(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

For years, crypto liquidity moved fast and sometimes recklessly. When volatility struck, many platforms were not structurally prepared for disciplined risk management. That is when regulated crypto bank platforms began gaining traction, as businesses realized that digital assets require capital controls and transparent reporting.

As institutions gradually entered the market, they understandably demanded custody governance and compliance standards comparable to traditional banks. Platforms had to evolve beyond simple trading engines and integrate banking APIs with structured monitoring systems. Automated AML engines and insured custody frameworks became necessary rather than optional.

We’ve developed numerous regulated crypto banking platform solutions powered by licensed crypto custody systems and compliant digital asset platforms. As IdeaUsher has this expertise, we are sharing this blog to discuss the structured steps required to develop a regulated crypto bank platform.

Key Market Takeaways for Regulated Crypto Bank Platforms

Source: Grand View Research

Regulated crypto banks are gaining traction because they offer something traditional finance understands. Structured compliance, licensed custody, audited controls, and regulatory oversight.

With regulatory frameworks such as MiCA in Europe and increasing federal guidance in the United States, these platforms are becoming a credible bridge between legacy banking and blockchain ecosystems.

Two notable examples illustrate this shift. Anchorage Digital Bank became the first federally chartered crypto bank in the United States, operating under the OCC’s oversight and providing institutional custody, staking, trading, and stablecoin infrastructure.

Kraken Financial operates under Wyoming’s SPDI banking charter, enabling regulated custody and fiat-to-crypto services while positioning itself for broader compliance expansion under European MiCA licensing frameworks.

What Is a Regulated Crypto Bank Platform?

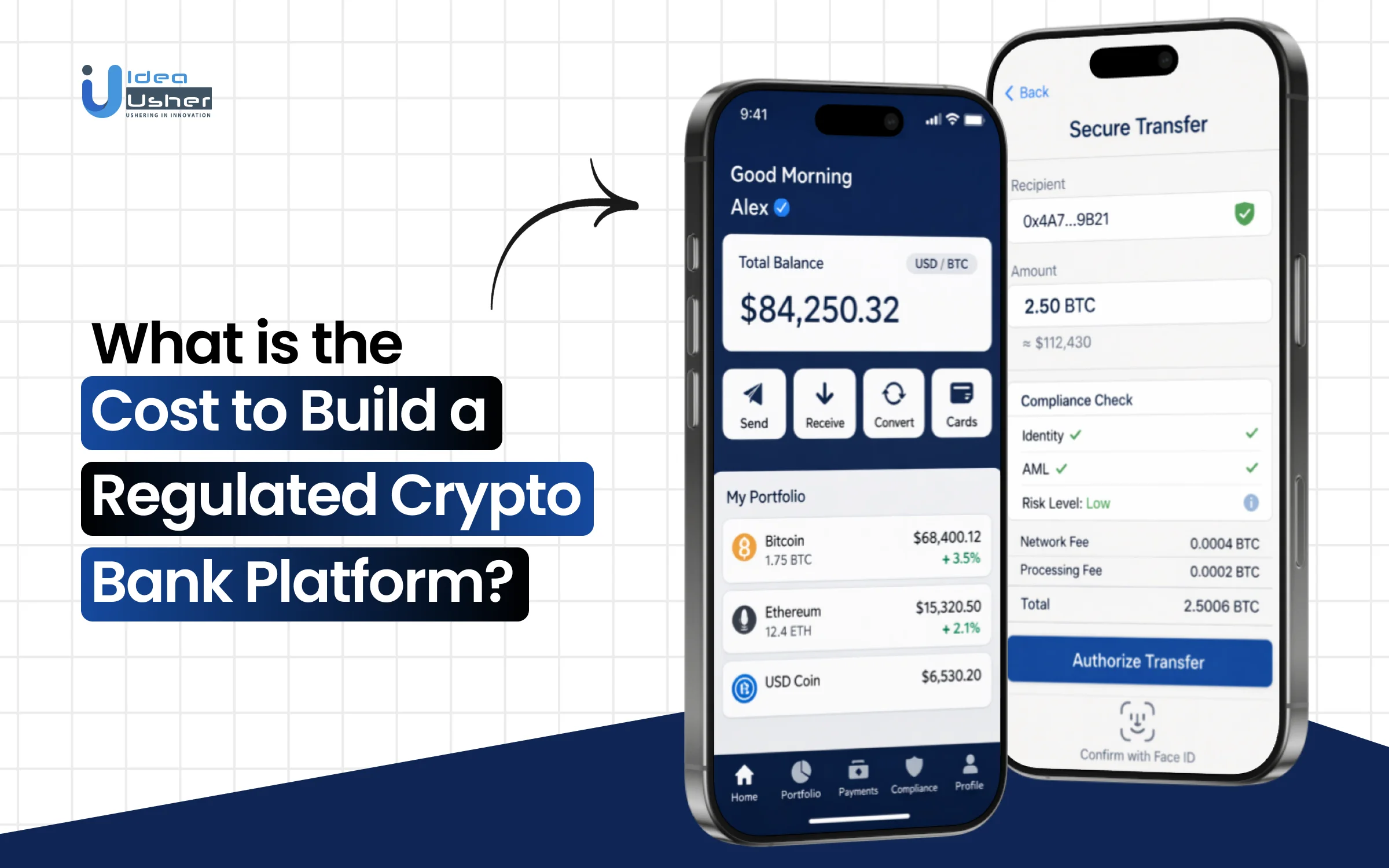

A regulated crypto bank platform is a digital financial institution that combines blockchain-based asset services with formal regulatory oversight. It allows users to custody, transfer, and trade digital assets, and sometimes earn yield, while operating under defined legal frameworks, such as banking licenses or virtual asset service provider registrations.

Unlike unregulated exchanges, it embeds KYC, AML, custody governance, transaction monitoring, and reporting controls directly into its architecture.

How Does a Regulated Crypto Bank Platform Work?

A regulated crypto bank platform links a fiat ledger with a blockchain ledger that syncs in real time. When you send funds, verify identity, run compliance checks, and securely update balances before settlement. Custody controls and risk engines quietly ensure everything stays safe and compliant.

The Dual-Ledger Architecture

At its core, a regulated crypto bank maintains two parallel record-keeping systems that are continuously synchronized.

The Fiat Ledger (Traditional Banking Layer)

This is the familiar banking infrastructure. It tracks everything in traditional currencies such as the U.S. dollar, the euro, and the pound. When a user deposits cash via wire transfer, it appears in this section.

When they spend with a debit card, the deduction happens here. This ledger follows all the rules of traditional banking. It is subject to reserve requirements, eligible for FDIC or equivalent insurance, and auditable by financial regulators using standard accounting principles.

The Blockchain Ledger (Crypto Layer)

This tracks digital assets such as Bitcoin, Ethereum, stablecoins, and tokenized assets. Every transaction here happens on-chain, meaning it is recorded permanently on a distributed ledger. Unlike a personal wallet, the bank system manages these assets with institutional-grade controls.

The synchronization engine sits in the middle. When a user moves money from their fiat account to buy crypto, both ledgers update instantly and accurately.

The Three-Layer Operational Model

A regulated crypto bank platform operates across three distinct layers, each with its own purpose and controls.

Layer 1: The User Experience Layer

This is what customers see in the mobile app or web dashboard. They can:

- View combined balances, both fiat and crypto in one place

- Buy and sell cryptocurrencies with fiat

- Send money to other users instantly

- Pay bills using either fiat or crypto

- Stake assets to earn yield

- Apply for loans collateralized by their crypto holdings

To the user, it feels like one seamless financial account. They do not see the complexity underneath.

Layer 2: The Orchestration Engine

This is the brain of the operation. It:

- Routes transactions to the correct internal system

- Enforces business rules such as minimum balances and trading limits

- Applies compliance checks before any money moves

- Manages synchronization between fiat and crypto ledgers

- Handles fee calculations and currency conversions

When a user clicks “Buy $1,000 worth of ETH with my USD balance,” the orchestration engine verifies sufficient funds, checks compliance rules, locks the USD, requests a price quote from liquidity providers, executes the trade, and updates both ledgers within seconds.

Layer 3: The Settlement & Custody Layer

This is where assets actually live.

For fiat:

User funds are held in pooled accounts at partner banks, typically with individual subledger accounting. In regulated jurisdictions, these funds are often protected by pass-through insurance, meaning each user is insured up to specified limits, even though the funds are technically pooled.

For crypto:

Assets are held across hot, warm, and cold wallets managed by the custody system. The vast majority, typically 95 percent or more, sits in cold storage, which remains air gapped and offline. A small percentage stays in hot wallets for daily withdrawals. The custody system automatically manages movement between these tiers based on demand.

The Daily Lifecycle of a Transaction

Let us follow a simple transaction through the entire system. Sarah wants to send $500 worth of USDC to her friend Mike, who also banks with the same platform.

| Step | Description |

| Initiation | Sarah opens the app, enters Mike username or wallet address, and taps send. |

| Validation | The system confirms Sarah has $500 USDC, checks account status, and verifies limits. |

| Compliance Scan | The transaction is screened against sanctions lists and risk databases. |

| Ledger Update | Internal balances are updated instantly as an “off-chain transfer” with no network fee. |

| Notification | Both users receive confirmation in real time. |

If Sarah sends to an external wallet:

- Initiation & Validation: Same initial checks apply.

- Compliance Extended: The system handles Travel Rule requirements. It identifies the receiving wallet owner when possible, prepares beneficiary data, and verifies that the destination is not sanctioned.

- Hot Wallet Preparation: The custody system selects a hot wallet with sufficient USDC. If required, it sweeps funds from warm storage to replenish liquidity.

- Multi-Signature Authorization: The transaction requires multiple cryptographic signatures distributed across separate signing nodes. No single person or server controls the full key.

- Blockchain Broadcast: Once enough signatures are collected, the transaction is broadcast to the blockchain network and monitored for confirmations.

- Final Settlement: Once confirmed on-chain, balances update, and compliance logs are finalized for regulatory reporting.

The Compliance Infrastructure

What distinguishes a regulated platform is the compliance layer embedded throughout every workflow.

Identity Verification (KYC)

Every user undergoes identity verification before accessing services. Advanced systems continuously monitor document validity, jurisdiction risk, and suspicious behavioral shifts.

Transaction Monitoring

All transactions, on-chain and off-chain, pass through monitoring systems that detect:

- Structuring behavior

- Rapid asset layering across tokens

- Exposure to high-risk wallets

- Unusual velocity compared to historical patterns

Travel Rule Compliance

For transactions above defined thresholds, typically between $1,000 and $3,000, depending on jurisdiction, beneficiary information is securely exchanged between institutions. If the receiving institution cannot process the required data, the transaction is paused or blocked.

Sanctions Screening

All counterparties are screened against global sanctions databases. Screening includes names, wallet addresses, IP signals, and behavioral indicators.

Regulatory Reporting

Suspicious activity reports, large transaction reports, and prudential disclosures are generated automatically and submitted to regulators. Supervisory authorities may receive structured data feeds for oversight.

The Reserve Management System

If the platform issues a stablecoin or holds crypto deposits, reserve management becomes critical.

The treasury system:

- Tracks real-time liabilities

- Monitors reserves across bank accounts and custody storage

- Maintains regulatory reserve ratios

- Generates proof of reserves or public attestations

- Manages liquidity waterfalls to balance withdrawal demand and security

If withdrawals exceed hot wallet capacity, the system automatically transfers funds from warm storage. If additional liquidity is required, controlled procedures initiate cold storage access, which often requires physical keyholder participation.

The Fiat On Ramp and Off Ramp

Connecting to the traditional banking system requires a structured infrastructure.

On Ramping Fiat to Crypto

When a user deposits cash via wire, ACH, SEPA, or card network, the banking partner confirms receipt. The orchestration engine credits the fiat ledger. If the user buys crypto, the platform sources liquidity, executes the trade, and moves assets into custody.

Off-Ramping Crypto to Fiat

When a user sells crypto, the platform executes the sale with liquidity providers. The resulting fiat balance is credited internally and made available for withdrawal to an external bank account.

The core challenge is regulatory synchronization. Each movement must comply with both blockchain compliance rules and traditional banking requirements. A transaction valid in crypto must also align with banking controls, and the reverse is equally true.

Cost to Develop a Regulated Crypto Bank Platform

Developing a regulated crypto bank platform requires strong compliance and secure engineering, but costs can be controlled with the right structure. We follow a cost-effective, phased approach that keeps our clients regulator-ready while avoiding unnecessary overhead.

1. Legal Framework & Regulatory Licensing

| Sub-Step | Cost Range (Low – Mid) | Cost Range (Enterprise / Tier 1) | Notes |

| Jurisdictional Mapping | $25,000 – $50,000 | $75,000 – $150,000 | Legal opinions on token classification. |

| License Application | $40,000 – $100,000 | $250,000 – $750,000+ | MiCA (EU) is cheaper than a U.S. banking charter. |

| Minimum Capital | $135,000 (MiCA) | $5,000,000 – $20,000,000 | Mandatory reserves. Not a development cost. |

| Compliance Perimeter | $30,000 – $60,000 | $80,000 – $150,000 | Drafting AML, KYC, and privacy policies. |

2. Core Engineering (Ledger & Architecture)

| Sub-Step | Cost Range (Low – Mid) | Cost Range (Enterprise / Tier 1) | Notes |

| Hybrid Ledger System | $150,000 – $300,000 | $500,000 – $1,200,000 | Off-chain banking core with on-chain synchronization. |

| Reconciliation Engine | $50,000 – $100,000 | $150,000 – $300,000 | Real-time parity verification logic. |

| Fiat / Crypto On-Ramp | $30,000 – $70,000 | $100,000 – $250,000 | Direct API integrations with partner banks. |

3. Institutional Custody Framework

| Sub-Step | Cost Range (Low – Mid) | Cost Range (Enterprise / Tier 1) | Notes |

| Custody Setup (MPC / HSM) | $50,000 – $150,000 | $200,000 – $450,000 | Key management and shard distribution. |

| Governance Logic | $20,000 – $50,000 | $70,000 – $150,000 | Multi-signature quorums and withdrawal limits. |

| Wallet Segregation | $15,000 – $40,000 | $60,000 – $120,000 | Individual client vaults versus omnibus structure. |

4. Compliance & Smart Contract Controls

| Sub-Step | Cost Range (Low – Mid) | Cost Range (Enterprise / Tier 1) | Notes |

| KYC / AML Integration | $40,000 – $80,000 | $100,000 – $200,000 | Provider fees plus custom workflow development. |

| Travel Rule Engine | $25,000 – $50,000 | $60,000 – $120,000 | Automated VASP to VASP data sharing. |

| Pauseable Contracts | $15,000 – $35,000 | $50,000 – $100,000 | Emergency circuit breakers and override logic. |

5. Security, Audit & Launch Preparation

| Sub-Step | Cost Range (Low – Mid) | Cost Range (Enterprise / Tier 1) | Notes |

| Smart Contract Audit | $30,000 – $70,000 | $150,000 – $400,000 | Performed by firms such as OpenZeppelin. |

| Penetration Testing | $20,000 – $50,000 | $80,000 – $180,000 | Testing APIs and infrastructure layers. |

| Regulatory Simulation | $15,000 – $30,000 | $50,000 – $100,000 | Testing regulatory reporting workflows prior to approval. |

The estimated development cost ranges from $850,000 to $ 3,500,000 USD, depending on scope and regulatory requirements. These figures are indicative and may vary based on your specific model. For a precise quote, feel free to connect with us for a free consultation.

Factors Affecting the Cost of a Regulated Crypto Bank Platform

When you build a regulated crypto bank platform, jurisdiction, custody model, compliance automation, security depth, and fiat integration will directly shape cost and risk. Each choice can significantly impact capital reserves and regulatory exposure. If you design these layers carefully, the platform can scale securely and efficiently under supervision.

1. Jurisdiction & Licensing Model

Your choice of jurisdiction is not just a legal checkbox; it is the single biggest financial variable in your project.

The Cost Fluctuation: $100,000 – $700,000+

Why it varies:

A fast-path regulatory sandbox in a jurisdiction such as Lithuania or the UAE might cost $50,000 to $100,000 in legal fees and have minimal capital requirements.

However, applying for a New York BitLicense or a full banking charter in Germany through BaFin can easily consume $300,000 to $700,000 in legal retainers, local director fees, and business plan audits before you even touch a line of code.

2. Custody Architecture Depth

This decision defines whether you rely on third-party custody infrastructure or invest in building a hardened in-house cryptographic security architecture.

The Cost Fluctuation: $30,000 – $180,000

Why it varies:

The “API Wrapper” ($30k – $60k): Integrating a third-party custody provider like Fireblocks or Copper is the fastest route. You are essentially renting their infrastructure.

The “Self Custody” Leap ($80k – $180k): Building your own Multi Party Computation infrastructure with geographically distributed nodes and Hardware Security Module integration doubles or triples the engineering hours. You are paying for deep cryptography PhDs and hardware audit certifications such as FIPS 140-2 Level 3.

3. Compliance Automation Level

You can hire 20 compliance officers, or you can build a robot. The math favors the robot, but the robot is expensive to build.

The Cost Fluctuation: $40,000 – $150,000+

Why it varies:

Manual or Reactive ($40k – $70k): Integrating a basic KYC provider like Onfido and a standard AML screening tool like Elliptic that checks wallets against a blacklist. This requires a manual review team.

Proactive RegTech ($100k – $150k+): Implementing Entity-Based AML scoring, where the system uses AI to build risk profiles based on transaction patterns, not just wallet addresses.

Adding “Travel Rule” automation via Notabene or TRISA integration incurs an additional $20k-$40k in development costs because you must map transactions to specific counterparties in real time.

4. Security Layer Sophistication

Security is the one area where “good enough” is a euphemism for future headline.

The Cost Fluctuation: $25,000 – $90,000+

Why it varies:

Standard Audit ($25k – $40k): A standard smart contract audit and a basic penetration test. This gets you past the minimum requirement for a license application.

Fortress Mode ($50k – $90k+): Layered penetration testing, both internal and external, continuous bug bounty programs on a yearly retainer, and the implementation of Hardware Security Modules for key management.

You also need Governance Modules with multi-signature workflows for admin functions that require legal sign-offs, which adds development complexity.

5. Fiat Banking Partnerships

Crypto is the engine, but fiat is the fuel. Getting it in and out of the traditional system is a messy, expensive problem.

The Cost Fluctuation: $20,000 – $120,000+

Why it varies:

Simple On-Off Ramp ($20k – $50k): Integrating a payment processor like MoonPay or Banxa. Fast, but expensive per transaction, and it keeps you at arm’s length from the actual banking system.

Direct Banking Integration ($70k – $120k+): Establishing a direct partnership with a correspondent bank and integrating via APIs to offer Virtual IBANs International Bank Account Numbers. This requires building middleware to translate between the bank’s legacy core system, ISO 8583, and your modern ledger.

What Reporting Obligations Does a Regulated Crypto Bank Have?

A regulated crypto bank must report suspicious transactions, large value transfers, capital ratios, and liquidity positions to regulators. It should promptly file AML and Travel Rule disclosures while maintaining detailed audit records. These obligations must be tightly integrated into the core ledger and compliance systems to ensure accurate and timely reporting.

1. AML & Suspicious Activity Reporting

This is the frontline of regulatory reporting. When something looks wrong, you must tell someone quickly.

Suspicious Activity Reports SARs / Suspicious Transaction Reports STRs

What triggers it: Any transaction that raises reasonable grounds for suspicion, whether it involves money laundering, terrorist financing, tax evasion, or fraud.

The threshold: In the US, SARs are required for transactions of $2,000 or more that appear suspicious. In the EU under MiCA, the threshold is typically €1,000, though some member states set lower amounts.

What to look for:

Structuring, which involves multiple small transactions just below reporting thresholds

- Rapid movement through multiple assets or wallets

- Connections to high-risk jurisdictions

- Use of mixing or obfuscation services

- Transactions inconsistent with the customer’s profile or business activities

What the report must include:

A suspicious activity report must clearly include full customer identification details and verified account information. It should precisely describe the unusual behavior and provide complete transaction data, including amounts, dates, and counterparties.

The bank must also provide a logical explanation of why the activity appears suspicious, so regulators can properly assess the risk and take action if required.

Timing: Immediately upon forming a reasonable suspicion. Delays invite regulatory sanctions.

Record retention: All analysis and supporting documentation must be kept for five years, including the reasons for submitting or not submitting a report.

Currency Transaction Reports CTRs:

In the US, transactions involving cash or cash equivalents above $10,000 must be reported to FinCEN, regardless of whether they appear suspicious.

2. The Travel Rule

The Travel Rule requires that specific customer information travel with transactions above certain thresholds.

What must be transmitted:

- Originator’s name and address

- Originator’s account or wallet information

- Beneficiary’s name

- Beneficiary’s account or wallet information

Thresholds by jurisdiction:

- FATF Standard: $1,000 or €1,000

- United States: $3,000

- European Union: €1,000 under MiCA

- Japan: ¥100,000, which is approximately $750

The technical challenge:

This information must be transmitted securely to the receiving VASP using protocols such as TRISA or OpenVASP. If the receiving institution cannot accept Travel Rule data, the transaction may need to be blocked or held.

EU specific:

Under the EBA Travel Rule Guidelines, service providers must have procedures to detect and manage transfers with missing or incomplete information and manage the associated money laundering and terrorist financing risk.

3. Market Abuse Reporting (MiCA and Equivalent)

Under MiCA Title VI, crypto banks must actively monitor for and report market abuse.

What must be monitored:

A regulated crypto bank must continuously monitor all orders and transactions, whether they occur on-chain or within internal ledgers. It should also carefully assess how the distributed ledger operates, including the consensus mechanism to detect manipulation risks.

This oversight must operate in real time so potential market abuse can be identified and reported without delay.

Types of market abuse to detect:

- Insider dealing

- Market manipulation, including pump and dump schemes

- Unlawful disclosure of inside information

Suspicious Transaction or Order Reports STORs: When market abuse is suspected, a STOR must be filed with the competent authority using prescribed templates.

ICT Systems: Banks must employ appropriate information and communication technology systems to assist in monitoring, with human analysis integrated throughout the process.

Staff training: Regular and comprehensive market abuse training for all relevant staff is mandatory.

4. Prudential Reporting

Regulators need to know you are financially sound and not just compliant.

Capital Adequacy: Under the FCA proposed CRYPTOPRU regime expected in 2026:

Minimum own funds:

- Stablecoin issuers: £350,000

- Crypto custodians: £150,000

Calculation:

The minimum capital a regulated crypto bank must hold is determined by whichever requirement is highest under the framework.

It should compare the Permanent Minimum Requirement, the Fixed Overhead Requirement (equal to one quarter of annual fixed expenses), and the K factor Requirement, which reflects activity-based risk exposure. This structure ensures capital levels can realistically scale with operational risk and business volume.

K factor examples:

- Stablecoin issuers must hold 2 percent of total stablecoins in circulation

- Custody providers must hold 0.04 percent of total client cryptoassets safeguarded

Liquidity Reporting

Banks must hold liquid assets to meet short-term obligations.

Basic Liquid Assets Requirement BLAR:

The Basic Liquid Assets Requirement requires a crypto bank to hold sufficient highly liquid assets at all times. It should maintain at least one-third of the Fixed Overhead Requirement and, in addition, 1.6 percent of any guarantees issued to clients.

This buffer can help the institution meet short-term obligations and manage unexpected liquidity stress effectively.

Stablecoin specific: Issuers must also meet an Issuer Liquid Assets Requirement ILAR to cover potential shortfalls in the backing asset pool within T plus 1.

Crypto Asset Exposure Reporting (Canada)

Under the OSFI final guidelines, effective from 2025 to 2026:

Two approaches:

- A simplified approach in which all crypto exposures are deducted from Common Equity Tier 1 capital.

- Comprehensive approach using a risk-sensitive framework with four asset categories named Groups 1a, 1b, 2a, and 2b

Limits: Maximum gross exposure to Group 2 crypto assets is 5 percent of Net Tier 1 capital.

Notification: Banks choosing the comprehensive approach must notify OSFI and maintain detailed documentation of their asset categorizations.

5. Token-Specific Reporting

If you issue or handle Electronic Money Tokens EMTs such as USDC or EURC, additional reporting applies.

Under MiCA EU

Quarterly reporting due by the 21st of April, July, October, and January:

Quarterly reporting must be submitted by the twenty-first of April, July, October, and January, and it should include detailed information on token holders, transaction volumes, and how the token is used as a means of exchange.

Daily reporting:

Daily reporting must provide end-of-business-day data on total token holdings so supervisors can closely monitor circulation and backing adequacy.

Format requirements:

Format requirements require that all monetary values be reported in EUR at the ECB spot exchange rate, and that standardized templates and naming conventions be strictly followed.

“Nothing to Report”: Even if there is no data, a confirmation must be submitted.

For USDC or EURC specifically, CASPs must report directly to the issuer, Circle, to help it fulfill its regulatory obligations.

The Consequences of Getting It Wrong

The stakes are real. The SEC 2024 enforcement action against Silvergate Bank resulted in the following:

- $50 million civil penalty

- CEO and CRO barred from serving as officers of public companies

- Five-year officer and director bars

- Reputation destroyed and business wound down

The charge involved misleading investors about the strength of the BSA and AML compliance program and failing to monitor over $1 trillion in transactions, including nearly $9 billion in suspicious transfers involving FTX.

How Does a Regulated Crypto Bank Protect Users from Validator Slashing?

A regulated crypto bank reduces slashing risk through remote signing controls and strict validator orchestration, helping prevent double signing and prolonged downtime. It may secure keys within HSMs or MPC systems to minimize operational faults. It also typically maintains active monitoring and insurance coverage, ensuring client assets remain financially protected in the event of a rare penalty.

Understanding the Threat

Before diving into protections, it is important to understand what banks are protecting against. Slashing is not random. It is triggered by specific validator failures:

Double Signing

This is the most severe offense. When a validator signs two conflicting blocks for the same slot, it creates an immediate inconsistency that could cause a chain fork. Double signing almost universally incurs the highest penalties.

Extended Downtime

While less severe than double signing, validators who go offline for extended periods can be penalized, jailed, removed from the active set, and lose rewards.

What is the real-world impact?

Since Ethereum staking launched, validators have been slashed 474 times. In one notable 2023 incident, Bitcoin Suisse lost nearly 200000 dollars after 100 newly set up validators were slashed. In September 2025, 39 validators were slashed in a single correlated event linked to operator issues.

Most slashing occurs due to coding errors or human error, not malicious intent. And that means it is preventable with the right systems.

1. Architectural Prevention

The first and most important line of defense happens before any validator ever goes live. Regulated banks architect their infrastructure to make slashing nearly impossible.

Double Signing Protection DSP

Double signing is the most heavily penalized offense, so banks prioritize preventing it entirely.

Local Anti-Slashing Databases: Each validator node maintains a local database tracking every block and attestation it signs. Before signing any new documents, the client checks this database to ensure there are no conflicting actions.

Infrastructure-level primitives: Banks use orchestration tools such as Kubernetes to ensure that multiple validator instances do not run simultaneously. When updates happen, the previous version is fully deleted before its replacement is deployed.

Remote Signing with High Watermarks: Instead of validator clients signing messages directly, signing is delegated to a secure remote signer that maintains a high watermark, a record of the last valid action signed. If a new request arrives for an older slot or conflicts with the watermark, it is automatically rejected.

Client Diversity

Running identical software across all validators creates systemic risk. A single bug could take down the entire fleet.

Banks enforce client diversity across both execution and consensus layers. By spreading validators across multiple client implementations, they ensure that a bug in any single client cannot trigger a correlated slashing event.

Geographic and Infrastructure Diversity

Banks distribute validators across:

- Multiple data centers

- Different cloud providers

- Various geographic regions

- Diverse power grids and network backbones

This prevents localized outages, whether from cloud provider failures, regional power outages, or network disruptions, from triggering mass downtime penalties.

2. Key Management

Validator keys are the crown jewels. If they are compromised or mismanaged, slashing becomes trivial.

Hardware Security Modules HSMs

Leading banks store validator keys in HSMs, tamper-proof hardware devices that generate, store, and use cryptographic keys without exposing them to the outside world. Keys never exist in plain text on disk or in memory outside secure hardware.

Multi-Party Computation MPC

For additional protection, banks use MPC to split private keys into fragments and distribute them across independent signing nodes. No single node ever holds a complete key, and a threshold of fragments must come together to sign any transaction.

Key Separation

Banks maintain strict separation between:

- Withdrawal keys, which control fund movement

- Validator signing keys, used for daily duties

This means even if a validator key is compromised during daily operations, withdrawal capabilities remain protected.

3. Operational Excellence

Prevention is ideal, but detection and rapid response are essential backups.

Real Time Monitoring

Banks deploy comprehensive monitoring across dozens of health indicators for each validator:

- Attestation performance and timing

- Network sync status

- Peer connectivity

- Disk health and system resources

- Client-specific error rates

Automated Alerts

When metrics deviate from normal ranges, alerts fire immediately. Modern institutional platforms now offer direct alerting integrations with Slack, Microsoft Teams, and API webhooks, enabling ops teams to respond within seconds rather than hours.

Safe Failover Protocols

If a primary validator fails, banks do not simply spin up a backup. That could trigger double-signing if both instances become active. Instead, they use:

- Hot standbys with remote signers that understand signing history

- Quorum-based key management that prevents simultaneous activation

- Staggered deployments with blue-green or canary patterns

Incident Response Playbooks

When something does go wrong, banks follow documented playbooks that include on-chain forensics to precisely determine the root cause, structured communication templates for clients and regulators, defined escalation paths with controlled emergency decision making, and formal post-mortem processes to systematically prevent recurrence.

4. Insurance

Despite best efforts at prevention, sophisticated clients demand a financial guarantee. This is where insurance comes into play.

Slashing Specific Insurance

Regulated insurers now offer products specifically designed to cover slashing losses. Chainproof, a Bermuda Monetary Authority-regulated primary insurance carrier, offers slashing insurance for proof-of-stake validators and node operators.

Their policies reimburse 95-98% of expected staking returns when slashing reduces yields below benchmark rates.

Yield Guarantee Products

More advanced products do not just cover losses from slashing. They guarantee minimum annual yields. Chainproof coverage, for example, tops up stakers’ returns if slashing causes their yield to fall below the Composite Ether Staking Rate CESR, a benchmark representing the average network-wide staking yield.

How It Works

When a client’s validator is slashed, the bank:

- Documents the incident with on-chain evidence

- Submits a claim to the insurer

- Upon approval, the recipient receives reimbursement

- Credits the client’s account for the lost value

This transforms an unpredictable operational risk into a known, insured exposure.

As one industry observer noted, “Insuring validator yields opens the door to financial products once thought too risky. With a reliable floor on returns, we could soon see total return staked ether ETFs and other structured products built on staking income”.

5. Provider Due Diligence

For banks that do not operate their own validators, selecting staking partners is a critical layer of protection.

What Banks Evaluate

Before delegating client funds, regulated banks scrutinize potential staking providers on:

| Due diligence area | What the bank checks |

| Slashing Record | Have any validators ever been slashed? How many, when, and why? A clean record is table stakes. |

| Uptime History | What is the historical validator uptime over 30, 90, and 365 days? How do realized rewards compare to network benchmarks? |

| Security Architecture | Do they use HSMs? Are keys ever present in plain text? Is there a clear separation between withdrawal and validator keys? |

| Governance Participation | Do they follow and understand network upgrades? Have they published research or improvement proposals? Providers active in governance are better prepared for changes that could affect returns. |

| Regulatory Compliance | What licenses do they hold? Do they have KYC AML controls? Can they produce audit-ready reports? |

Ongoing Monitoring

Due diligence is never a one-time checklist because stakeholder risk can evolve over time. Banks continuously monitor partners through public explorers, independent performance benchmarks, and periodic security assessments with SOC reporting.

When incidents occur, they carefully review post-mortems to quickly identify and systematically correct operational weaknesses.

6. Restitution Policies

Even with layered controls in place, regulated banks must clearly define financial responsibility when operational mistakes occur. If a client is harmed by a bank error, the loss is typically absorbed by the institution through reserves or insurance rather than passed on to the user.

Make Whole Provisions

Reputable regulated banks include clear restitution policies in their stakeholder agreements. If slashing occurs due to a bank or validator operational failure, the bank makes the client whole, either from operating revenue or insurance proceeds.

This stands in stark contrast to retail staking platforms, where users simply absorb losses.

Capital Reserves

Regulated banks maintain capital reserves specifically for operational risks. Under frameworks like the UK FCA proposals, banks must hold capital against staked assets. The K factor for clients’ cryptoassets staked in K CCS is 0.04 percent of the average staked amount, as regulatory capital.

The Track Record: Does It Work

The proof is in the results. Major institutional providers with robust slashing protections have never been slashed on supported networks.

Coinbase, for example, states: “With our robust slashing protections, Coinbase validators have never been slashed on any of the networks we support.”

This track record stems from the multi-layered approach described above: local anti-slashing databases, infrastructure primitives that prevent duplicate instances, and remote signing with high watermarks.

Top 5 Regulated Crypto Bank Platforms

We recently conducted focused research and identified a few regulated crypto bank platforms that may offer compliant custody and staking within structured regulatory frameworks. These platforms typically combine licensed banking infrastructure with blockchain systems in a technically reliable way.

1. Sygnum Bank

A Switzerland-based digital asset bank that combines traditional banking services with crypto custody, trading, staking, and tokenization. It serves institutional clients and professional investors.

Regulation: Fully licensed and supervised by the Swiss Financial Market Supervisory Authority (FINMA) under a Swiss banking and securities dealer license. This places it under strict capital, AML, and compliance requirements.

2. AMINA Bank

A regulated crypto bank offering fiat accounts, crypto custody, trading, staking, and structured investment products. It focuses on bridging traditional finance with digital assets.

Regulation: Holds a Swiss banking license from the Swiss Financial Market Supervisory Authority (FINMA) and operates under additional regulatory approvals in key international markets.

3. SoFi

A U.S. digital bank that integrates crypto trading and custody services within its broader financial ecosystem, alongside loans, investing, and personal banking.

Regulation: Operates under a national bank charter regulated by the Office of the Comptroller of the Currency (OCC) and is insured by the Federal Deposit Insurance Corporation (FDIC), ensuring compliance with U.S. federal banking standards.

4. Xapo Bank

A Gibraltar-based private bank that combines traditional USD banking with Bitcoin custody and crypto-enabled payment services. It focuses on high-net-worth individuals and long-term crypto holders.

Regulation: Fully licensed as a credit institution and regulated by the Gibraltar Financial Services Commission (GFSC) under Gibraltar’s Financial Services Act.

5. Bank Frick

A Liechtenstein-based bank providing crypto custody, trading, staking, and seamless fiat-crypto account integration for institutional and professional clients.

Regulation: Licensed and supervised by the Financial Market Authority (FMA) of Liechtenstein, operating under EU-aligned financial regulations and strict AML/KYC requirements.

Conclusion

Building a regulated crypto bank platform in 2025 is not just another software release; it is a financial infrastructure program that must carefully combine regulatory compliance, core banking logic, blockchain protocols, and institutional-grade security controls. You will need to invest significantly up front, but the long-term revenue potential and strategic regulatory positioning can justify that capital when the architecture is designed correctly.

Looking to Develop a Regulated Crypto Bank Platform?

IdeaUsher can help you design and build a regulated crypto bank platform that aligns with licensing frameworks while embedding KYC, AML, and custody governance directly into the core architecture.

With 500,000+ hours of coding experience, our team of ex-MAANG and FAANG developers has mastered the delicate balance between blockchain innovation and regulatory compliance. We do not just write code.

Why builders choose Idea Usher:

- Ex-MAANG and FAANG engineers – We have built at Google, Amazon, Microsoft, and Meta scale

- 500K+ development hours – Deep expertise in MPC custody, HSMs, and zero-knowledge proofs

- Regulatory-ready architecture – MiCA, Travel Rule, and FDIC compliant by design

- End-to-end delivery – From licensing strategy to smart contract deployment

- Proven track record – 20+ blockchain projects delivered across 5 countries

FAQs

A1: You should start by defining the regulatory model and jurisdiction, as licensing will shape the overall architecture. Finally, you integrate blockchain nodes, compliance engines, and policy-driven access controls so the platform can securely process digital assets and fiat transactions at scale.

A2: The cost can vary based on custody design, compliance scope, and geographic licensing requirements. The final budget will largely depend on security depth, transaction volume targets, and whether you build proprietary infrastructure or integrate third-party services.

A3: A crypto bank platform should include regulated onboarding with KYC and AML screening, secure custody with wallet tiering, real-time transaction monitoring, and fiat on and off-ramp integrations. Advanced platforms typically implement unified risk-scoring governance controls and institutional-grade access management to enhance operational resilience.

A4: At its core, the platform connects user accounts to blockchain infrastructure while enforcing compliance and custody governance at every step. Internally, the banking layer records balances, reconciles ledger entries, and continuously monitors activity to detect anomalies and maintain regulatory alignment.