trade finance tokenization market is moving quickly from experimentation to real-world adoption by banks. Tokenized trade finance assets were valued at around USD 3.9 billion in 2024 and are expected to grow at close to 29 percent annually through 2033. This momentum is closely tied to the USD 2.5 trillion global trade finance gap, where banks are being pushed to digitize documents, improve asset visibility, and make trade instruments easier to distribute and fund.

Source: DataIntelo

On the platform side, banks are laying digital foundations that naturally support tokenization. Contour, co-founded by leading global banks including HSBC, has digitized the full letter-of-credit lifecycle on a shared blockchain network.

By integrating with document and trade data providers, Contour enables paperless issuance, verification, and exchange, making underlying trade flows easier to standardize and tokenize.

At the infrastructure level, cross-bank initiatives are addressing the settlement layer needed for scalable tokenization. Fnality International, backed by banks including Santander, Barclays, UBS, and HSBC, is building a blockchain-based network to settle transactions in tokenized central bank money.

What Does a Trade Finance Tokenization Platform Mean for Banks?

A trade finance tokenization platform for banks is a secure digital system that converts instruments like letters of credit, invoices, and bills of lading into regulated digital tokens. These tokens represent real legal claims and can be issued, transferred, and settled on a permissioned ledger with built-in compliance checks.

This helps banks reduce paperwork, improve transparency, and achieve faster settlement while staying aligned with existing trade finance laws and regulations.

Types of Trade Assets That Can Be Tokenized

Trade assets in tokenized trade finance may include payment obligations, shipment ownership records, and inventory claims. These assets can be digitized on-chain and verified in a controlled way. This can gradually improve settlement speed and risk visibility for banks.

1. Trade Receivables (Invoices)

Trade receivables represent confirmed payment obligations from buyers to sellers. When tokenized, invoices become digitally verifiable assets that banks can finance, fractionally distribute, or pledge as collateral while maintaining full traceability and audit control.

2. Letters of Credit (LCs)

Letters of credit can be tokenized as programmable bank commitments linked to trade conditions. This allows banks to automate document checks, track LC status in real time, and trigger settlement only when contractual conditions are satisfied.

3. Bills of Lading

Bills of lading represent legal ownership of goods in transit. Tokenizing them enables secure digital transfer of title, reduces document fraud, and allows banks to finance shipments while goods are still moving through the supply chain.

4. Inventory and Warehouse Receipts

Inventory stored in approved warehouses can be tokenized using digital warehouse receipts. This gives banks confidence in asset existence and custody while enabling faster inventory-backed financing and real-time collateral monitoring.

5. Purchase Orders (POs)

Purchase orders reflect a buyer’s intent to purchase goods under agreed terms. Tokenizing POs allows banks to provide pre-shipment financing with clear visibility into buyer credibility, order value, and fulfillment status.

5. Commodities Under Trade

Physical commodities such as oil, metals, or agricultural goods can be tokenized as trade-backed assets. Each token represents a defined quantity and quality, enabling banks to finance commodity flows with improved transparency and reduced reconciliation risk.

6. Export and Import Finance Contracts

Export and import finance agreements can be tokenized to standardize terms and automate lifecycle management. This helps banks manage exposure, enforce compliance rules, and enable secondary participation where permitted.

7. Insurance and Guarantee Instruments

Trade credit insurance policies and bank guarantees can be represented as tokenized risk instruments. This allows banks to link protection directly to financed assets and automate claim or payout events when predefined conditions occur.

8. Supply Chain Finance Obligations

Approved payables in supply chain finance programs can be tokenized once buyers validate them. This gives banks and investors high-confidence assets while preserving confidentiality and improving liquidity for suppliers.

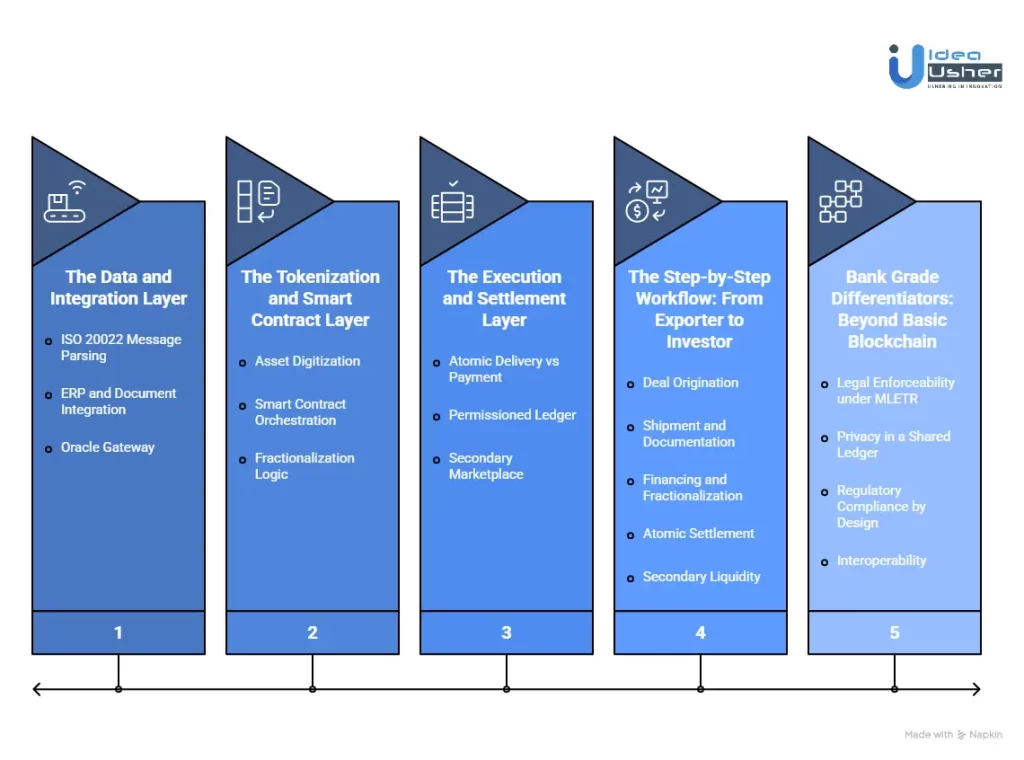

How Does a Trade Finance Tokenization Platform for Banks Work?

A trade finance tokenization platform connects bank systems to a digital ledger, where trade documents can be converted into legally enforceable tokens. Smart contracts may automatically validate shipment events and should trigger payment only when conditions are met.

1. The Data and Integration Layer

This is where physical trade processes connect to digital infrastructure. The platform does not replace core banking systems. It integrates with them.

- ISO 20022 Message Parsing: The platform ingests standard SWIFT messages such as MT700 for Letters of Credit, through existing banking channels.

- ERP and Document Integration: Structured data is pulled from SAP, Oracle, or trade document portals. Paper-based Bills of Lading, invoices, and certificates of origin are digitized into structured records.

- Oracle Gateway: Verified external data sources such as IoT container sensors, AIS ship tracking, and customs APIs are connected. Real-world trade events are securely brought onto the digital ledger.

2. The Tokenization and Smart Contract Layer

This layer converts static documents into dynamic, programmable financial assets.

Asset Digitization

A Letter of Credit or Bill of Lading is minted as a unique digital token. This token is legally structured to represent exclusive possession and is compliant with MLETR requirements.

Smart Contract Orchestration

Self-executing contracts encode the trade agreement logic. Payment is released only when the required conditions are met, such as presentation of the Bill of Lading token and confirmation of port arrival from shipping oracles.

Fractionalization Logic

A single trade finance exposure, for example, a $10M loan, can be divided into thousands of smaller digital notes. Each unit becomes a tokenized security that can be distributed or traded.

3. The Execution and Settlement Layer

This is where final settlement and risk elimination occur.

Atomic Delivery vs Payment

The platform integrates with digital deposit tokens or regulated stablecoins. When the Bill of Lading token transfers ownership, the payment token settles simultaneously in a single atomic transaction. Settlement time drops from days to seconds.

Permissioned Ledger

Transactions run on a private bank-controlled blockchain or a permissioned public network. Privacy is preserved among known participants while an immutable audit trail is maintained.

Secondary Marketplace

Fractional trade finance tokens can be listed on a regulated internal marketplace. Institutional investors can acquire exposure, providing new liquidity channels for banks.

The Step-by-Step Workflow: From Exporter to Investor

Let’s walk through a tokenized trade finance transaction.

| Stage | Description |

| Deal Origination | Exporter and importer agree on terms and the bank issues a digital Letter of Credit token. |

| Shipment and Documentation | Goods are shipped and a tokenized electronic Bill of Lading is created after oracle verification. |

| Financing and Fractionalization | The bank may finance the trade and split the asset to share risk. |

| Atomic Settlement | Payment and document transfer settle instantly through a smart contract. |

| Secondary Liquidity | Performed loans can be sold to investors to recycle capital. |

Bank Grade Differentiators: Beyond Basic Blockchain

A production-ready platform embeds legal enforceability, privacy controls, and regulatory compliance directly into the core architecture. It integrates with real banking systems and supports live settlement, governance, and auditability at scale

- Legal Enforceability under MLETR: The token is designed as the single authoritative digital original. Smart contract controls ensure exclusive possession equivalent to paper instruments.

- Privacy in a Shared Ledger: Zero-knowledge proofs or private data channels allow validation without exposing sensitive commercial information to other participants.

- Regulatory Compliance by Design: KYC and AML checks are embedded at the protocol level. Tokens can automatically freeze or restrict transfers if sanctions or compliance violations occur.

- Interoperability: The platform acts as an orchestration layer. It connects legacy banking systems with multiple blockchains and digital currency networks without creating a closed ecosystem.

How to Develop a Trade Finance Tokenization Platform for Banks?

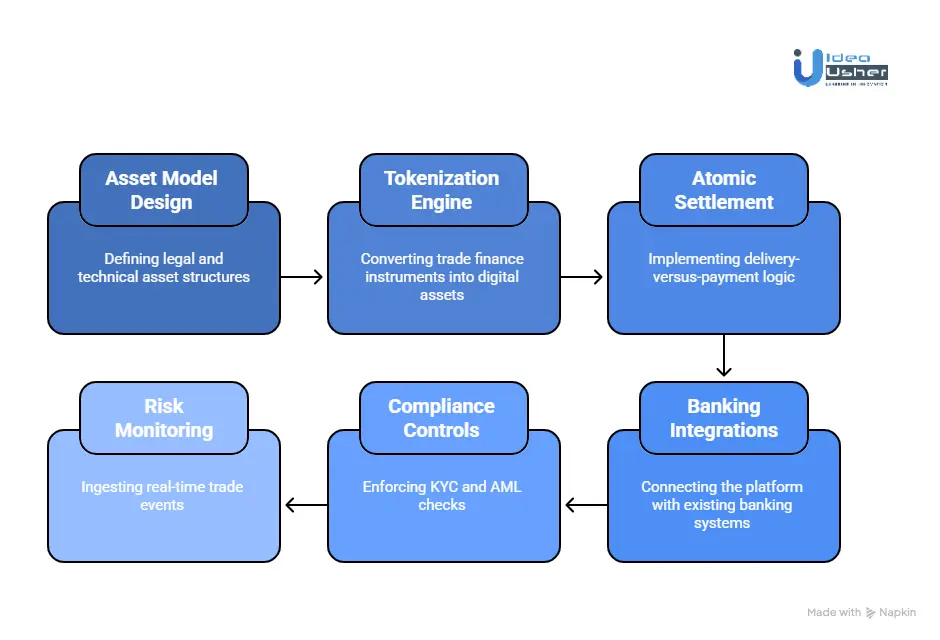

Developing a trade finance tokenization platform for banks typically begins by aligning legal ownership with on-chain control. We may then tokenize trade assets and connect settlement to regulated payment rails, reducing risk early.

We have worked with banks to build trade finance tokenization platforms, and here is how we typically do it.

1. Asset Model Design

We begin by defining a legal and technical asset structure that aligns with MLETR. Tokens are designed to represent possession and control in a legally recognized way. Transfer and revocation logic is clearly defined, so banks retain enforceability and auditability at every stage.

2. Tokenization Engine

We build the core engine that converts trade finance instruments into digital assets. Token standards and metadata are structured to reflect real trade documents. Lifecycle controls ensure issuance, updates, and settlement states are consistently tracked on-chain.

3. Atomic Settlement

We implement delivery-versus-payment logic to mitigate counterparty risk. HTLC or relay-based mechanisms ensure that asset transfer and payment occur together. This layer is integrated with deposit tokens or regulated stablecoins to support bank-grade settlement.

4. Banking Integrations

We connect the platform with existing banking and enterprise systems. On-chain events are mapped to ISO 20022 messages. Secure APIs enable seamless integration with core banking platforms and ERPs without disrupting current operations.

5. Compliance Controls

Compliance is embedded directly into the transaction flow. KYC and AML checks are enforced at the token level. Jurisdictional and sanctions rules are applied automatically so only compliant transfers can occur.

6. Risk Monitoring

We add real-world data awareness through oracles and monitoring services. External trade events are ingested in real time. Smart contracts respond automatically to risk signals, helping banks proactively manage exposure.

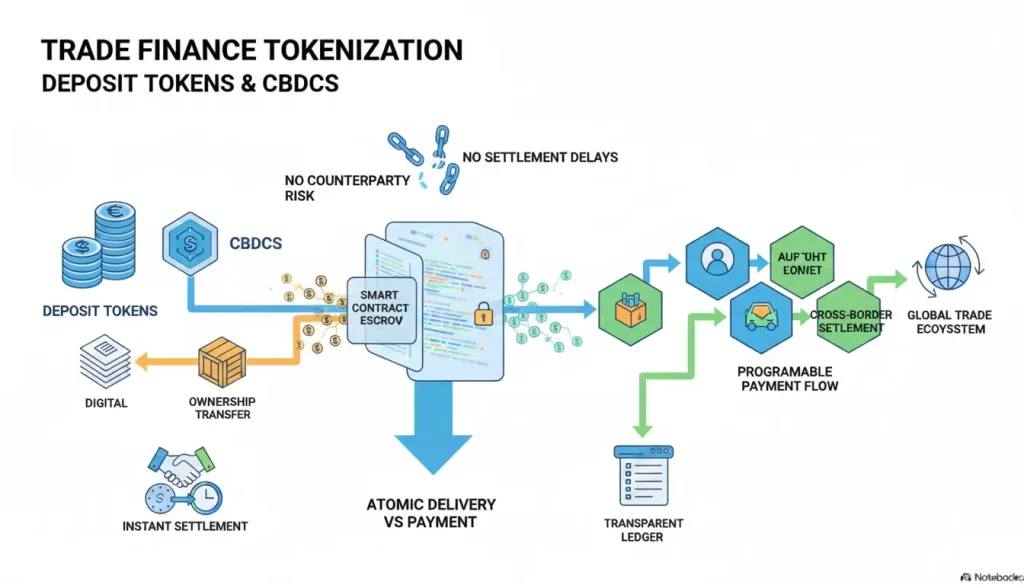

What Role Do Deposit Tokens or CBDCs Play in Trade Finance Tokenization?

Deposit tokens and CBDCs may close the gap between trade documents and actual payments by enabling on-chain settlement that occurs simultaneously with ownership changes. They can enable banks to settle trades instantly and verifiably, potentially reducing counterparty risk and trapped liquidity.

What Are They? The Digital Money Spectrum

First, let’s clarify the players.

| Digital Currency Type | Issuer | Backing | Primary Role in Trade |

| Commercial Bank Deposit Tokens | Commercial Banks | Bank deposits are one-to-one fiat | Institutional settlement between known counterparties |

| Wholesale CBDCs | Central Banks | Sovereign currency | Interbank settlement and cross-border interoperability |

| Regulated Stablecoins | Non-bank entities | Fiat reserves or collateral | Bridge currency and secondary market liquidity |

For banks, deposit tokens such as bank-issued digital money and wholesale CBDCs represent the institutional-grade digital cash required for programmable finance.

The Three Revolutionary Roles in Tokenized Trade

1. Enabling Atomic Delivery vs. Payment DvP

This is the single most transformative function.

The Traditional Problem

A bank releases payment after receiving and manually verifying paper documents, a process that takes days. During this gap, both parties carry risk. The seller risks non-payment, while the buyer risks non-delivery.

The Tokenized Solution with Deposit Tokens

When a tokenized Bill of Lading representing goods is transferred on-chain, a smart contract simultaneously transfers the corresponding deposit tokens representing money. This occurs in a single atomic transaction. Either both legs execute perfectly, or the entire transaction reverts.

Take HSBC’s Orion platform, which tokenizes gold bars. When ownership of a digital gold token is transferred between institutions, the corresponding blockchain-based digital cash settles instantly.

The same atomic DvP principle is now being applied to trade finance assets, enabling a tokenized soybean shipment to be exchanged for digital dollars in a single irreversible click.

2. Creating Programmable, Smart Money

Deposit tokens are not just digital dollars. They are money with embedded intelligence.

How It Works

When integrated with trade finance smart contracts, these tokens become conditional.

- They can be locked in escrow by smart contracts until specific conditions are met, such as the arrival of goods or the verification of certificates.

- They can auto-release when IoT sensors confirm shipment delivery.

- They can split and route automatically, sending partial payments to suppliers, logistics providers, and insurers based on predefined rules.

J.P. Morgan’s Onyx uses its deposit token to enable programmable escrow in trade finance. In pilots with large corporates, smart contracts automatically release payments when blockchain-verified shipping milestones are reached. This turns static money into an active participant in trade execution.

3. Unlocking Cross-Border Interoperability

International trade’s biggest friction point is currency conversion and correspondent banking.

The CBDC Vision

If Bank A in the US uses a digital dollar and Bank B in Singapore uses a digital Singapore dollar, they could settle directly via programmable FX smart contracts or through multi-CBDC platforms such as Project mBridge.

The Immediate Reality with Deposit Tokens

Major global banks issuing their own deposit tokens can create direct settlement corridors. Instead of money flowing through three to five correspondent banks, each adding fees and delays, it moves directly between the trading parties’ banks on a shared ledger.

The Strategic Advantages for Banks

For Treasury and Liquidity Management

- Real-time visibility. Treasury teams can see settlement positions instantly rather than at T+2.

- Reduced nostro accounts. Less capital remains trapped in pre funded foreign currency accounts.

- Twenty-four-seven settlement. Money moves outside traditional banking hours, accelerating capital turnover.

For Risk Management

- Zero settlement risk. Atomic DvP eliminates Herstatt Risk, where one party performs while the other defaults.

- Transparent audit trails. Every transaction is immutable and time-stamped, simplifying compliance and dispute resolution.

- Reduced fraud. Programmable money moves only according to verified conditions, not manual or fraudulent instructions.

For Business Development

- New products. Banks can offer instant trade settlement as a premium service.

- Competitive edge. Early movers attract clients frustrated by traditional settlement delays.

- Secondary markets. Tokenized trade assets settled with digital cash appeal to institutional investors seeking yield with transparency.

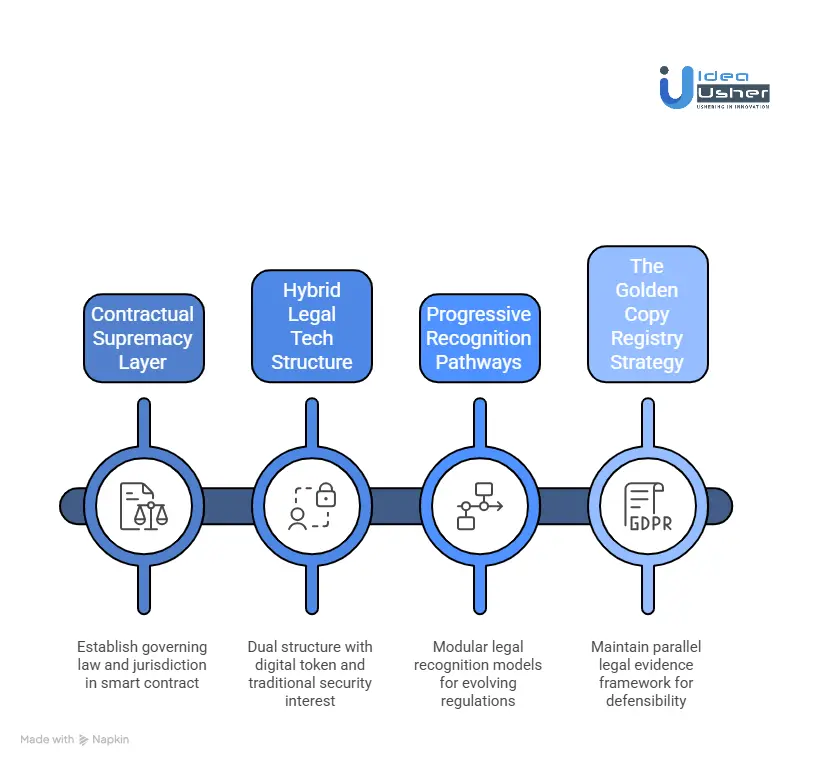

What Happens if a Jurisdiction Does Not Yet Recognize MLETR?

The MLETR or Model Law on Electronic Transferable Records is widely regarded as the legal gold standard for recognizing electronic trade documents as legally “possessable” instruments.

However, if a jurisdiction does not yet recognize MLETR, tokenization can still operate through contract-led structures rather than pure legal possession. Banks can rely on governing law clauses and SPV-based wrappers to preserve enforceability across borders.

1. Contractual Supremacy Layer

Before any token is minted, the platform establishes a governing law and jurisdiction clause in the smart contract framework, typically designating an MLETR-adopted or digitally progressive jurisdiction.

How it works

- All participants sign a multi-party electronic agreement that explicitly recognizes the digital token as representing rights to the underlying asset.

- The agreement includes choice-of-law provisions selecting a favorable jurisdiction, commonly English or New York law, both of which are increasingly supportive of digital asset enforcement.

- Arbitration clauses designate a forum, such as the ICC or SIAC, with experience in cross-border digital commerce disputes.

2. Hybrid Legal Tech Structure

Where direct legal recognition of token possession is absent, platforms adopt a dual structure model.

Digital Token (On-Chain) + Traditional Security Interest (Off-Chain)

The token represents a beneficial interest or claim against a special purpose vehicle (SPV) that legally holds the asset.

- The SPV, established in an MLETR jurisdiction, becomes the legal holder of the trade document.

- Token holders have contractual rights to the SPV’s assets.

- This structure is familiar to capital markets (similar to depositary receipts) and provides legal comfort to conservative institutions.

3. Progressive Recognition Pathways

Platforms design modular legal recognition models that can evolve as local regulations mature.

| Jurisdictional Status | Platform Approach | Example Mechanism |

| MLETR Adopted | Full token possession | Direct on-chain transfer of electronic bill of lading tokens |

| Digital Friendly (No MLETR) | Contractual tokenization | Smart contracts combined with enforceable electronic signatures |

| Conservative or Paper-Based | Hybrid wrapper model | Token represents SPV interest with physical document escrow |

This flexibility allows the same platform to operate seamlessly across multiple legal environments.

4. The Golden Copy Registry Strategy

To maximize legal defensibility, leading platforms maintain a parallel legal evidence framework.

- Every token transfer generates timestamped and cryptographically signed legal attestations.

- These records act as digital witnesses that may be admissible in traditional court proceedings.

- The system preserves parallel documentation that meets both legacy paper requirements and modern digital workflows.

A strong example of this approach is HSBC’s trade digitization strategy. By concentrating first on the Hong Kong Singapore trade corridor, two jurisdictions actively supporting digital trade, they created real market usage before global rollout.

Participation from major corporates helped establish operational precedent, which is now influencing regulatory thinking in connected markets such as India and Vietnam. This network-first strategy often accelerates legislative change faster than policy advocacy alone.

Top 5 Trade Finance Tokenization Platforms for Banks

We researched how banks are using tokenization in trade finance today. What stood out was a small group of platforms that could effectively combine compliance, distribution, and real asset structuring.

1. Tradeteq

Tradeteq is a specialist platform built specifically for trade finance distribution and tokenization. It allows banks and lenders to structure trade finance assets into regulated, tokenized instruments accessible to institutional investors, with live deployments on the XDC Network expanding liquidity beyond traditional balance sheets.

2. Taurus

Taurus provides enterprise-grade digital asset infrastructure through its Taurus-CAPITAL tokenization platform. Banks use it for compliant issuance, custody, and distribution of tokenized assets, with real trade finance transactions already executed on its regulated TDX marketplace.

3. Securitize

Securitize is an institutional tokenization platform widely adopted for compliant real-world asset issuance. Although broader than trade finance alone, banks use their regulatory framework to tokenize debt instruments, receivables, and similar assets, providing built-in compliance and secondary-market access.

4. TradeFinex

TradeFinex is an ecosystem initiative exploring blockchain-native trade finance use cases, including tokenized Letters of Credit and supply-chain financing. It aims to improve working capital liquidity by connecting decentralized technologies with traditional trade documentation and financing models.

5. Komgo

Komgo is a blockchain platform that digitizes trade finance documentation and workflows for banks and corporates. While document-centric, it provides a token-ready foundation by standardizing data, identities, and approvals across commodity and trade finance transactions.

Conclusion

Trade finance tokenization is not about replacing banks, but about rebuilding the infrastructure they rely on every day. When legal logic, technical controls, and operations are designed correctly, trade documents can become programmable assets that may move faster and settle with more certainty. Platforms that take this seriously will quietly shape the next phase of global trade finance. For enterprises and platform owners, this moment should be seen as a practical opportunity to modernize systems that are otherwise slow and capital-locked.

Looking to Develop a Trade Finance Tokenization Platform?

IdeaUsher can help you design a bank-grade trade finance tokenization platform by starting with legal and regulatory alignment first. The team may build a permissioned architecture that integrates with existing banking systems and preserves legal ownership of trade documents.

Why partner with us?

- 500,000+ hours of coding experience led by ex-MAANG and FAANG developers

- End-to-end solutions from smart contracts to secure and scalable infrastructure

- A strong focus on legal tech synchronization that ensures tokens remain enforceable and fraud-proof

- Built for real-world use with fractionalization, instant settlements, and seamless ISO 20022 integration

See how we have delivered for global clients. Explore our latest projects and let us build what comes next.

FAQs

A1: A trade finance tokenization platform should start with legal structuring before any technical build begins. Trade documents must be digitized in a way that preserves legal possession under frameworks like MLETR. The platform can then add a permissioned ledger with identity checks and document control logic. This approach allows banks to adopt it gradually without breaking existing workflows.

A2: The cost may vary widely depending on the depth of compliance and the scope of integration. A basic pilot could start in the mid-six-figure range, while enterprise-grade platforms usually cost more. Legal design and regulatory alignment often consume a large share of the budget. Ongoing costs should also be expected for audits and system maintenance.

A3: Core features usually include digital document issuance and controlled transfer of possession. Identity verification and permissioned access are essential for regulated participants. The platform should also support settlement automation and audit visibility. These features together ensure trust and enforceability.

A4: Platforms typically earn revenue across the transaction lifecycle. Fees may be charged for document origination and settlement execution. Subscription access for banks and corporates is also common. Some platforms could later add compliant secondary transfer services.