Key Takeaways

- Rising adoption of stablecoin banking platforms is transforming global payments by enabling faster, low-cost transactions with blockchain-powered financial infrastructure.

- Platforms like Plasma combine stablecoin wallets, payment cards, cross-border payments, yield features, and developer APIs to deliver a seamless digital banking experience.

- A successful platform requires secure blockchain architecture, banking integrations, regulatory compliance, fraud prevention, and scalable payment infrastructure to support businesses and consumers.

- Stablecoin banking is creating new opportunities across fintech, global payroll, cross-border remittances, and B2B payments by simplifying international money movement.

- How Idea Usher can help businesses build stablecoin banking platforms with blockchain development, secure wallet architecture, compliance systems, and scalable fintech infrastructure.

People today expect money to move as easily as information. They want fast, around-the-clock payments that are simple to use, no matter where they are. This growing demand is making stablecoin banking platforms like Plasma increasingly popular. What sets these platforms apart is that they deliver a familiar banking experience while using blockchain to make transactions faster and more efficient. If you’re planning to build a platform like Plasma, success depends on creating a secure and trusted platform that feels as intuitive as a modern banking app while offering the benefits of stablecoin-powered payments.

We’ve developed several stablecoin banking solutions that combine blockchain payment infrastructure with secure digital wallet architecture to deliver fast and reliable financial experiences. Drawing on this expertise, we’re writing this blog to explain how to create a stablecoin banking platform like Plasma.

Market Trends Driving Stablecoin Banking Adoption

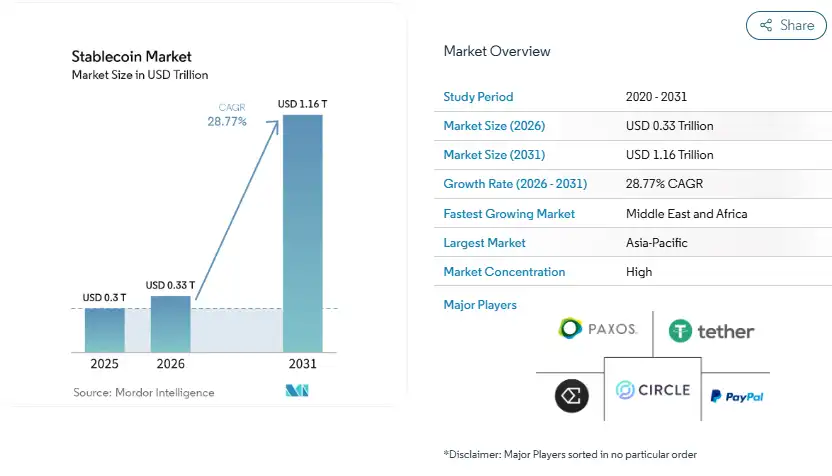

According to Mordor Intelligence, the stablecoin market is expected to grow from USD 0.33 trillion in 2026 to USD 1.16 trillion by 2031, showing how quickly businesses are adopting digital dollars for everyday payments. Much of this growth comes from the demand for faster global transactions. Instead of waiting several days for bank transfers to clear, businesses can send and receive stablecoins almost instantly while reducing payment costs.

Source: Mordor Intelligence

This makes stablecoins a practical choice for modern financial platforms. For entrepreneurs looking to build in this space, the primary value proposition lies in replacing legacy infrastructure like SWIFT for specific business use cases.

- Corporate Treasury: Companies use stablecoins to move capital between global subsidiaries instantly.

- Supply Chain Settlement: Importers pay overseas manufacturers without waiting days for clearance.

- Freelance Platforms: Global marketplaces use digital dollars to pay remote talent without heavy remittance fees.

A prime example of a platform capitalizing on this infrastructure shift is Bridge. The company provides stablecoin orchestration and issuance APIs to help businesses move money globally. Its financial success proves the market demand. Bridge generated $28.1 million in revenue before attracting a historic $1.1 billion acquisition by Stripe.

Building a platform that mirrors this success means targeting high-volume corridors. Success depends on creating clean user interfaces that hide the underlying blockchain complexity from the end business user.

Institutional Adoption

Legacy banks are no longer ignoring digital assets. Major institutions are actively launching their own stable tokens or integrating public stablecoins into their networks. This shift is driven by the need to defend market share against agile fintech competitors. This institutional entry validates the technology and creates massive business-to-business opportunities.

| Institutional Activity | Strategic Objective |

| Tokenizing Deposits | Creating digital representations of fiat for instant internal transfers. |

| Custody Services | Holding digital assets securely for institutional clients. |

| Liquidity Provision | Serving as market makers for stablecoin-to-fiat pairs. |

Another major player demonstrating the immense profitability of this trend is BVNK. This platform bridges traditional banking with digital assets by processing billions in stablecoin volume for global fintechs and payment service providers. BVNK scales its business model aggressively, reaching approximately $120 million in annualized revenue. This strong financial position recently led to an acquisition deal with Mastercard for up to $1.8 billion.

Capitalizing on this trend requires building institutional-grade security from day one. Entrepreneurs must focus on architecture that plugs directly into existing banking APIs and legacy core systems.

Regulatory Progress

Stablecoins are becoming easier for businesses to adopt as governments introduce clearer regulations around how they should operate. This reduces legal uncertainty and gives enterprises more confidence to build on this technology. If you’re developing a stablecoin banking platform, compliance should be part of the product from the start. Features like identity verification, transaction monitoring, and support for regional regulations not only help meet legal requirements but also make the platform more trustworthy and ready for long-term growth.

The Vision Behind Plasma’s Stablecoin-First Ecosystem

Plasma is a specialized network designed precisely for stablecoins. It avoids the broad, multi-purpose approach of typical networks like Ethereum or Solana. By stripping away non-essential elements like NFTs and governance tokens, Plasma creates a streamlined channel engineered for fast digital money movement.

The financial backing behind this vision is substantial, with the project securing $77.5 million in total funding. This capital injection includes a $24 million Series A round co-led by Framework Ventures and Bitfinex, alongside strategic support from Peter Thiel’s Founders Fund and Tether CEO Paolo Ardoino. Early indicators of the ecosystem’s economic viability are already visible, with Plasma generating over $226,000 in protocol revenue from transaction fees as it expands its operational scale.

1. Purpose-Built Blockchain

General-purpose networks struggle with predictable costs because they treat every transaction the same. A complex smart contract execution or an NFT mint competes for space with a simple payment, driving up network fees. Plasma eliminates this friction by tailoring its entire architecture exclusively to stablecoins like USDT and USDC.

This single-focus infrastructure provides clear strategic advantages for operators.

- Predictable Operational Costs: Eliminating network congestion protects businesses from erratic fee spikes during high-traffic events.

- Optimized Settlement Speeds: The technical design targets sub-second block times, matching the speed requirements of commercial payment networks.

- Maximizing Capital Efficiency: By optimizing transaction paths, Plasma allows financial platforms to settle high-volume transfers with minimal overhead.

Entrepreneurs evaluating this layer can think of it as a dedicated express lane for money. Building on a payment-specific network ensures that enterprise applications retain their speed and cost-efficiency as transaction volumes scale.

2. Everyday Banking Experience

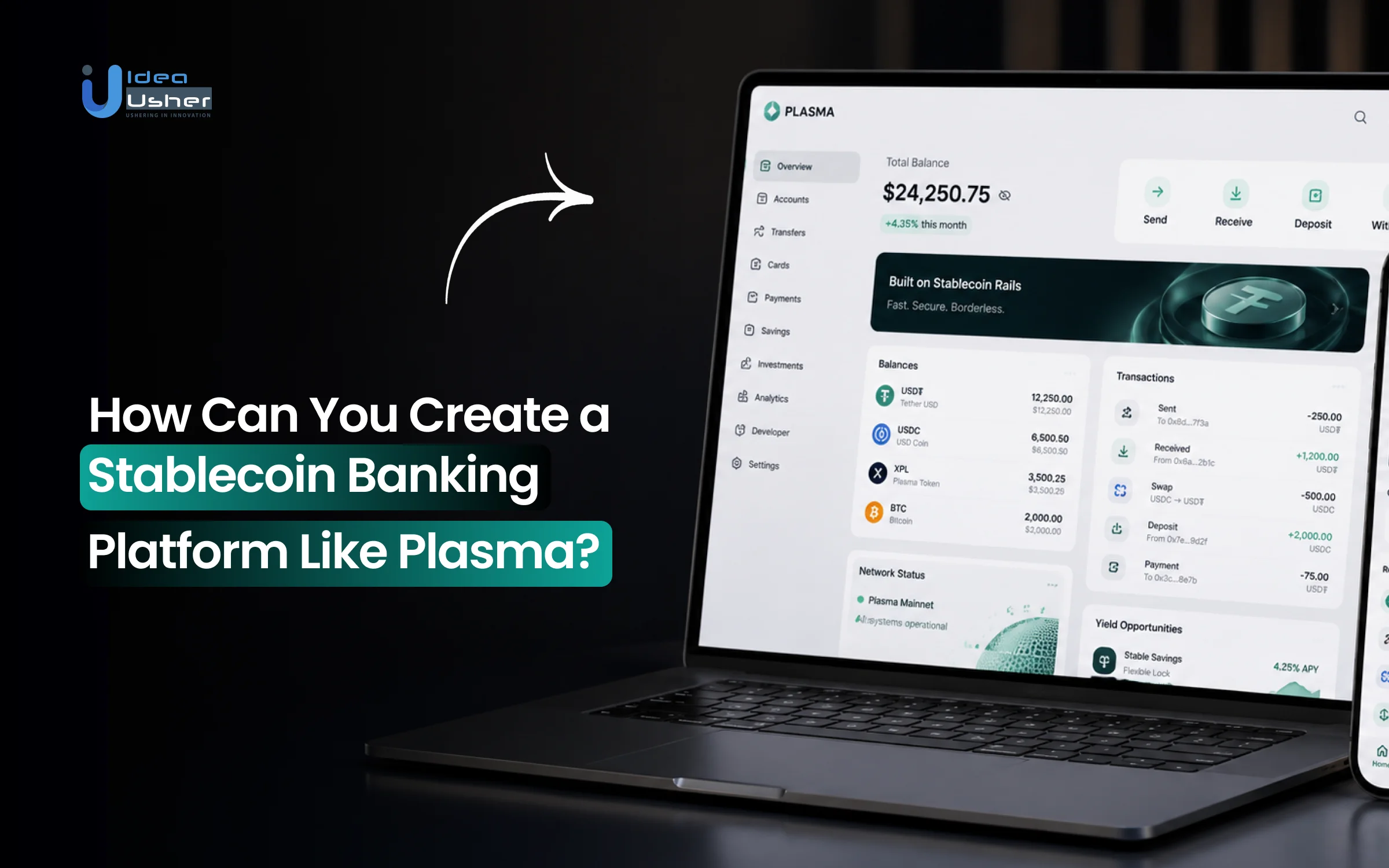

The mass adoption of digital assets depends on removing technical friction. Most non-technical users find seed phrases, gas fees, and wallet addresses confusing. Plasma bridges this gap by abstracting the blockchain layer completely, delivering a user experience that looks and feels like standard online banking. Through its consumer-facing platform, Plasma One, users can interact with digital dollars using familiar tools.

| Feature Area | Legacy Crypto Experience | Plasma Approach |

| Transaction Fees | Requires holding a separate native token (like ETH or SOL) for gas. | Zero-fee transfers, allowing users to spend clean dollar balances. |

| Point of Sale | Limited merchant acceptance requiring direct wallet integration. | Direct card issuance backed by Visa and Mastercard networks. |

| Capital Access | Complex decentralized lending pools with variable rates. | Integrated accounts providing up to 4% cashback and 6% yield. |

This strategy shifts the focus from speculative trading to everyday utility. For platforms building in this ecosystem, this means significantly lower user acquisition costs and higher retention rates among mainstream customers.

3. Global Finance Foundation

The long-term goal for Plasma extends beyond individual wallet applications. The platform aims to serve as the underlying infrastructure for global digital money movement. By offering compliance-ready frameworks and robust developer tools, Plasma enables external businesses to deploy automated financial products effortlessly.

This structural position aligns perfectly with the evolving global stablecoin market, where 140 major companies, including Visa, Stripe, and BlackRock, recently formed a consortium to launch Open USD. Plasma stands as a vital technical partner within this shift, moving the industry away from proprietary, single-issuer models toward shared financial networks.

Plasma One: The Consumer Banking Experience

Plasma One acts as the user-facing application layer of the network. It brings the efficiency of backend blockchain infrastructure directly to everyday financial interactions. The product architecture merges multi-currency stability with retail utility, removing the fragmented interfaces that typically slow down consumer adoption.

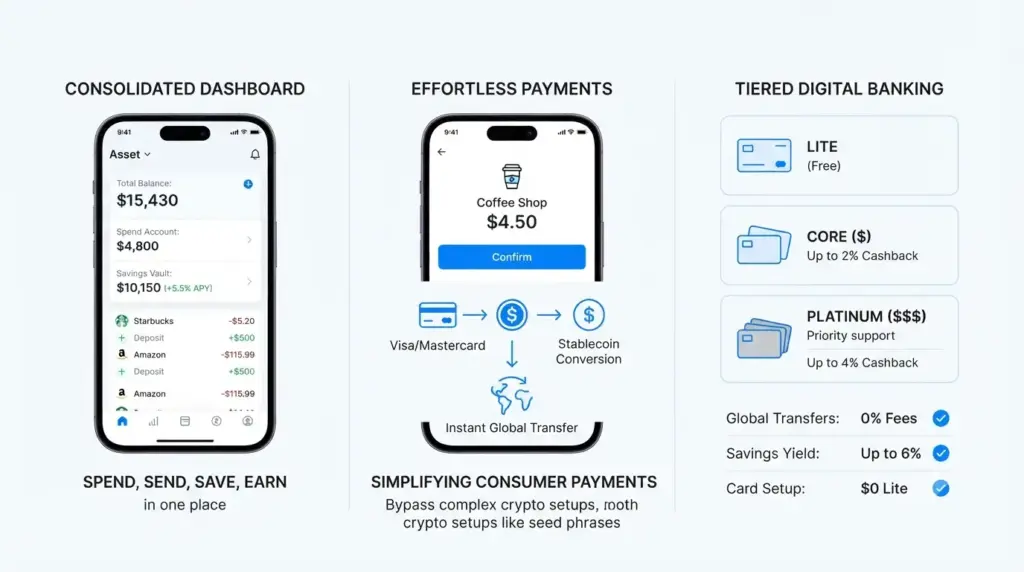

To maintain its digital banking ecosystem and card programs, the platform operates a transparent, tiered monetization model across its Lite, Core, and Platinum subscription tiers.

1. Spend, Send, Save, Earn

Retail users usually have to manage multiple applications to navigate the digital asset ecosystem. They buy on an exchange, move funds to a non-custodial wallet, and use external protocols to find yield. Plasma One concentrates these isolated financial functions into a single dashboard. This consolidation redefines how users manage their daily capital allocations.

- Unified Asset View: Users track balances, active yields, and transaction histories side by side.

- Instant Capital Deployment: Moving funds from a high-yield savings sleeve to an active spending card takes one tap.

- Streamlined Rewards: Cashback from merchant purchases routes directly back into the user balance as digital dollars.

By removing structural friction, the platform turns stablecoins into functional money. It changes the consumer perception from holding a digital asset to simply managing an online cash balance.

2. Simplifying Consumer Payments

The onboarding process bypasses the complex setup of traditional crypto wallets. Users do not manage seed phrases or configure gas limits. They complete a quick, compliant identification check and link a standard funding source like a debit card or bank account to load digital dollars.

When a user initiates a transaction, the underlying system handles the token settlement automatically. Global peer-to-peer transfers complete within seconds. For retail spending, Plasma One links directly with Visa and Mastercard networks, allowing users to spend their balances at over 175 million global merchants. The merchant receives local fiat while the system handles the stablecoin debit behind the scenes.

3. Digital Bank Differentiation

Traditional digital banks rely heavily on interchange fees and wire costs, passing those structural expenses down to the consumer. Plasma One uses the lean design of the Plasma network to lower operational costs, passing the financial benefits back to its users. The platform provides a distinct advantage over legacy neo-banking structures.

| Financial Feature | Neo-Bank Standard | Plasma One Model |

| Global Transfer Fees | Heavy markups on cross-border wires and exchange rates. | Zero-fee global transfers with immediate settlement. |

| Account Yield | Minimal returns tied to central bank interest rates. | Integrated token strategies providing up to 6% yield. |

| Account Fees & Card Setup | Monthly maintenance caps or hidden activation charges. | $0 setup fees for virtual cards on the base Lite tier. |

While peer-to-peer transfers remain free and virtual card setup on the Lite tier costs nothing, Plasma One charges standard foreign exchange fees up to 1% on non-USD purchases to cover card network processing. Users looking for enhanced features can scale into the paid Core and Platinum tiers.

These tiers reduce foreign exchange costs and add premium perks like priority VIP support, multiple physical cards, and up to 4% cashback on everyday purchases. This tiered structure ensures a predictable revenue stream for the platform while keeping entry barriers low for the mass market.

Key Features of Stablecoin Banking Platforms Like Plasma

Building a platform like Plasma is about creating a banking experience that feels simple for users while running on a powerful blockchain infrastructure behind the scenes. By combining consumer-friendly features with tools for businesses and developers, Plasma demonstrates how a stablecoin platform can serve individual users, enterprises, and fintech partners from a single ecosystem.

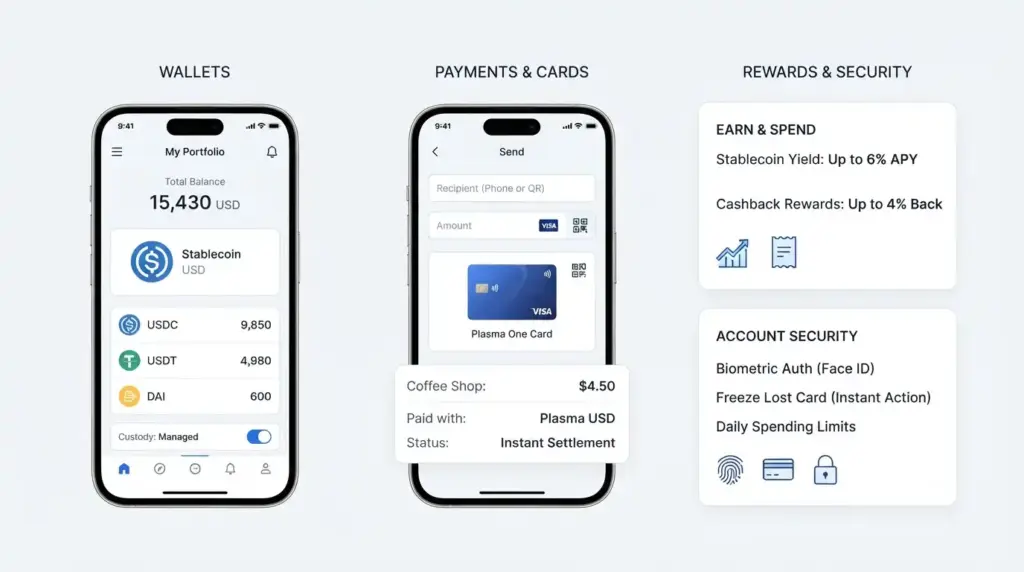

1. Stablecoin Wallets

The stablecoin wallet is the core of the Plasma experience, giving users a simple way to store, send, receive, and manage digital dollars. It supports both managed custody and self-custody, allowing users to choose the level of control that suits them. The wallet also offers easy fiat on-ramps and a unified view of supported stablecoins, making digital assets feel as convenient to use as a traditional banking app.

2. Cross-Border Payments

Plasma simplifies cross-border payments by allowing users to send stablecoins using a phone number or QR code, with transactions settling in under one second on supported payment corridors. By removing gas fees for eligible transfers, the platform creates a smoother user experience while generating revenue through business-focused settlement services instead of charging consumers for everyday transactions.

3. Payment Cards

Plasma One makes stablecoins easy to use for everyday spending by connecting them to Visa-backed payment cards. Users can pay online with a virtual card or use a physical card in stores just like a regular debit card. The platform automatically converts stablecoins into local currency during each transaction, so payments feel seamless without requiring users to manually exchange their digital assets first.

4. Rewards and Yield

Plasma creates active financial incentives for users to maintain capital within its ecosystem. Instead of letting funds sit idle, Plasma One connects users with native yield opportunities that deliver up to 6% returns on eligible stablecoin holdings. This capability runs parallel to a built-in merchant rewards program. The economic model rewards consistent ecosystem engagement.

| Incentive Type | Mechanism | Target User Base |

| Cashback Rewards | Up to 4% back on retail purchases using the Plasma card. | Daily retail shoppers |

| Stablecoin Yield | Automated returns paid out directly to holding accounts. | Long-term savers |

| Referral Bonuses | Tokenized rewards for expanding the active user network. | Community growth advocates |

These integrated features increase user retention significantly, as customers can spend, save, and grow their capital within a single mobile interface.

5. Account Security

Plasma combines strong security with simple account controls to help users protect their funds. The app lets users instantly freeze a lost card, approve transactions with biometric authentication such as passkeys or Face ID, and set daily spending limits for added protection. Regular third-party smart contract audits further strengthen platform security, creating a safer and more reliable experience for everyday stablecoin payments.

6. High-Speed Blockchain

Plasma is built on a payment-focused blockchain designed for speed and reliability. With one-second block times, it delivers fast transaction confirmations that are well suited for everyday payments. The network is also EVM-compatible, allowing developers to build or migrate Ethereum applications with minimal changes.

Its infrastructure is designed to handle thousands of transactions per second while keeping fees predictable and performance consistent. This gives businesses a strong foundation to support large user bases without sacrificing speed or reliability.

7. Developer APIs

Plasma goes beyond a consumer banking app by offering APIs and developer tools for businesses. Companies can use its infrastructure to build branded payment solutions, digital wallets, or stablecoin-powered financial services without creating everything from scratch. This makes it easier to launch new products while expanding the platform’s ecosystem and revenue opportunities.

How to Create a Stablecoin Banking Platform Like Plasma?

Launching a successful stablecoin banking platform requires a smart blend of blockchain speed and strict financial compliance. For entrepreneurs looking to capture this market, the setup must be highly strategic. At IdeaUsher, we engineer these exact digital systems, helping you deploy scalable architectures that mix advanced web3 infrastructure with familiar retail banking tools.

1. Define a Strategy

The first phase requires pinpointing your core audience and their exact financial pain points. You must decide if your application will prioritize retail remittances or corporate treasury management. Platforms like Plasma stand out because they do not just add digital assets as a side feature. They build their entire business model around stablecoins from day one.

A sharp product strategy shapes your early technical choices.

- Target Audience: Decide if you are launching a B2B treasury tool or a consumer payment app.

- Asset Selection: Choose which regulated digital dollars to support based on regional demand.

- Core Utility: Focus on solving a specific issue like reducing high international wire costs.

Getting these variables right keeps your project focused. It helps you avoid spending money on unneeded features and keeps your budget aligned with clear market needs.

2. Build Blockchain Infrastructure

Your backend engine needs to process thousands of transactions without sudden delays or fee spikes. Plasma handles this by using a specialized network layer optimized for payments. This layout delivers fast settlement times and low costs while keeping things fully compatible with standard Ethereum development tools.

We write clean smart contracts and design secure node networks. This structural setup ensures your ledger remains fast, highly reliable, and fully protected against external security threats.

3. Create Banking Experience

Mainstream adoption happens when digital assets behave just like regular money. Your mobile and web applications must look and feel like standard online banking tools. Users should be able to send funds globally without needing to learn about gas fees or complex blockchain keys.

A clean design turns casual users into long-term customers.

| Legacy Crypto Pain Point | Your Platform Solution |

| Complex public wallet addresses | Simple phone number or email routing |

| Unpredictable transaction costs | Fixed or zero-fee transfer paths |

| Confusing seed phrase backups | Standard biometric login and recovery |

We focus on building these simple, familiar interfaces. By hiding the technical backend, we ensure your app remains accessible to everyday users who just want a faster digital account.

4. Integrate Global Networks

A stablecoin banking platform delivers real value when users can spend their digital dollars just like regular money. That requires seamless connections between blockchain infrastructure, payment cards, and traditional banking systems. The result is a familiar payment experience that works both online and in physical stores.

Our team builds these integrations so users can pay with their stablecoin balances without thinking about what happens in the background. We connect your platform with card issuers, banking partners, and payment networks to create fast, reliable transactions that feel as simple as using a traditional debit card.

5. Implement Banking-Grade Security

Operating a global money network means compliance must be built directly into your software architecture. You cannot afford to treat identity checks or fraud screening as an afterthought. Enterprise clients and major banks will only partner with platforms that prove they can protect user data and track suspicious transactions.

Security must run through every part of the system.

- Identity Verification: Automated user screening during onboarding.

- Transaction Monitoring: Real-time software alerts to stop fraudulent transfers.

- Data Privacy: Strict encryption layers to protect private financial records.

Our development approach focuses heavily on safety. We install advanced security protocols and real-time monitoring tools, ensuring your system guards client assets while meeting international regulatory standards.

6. Develop Business APIs

Expanding beyond consumer banking can unlock new revenue opportunities. We build secure APIs and developer tools that let businesses integrate with your platform for services like payroll, cross-border payments, and treasury management. This helps you grow from a banking app into a financial infrastructure provider that serves both individual users and enterprise clients.

7. Scale the Ecosystem

Launching your MVP is only the beginning. As your platform grows, you’ll need to support new markets, expand payment capabilities, and keep the infrastructure ready for higher transaction volumes. At IdeaUsher, we help you build with long-term growth in mind by delivering a secure, scalable platform that can evolve as your business and user base expand.

Cost to Create a Stablecoin Banking Platform Like Plasma

When budgeting for a stablecoin banking platform, the financial commitment depends heavily on product scope and structural depth. Building a system that mimics Plasma requires combining secure ledger mechanics with consumer-facing financial integrations. For entrepreneurs evaluating this space, breaking down the project into clear phases keeps the initial capital requirement predictable while clearing a direct path toward market validation.

MVP Development Cost

A minimum viable product focus allows you to launch core services without spending money on complex custom network nodes right away. This early setup concentrates strictly on building stablecoin wallets, an automated user identity check, and basic fiat entry and exit points. Launching an MVP helps founders test user adoption and secure early transaction volumes before investing in heavy infrastructure expansions. An MVP model typically demands a lower entry budget.

- Target Cost Range: Developing a functional payment MVP generally costs between $50,000 and $90,000.

- Timeline Estimate: Building and testing this initial setup takes roughly three to five months.

- Core Goal: Deliver a working mobile application where users can fund balances and send digital dollars seamlessly.

We specialize in launching these targeted MVPs at IdeaUsher. By keeping the early feature set lean, we help you get to market faster so you can gather real feedback from your users before deploying larger budgets.

Cost-Influencing Factors

The total investment required to scale beyond a basic MVP shifts depending on the operational features you want to add. Introducing custom elements like physical payment card lines, global banking connections, or enterprise business dashboards changes your engineering requirements. Several technical choices determine your ultimate development budget.

- Ledger Infrastructure: Using existing networks keeps costs low, while designing a custom layer increases backend expenses.

- Card Issuance Links: Connecting with card processors to offer physical and virtual cards adds integration steps.

- Compliance Software: Installing automated identity screening and real-time transaction tracking impacts costs.

- API Complexity: Providing open business-to-business tools for payroll or merchant setups requires extra development time.

Our engineering team works closely with you to map out these technical choices. We guide you toward the most cost-efficient integrations, making sure your platform stays highly secure without blowing past your budget parameters.

Phase Cost Breakdown

To give you a precise understanding of capital allocation, it helps to review a detailed financial breakdown across a standard development lifecycle. Scaling from initial design to a fully realized production system requires dividing resources across multiple specializations. The following framework shows a typical budget allocation for building a comprehensive stablecoin banking solution.

| Development Stage | Estimated Cost Range (USD) | Primary Deliverables |

| Product Discovery & UI/UX Design | $8,000 – $15,000 | Wireframes, user journey maps, and mobile interfaces. |

| Frontend & Backend Engineering | $25,000 – $45,000 | Core application logic, database setup, and user profiles. |

| Blockchain Implementation | $20,000 – $35,000 | Smart contracts, ledger connections, and custody vaults. |

| Banking Rails & Card API Integration | $15,000 – $30,000 | Card processing setups and fiat deposit networks. |

| Compliance & Fraud Architecture | $12,000 – $22,000 | Identity checks, anti-money laundering tools, and tracking software. |

| Security Auditing & Quality Testing | $10,000 – $18,000 | Code vulnerability reviews and end-to-end payment stress tests. |

| Ecosystem Deployment & Maintenance | $10,000 – $15,000 | Cloud hosting infrastructure and ongoing performance updates. |

| Total Estimated Investment | $100,000 – $180,000 | A secure, fully scaled stablecoin banking platform. |

Managing this mix of software design, ledger engineering, and strict compliance takes an experienced development team. Partnering with us at IdeaUsher gives you direct access to professional fintech developers who can build your platform from the ground up. We coordinate every stage of the breakdown, ensuring your digital dollar application launches smoothly, securely, and fully optimized for long-term growth.

Industries That Benefit Most from Stablecoin Banking

The biggest opportunity for stablecoin banking often lies in business payments rather than consumer transactions. Many companies still deal with slow settlements, high transfer fees, and costly currency conversions. By solving these challenges, a stablecoin platform can reduce operational costs, improve cash flow, and create a strong competitive advantage in high-value financial markets.

1. Fintech Platforms

Stablecoin infrastructure gives fintech companies a faster way to expand into new markets without relying on traditional banking networks in every country. By offering multi-currency digital wallets and global payment capabilities, businesses can reduce transaction costs while giving users a seamless cross-border experience.

Helio Pay demonstrates the potential of this approach. The platform has processed more than $1.5 billion in transactions for thousands of online merchants through stablecoin-powered checkouts. Its growth and market traction ultimately led to a $175 million acquisition by MoonPay, highlighting the increasing demand for modern digital payment infrastructure..

Building a platform for the fintech sector means providing clean software components.

- Embedded Finance: Let third-party apps insert digital balances right into their client dashboards.

- Instant Exchange Layers: Provide automated conversions between public stable tokens and localized cash.

- Shared Liquidity Pools: Maintain deep asset reserves so large client withdrawals never cause processing delays.

Targeting this sector guarantees high transaction volumes, as every fintech app built on top of your architecture funnels its own user base directly through your payment infrastructure.

2. Cross-Border Remittance

Cross-border payments are one of the biggest opportunities for stablecoin platforms. Unlike traditional remittance systems that rely on multiple intermediaries, stablecoins enable faster settlements and significantly lower transfer costs. This makes them especially valuable in regions where affordable international payments are in high demand.

A platform like Gnosis Pay shows how this can work in practice by connecting stablecoin balances with everyday payments. To build a successful remittance platform, it’s also important to support smooth fiat deposits and withdrawals.

3. Global Payroll

Managing payroll across multiple countries can be slow and expensive with traditional banking systems. Stablecoin payments simplify this process by enabling businesses to send salaries to employees and contractors within minutes while reducing transfer costs and delays. This makes them especially useful for companies with global teams.

Bitwage is a strong example of this model. The platform allows employees to receive part or all of their salaries in stablecoins such as USDC or USDT and has processed over $400 million in crypto payroll volume for thousands of businesses worldwide.

| Corporate Payroll Feature | Business Operational Utility |

| Automated Invoicing | Lets international freelancers generate compliant bills directly inside the system. |

| Mass Payout Routing | Allows human resource teams to pay hundreds of remote staff with one click. |

| Accounting Software Links | Syncs transaction histories with popular enterprise bookkeeping tools automatically. |

4. B2B Payments

Large enterprise corporations routinely struggle with liquidity freezes caused by slow cross-border vendor payments. Settling invoices with overseas suppliers often traps valuable working capital in clearing networks for days. Stablecoin systems resolve this capital inefficiency, allowing corporate treasuries to move millions of dollars instantly at any hour of the day.

Build a Stablecoin Banking Platform with Idea Usher

Investing in digital dollar infrastructure requires a technical partner who understands how to bridge decentralized networks with institutional banking rails. Navigating this landscape alone often exposes founders to severe security gaps and costly licensing delays. We eliminate these execution risks by acting as your dedicated technology team, turning high-level investment concepts into highly polished, production-ready financial applications.

Concept to Product

We manage the complete development process from product discovery to app launch. We design intuitive user experiences, validate ideas with interactive prototypes, and build scalable architectures that make future feature additions easier. This approach helps you launch faster with a stablecoin platform that is easy to use, ready to scale, and built for long-term growth.

Scalable Banking Infrastructure

A sustainable stablecoin network must withstand intense transaction volumes and strict regulatory scrutiny. Our developers write optimized smart contracts and construct banking-grade security architectures to secure user assets. We embed automated compliance protocols right into the transaction layer, protecting your business from operational liabilities. We integrate all the essential components needed to run a premium fintech enterprise.

| Infrastructure Layer | Technical Focus | Business Protection |

| Identity Verification | Seamless KYC and AML automation | Keeps fraudulent actors off your platform |

| Card Integration | Direct API hookups with Visa and Mastercard | Provides immediate retail utility for balances |

| Security Vaults | Multi-signature custody and data encryption | Defends user funds against network vulnerabilities |

Our technical depth keeps your ecosystem highly resilient. We install continuous fraud tracking tools and design high-throughput codebases, ensuring your platform processes transactions instantly even during peak market traffic.

Long-Term Growth Experts

Our team brings over 500,000 hours of custom software development experience to your project, backed by seasoned engineers with a track record of building complex fintech platforms. We do not just hand over source code and walk away after deployment. We remain your long-term technical allies, optimizing your servers and expanding your features as your transaction volumes grow.

True competitive advantages are built when a platform can scale up its active user base smoothly without experiencing network downtime.

- Continuous Maintenance: We monitor cloud infrastructure to keep application performance completely fluid.

- Corridor Expansion: We hook up new international fiat rails to open up extra remittance routes for your users.

- Feature Evolution: We integrate advanced tools like automated corporate payroll routing and merchant checkout widgets.

Conclusion

Building a stablecoin banking platform like Plasma is about much more than integrating blockchain into a banking app. Success comes from creating a product that feels simple for users while delivering fast payments, strong security, and seamless financial services behind the scenes. If you start with the right technology strategy and build on scalable infrastructure from day one, you’ll be in a much better position to launch quickly, adapt to changing regulations, and grow your platform as demand for stablecoin banking continues to rise.

Things to Know About Stablecoin Banking Platforms

A1: A stablecoin banking platform is a financial app that lets people store, send, receive, and spend stablecoins through an experience that feels similar to online banking. Instead of relying on traditional payment networks, it uses blockchain technology to move money quickly and at a lower cost. Many platforms also support payment cards and international transfers, making them useful for both individuals and businesses that want faster digital payments.

A2: The biggest difference is how money moves. Traditional banks depend on banking networks that can take time to process payments, especially across countries. Stablecoin banking platforms use blockchain to settle transactions much faster and are usually available around the clock. They also give users easier access to digital assets while still offering familiar features like accounts, payments, and spending tools.

A3: Yes, they can be very secure when built with the right technology. Most leading platforms protect users with encryption, two-factor authentication, identity verification, and continuous fraud monitoring. It’s also important to choose a platform that follows financial regulations and is transparent about how it protects customer funds. Strong security builds trust and is one of the most important parts of any stablecoin banking platform.

A4: A successful platform should make digital payments simple. Users expect a secure wallet, instant transfers, payment cards, and an easy way to move money between fiat and stablecoins. Businesses often need additional features such as payment APIs and account management tools. Platforms like Plasma also focus on reducing transaction costs and creating a smooth payment experience for everyday use.