(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Crypto markets do not slow down for support tickets or manual reviews, and many users have already paid that price. When prices move fast, platforms that rely on people or delayed systems may simply react too late. That is why more users are shifting toward non-custodial crypto lending apps today.

These systems eliminate intermediaries and operate solely through smart contracts with transparent rules visible on the blockchain. Collateral health is monitored continuously, while interest accrual and repayments are calculated automatically. This approach better protects lenders and borrowers because execution occurs instantly and balances remain verifiable at all times.

Over the years, we’ve built numerous non-custodial crypto lending solutions, powered by smart contract-based risk logics and decentralized price oracle systems. Given our expertise, we’re sharing this blog to break down the steps involved in developing a non-custodial crypto lending app with automated liquidations.

Key Market Takeaways for Crypto Lending Apps

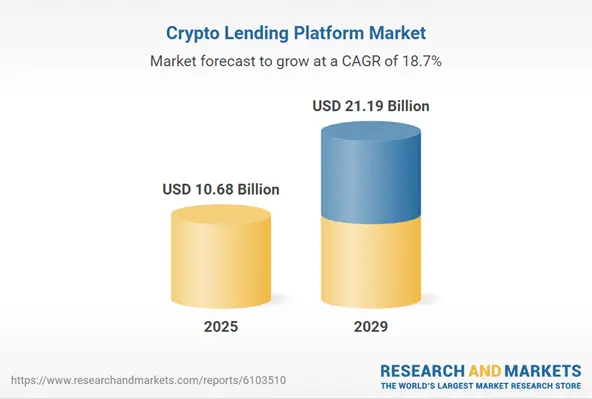

According to Research And Markets, the non-custodial crypto lending market is scaling quickly, growing from $9.03 billion in 2024 to $10.74 billion in 2025, reflecting a 19.0% CAGR. This growth is being driven by deeper DeFi adoption, rising retail participation, and a clear preference for accessing liquidity without selling long-term crypto holdings. In contrast to centralized platforms, non-custodial apps rely on smart contracts, allowing users to retain full control of assets and reduce counterparty risk.

Source: Research And Markets

Trust dynamics have played a major role in this shift. On-chain lending TVL reached $19.1 billion by late 2024, marking a 959% rebound from 2022 lows, as users moved away from custodial failures such as Celsius and BlockFi. Non-custodial platforms now account for over 20% of Ethereum lending activity, with capital efficiency exceeding 90% through optimized peer-to-peer and pooled liquidity models.

At the protocol level, Aave remains the market leader, holding around 51.5% share and nearly $33 billion in TVL, while enabling cross-chain borrowing through fully non-custodial liquidity pools. Morpho has emerged as a fast-growing alternative since 2024, reaching $6–7 billion in TVL by offering isolated vaults with competitive single-asset rates and reduced risk exposure.

In parallel, enterprise-focused moves such as the March 2025 partnership between C2 Blockchain and CoinEdge highlight how non-custodial lending is expanding beyond DeFi natives into structured retail and institutional crypto loan products.

What Is a Non-Custodial Crypto Lending App?

A non-custodial crypto lending app is a decentralized platform where users lend or borrow crypto directly via smart contracts, retaining full control of their funds at all times. The protocol never holds user assets or private keys. All lending interest rates, collateral rules, and liquidation logic are enforced transparently on chain without relying on any central authority.

How It Differs From Custodial & Semi-Custodial Lending?

The distinction between non-custodial and other lending models is not only technical. It is also philosophical and operational, shaping how risk, trust, and control are handled.

Non-Custodial vs. Custodial Lending

| Aspect | Non-Custodial Model | Traditional Custodial Model |

| Control | You control your keys at all times | You surrender keys to the platform |

| Trust Assumption | Trust code rather than companies | Trust the company’s security and integrity |

| Transparency | All rules are visible on the chain | Internal processes remain opaque |

| Insolvency Risk | Your funds are not platform liabilities | Your funds are at risk if the platform fails |

| Examples | Aave, Compound | BlockFi, Celsius (pre-collapse) |

The Semi-Custodial Middle Ground

Some platforms adopt a hybrid approach, holding certain assets while allowing others to remain in self-custody. This introduces complexity without eliminating core custodial risks. If a platform controls any portion of user assets, it remains exposed to its operational and financial risks.

Why Automation Matters More Than Ever

Automated liquidations represent more than convenience. They form the foundation of effective on-chain risk management.

- No Human Bias: Algorithms do not become emotional, fatigued, or conflicted.

- 24/7/365 Operation: Markets operate continuously and smart contracts enforce rules without interruption.

- Consistent Execution: Every position follows the same parameters regardless of size or user identity.

- Immediate Response: Rapid execution is critical when markets move sharply.

Real-World Implications

The 2022 lending platform collapses highlighted structural weaknesses in custodial models. Many custodial platforms failed because:

- They promised high yields without sustainable mechanisms.

- They commingled user funds.

- They made discretionary investment decisions using customer assets.

- They lacked transparent and enforceable risk management systems.

Non-custodial protocols such as Aave and Compound endured the same market stress because automated liquidation systems preserved solvency. There were no boardroom decisions or emergency interventions. The code executed predefined rules exactly as designed.

How Crypto Lending Apps with Automated Liquidations Work?

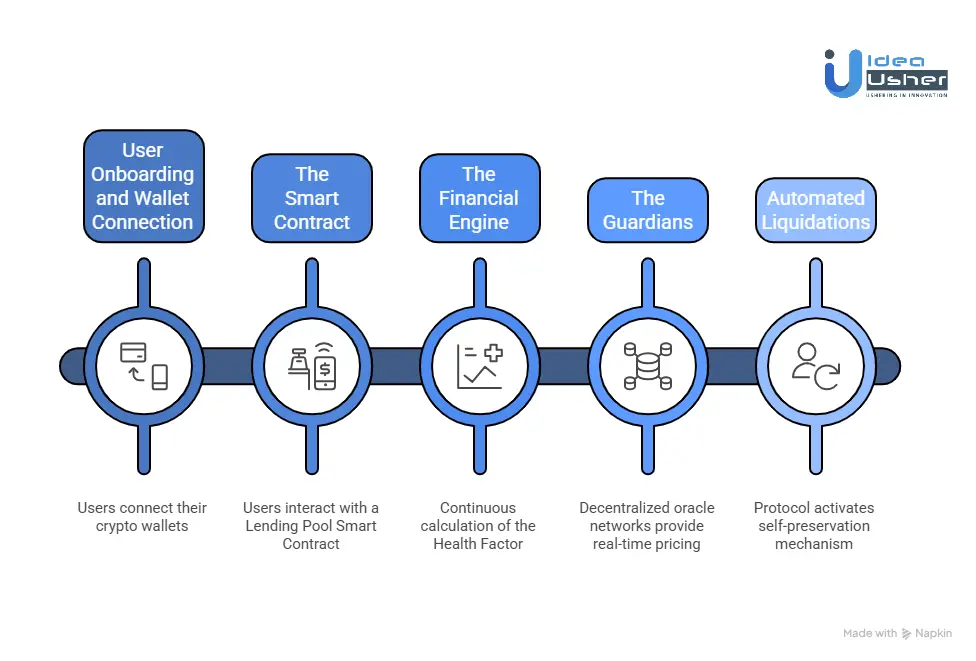

A non-custodial lending app enables users to connect their wallets and interact directly with smart contracts while maintaining full control. Collateral values are continuously monitored using decentralized price feeds, and the system may recalculate risk using a health factor.

1. User Onboarding and Wallet Connection

It begins with self-sovereignty. Users connect their personal crypto wallet, such as MetaMask, Phantom, or a hardware wallet, to the lending platform interface.

Critical Point: At no stage does the user deposit funds into a platform-controlled account. Instead, the user grants a smart contract permission to temporarily manage specific assets. Private keys and ultimate control never leave the user’s possession.

2. The Smart Contract

Once connected, users interact with a Lending Pool Smart Contract. This contract functions as an autonomous and incorruptible vault governed by publicly auditable rules.

For Lenders:

Users supply assets into the contract. In return, they receive a liquid representative token such as aTokens in Aave or cTokens in Compound. These tokens accrue interest continuously and can be redeemed at any time for the underlying asset plus earned interest.

For Borrowers:

Borrowers deposit collateral into the contract first. The protocol then allows borrowing of a different asset up to a predefined percentage of the collateral value. This limit is defined by the Loan-to-Value ratio.

3. The Financial Engine

Automation uses a continuous calculation, the Health Factor, for every borrower.

Health Factor = (Total Collateral Value × Liquidation Threshold) ÷ Total Borrowed Value

Example:

- Alice deposits 1 ETH as collateral, valued at $ 3,000.

- The liquidation threshold for ETH is 80 percent.

- The maximum LTV allowed is 75 percent.

- She borrows 2,000 USDC.

- Her Health Factor equals (3,000 × 0.80) ÷ 2,000 = 1.2.

The Golden Rule: If the Health Factor falls below 1, the position becomes eligible for liquidation.

4. The Guardians

Health Factor accuracy depends on real-time pricing. This data is provided by decentralized oracle networks such as Chainlink and Pyth.

These networks aggregate prices from multiple exchanges and deliver tamper-resistant market data to the smart contract. This ensures that collateral valuations reflect actual market conditions rather than relying on a single data source.

5. Automated Liquidations

When the Health Factor drops below 1, the protocol automatically activates its self-preservation mechanism.

Step A: Detection

The smart contract continuously monitors all positions using oracle data. The moment a position crosses below the threshold, it is flagged.

Step B: Auction and Incentive

The protocol offers a liquidation bonus, typically between 5 and 10 percent, to independent participants known as liquidators or keeper bots. This incentive ensures rapid resolution.

Step C: Atomic Execution

A liquidator submits a single transaction that performs all actions atomically:

- Repays part or all of the borrower’s debt using their own capital or a flash loan.

- Receives collateral at a discounted rate relative to market value.

- Optionally sells the collateral on a decentralized exchange to lock in profit and repay any flash loan.

The Atomic Guarantee: If any part of this transaction fails, the entire transaction reverts. The protocol is never left in a partially resolved or insolvent state.

Step D: Position Resolution

The borrower’s debt is reduced or fully cleared. Any remaining collateral is unlocked. The protocol returns to a fully collateralized state, and systemic solvency is preserved without manual intervention.

How to Develop a Non-Custodial Crypto Lending App?

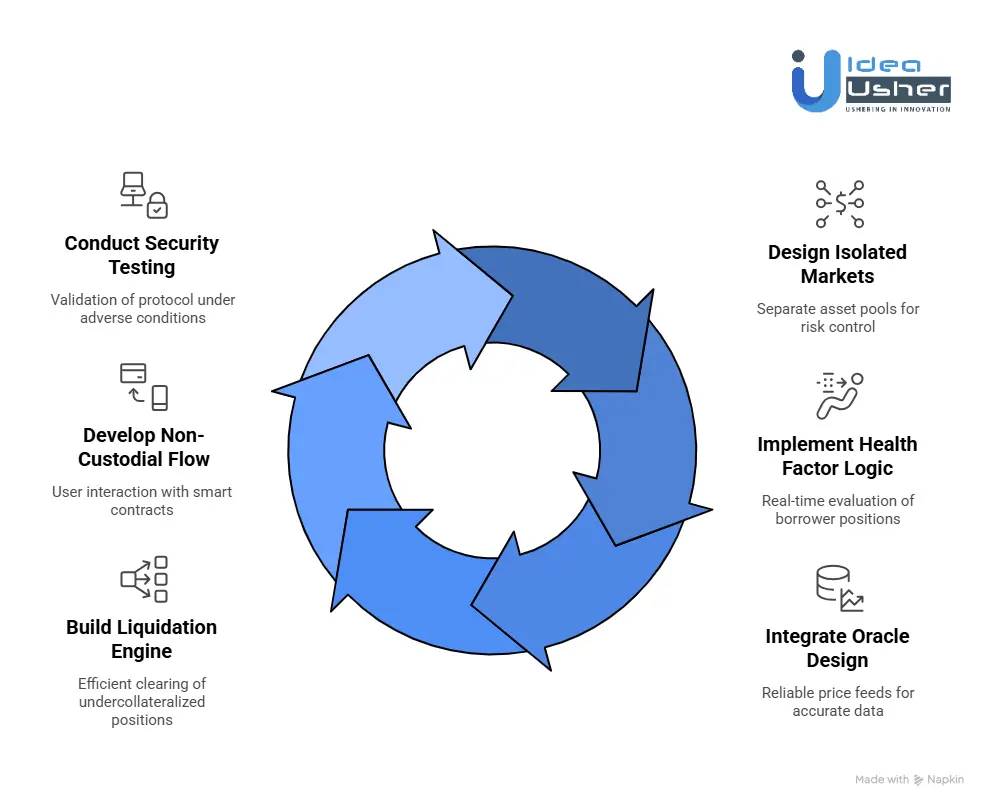

Developing a non-custodial crypto lending app starts with smart contracts that hold the rules, not the funds, and automatically enforce risk. The system should separate lending markets and rely on real-time price feeds so positions may adjust safely as prices move.

We have delivered several non-custodial crypto lending apps, and the process below reflects how we build them in practice.

1. Isolated Markets

We design isolated lending pools so each asset market is ring-fenced from others. High-volatility assets are separated from stable or highly liquid assets, which prevents cascading failures during sharp price movements. This structure allows precise risk control without compromising the rest of the protocol.

2. Health Factor Logic

We implement a health factor model that continuously evaluates borrower positions in real time. Asset-specific LTVs, liquidation thresholds, and penalties are calibrated based on volatility and liquidity behavior. This ensures liquidations occur decisively when required while avoiding premature position closures.

3. Oracle Design

We integrate multiple price feeds into an aggregated oracle layer to reduce manipulation and downtime risk. Freshness checks, deviation filters, and fallback pricing logic are built in to reject unreliable data. This keeps borrowing limits and liquidations aligned with real market conditions.

4. Liquidation Engine

We build atomic liquidation flows that are compatible with flash loans and third-party bots. Liquidator incentives are structured to encourage rapid participation without protocol intervention. This ensures undercollateralized positions are cleared efficiently and consistently.

5. Non-Custodial Flow

We develop a frontend that enables users to interact directly with smart contracts via self-custody wallets. All actions are signed on-chain, and the platform never holds any assets or private keys. This maintains decentralization while giving users full control over their funds.

6. Security Testing

We conduct comprehensive audits, simulations, and stress tests before deployment. Extreme volatility, oracle failures, and cascading liquidation scenarios are actively modeled. These tests validate that the protocol remains solvent and predictable under adverse conditions.

Can Automated Liquidations Hold Up in Black Swan Events?

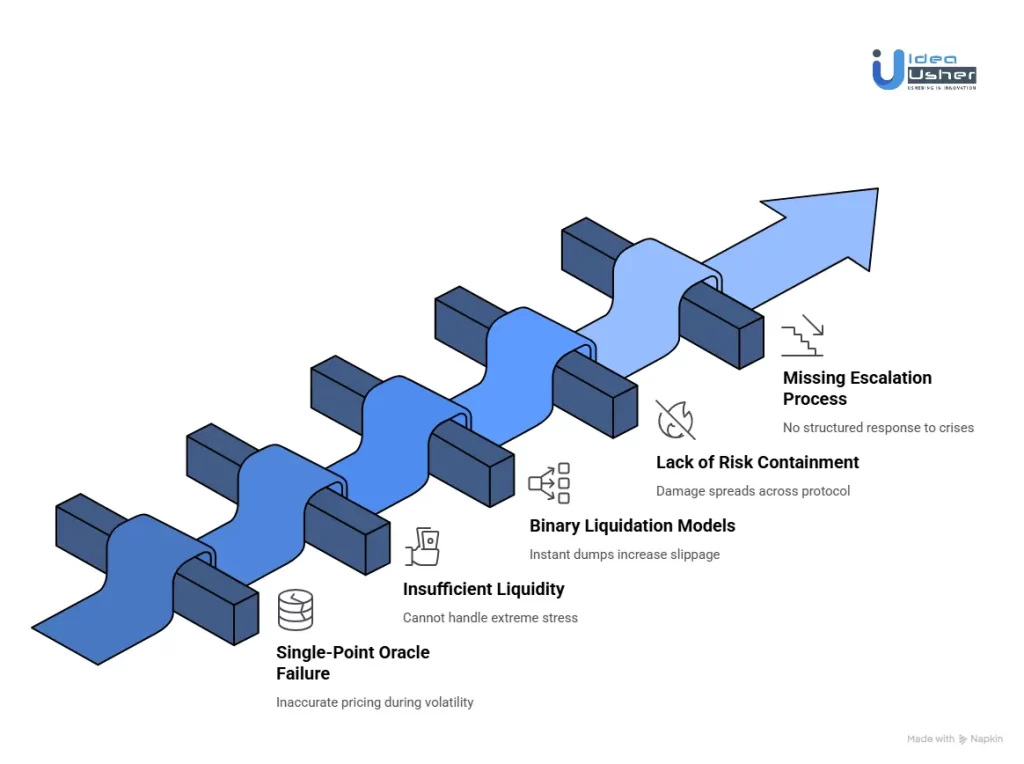

The short answer is yes, but only if they are designed for failure from day one. Automated liquidations are typically engineered for normal volatility. Black swan events like the 2022 LUNA collapse or the 2020 COVID crash expose whether a protocol has truly antifragile architecture. Two real-world case studies clearly show what works and what fails.

The Anatomy of a Black Swan Failure

Case Study 1: The Terra LUNA Collapse

In May 2022, UST lost its dollar peg, triggering a rapid death spiral for LUNA. Prices collapsed by more than 99.9 percent within days.

Take Venus Protocol on BSC as an example. The protocol had significant LUNA exposure. As prices collapsed, its oracle system relied on a single price feed from Chainlink and could not keep up with the speed of the decline.

The reported price lagged far behind real market prices. Borrowers were able to continue borrowing against LUNA collateral valued at $50, even though the market price was closer to $2. This mismatch resulted in more than $13 million in bad debt that continues to impact the protocol treasury.

The lesson: A single-point oracle failure during extreme volatility creates dangerous windows in which the protocol operates on inaccurate pricing rather than reality.

Case Study 2: The March 2020 COVID Crash

In March 2020, ETH fell by roughly fifty percent in twenty-four hours. Gas prices increased by nearly ten times as panic spread across the network.

MakerDAO provides a useful contrast. While it faced serious challenges and came close to triggering an emergency shutdown, its architecture ultimately held. The key difference was its multi collateral design and decentralized oracle network.

The protocol incurred roughly four million dollars in bad debt due to undercollateralized vaults. This was later recapitalized through MKR token auctions. Emergency pause mechanisms and rapid governance response allowed the system to recover without total failure.

The contrast: Many smaller lending protocols that day used similar liquidation logic but lacked Maker’s liquidity depth and collateral diversity. Several became permanently insolvent, resulting in lender losses.

The Solution Stack

1. Oracle Architecture

Modern protocols now implement safeguards that the LUNA collapse made unavoidable.

- Multi-source price aggregation: Using Chainlink, Pyth, API3, and time-weighted average prices from at least three major decentralized exchanges

- Volatility-based frequency: Price updates every sixty seconds in normal conditions and every ten seconds when price movement exceeds five percent

- Functional circuit breakers: Automatic freezes when price deviations exceed twenty-five percent within one hour, preventing delayed pricing scenarios

2. Liquidity Solutions

Protocols now account for extreme-liquidity-stress scenarios.

- Protocol-controlled reserve assets: Two to five percent of total value locked held in stablecoins to act as internal market liquidity

- Gradual Dutch auctions: Liquidations executed over two to four hours instead of instant market dumps, reducing slippage during panic

- Cross-chain liquidation bots: Liquidators capable of executing on Layer 2 networks or alternate chains when Ethereum mainnet fees spike

3. The Soft Liquidation Innovation

The most significant evolution since these crises has been the shift away from binary liquidation models.

- MakerDAO post-crisis changes: Introduction of more gradual liquidation mechanisms

- Modern protocols like Euler: Use tiered health factors and dynamic interest rate adjustments during volatility

- Our approach at Idea Usher: Pre-liquidation warning systems trigger at a health factor of 1.2, giving users hours to act instead of seconds

The Institutional Grade Architecture Difference

Aave provides a strong example of systemic risk containment.

Aave V3 introduced isolation mode after lessons from 2022. New assets can be listed with strict borrowing caps and isolated risk pools.

If another LUNA-type event occurs, the damage remains contained instead of spreading across the entire protocol.

Compound offers another perspective.

During the USDC depeg in March 2023, Compound governance passed emergency proposals within hours to adjust collateral factors and protect lenders. This structured escalation process proved critical and was missing from many failed protocols.

Keeping Liquidation Incentives Fair During Volatility

Liquidation incentives stay fair when the protocol rewards work that genuinely protects solvency rather than activity that exploits distressed users. A balanced bonus that covers gas costs and adds a small premium may create competition without inviting aggressive liquidators.

The Traditional Flaw

Early DeFi protocols used fixed liquidation bonuses, typically 5 to 10 percent. This created three predatory patterns.

- MEV Front-Running: Bots paid exorbitant gas fees to secure first-in-line positions, making liquidations unprofitable for smaller participants.

- Oracle Manipulation: Sophisticated actors briefly manipulated Oracle prices to trigger unnecessary liquidations.

- Over-Liquidation: Liquidators repaid the minimum debt to maximize their bonus-to-gas ratio, leaving borrowers with multiple partial liquidations and extremely high gas fees.

The result was predictable. Borrowers felt hunted, and the protocol earned a reputation for being user-hostile.

The solution stack focuses on designing incentives that reward real risk mitigation rather than speed or exploitation. Each mechanism is engineered to align liquidator profit with protocol solvency and borrower fairness.

1. Dynamic Bonus Scaling

Instead of a flat percentage, modern protocols use slippage-aware dynamic bonuses.

How it works

- Small positions in liquid assets receive a 3 to 5 percent bonus

- Large positions or illiquid collateral receive an 8 to 12 percent bonus

- Real-time adjustment occurs based on DEX liquidity depth

Example: Liquidating a 10 million dollar ETH position requires moving markets. The protocol automatically estimates expected slippage and applies a sufficient bonus to ensure profitability without overpaying.

2. Time-Based Dutch Auction Liquidations

This approach eliminates the first-come, first-served race entirely.

The process

- When a position becomes undercollateralized, it enters a liquidation auction

- The bonus starts high, for example, 15 percent, and decreases linearly over 1 to 4 hours

- The first liquidator willing to accept the current bonus executes the liquidation

- If no bids occur, the protocol treasury steps in as liquidator

The result

This approach eliminates gas wars entirely, allows the market to naturally determine the true cost of liquidation, and gives borrowers meaningful time to add collateral or stabilize their position before further action.

Take MakerDAO as an example. Its Dutch auction liquidations sell collateral gradually rather than instantly, reducing fire-sale risk and improving price discovery. Any surplus after debt repayment is returned to the vault owner, keeping liquidations fair for both the protocol and the user.

3. Partial Liquidation Caps & Cooldown Periods

To prevent repeated rapid liquidations on the same position, protocols enforce structural limits.

Implementation

- A maximum of 50 percent of a position can be liquidated at once

- A one-hour cooldown applies before further liquidation on the same position

- Collateral unwinds gradually instead of collapsing in a single event

User benefit: Borrowers gain breathing room to respond to volatility without immediate total loss.

4. Oracle Safeguards & Manipulation Resistance

Predatory liquidations often exploit oracle weaknesses. Modern systems address this by adding layered safeguards that reduce the impact of short-term price manipulation.

These include multi-source oracle aggregation, 30-minute time-weighted average pricing, circuit breakers for extreme moves, and confidence bands around reported prices.

5. Protocol Owned Insurance Fund and Backstop

Protocols no longer rely solely on external liquidators to maintain solvency. Instead, a portion of protocol fees is continuously routed into an insurance fund that acts as a financial backstop.

If third-party liquidators do not step in, the protocol treasury conducts the liquidation directly, and any excess profits beyond the fair bonus are recycled into the insurance fund. This structure helps preserve solvency even during black swan events.

The Fairness Matrix: Balancing Stakeholder Interests

| Stakeholder | Traditional Model Pain Points | Modern Fair Solutions |

| Borrowers | Surprise wipeouts, repeated liquidations, front running | Gradual unwinding, auction windows, partial liquidation caps |

| Liquidators | Gas wars, MEV extraction, and unprofitable small positions | Dutch auctions, dynamic bonuses, predictable profitability |

| Lenders | Protocol insolvency risk during black swan events | Insurance funds, protocol backstop, diversified collateral |

| Protocol | Reputation damage, user churn, regulatory scrutiny | Transparent rules, predictable outcomes, long-term sustainability |

Case Study

Compound v3 relies on a fixed liquidation bonus in the 5 to 8 percent range with first come first served execution. While this design enables fast liquidations and protects protocol solvency, it also encourages MEV-driven gas competition, making the process efficient but often predatory for borrowers.

Most Successful Business Models for Crypto Lending Apps

Successful non-custodial lending apps usually earn from interest spreads and may also benefit from liquidation fees during volatile periods. Over time, they can quietly build value through governance tokens and selective premium services.

1. The Protocol Fee Revenue Model

The most dominant and sustainable business model in DeFi lending is the protocol-controlled interest rate spread. Platforms like Aave and Compound generate revenue by charging fees on the interest borrowers pay, creating a predictable revenue stream that scales directly with protocol usage.

How It Works

The protocol takes a small percentage, typically 10 to 30 percent, of the interest paid by borrowers before distributing the remaining yield to lenders. This is typically implemented through a reserve factor mechanism, in which a portion of interest payments is allocated to a protocol-controlled treasury or reserve pool.

Real World Example

Aave (AAVE) charges up to 30 percent reserve factor on certain stablecoin markets. In 2023, Aave generated 158.7 million USD in protocol revenue, with a significant share coming from interest rate spreads. During peak market conditions, daily revenue exceeded USD 1 million.

2. The Liquidation Fee Model

A unique revenue stream exclusive to automated lending protocols comes from liquidation penalties and incentives. When positions become undercollateralized and are liquidated, the protocol captures a portion of the liquidation bonus as revenue.

How It Works

Most protocols charge a liquidation penalty of 5-15% on liquidated positions. This penalty is split between the liquidator, as an execution incentive, and the protocol treasury, as revenue. Some protocols route these fees directly into insurance or risk funds.

Market Data and Financial Impact

- Compound applies a standard 8 percent liquidation incentive, with the protocol earning fees from liquidations based on market conditions and configuration.

- Venus Protocol charges a 10 percent liquidation penalty on most markets, with proceeds directed to its Risk Fund. By mid-2024, this fund had grown to over USD 18.7 million, strengthening protocol solvency.

Revenue Potential

During volatile periods, such as May 2022 during the Terra collapse, lending protocols generated millions of dollars in daily liquidation fees. For a well designed protocol, liquidation fees can represent 15 to 35 percent of total revenue, particularly during bear markets when liquidations are frequent.

3. The Governance Token Utility Model

Many successful lending protocols use governance token models in which token holders capture protocol value through fee sharing, staking rewards, or buyback mechanisms.

Implementation Strategies

- Fee Distribution to Stakers: Aave allows AAVE holders who stake their tokens to receive around 30 percent of protocol fees, distributed as additional tokens or ETH.

- Token Buybacks Using Revenue: MakerDAO uses protocol revenue to buy back and burn MKR tokens, creating deflationary pressure. In Q1 2024 alone, 32.8 million USD was spent on MKR buybacks.

- Revenue Governance Allocation: Compound’s COMP token holders participate in governance decisions that direct protocol revenue toward community initiatives, incentives, or ecosystem growth.

Financial Outcomes

Aave’s staking program has distributed over 45 million USD in rewards to stakers since inception, reinforcing long term participation. MakerDAO has reduced supply through buybacks, removing more than 6,500 MKR, worth roughly 20 million USD, from circulation since 2020.

Market Validation

Protocols with strong token utility models consistently achieve higher market capitalization-to-revenue ratios. Aave, supported by its fee-sharing design, trades at an estimated price-to-sales ratio of 8 to 12 times, well above traditional fintech benchmarks.

4. The Premium Services and Enterprise Model

Beyond protocol-level revenue, many lending platforms generate income through premium features, institutional products, and white-label infrastructure.

Enterprise Services Pricing

- Custom Market Creation: Permissioned pools such as Aave Arc charge setup fees ranging from USD 50,000 to 250,000, along with a 20-30% ongoing revenue share.

- White Label Lending Infrastructure: Infrastructure providers like Clearpool or Exactly Protocol charge 100,000 to 500,000 USD in licensing fees, plus 15 to 25 percent revenue share.

- API Access and Premium Data: Institutional-grade APIs typically cost USD 5,000 to 25,000 per month, with additional fees for high-throughput usage.

Case Study

Goldfinch Finance, which focuses on real-world asset lending, charges borrower onboarding fees of 1 to 3 percent of loan principal, along with ongoing servicing fees. Since launch, total originator fees on the platform have exceeded USD 25 million.

Top 5 Non-Custodial Crypto Lending Apps in the USA

We reviewed how non-custodial lending protocols behave under real market stress and what makes their liquidation systems reliable. A few platforms consistently stood out for their smart contracts, which can manage risk cleanly and fairly while preserving user control.

1. Aave

Aave is one of the most mature non-custodial lending protocols in DeFi, allowing users to supply crypto assets, earn yield, and borrow against collateral without giving up control of their private keys. It operates entirely through audited smart contracts across Ethereum and multiple Layer-2 networks, making it widely used by U.S.-based DeFi participants.

Liquidations: Positions are automatically liquidated when the health factor drops below 1. Smart contracts enable third-party liquidators to repay a portion of the debt and seize collateral when predefined liquidation thresholds are met.

2. Compound

Compound is a protocol-driven money market where interest rates adjust algorithmically in response to supply and demand. Users interact directly with on-chain contracts, and funds remain non-custodial at all times. It is often favored for its simplicity, transparency, and conservative risk parameters.

Liquidations: If a borrower’s collateral value falls below the required levels, the protocol enables automated liquidations in which liquidators repay the debt and receive collateral at a discount.

3. Morpho

Morpho improves capital efficiency by matching lenders and borrowers peer-to-peer while relying on established pools like Aave and Compound as fallback liquidity sources. This hybrid design allows better rates without changing custody or risk ownership.

Liquidations: Morpho inherits automated liquidation logic directly from the underlying protocol, meaning liquidations are triggered using Aave or Compound smart-contract rules.

4. Solend

Solend is a leading non-custodial lending protocol on Solana, designed for high-throughput and low-fee lending markets. It supports major Solana-native assets and is commonly used by U.S. DeFi users active in the Solana ecosystem.

Liquidations: Liquidations are fully automated and executed on-chain when loan-to-value limits are breached, often via rapid liquidator bots, given Solana’s low latency.

5. Silo Finance

Silo Finance introduces isolated lending markets where each asset pair operates independently, reducing systemic risk across the protocol. Users retain full custody through smart contracts while accessing more flexible, experimental collateral options.

Liquidations: Each silo has its own automated liquidation parameters, ensuring liquidations occur only within the affected market and do not spread risk across the protocol.

Conclusion

Non-custodial crypto lending apps with automated liquidation are shaping the future of decentralized credit. They may offer a practical balance between trustless security and disciplined risk control while still scaling revenue in real conditions. As institutional capital gradually increases, platforms with precise liquidation logic could quietly become the backbone of next-generation DeFi infrastructure.

Looking to Develop a Crypto Lending App With Automated Liquidations?

IdeaUsher can help build a crypto lending app where automated liquidations behave predictably during volatility. We may design risk engines and liquidation flows that should protect collateral value and maintain protocol health.

Why Build With Us?

- 500,000+ Hours of Elite Coding Experience – Our team of ex-MAANG/FAANG developers doesn’t just write code; we engineer resilient financial systems.

- Beyond Basic Forks – We implement soft liquidations, oracle fail-safes, and compliance-ready zk-KYC to make your app stand out in 2026’s institutional DeFi landscape.

- Full-Cycle Delivery – From smart contract auditing to a gas-optimized front end, we handle everything so you can focus on growth.

Explore our latest DeFi projects and see the proof in the code.

FAQs

A1: Automated liquidation can be safe during sharp market moves when the system is designed correctly. Platforms usually rely on multiple oracle feeds and atomic execution so prices update fast and actions settle in one step. Isolated pools may further limit contagion, helping contain risk during sudden volatility.

A2: Enterprises can monetize these platforms through several aligned revenue paths. Interest rate spreads and liquidation fees may generate steady income as usage grows. Dedicated institutional pools could also attract larger capital flows with predictable returns.

A3: Non-custodial design does not remove regulation, but it does change the exposure profile. By avoiding asset custody platforms reduce balance sheet risk and custody liability. Compliance layers may still be added around access reporting and jurisdictional controls.

A4: Most non-custodial lending platforms take around three to six months to build. Timelines usually depend on liquidation logic, asset variety, and chain support. More advanced oracle design and cross-chain features could slightly extend the delivery timeline.