(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

For years, auto insurance models have used outdated metrics like age, gender, and credit score to determine premiums, often leaving good drivers paying higher rates. In contrast, risky drivers benefit from lower costs. This one-size-fits-all approach has left many disappointed, with premiums not reflecting their actual driving behavior. But now, the industry is experiencing a shift toward behavior-based auto insurance models like Root Insurance, which uses real-time driving data to customize rates. With technologies like smartphone apps and telematics, these platforms reward safe driving with lower premiums and provide a fairer, more personalized approach to insurance.

The market for behavior-based insurance is rapidly expanding, with a projected growth rate of over 25% annually in the coming years. The rise of connected devices, smart cars, and telematics is making it easier to collect and analyze driving data, creating a perfect storm for new players in the market. This blog will guide entrepreneurs who are interested in developing a behavior-based auto insurance model to understand the technology, opportunities, and key steps to create a successful platform. With the right strategy, you can tap into this growing market and offer a solution that resonates with modern consumers.

Key Market Takeaways of Usage-based Auto Insurance

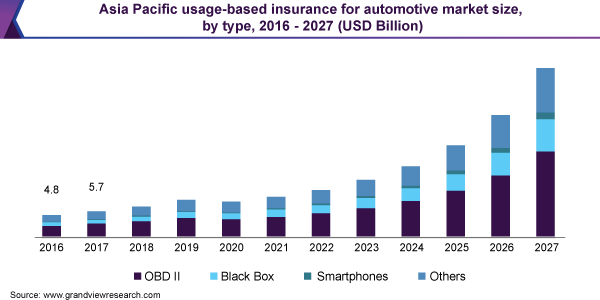

According to Grand View Research, the global usage-based insurance for the automotive market size was valued at USD 60.82 billion in 2023 and is projected to grow at a CAGR of 22.9% from 2024 to 2030. The steadily rising presence of passenger and commercial vehicles on roads has increased the risk of accidents caused by reckless or distracted driving, forcing insurance companies to launch solutions that can enforce ideal driving behavior by tracking parameters such as distance driven, time of day, and phone or media usage while driving.

Source: GrandViewResearch

Companies gain significant advantages from usage-based insurance features, including more accurate pricing, improved fraud detection, streamlined claims management, stolen vehicle recovery, and the potential reduction or elimination of towing costs. The data collected through these systems not only enhances the services offered to policyholders but also helps lower operational costs and minimize claims leakage. The rise of new companies providing innovative, tech-driven solutions has intensified competition in the market, compelling established firms to invest in advanced technologies like AI and machine learning to maintain their edge.

Overview of Behavior-Based Auto Insurance Model Root Insurance

Root Insurance provides customized rates based on each driver’s behavior behind the wheel using telematics. Through its smartphone app, it monitors driving habits to assess risk more accurately, enabling the company to offer reduced rates to safer drivers. This approach not only promotes fairer insurance pricing but also encourages responsible driving, contributing to overall road safety. By rewarding those who demonstrate safe driving habits, Root aims to reduce accidents and create a more equitable system for setting insurance premiums.

How Root Insurance Works?

Root Insurance uses telematics technology to deliver customized auto insurance rates by analyzing individual driving behaviors. Telematics allows Root Insurance to gather detailed data about driving habits through its smartphone app. Beyond telematics, it also incorporates machine learning and artificial intelligence to continuously enhance its models, allowing the company to respond to new driving trends and refine its risk assessments. Here’s how Root uses these technologies:

- Smartphone App: Root’s mobile app uses built-in sensors, such as the accelerometer, gyroscope, and GPS, to capture real-time data on driving habits.

- Data Collection: The app records several critical driving metrics, including acceleration, braking patterns, cornering, phone usage while driving, driving times, and locations.

- Data Analysis: Root employs proprietary algorithms to analyze this data, developing a unique risk profile for each driver based on observed behaviors.

- Personalized Pricing: With insights from the analysis, Root assigns personalized insurance rates, offering discounts to drivers who demonstrate safe driving practices.

Business and Revenue Model of Root Insurance

Root Insurance tracks factors like speed, braking patterns, acceleration, and phone usage to determine each driver’s risk level. By using actual driving behavior as the core factor in rate determination, Root differentiates between low-risk and high-risk drivers and offers a premium rate that reflects each individual’s driving habits. This business model also encourages safe driving. The approach appeals to customers who feel they deserve fair pricing based on their real driving patterns rather than standardized metrics.

For example, a driver who maintains safe habits, such as smooth acceleration, gentle braking, and limited phone usage, would be assessed as a lower risk. Root may then offer this driver a lower premium, as their driving behavior reduces the likelihood of accidents. Conversely, a driver who exhibits riskier behaviors like hard braking or frequent phone use while driving would have a higher risk profile and thus face a higher premium.

Revenue Model

Root Insurance caters to a wide range of drivers while maximizing its revenue opportunities through customizable premium structures. Here are the core components of Root’s revenue model:

- Insurance Premiums Through Personalized Pricing

Root generates revenue primarily from the premiums paid by its customers. It leverages driving data collected through telematics to assign a risk profile to each driver. Based on this profile, it offers a personalized premium rate. Safe drivers receive discounted premiums, while riskier drivers may face higher rates. This creates a direct link between driving habits and insurance costs.

- Usage-Based and Pay-Per-Mile Plans

Another significant component of Root’s revenue model is its usage-based pricing options, including pay-per-mile plans. These plans appeal to customers who don’t drive often, like remote workers or urban residents using public transport. By charging only for miles driven, Root caters to drivers who would pay full premiums under traditional policies.

- Revenue Opportunities Through Expanded Insurance Offerings

Root has also explored opportunities for future revenue growth through additional insurance products and services. By expanding into renters or homeowners insurance, for example, Root can cross-sell products to its existing customer base. Through this strategy, Root enhances customer loyalty and retention while building additional revenue streams that complement its core auto insurance offerings.

Why Is A Behavior-Based Auto Insurance Model Like Root Insurance A Strong Business Investment?

A behavior-based auto insurance model presents a promising business opportunity by meeting modern consumer expectations for fairness and personalization. Root Insurance’s recent revenue of ₹87.17 billion and a market cap of $1.24 billion show the financial potential in this innovative insurance sector. This model maximizes revenue through personalized premiums. It also offers flexibility with usage-based pricing options, like pay-per-mile plans.

For those entering the market, this approach is a robust investment. It taps into evolving customer expectations for fairer, responsive insurance options based on actual driving behavior. Looking ahead, the global market of behavior-based auto insurance is expected to reach approximately $95.28 billion by 2028, driven by the rise of connected and autonomous vehicles, further improvements in artificial intelligence and machine learning, and regulatory support for safer driving practices.

What Are The Emerging Models In Insurance?

| Insurance Model | Description | Pros | Cons |

| Usage-Based Insurance (UBI) | |||

| Telematics-Based | Uses devices or apps to monitor driving behavior and adjust premiums. | – Personalized premiums based on individual behavior- Encourages safer driving- Potentially lower costs for safe drivers | – Privacy concerns- High initial cost for telematics setup- Limited to specific vehicle types |

| Pay-Per-Mile | Charges premiums based on miles driven. | – Fair pricing for low-mileage drivers- Encourages environmentally-friendly behavior- Simple to understand | – May not benefit high-mileage drivers- Tracking required |

| Microinsurance | Provides affordable coverage for low-income individuals and small businesses. | – Affordable and accessible- Flexible coverage- Can reduce financial vulnerability | – Limited coverage- Lower margins for insurers- May require subsidies to remain sustainable |

| Parametric Insurance | Pays claims based on pre-defined triggers like weather events. | – Quick payouts- Clear, objective parameters- Simplified claims process | – No customization for non-standard events- May not cover full losses |

| Insurtech Models | |||

| Digital Insurance | Uses tech to streamline processes and offer innovative products. | – Lower operating costs- Faster processing times- Access through digital channels | – Potential cybersecurity risks- Limited human interaction for complex issues |

| Peer-to-Peer Insurance | Connects individuals to share risks and pool premiums. | – Lower premiums through pooled resources- Stronger sense of community- Fewer overhead costs | – Limited to specific types of risk- Regulatory challenges in some regions |

| Blockchain-Based Insurance | Enhances transparency, security, and efficiency in insurance processes using blockchain technology. | – Improved transparency and data integrity- Reduces fraud- Simplifies claims process | – Complexity in setup- Regulatory challenges- Limited adoption so far |

Development Steps for Behavior-Based Auto Insurance Model Like Root Insurance

Building a behavior-based auto insurance model like Root Insurance requires a tech-focused strategy focused on data, analytics, and engagement. Here are the essential steps to follow:

Step 1: Define Core Business Model and Target Market

Start by defining the business model and identifying the target demographic. Decide whether you’ll focus on general drivers, low-mileage drivers, or specific groups, like young drivers. Outline your pricing model. Decide if it will be purely behavior-based, usage-based, or a hybrid model with flexible plan options.

Step 2: Develop a Robust Telematics Platform

Invest in developing or integrating a telematics platform to collect real-time driving data. This platform should use smartphone capabilities, including GPS and accelerometers, to monitor driving behaviors like speed, braking, and acceleration. Collaborate with telematics solution providers to guarantee accurate data collection and seamless integration with mobile devices.

Step 3: Build a User-Friendly Mobile App

Create a mobile app that users can easily download and set up. The app should continuously monitor driving behaviors, offer data insights, and provide feedback to drivers about their habits. Ensure the app has a clear interface, adheres to privacy regulations, and lets users control their data permissions.

Step 4: Implement Data Analytics and Machine Learning Models

Use machine learning algorithms to analyze driving data and predict risk profiles. Implement predictive modeling techniques to identify patterns and assess risk factors accurately, enabling personalized insurance quotes. The system should be capable of updating risk profiles dynamically as driving data changes over time.

Step 5: Develop a Customizable Pricing Engine

Create a pricing engine that uses behavioral data to calculate personalized premiums. Include flexibility for pay-as-you-drive or pay-how-you-drive models. Ensure that the engine can process large data volumes in real-time to adjust premiums accurately based on safe driving behaviors.

Step 6: Ensure Compliance with Data Privacy Laws

Given the reliance on personal driving data, compliance with data privacy laws such as GDPR and CCPA is crucial. Develop protocols to encrypt data, anonymize user information, and provide users with transparency about data usage. Regular audits and compliance checks are essential to maintain user trust and legal standing.

Step 7: Design an Incentive Program for Safe Driving

Encourage safe driving by developing rewards or discounts that are visible in the app. These could include immediate feedback on good driving or periodic reductions in premiums for maintaining safe driving habits. This step helps to improve user engagement and retention by incentivizing users to drive safely.

Cost of Developing A Behavior-Based Auto Insurance Model Like Root Insurance

| Category | Description | Estimated Cost Range |

| Research and Development | Data collection, cleaning, analysis, machine learning model development, risk modeling, and pricing algorithms | $1,000 – $15,000 |

| Telematics Technology Integration | Partnering with telematics providers or building in-house technology, data integration | $2,000 – $8,000 |

| User Research and Testing | User surveys, interviews, and usability testing | $2,000 – $5,000 |

| Front-End Development | Mobile app development (iOS and Android), UI/UX design, real-time feedback | $1,000 – $20,000 |

| Web Portal Development | Customer portal for policy management, claims, and communication | $5,000 – $10,000 |

| Back-End Development | Cloud-based infrastructure (AWS, GCP, Azure), data storage and processing | $5,000 – $10,000 |

| API Development | APIs for data exchange between mobile apps, web portals, and backend systems | $5,000 – $10,000 |

| Data Analytics Platform | Data warehousing, data mining, and business intelligence tools | $5,000 – $10,000 |

| Testing and Quality Assurance | Unit, integration, and user acceptance testing | $2,000 – $5,000 |

| Ongoing Costs | Maintenance, updates, customer support, marketing, and sales | variable |

| Total Estimated Cost Range | $10,000 – $100,000 |

Factors Affecting the Development Cost of Behavior-Based Auto Insurance Model

- Telematics Integration

The integration of telematics solutions for tracking driver behavior is a critical part of a behavior-based insurance model. Whether partnering with telematics providers or developing in-house solutions, this can affect the development cost significantly. - Data Collection and Analysis

Collecting accurate, comprehensive driving behavior data is essential for creating personalized insurance models. Gathering, cleaning, and analyzing this data can be costly. Ensuring the accuracy of insights for pricing and risk assessments adds to the expense. - Machine Learning and AI Model Complexity

Developing algorithms that can interpret driver behavior and provide accurate pricing based on risk assessment is a highly technical task. The complexity of these models directly impacts development costs. - Regulatory Compliance

Insurance models, especially behavior-based ones, must comply with local, state, or even international regulations. Ensuring data privacy, anti-discrimination laws, and fair pricing can add significant overhead to development, especially when working across multiple jurisdictions.

Conclusion

In my opinion, creating a behavior-based auto insurance model like Root Insurance leads innovation in a transforming industry. The market for behavior-based auto insurance is growing steadily, creating a prime opportunity to capitalize. Advances in telematics, AI, and machine learning enable accurate, cost-effective pricing models. Consumers increasingly seek fairer, personalized options, making this approach appealing. This method improves customer satisfaction and drives operational efficiency, benefiting both consumers and entrepreneurs.

Want to Develop a Behavior-Based Auto Insurance Model Like Root Insurance?

At Idea Usher, we recognize the immense potential of a behavior-based auto insurance model and are thrilled to help turn your app idea into a reality. With over 500,000 hours of coding experience in app development, our team is well-equipped to guide you through every step of building a seamless, data-driven platform that can revolutionize the insurance industry. We’re passionate about helping entrepreneurs like you create innovative solutions that not only meet market demands but also set new industry standards.

Let’s work together to develop a platform that not only empowers your business but also provides customers with the personalized, fair insurance experience they deserve. We’re here to help you succeed!

FAQs

What technologies are required to build this kind of platform?

To build a behavior-based auto insurance model, you will need technologies such as telematics, mobile apps, machine learning algorithms, and cloud infrastructure. These technologies help in collecting driving data, processing it, and delivering insights in real-time to assess risk and determine premiums.

How do you collect driving data?

Driving data is typically collected through mobile apps or devices that track user behavior, including speed, acceleration, braking, and distance driving. The data is then processed and analyzed to evaluate the driver’s risk profile.

What are the benefits of a behavior-based auto insurance model?

This model provides more accurate pricing, as premiums are based on individual driving behaviors rather than general demographic factors. It rewards safe drivers with lower premiums, promotes better driving habits, and reduces fraud by using real-time data analysis.

How can AI and machine learning help in this model?

AI and machine learning can analyze large amounts of driving data to create personalized pricing models and predict future driving behavior. These technologies can also help in detecting anomalies, ensuring accuracy in assessing risk, and automating claims processes.