Key Takeaways

- Digital loan origination platforms unify borrower onboarding, AI underwriting and workflow automation into one intelligent lending system.

- Core capabilities include AI document processing, automated verification, borrower portals and enterprise banking integrations.

- AI-first lending reduces approval times, lowers operational costs and improves compliance while enhancing borrower experiences.

- Scalable architecture, explainable AI and secure integrations are essential for enterprise-grade digital lending platforms.

- How Idea Usher can help you build digital loan origination platform like Blend with AI automation, enterprise integrations and secure lending infrastructure.

The competitive advantage in lending is no longer determined by who offers capital first. It is determined by who removes friction from the borrowing journey. This shift is driving demand for a digital loan origination platform like Blend, as financial institutions replace fragmented loan workflows with intelligent, end-to-end origination infrastructure that accelerates decisions without increasing operational complexity.

Traditional loan origination relied on disconnected applications, manual document reviews, and siloed underwriting. Modern lenders increasingly expect digital borrower onboarding, AI-powered document intelligence, workflow orchestration, verification hubs, intelligent underwriting, automated compliance, omnichannel lending, AI loan agents, application-to-close automation, and enterprise integrations to accelerate approvals, improve borrower experiences, and strengthen regulatory compliance.

In this blog, we’ll explore the essential features of a digital loan origination platform like Blend, covering its core capabilities, architecture, AI-driven workflows, technology stack, and how IdeaUsher can help build enterprise-grade digital lending platform for the shift toward AI-native lending operations.

Why AI-First Loan Origination Is Replacing Legacy Lending Systems

The lending industry is rapidly adopting AI-first loan origination platforms as institutions manage rising application volumes, faster credit decision expectations, and stricter regulatory requirements. With the global Loan Origination System (LOS) market projected to reach $15.43 billion by 2032, legacy platforms are struggling to keep pace.

Industry benchmarks show that AI-native lending platforms improve underwriter productivity by 20%–60%, accelerating the shift from manual, rule-based processes to intelligent, automated lending workflows.

A. Legacy Loan Origination Systems Create Operational Bottlenecks

The structural breakdown of legacy LOS infrastructure stems from a reliance on rigid, linear task routing that requires continuous human intervention. Modern credit analysts spend up to 40% of their time on non-core, administrative activities, actively restricted by architectural flaws:

- Fragmented Lending Systems: Separate document intake, identity verification, risk assessment, and core banking systems create data gaps, increase operational complexity, and raise commercial loan origination costs to an average of $3,500 per file.

- Manual Document Processing: Traditional platforms treat PDFs, tax returns, and bank statements as static files, requiring underwriters to extract 150+ data fields manually, slowing approvals.

- The 15-Day Approval Cycle: Legacy workflows keep applications in review for 12–15 business days, contributing to a 32% application abandonment rate as borrowers switch to faster lenders.

B. How AI Transforms Every Stage of the Lending Lifecycle

By inserting self-executing domain models and agentic workflows directly into the core system of record, AI-first platforms turn the entire lending lifecycle into a fluid, automated pipeline.

The transformation spans every core phase of the application lifecycle, from borrower onboarding and verification to underwriting, approvals, closing, and funding.

- Intake & Document Intelligence: The platform ingests tax returns, bank records, and financial statements, extracting data with 99.4% accuracy in under 60 seconds. If information is missing, AI agents automatically follow up via text or email, increasing application completion rates from 5% to 70%.

- Verification & AI Underwriting: The platform performs fraud checks, KYB verification, and AI-powered credit analysis using up to 10,000 borrower data points far beyond the 50–100 used in traditional scoring, helping reduce non-performing loans (NPLs) by 15%–25%.

- Workflow Orchestration & Decisioning: Applications are routed automatically while AI generates complete credit memos for lenders. This reduces decision time by 50%–75%, shortens approvals to 6–8 days, and lowers origination costs by 60% to around $1,400 per loan.

C. Why Enterprises Are Investing in Digital Loan Origination Platforms

For enterprise leaders and banking executives, consolidating workflows, integrations, compliance, and AI into a single platform offers an efficient path to scale operations without a proportional increase in headcount. Financial institutions see an average 2.3x return on investment (ROI) within 13 months of adopting agentic AI platforms.

The corporate value of moving to a unified digital origination framework is clear:

| Venture Scaling Vector | Legacy Origination Infrastructure | AI-First Unified Platforms | Direct Business & Financial Impact |

| Operational Efficiency | Manual processing and frequent data entry errors. | Hyper-automation reduces operational costs by 40%. | Improves efficiency ratios and expands operating margins. |

| Portfolio Throughput | Loan volume limited by staffing capacity. | Teams process 3×–4× more applications with the same workforce. | Accelerates portfolio growth without additional hiring. |

| Risk & Compliance | Manual underwriting creates 15%–25% decision variance. | Explainable AI provides complete audit trails and data lineage. | Strengthens compliance and reduces regulatory risk. |

| Borrower Experience | Slow, opaque workflows increase abandonment. | Mobile updates and 90% faster processing. | Improves borrower retention and competitive advantage. |

The Enterprise Takeaway: AI-native loan origination platforms replace manual, labor-intensive workflows with intelligent, automated lending operations. By accelerating approvals, reducing operational costs, and strengthening compliance, they help financial institutions build scalable, efficient lending ecosystems ready for the future of digital banking.

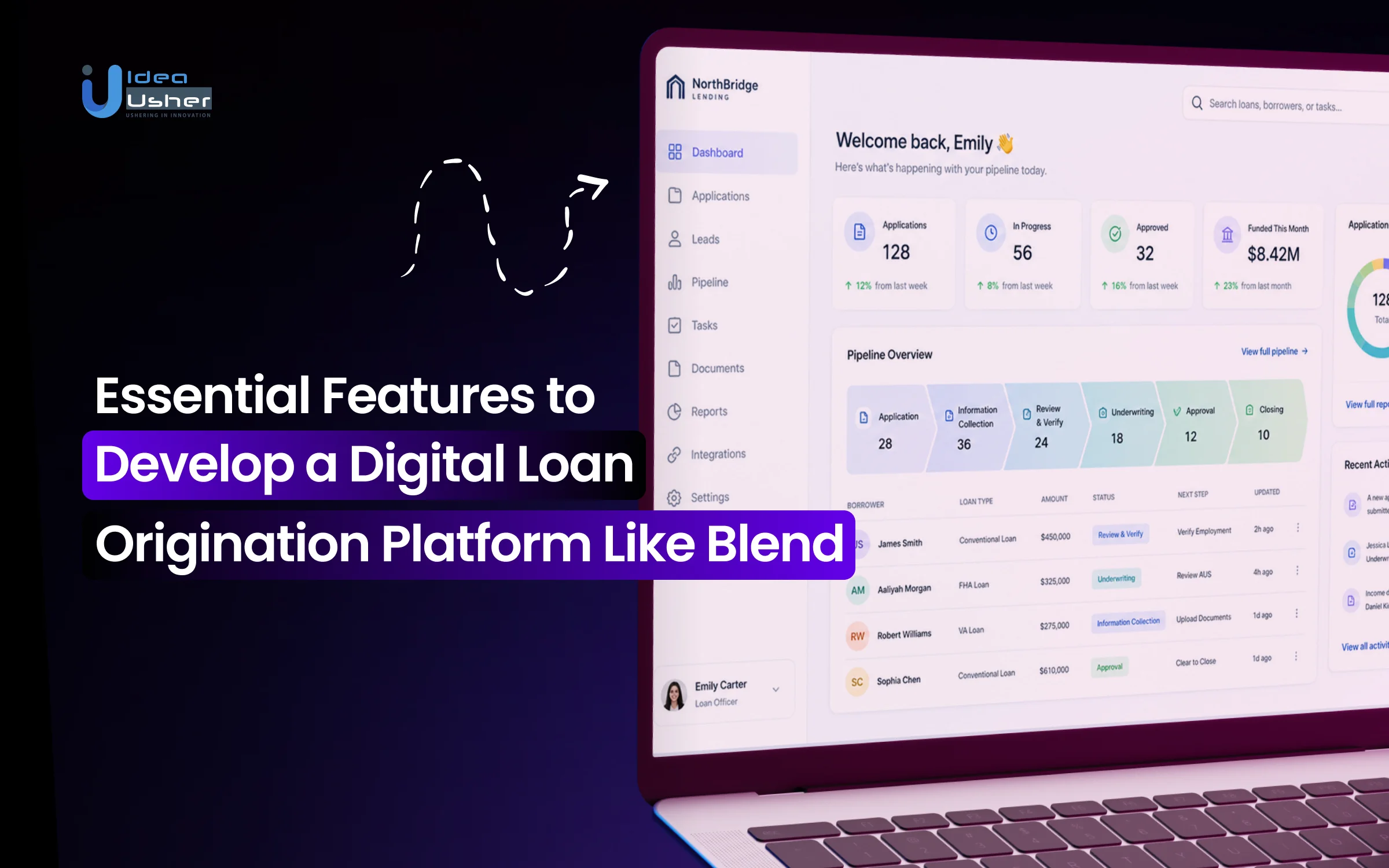

What Is a Digital Loan Origination Platform like Blend?

The digital lending industry is shifting toward unified loan origination platforms that reduce operational costs and automate lending workflows. Blend Labs (NYSE: BLND) is a leading cloud-based lending platform that supports major banks, independent mortgage banks (IMBs), and credit unions. By digitizing lending operations, it helps reduce the high costs of originating products such as mortgages (over $11,000) and HELOCs (around $2,000 in manual processing costs).

Rather than functioning as a standalone application portal, Blend serves as a digital origination infrastructure spanning mortgages, HELOCs, vehicle loans, and deposit account onboarding. With Intelligent Origination and the Autopilot MCP Server framework, it automates document collection, workflows, and decision-making, transforming lending into a connected, AI-driven banking ecosystem.

A. Intelligent Origination Instead of Traditional LOS

Traditional Loan Origination Systems (LOS) rely on rigid workflows that require teams to manually verify data, review compliance, and move documents across disconnected systems. Many lenders have added standalone AI tools, but these often increase complexity rather than reduce it.

MIT research found that while 80% of financial institutions are experimenting with AI, only 5% successfully deploy it into production. Blend solves this by embedding its Intelligent Origination engine directly into the lending workflow.

Instead of simply extracting text, Blend understands relationships across loan applications, financial documents, and lending guidelines. It automatically identifies missing information, processes unstructured PDFs, and performs rules-based data matching, reducing manual handoffs while maintaining accurate, auditable compliance.

B. How Blend Connects the Entire Lending Lifecycle

The primary operational advantage of the Blend platform is its ability to tie together a fragmented consumer journey into a smooth, single interaction loop. The lifecycle moves instantly from customer intake straight through to electronic closing.

Step 1: Intelligent Application Ingestion

The borrower initiates an application through an intuitive mobile or web layout. Blend’s dynamic questioning engine tailors the application form in real time based on user answers, expanding new digital deposit account conversions by 50%.

Step 2: Automated Financial Verification

Rather than requiring users to track down physical paperwork, Blend integrates directly with providers like Plaid and DocuSign. The system securely pulls verified payroll data, asset statements, and tax files directly from the source, cutting application submission times by 60%.

Step 3: Autopilot Processing & Condition Clearing

Lender-built AI agents running on Blend’s Autopilot MCP Server analyze incoming data arrays. The engine pulls credit profiles, evaluates asset balances against loan parameters, and flags potential fraud patterns automatically.

Step 4: Automated LOS Integration & Settlement

The verified file pushes instantly into the bank’s core LOS backend (such as Encompass or MeridianLink). This automated process saves up to 16+ hours of manual labor per loan and dramatically accelerates closing timelines.

C. Why Financial Institutions Are Adopting AI-Driven Lending

For executive teams and enterprise leaders, adopting an AI-driven lending platform provides a highly efficient path to grow loan portfolios without adding costly operational headcount. Transitioning to an intelligent platform changes origination from a slow, human-intensive chore into a scalable, high-volume software ecosystem.

The massive efficiency differences across these technological layers show why major regional banks and independent mortgage lenders are aggressively investing in Blend’s infrastructure:

| Banking Performance Vector | Legacy Manual Lending Systems | AI-Driven Blend Ecosystem | Direct Corporate Impact |

| Loan Processing Speed | Loan approvals take 20–30 days through manual workflows. | AI-driven workflows reduce closing times by 50%+. | Improves borrower retention and accelerates capital deployment. |

| Operational Efficiency | Heavy manual follow-ups and data entry. | Automation saves 16 hours per loan file. | Enables loan officers to increase loan volume by 33%. |

| Risk & Quality Control | Quality checks occur late in the process. | Continuous pre-funding quality control detects issues in real time. | Reduces compliance errors and loan defaults. |

| Application Completion | Repetitive forms and manual processes increase abandonment. | Connected data workflows boost submissions by 105%. | Improves conversion rates and lowers customer acquisition costs. |

The Enterprise Takeaway: Legacy loan origination systems can’t meet modern lending demands. AI-native platforms like Blend automate and streamline loan processing into a transparent, scalable workflow. By embedding intelligent automation across the lifecycle, financial institutions boost efficiency, enhance compliance, and deliver faster borrower experiences while protecting profitability.

How AI Processes a Loan in Lending Origination Platform

Traditional manual loan lifecycles are notoriously slow, dragging files through friction-filled human handoffs for weeks. An AI-driven Loan Origination System (LOS) collapses this timeline into a synchronized, data-driven pipeline. By running administrative, verification, and analytical tasks in parallel, AI safely reduces standard loan cycle times by 50% to 80%.

Here is how an application moves from initial digital submission to final funding under an AI architecture.

1. Application Submission

The lifecycle begins the moment a borrower interacts with the front-end consumer portal. Instead of relying on static, exhaustive forms that lead to high drop-off rates, the intake layer uses conversational and adaptive AI.

- Dynamic Form Fields: The application adapts in real time based on borrower inputs. For example, freelance applicants are prompted to upload 1099s or relevant tax documents instead of W-2s.

- Omnichannel Document Uploads: Borrowers can upload files from desktop or capture documents with a smartphone. AI-powered image validation instantly checks clarity and completeness, prompting re-uploads within 3 seconds if documents are blurred or incomplete.

2. Document Intelligence

Once submitted, the paperwork enters the Intelligent Document Processing (IDP) engine. This stage handles the heaviest historical bottleneck: reading and understanding unstructured financial data.

- Context-Aware Classification: Machine learning automatically classifies PDFs and financial documents such as utility bills, pay stubs, and tax forms with 98%+ accuracy, eliminating manual document sorting.

- Semantic Data Extraction: Combining OCR and LLMs, the platform understands document context, standardizes fields like Gross Income across different formats, and reduces manual data entry by 30%–40%.

3. Automated Verification

With the extracted data structured, the AI acts as a digital investigator, running parallel cross-checks against authoritative external databases via API loops.

- Cross-Document Validation: The platform automatically cross-checks data across applications, IDs, bank statements, pay stubs, and W-2s, identifying inconsistencies before underwriting begins.

- Fraud & Anomaly Detection: AI detects document tampering, verifies applicant information against credit bureaus, employment databases, and AML/KYC watchlists, helping prevent fraud and accelerate risk assessment.

4. AI-Assisted Underwriting

Once all data is verified, the core machine learning risk models evaluate the borrower’s long-term creditworthiness.

- Alternative Data Scoring: The underwriting engine analyzes transaction history, account balances, subscription payments, rent records, and cash-flow patterns to build a more comprehensive borrower risk profile beyond traditional FICO scores.

- AI Exception Routing: Low-risk applications that meet predefined criteria are automatically approved through Straight-Through Processing (STP), covering up to 80% of consumer loans. Applications with exceptions are routed to underwriters with AI-generated insights highlighting the specific risks requiring review.

5. Decisioning and Closing

The final stage translates the algorithmic risk score into an official credit decision and executable loan package.

- Personalized Offer Generation: Once approved, the platform generates personalized loan offers by matching the borrower’s risk profile with real-time lending criteria, optimizing loan amount, interest rate, and repayment terms.

- Instant Document Generation: The platform automatically creates loan agreements and closing documents, delivering them to the borrower’s portal for e-signature and enabling standard consumer loans to reach a closing-ready stage in under 30 minutes.

Core Features of a Blend-Like Digital Loan Origination Platform

Building a digital loan origination platform like Blend requires more than digitizing loan applications. It demands an AI-driven ecosystem that unifies borrower experiences, document intelligence, workflow automation, decisioning, enterprise integrations, and compliance into a single intelligent platform that accelerates approvals while reducing operational costs.

A. AI-Powered Digital Borrower Experience

A seamless borrower journey is the foundation of modern digital lending. This category focuses on creating intuitive, personalized, and self-service experiences that reduce application abandonment, improve customer satisfaction, and accelerate loan completion.

1. Dynamic Multi-Product Loan Applications

A unified application experience that supports mortgages, personal loans, HELOCs, auto loans, and other lending products through adaptive flows. These flows adjust questions, eligibility criteria, and required documentation based on the selected loan type, ensuring a streamlined and relevant borrower journey.

2. AI-Guided Digital Borrower Onboarding

An AI-assisted onboarding process that guides borrowers through each step of the application journey. This approach reduces confusion, minimizes incomplete submissions, and improves conversion rates through personalized recommendations and contextual assistance.

3. Omnichannel Loan Application Journey

A consistent application experience across mobile apps, web portals, branch offices, and contact centers. Borrowers can start, pause, and resume applications seamlessly while maintaining synchronized data across all channels.

4. Self-Service Borrower Portal

A secure digital portal that enables borrowers to upload documents, complete pending tasks, review loan progress, and communicate with lenders. This reduces dependency on manual interactions and enhances borrower convenience.

5. Real-Time Loan Status Tracking

Continuous visibility into loan progress through automated updates, milestone notifications, and estimated timelines. This transparency improves borrower confidence and reduces the need for support inquiries.

6. Intelligent Borrower Communication

AI-driven communication systems deliver personalized notifications, reminders, and document requests to borrowers. These intelligent interactions enhance engagement, minimize delays, and ensure applications progress smoothly toward faster and more efficient loan approvals.

As borrower experience capabilities establish a strong foundation, the next critical layer focuses on transforming raw documents into actionable insights through intelligent automation, ensuring accuracy, speed, and trust in lending decisions.

B. AI Document Intelligence and Verification

Modern lending depends on accurate data extraction and verification. AI-powered document intelligence minimizes manual processing, improves data quality, accelerates approvals, and strengthens risk management across every loan application.

1. Intelligent Document Capture and OCR

Advanced document capture capabilities combined with OCR technology digitize, classify, and process borrower documents efficiently. This approach reduces manual data entry, enhances processing speed, and improves overall accuracy in handling financial documentation.

2. AI Document Understanding

Deep document analysis powered by AI that interprets financial records, extracts key data points, and identifies missing information. This goes beyond traditional OCR by understanding document context.

3. Automated Identity Verification

Automate identity verification by validating government-issued IDs, performing biometric checks, and using facial recognition and digital authentication methods. This ensures secure borrower onboarding, reduces identity fraud risks, and enhances compliance with regulatory requirements.

4. Income, Asset, and Employment Verification

Direct integrations with payroll systems, banking networks, and financial data providers to validate borrower income, employment status, and assets. This reduces reliance on manual document collection.

5. Fraud Detection and Risk Validation

AI-driven risk analysis that detects anomalies, suspicious patterns, and potential fraud indicators across borrower data and documents before underwriting. This strengthens financial security, reduces losses, and ensures compliance with regulatory standards.

6. Cross-Document Data Validation

Automated comparison of data across borrower documents, application inputs, and third-party sources to identify inconsistencies and discrepancies. This improves data accuracy, reduces manual verification efforts, and ensures reliable information before loan approval.

With verified and structured data in place, the platform can now streamline operations through intelligent workflows, ensuring every application progresses efficiently while minimizing manual intervention and operational bottlenecks across lending processes.

C. Intelligent Loan Workflow Automation

Workflow automation enables lenders to eliminate repetitive manual tasks, improve operational efficiency, standardize lending processes, and ensure every application moves through the origination lifecycle with minimal delays.

1. AI Workflow Orchestration

An intelligent orchestration layer that routes applications, triggers actions, and prioritizes workloads based on business rules and real-time conditions. This ensures efficient process execution.

2. Automated Task Assignment

A structured task distribution system that assigns reviews, approvals, and follow-ups based on team capacity, expertise, and loan requirements. This improves operational efficiency and accountability.

3. Conditions Management

A centralized system that automatically generates, tracks, and resolves loan conditions throughout the approval lifecycle. It ensures borrowers meet all requirements, reduces manual follow-ups, and accelerates closing timelines with improved visibility and control.

4. Intelligent Follow-Up Automation

AI-powered monitoring continuously analyzes application progress to detect missing documents, stalled steps, or borrower inactivity. It triggers timely, personalized follow-ups, helping maintain momentum, reduce delays, and improve overall loan completion rates.

5. Loan Officer Productivity Workspace

A unified dashboard that brings together borrower data, documents, tasks, communication history, and AI-driven insights. It enables loan officers to prioritize work efficiently, make faster decisions, and manage multiple applications with greater accuracy and productivity.

6. Enterprise Workflow Configuration

Flexible configuration tools allow institutions to design and customize workflows, automation rules, and task routing based on business needs. This adaptability supports diverse lending processes while minimizing development effort and ensuring operational consistency across teams.

As workflows become more efficient, the next evolution introduces intelligent decisioning capabilities that enhance underwriting accuracy, automate compliance checks, and empower lenders with AI-driven insights for faster, more reliable loan approvals.

D. AI Decisioning and Intelligent Loan Agents

AI-powered decisioning transforms lending by combining intelligent recommendations, automated compliance, and autonomous loan analysis to help lenders improve accuracy, reduce turnaround times, and scale lending operations efficiently.

1. AI Underwriting Assistance

AI-supported underwriting tools that provide eligibility assessments, risk evaluations, and decision recommendations. Human underwriters retain final authority while benefiting from enhanced insights.

2. AI-Powered Loan Origination Agent

An intelligent AI agent that autonomously reviews loan applications, analyzes borrower documents, identifies missing or inconsistent data, and recommends next steps, reducing manual workload while accelerating processing and improving efficiency.

3. Automated Compliance Reviews

An AI-driven compliance system that continuously evaluates loan applications against regulatory standards, internal policies, and risk frameworks, minimizing manual intervention while ensuring consistent adherence to legal requirements and reducing the likelihood of compliance violations.

4. Intelligent Loan File Review

Advanced AI capabilities analyze complete loan files to detect inconsistencies, missing documentation, and potential approval blockers early in the process, enabling lenders to resolve issues proactively and streamline underwriting workflows for faster decision-making.

5. Explainable AI Decision Support

AI-generated recommendations include clear explanations, data insights, and reasoning, enabling lenders to understand decision logic, build trust in automation, and maintain transparency while meeting regulatory expectations for accountable and explainable lending practices.

6. Audit-Ready Decision History

A comprehensive, time-stamped record of all decisions, actions, and AI-driven recommendations ensures full traceability, supporting audits, regulatory reviews, and governance requirements while providing lenders with complete visibility into the loan origination lifecycle.

To fully operationalize intelligent decisioning, seamless integration with enterprise systems and robust security frameworks becomes essential, ensuring scalability, compliance, and reliable data exchange across the entire lending ecosystem.

E. Enterprise Integration and Security

Production-ready lending platforms must integrate seamlessly with banking ecosystems while maintaining enterprise-grade security, regulatory compliance, and scalable infrastructure that supports long-term digital transformation.

1. LOS and Core Banking Integration

Seamless integration with loan origination systems (LOS) and core banking platforms helps lenders modernize digital experiences while preserving legacy investments, ensuring data consistency, minimizing disruption, and supporting the full loan lifecycle.

2. CRM and Third-Party Data Integration

Integration with CRM systems, credit bureaus, payment providers, and financial data services creates a unified lending ecosystem, enabling enriched borrower profiles, faster decision-making, improved customer engagement, and streamlined access to critical external data sources.

3. API-First Integration Framework

A flexible API-driven architecture simplifies system connectivity, supports scalability, and enables rapid integration with new services, allowing financial institutions to adapt quickly, extend platform capabilities, and future-proof their digital lending infrastructure.

4. Enterprise Role-Based Access Control

Granular access management through defined roles, permissions, and authentication policies ensures secure handling of sensitive borrower data, reduces unauthorized access risks, and supports compliance with enterprise security and regulatory standards.

5. Regulatory Compliance Framework

Configurable compliance mechanisms in loan origination platform like blend support regulatory requirements, data privacy standards, and policy enforcement across jurisdictions, helping lenders stay audit-ready, reduce risk, and adapt to evolving regulations.

6. Lending Analytics and Performance Insights

Real-time analytics and reporting tools provide visibility into loan performance, operational efficiency, and process optimization opportunities, enabling data-driven decision-making, identifying bottlenecks, and continuously improving lending workflows and business outcomes.

Blend like Digital Loan Origination Platform Feature-Wise Development Cost

The development cost of a digital loan origination platform like Blend depends on the AI capabilities, lending workflows, enterprise integrations, compliance requirements, and platform scalability you plan to build. While an MVP focuses on digitizing borrower onboarding, document processing, and loan workflows, advanced AI decisioning, intelligent automation, and enterprise infrastructure significantly increase the overall investment.

A. Core MVP Features & Estimated Cost

An MVP focuses on building the essential capabilities required to digitize the lending journey from borrower application to loan approval. These foundational features help financial institutions launch faster, validate product-market fit, automate repetitive lending tasks, and establish a scalable origination platform before investing in advanced AI and enterprise capabilities.

| Core MVP Feature | Estimated Cost | What the Feature Includes |

| Digital Borrower Experience | $12,000 – $22,000 | Multi-product loan applications, borrower onboarding, omnichannel applications, self-service portal, and real-time loan tracking. |

| AI Document Intelligence | $10,000 – $20,000 | Document capture, OCR, AI document understanding, automated data extraction, and document validation. |

| Borrower Verification Hub | $8,000 – $15,000 | Identity verification, income verification, employment verification, asset verification, and fraud prevention. |

| Loan Workflow Automation | $10,000 – $18,000 | Workflow orchestration, task management, conditions tracking, automated follow-ups, and workflow configuration. |

| Loan Officer Workspace | $8,000 – $12,000 | Centralized dashboards, borrower management, document management, communication tools, and operational visibility. |

| Admin & Operations Dashboard | $6,000 – $10,000 | User management, reporting, workflow monitoring, lending analytics, and operational controls. |

Estimated MVP Development Cost: $80,000 – $140,000

Note: An MVP loan origination platform like blend enables lenders to launch a production-ready digital loan origination platform with essential borrower onboarding, document processing, verification, and workflow automation capabilities while establishing a strong foundation for future AI-driven lending innovation.

B. AI Intelligence Features & Estimated Cost

Once the MVP is operational, organizations typically invest in AI capabilities that automate underwriting, accelerate loan processing, improve compliance, and reduce operational costs. These intelligent features transform traditional lending into an AI-powered origination platform capable of handling high application volumes with greater accuracy and efficiency.

| AI Intelligence Feature | Estimated Cost | What the Feature Includes |

| AI Underwriting Assistance | $25,000 – $50,000 | AI eligibility assessment, risk scoring, underwriting recommendations, and decision support. |

| AI-Powered Loan Origination Agent | $30,000 – $60,000 | Autonomous loan file review, document analysis, missing information detection, and intelligent next-step recommendations. |

| AI Decisioning Engine | $25,000 – $50,000 | Automated lending decisions, policy evaluation, explainable AI, and approval recommendations. |

| Automated Compliance Reviews | $20,000 – $45,000 | Regulatory validation, lending policy enforcement, compliance automation, and audit preparation. |

| Intelligent Document Intelligence | $20,000 – $45,000 | Context-aware document interpretation, cross-document validation, anomaly detection, and structured data extraction. |

| Lending Analytics & AI Insights | $15,000 – $30,000 | Predictive analytics, operational insights, approval trends, workflow optimization, and performance reporting. |

Note: AI-powered capabilities significantly improve lending efficiency by reducing manual reviews, accelerating loan approvals, strengthening compliance, and enabling financial institutions to process more applications with fewer operational resources.

C. Enterprise Features & Estimated Cost

Enterprise lending platforms require scalable infrastructure, advanced security, regulatory compliance, and seamless integration with existing banking ecosystems. These capabilities prepare the platform for high-volume lending operations while ensuring reliability, governance, and enterprise-grade performance.

| Enterprise Feature | Estimated Cost | What the Feature Includes |

| LOS & Core Banking Integrations | $20,000 – $45,000 | Integration with existing loan origination systems, core banking platforms, and lending infrastructure. |

| CRM & Third-Party Integrations | $18,000 – $40,000 | Credit bureaus, CRM systems, payroll providers, payment gateways, and financial data providers. |

| API-First Integration Framework | $18,000 – $40,000 | Secure APIs, webhook support, middleware, and enterprise integration services. |

| Enterprise Security Framework | $25,000 – $50,000 | Encryption, role-based access control, audit logs, identity management, and secure data protection. |

| Regulatory Compliance Framework | $20,000 – $45,000 | Compliance controls, audit trails, policy enforcement, data privacy management, and regulatory reporting. |

| Infrastructure Monitoring & Analytics | $15,000 – $30,000 | Platform monitoring, operational dashboards, system health tracking, performance analytics, and uptime reporting. |

Note: Enterprise loan origination platform like blend development investments prepare the platform for banks, mortgage lenders, credit unions, and financial institutions that require secure, compliant, and highly scalable lending infrastructure capable of supporting thousands of loan applications simultaneously.

D. Estimated Budget by Platform Scale

The overall investment depends on your target market, AI maturity, compliance obligations, integration requirements, and expected transaction volume. Most organizations begin with an MVP before expanding into AI-powered enterprise lending capabilities as customer adoption grows.

| Platform Level | Estimated Cost | Key Features Included |

| MVP Platform | $80,000 – $140,000 | Digital borrower experience, AI document processing, borrower verification, workflow automation, loan officer workspace, and admin dashboard. |

| Mid-Level Platform | $140,000 – $300,000 | AI underwriting, intelligent loan agents, compliance automation, advanced integrations, analytics, and AI decision support. |

| Enterprise Platform | $300,000 – $650,000+ | Enterprise integrations, advanced AI automation, scalable infrastructure, enterprise security, regulatory compliance, intelligent analytics, and multi-region deployment. |

Note: The ideal investment depends on your lending products, regulatory landscape, integration complexity, and long-term product strategy. Many organizations launch with an MVP before expanding into enterprise-grade AI automation, advanced compliance capabilities, and intelligent lending operations.

E. Factors That Influence Development Cost

Several technical and business factors influence the overall cost of building a loan origination platform like blend, affecting scalability, integrations, compliance requirements, and the complexity of AI-driven automation and workflows.

- Loan Product Support: Supporting mortgages, personal loans, auto loans, HELOCs, and other products with unique workflows and underwriting rules adds $15,000–$40,000.

- Third-Party Data Integrations: Connecting Experian, Equifax, Plaid, Argyle, Onfido, Persona, and property valuation APIs adds $10,000–$30,000, plus ongoing usage fees.

- Document Processing Complexity: Handling W-2s, tax returns, bank statements, pay stubs, and property documents adds $10,000–$25,000 for OCR and validation workflows.

- Lender Workflow Customization: Configuring institution-specific approval workflows, underwriting rules, and business processes requires $15,000–$35,000.

- Geographic & Regulatory Coverage: Supporting multiple states or countries with varying lending regulations increases development costs by $15,000–$40,000.

- User Roles & Permissions: Building role-based access for loan officers, underwriters, processors, compliance teams, and administrators adds $10,000–$25,000.

How IdeaUsher Builds Enterprise Lending Platforms

With 11+ years of experience, 250+ specialized developers, 1,000+ successful projects across 50+ countries, and a 4.9/5 Clutch rating, IdeaUsher builds secure, scalable fintech platforms for modern lending institutions.

We design and develop custom digital loan origination platforms powered by AI-driven underwriting, automated workflow orchestration, enterprise integrations, and secure cloud infrastructure. Our solutions accelerate lending operations, simplify compliance, and help financial institutions launch enterprise-grade lending platforms at scale.

A. AI Strategy and Product Discovery

We begin by mapping out your explicit credit models and localized compliance rules to establish a highly structured project blueprint before a single line of code is written.

- Alternative Data Underwriting: We build intelligent risk models that analyze cash flow, transaction history, and other alternative financial data to assess borrowers beyond traditional credit scores.

- Intelligent Document Processing: We develop NLP and OCR pipelines that automatically extract structured data from PDFs, bank statements, and tax returns, accelerating underwriting and reducing manual reviews.

B. Custom Platform Development

We build every piece of your lending environment from the ground up, keeping high-traffic user portals cleanly separated from back-end processing engines to maintain zero-latency operations.

- Application & Decisioning Microservices: We build independent microservices that keep borrower applications, risk checks, and credit decisioning running efficiently, even during peak lending periods.

- Dynamic Condition Management: We develop self-service borrower portals with save-and-resume functionality and automated document checklists, simplifying condition tracking while reducing manual follow-ups.

C. Banking System Integrations

We hook your interface directly into traditional payment grids and modern aggregators, removing administrative bottlenecks across the entire lifecycle of the loan.

- Bi-Directional Core Banking Integration: We build secure API connectors that synchronize data between core banking systems and loan management platforms, keeping records updated automatically.

- Multi-Rail Payment & Disbursement: We integrate ACH, instant payment rails, and institutional wire networks to automate loan disbursements and repayment collections.

D. Compliance, Security, and Deployment

We insulate your operations from regulatory issues and security threats by wrapping every deployment in strict compliance guardrails.

- Automated KYC & AML Onboarding: We integrate identity verification, facial biometrics, and AML screening directly into onboarding to streamline compliance.

- Banking-Grade AES-256 Encryption: We protect sensitive financial data with AES-256 encryption for data in transit and at rest, backed by comprehensive audit trails.

- Zero Vendor Lock-In: We deliver clean, well-documented source code, giving your business full platform ownership and long-term development flexibility.

Ready to transform your lending operations with a highly secure, automated enterprise credit engine? Partner with Idea Usher’s principal fintech software architects to map your product roadmap today.

Conclusion

Digital loan origination is rapidly evolving as financial institutions prioritize AI-driven automation, faster approvals, and seamless borrower experiences. A platform like Blend demonstrates how intelligent document processing, workflow orchestration, AI-assisted decisioning, and enterprise integrations can modernize the entire lending lifecycle. Whether you’re launching a new lending solution or upgrading an existing platform, partnering with an experienced development team is essential. At IdeaUsher, we specialize in building secure, scalable, and AI-powered lending platforms tailored to your business goals, regulatory requirements, and long-term growth strategy.

FAQs

A.1. A modern loan origination platform like blend should include AI-powered borrower onboarding, document intelligence, automated verification, workflow automation, AI decision support, enterprise integrations, compliance management, and real-time analytics to streamline lending operations and improve approval efficiency.

A.2. The loan origination platform like blend development costs typically range from $100,000 to $700,000+, depending on AI capabilities, lending products, enterprise integrations, compliance requirements, platform scalability, and the level of workflow automation required.

A.3. AI accelerates document processing, automates underwriting support, detects fraud, improves compliance, reduces manual effort, and enables faster, more accurate lending decisions while enhancing operational efficiency and borrower experiences.

A.4. A production-ready loan origination platform should integrate with loan origination systems, core banking platforms, credit bureaus, identity verification providers, payroll services, CRM solutions, payment gateways, and financial data providers for seamless lending operations.