(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Money sitting in a savings account once felt secure, but today it often feels unproductive as inflation steadily reduces purchasing power and traditional yields remain limited. You may notice that capital parked in banks rarely compounds meaningfully over time. This shift has gradually pushed individuals toward decentralized finance applications that operate continuously across global networks.

DeFi protocols can automatically deploy assets into smart contract vaults that rebalance strategies based on market conditions. Instead of waiting passively for marginal returns, you could actively allocate capital into programmable yield systems that run around the clock.

Over the years, we’ve developed numerous DeFi solutions that leverage technologies such as cross-chain interoperability protocols and yield-routing architectures. As IdeaUsher has this expertise, we’re sharing this blog to discuss the cost of developing a DeFi app like Superform.

Key Market Takeaways for DeFi Apps

According to Grandview Research, the DeFi market has moved well beyond early experimentation. From USD 26.94 billion in 2025 to a projected USD 1,417.65 billion by 2033, this pace of growth reflects how blockchain-based lending, borrowing, and trading are steadily reshaping financial infrastructure. Rising institutional participation and record total value locked figures signal that decentralized finance is becoming a structural layer rather than a niche alternative.

Source: Grandview Research

User adoption is being driven by transparency, yield opportunities, and open access. Platforms like Uniswap continue to dominate decentralized trading, with strong Layer-2 participation and millions of connected wallets, while Aave leads lending markets by enabling users to earn interest or borrow against collateral through automated smart contracts.

These applications demonstrate how capital can move efficiently without traditional intermediaries.

Strategic partnerships are further strengthening the ecosystem. For example, DeFi Development Corp. collaborated with Harmonic to enhance validator performance and decentralization within the Solana network.

Such integrations show how infrastructure-level innovation continues to improve scalability, revenue optimization, and network resilience across DeFi platforms.

What is the Superform App?

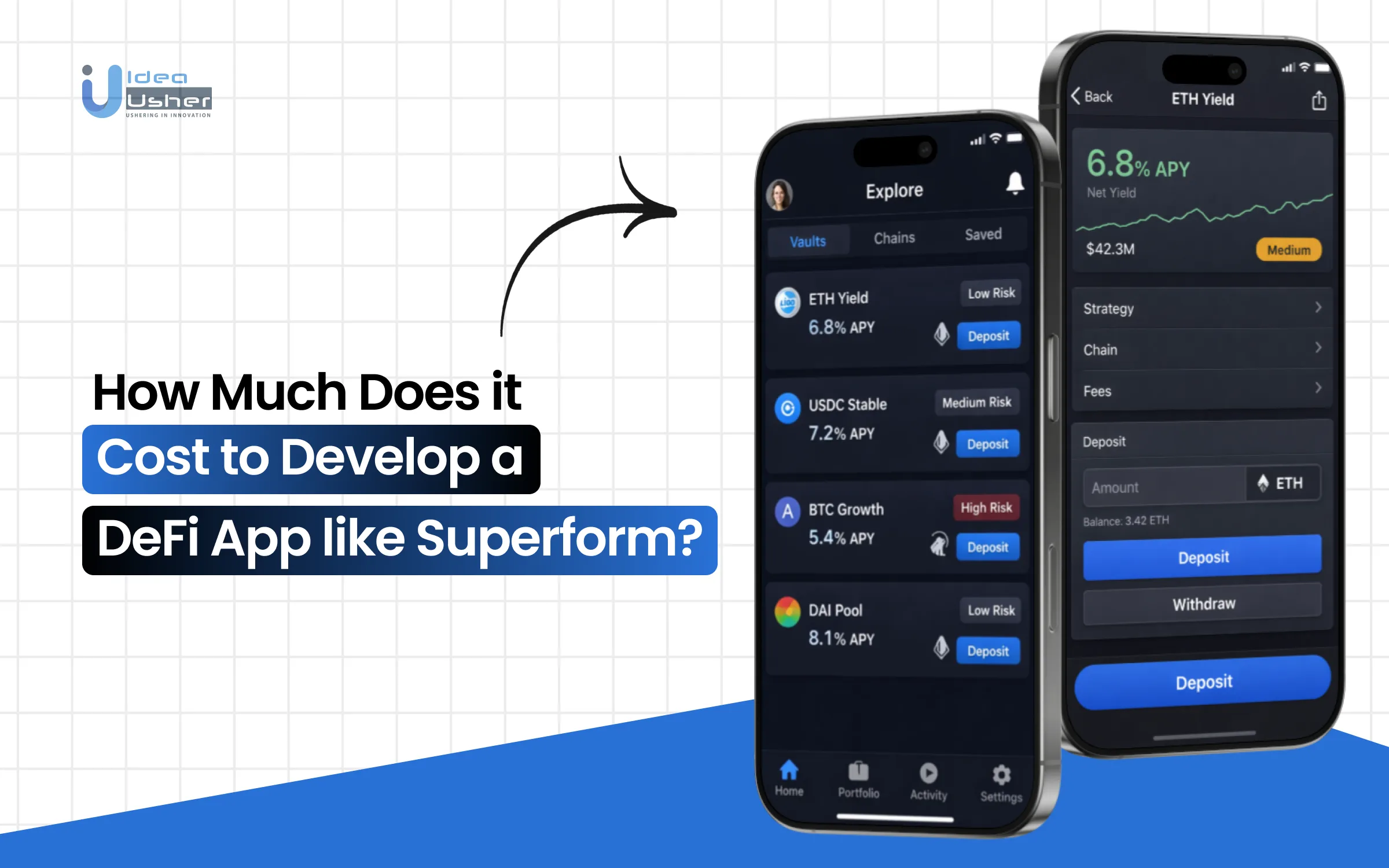

Superform is the on-chain wealth app from superform.xyz, a non-custodial platform that lets users save, swap, send, and earn optimized yields on crypto across chains. It provides a user-friendly web and mobile interface to interact with its underlying protocol for DeFi yield farming, lending, and staking.

The app connects to over 800 earning opportunities, such as SuperVaults, which automatically optimize returns on assets such as stablecoins, Bitcoin, and Ethereum. Users maintain full control of funds through self-custodial wallets secured with biometrics and multi-factor authentication. The protocol has secured billions in value through audited smart contracts.

Standout User Features of the Superform App

Superform quietly removes the usual DeFi friction by letting you deposit, swap, and bridge across chains in a single transaction, so your capital can start earning immediately. It can automatically rebalance into higher-yielding strategies and may intelligently route liquidity where it performs best.

1. One-Tap Deposits The Just Work Magic

Users can deposit into any vault on any chain using any asset in a single transaction. No manual bridging. Do not swap to the right token first. No switching networks.

Why it matters

The average DeFi user loses 15 to 20 minutes and pays 3 to 5 separate gas fees just to enter a single yield position. Superform collapses that into one click.

The user experience

A user holds USDC on Base. They see a Pendle vault on Arbitrum yielding 12 percent. They tap Deposit. Behind the scenes, Superform bridges its USDC swaps if needed and deposits. The user just watches it happen.

2. Cross-Chain Withdrawals

Users can withdraw from any vault directly to their preferred chain, even if that is not where the vault lives.

Why it matters

Most protocols trap users. A user deposits from Ethereum they must withdraw to Ethereum. Superform asks, “Where do you want your money?” Arbitrum Base: a bank account via Bridge. Done.

The user experience

A user has been earning yield on an Avalanche vault for six months. They need cash for rent. They withdraw select Send to Base funds, and the funds arrive on their preferred network. The vault never even knows they left.

3. Instant Swaps Memecoins Meet Maturity

Users can trade any crypto for any other crypto across 7 plus chains with built-in bridging. Yes, that includes the memecoin a friend recommended at 2 AM.

Why it matters

Swaps usually require liquidity pools and specific pairs. Superform routes through DEXes, bridges, and aggregators simultaneously to find the best path, then executes it in one tap.

The user experience

A user holds ETH on Arbitrum. They want DOGE on Dogechain. Normally, this is a three-step nightmare. On Superform, it’s a one-tap process. The app handles the how. The user just sees what.

4. Send to Addresses

Users can send stablecoins or crypto directly to any on-chain address or to a bank account via Bridge integration.

Why it matters

Crypto has always been great at moving value globally and terribly at moving it to a recipient’s checking account. Superform bridges that gap without becoming a bank.

The user experience

A friend owes a user 50 dollars. That friend is not on-chain. The user types a phone number, sends USDC, and the friend receives USD in their bank account. They never know crypto was involved. The user never leaves the app.

5. Portfolio Builder

Users can construct and manage custom yield portfolios from hundreds of opportunities across chains, all in one unified dashboard.

Why it matters

DeFi yield is fragmented across protocol chains and risk profiles. Portfolio Builder turns chaos into clarity. Want 30 percent Aave, 30 percent Morpho, 20 percent Pendle, 20 percent stablecoin lending, drag and drop deposit.

The user experience

Users are not chasing APYs anymore. They are building an allocation. The dashboard shows total exposure, projected returns, and risk concentration. It looks like a fintech app. It behaves like a hedge fund terminal.

6. Auto-Optimization

SuperVaults automatically rebalance users’ capital into the highest performing strategies, compounding yield without constant attention.

Why it matters

The best yield changes weekly, sometimes daily. Users should not have to. SuperVaults monitor the market, detect rate shifts, and move funds accordingly while users sleep, work, or touch grass.

The user experience

A user deposits 10000 dollars into superUSDC. They do nothing else. Three months later, they check, and they have outperformed every static stablecoin position they ever manually managed. The vault did the work. The user just provided the capital.

7. Virtual Payroll Users Salaries Smarter

A Bridge-powered virtual bank account that automatically converts users’ paychecks into stablecoins and routes them into yield-generating SuperVaults.

Why it matters

Getting paid in fiat, manually buying crypto, and manually depositing into DeFi are friction points. Virtual Payroll eliminates them entirely.

The user experience

A user provides their employer with their Superform account details. Payday arrives. Their USD salary deposits are converted to USDC and distributed across their chosen vault allocations. They never touched it. It just started earning.

How Does the Superform App Work?

Superform abstracts bridging, swapping, and routing into one execution layer so you can deposit from any supported chain without manual steps. It programmatically allocates capital into vault contracts and may optimize yield across networks in the background. You choose the strategy, and the system handles settlement and compounding automatically.

1. Earn: The Permissionless Yield Marketplace

When a user taps “Earn,” the deposit does not go into Superform. The deposit goes into a vault, perhaps on Arbitrum, perhaps on Base, perhaps on a chain the user has never interacted with before.

The Old Way

In the traditional flow, a user must manually bridge USDC to Arbitrum, then swap USDC for GLP, approve GLP for the vault contract, and finally deposit into the vault. This process requires signing four to five separate transactions and waiting several minutes for confirmations across chains before capital is fully deployed.

The Superform Way

With Superform, a user simply selects a vault, taps Deposit, signs one transaction, and waits a few seconds for execution. The protocol abstracts bridging, swapping, and routing into a single atomic flow, enabling capital to move across chains and into the target vault without manual coordination.

How it works: Superform deploys a network of Spoke Contracts on every supported chain. When you deposit USDC on Ethereum into a vault on Arbitrum, your USDC is simultaneously:

- Swapped for the vault’s required asset (via Li.Fi or Socket)

- Bridged to Arbitrum (via LayerZero/Wormhole/Hyperlane)

- Deposited into the vault contract

- Minted into a SuperPosition (ERC-1155A) receipt

All of this occurs in one atomic transaction. If any step fails, the swap slips, the bridge delays, or the vault rejects the entire transaction reverts. Funds never leave the user’s custody mid-flight.

2. SuperPositions: The ERC-1155A Breakthrough

This is the single most misunderstood feature of Superform, and arguably its greatest technical achievement.

The Problem: Traditional DeFi receipts are ERC-20 tokens. If a user deposits into Aave, the result is aUSDC. If a user deposits into Morpho, the result is mUSDC. These tokens are incompatible. A user cannot use aUSDC as collateral on Morpho without wrapping, unwrapping, or accepting liquidation risk.

The Superform Solution: When a user deposits capital, a SuperPosition is issued, an ERC 1155A token representing a specific position in a specific vault on a specific chain. ERC 1155A is transmutable.

Transmutation enables the conversion of a complex chain-specific vault-specific position into a standard ERC 20 token that any DeFi protocol can recognize. The cross-chain yield position becomes:

- Tradeable on Uniswap

- Usable as collateral on Aave

- Transferable to friends

- Composability without compromise

The website calls this making “fragmented yield” into a “unified, liquid layer.” In engineering terms, they’ve solved the liquidity fragmentation problem without forcing users to choose between yield and flexibility.

3. Validator-Secured Vaults

Superform is permissionless. Anyone can deploy a vault. Anyone can list strategies. This enables scaling by aggregating opportunities from more than 50 protocols, but it also introduces risk.

The Scam Vector: A malicious actor deploys a vault that promises 500% APY. Users deposit. The actor runs away with the money.

Superform’s Defense: A decentralized network of bonded validators.

Here’s the economic game theory:

- Validators must stake capital (in $UP tokens) to participate

- Validators review vaults and attest to their legitimacy

- If a validator approves a malicious vault, their stake is slashed—partially burned, partially distributed to victims

- Honest validators earn fees from protocol revenue

This is what CMT Digital means by “validator-secured vaults.” It’s not just code audits (though Superform has those from yAudit and Spearbit). It’s economic security. The cost of lying exceeds the potential profit.

The website promises “First Class Security” and “Boringly Reliable.” This validator mechanism is how they deliver it.

4. Multi-AMB Quorum

Cross-chain applications depend on messaging bridges. That dependency creates systemic risk. If an application relies solely on LayerZero and LayerZero fails, the application fails. If it relies only on Wormhole, and Wormhole halts operations, the application stalls.

Superform’s Innovation: The Multi-AMB Quorum.

For high-value transactions, Superform requires verification from multiple Arbitrary Messaging Bridges before finalizing a deposit or withdrawal.

- LayerZero confirms: “Yes, 1000 USDC arrived on Arbitrum.”

- Wormhole confirms: “Yes, 1000 USDC arrived on Arbitrum.”

The transaction finalizes. If one bridge is compromised or delayed, the others provide redundancy. If two bridges disagree on a transaction, the transaction pauses, and DAO governance resolves the discrepancy. This architecture reduces dependence on a single bridge and improves resilience for institutional-scale capital flows.

5. Save & Send: The Bridge to Fiat

The website’s “Save” and “Send” features reveal Superform’s long-term ambition: becoming the onramp and offramp for the global economy.

Save:

A user can create a virtual bank account powered by Bridge so income may automatically convert into stablecoins.

Superform partners with Bridge, a fiat-to-crypto infrastructure provider, to issue virtual bank accounts. Employers deposit USD. Bridge converts the funds to USDC. Superform automatically deposits USDC into the selected yield vault on a predefined schedule, without requiring the user to interact with the wallet.

Send:

A user can send stablecoins or initiate payments to traditional bank accounts directly from the Superform wallet balance.

When funds are sent to a bank account, Superform does not transfer crypto to the recipient. Stablecoins are burned on chain, and Bridge executes a wire transfer to the recipient’s bank. The recipient receives USD in a bank account without interacting with wallets or gas fees.

This structure applies chain abstraction to fiat settlement rails. The recipient does not need to understand decentralized finance infrastructure, while settlement logic remains programmable on-chain.

How Much Does it Cost to Develop a DeFi App like Superform?

Building a DeFi app like Superform demands precise architecture and disciplined engineering, and we follow a cost-effective approach that protects both performance and capital. We focus on modular design and phased execution so our clients can scale efficiently without unnecessary overhead.

Phase 1: Architecture & Strategic Blueprint

Focus: Designing the Hub-and-Spoke model and selecting interoperability layers such as LayerZero, CCIP, or Wormhole.

| Step | Sub-Step | Estimated Cost (USD) |

| 1. Design Architecture | Select Hub chain & define Registry logic | $15,000 – $25,000 |

| 1. Design Architecture | Choose & test AMB (Bridge) integrations | $10,000 – $20,000 |

| 1. Design Architecture | Map cross-chain liquidity routing | $10,000 – $15,000 |

| Phase 1 Total | $35,000 – $60,000 |

This phase determines whether your protocol scales cleanly or collapses under fragmented liquidity.

Phase 2: Router & Intent Engine Development

Focus: Building intent-based execution logic and solver integrations.

| Step | Sub-Step | Estimated Cost (USD) |

| 2. Router & Intent Engine | Intent-based logic & Swap + Bridge bundling | $40,000 – $70,000 |

| 2. Router & Intent Engine | Solver network integration & Slippage protection | $20,000 – $35,000 |

| Phase 2 Total | $60,000 – $105,000 |

This is where complexity spikes. The protocol must coordinate multiple chains and liquidity paths atomically.

Phase 3: SuperPosition & Vault Infrastructure

Focus: ERC-1155 multi-token design and ERC-4626 vault composability.

| Step | Sub-Step | Estimated Cost (USD) |

| 3. SuperPosition System | ERC-1155 Multi-token contracts & Batch logic | $30,000 – $50,000 |

| 3. SuperPosition System | ERC-4626 Vault adapters & Composability hooks | $25,000 – $40,000 |

| Phase 3 Total | $55,000 – $90,000 |

This layer enables yield abstraction across chains while preserving position composability.

Phase 4: State Synchronization & Indexing

Focus: Real-time cross-chain state management.

| Step | Sub-Step | Estimated Cost (USD) |

| 4. State Synchronization | Registry contracts & Global event listeners | $20,000 – $40,000 |

| 4. State Synchronization | Backend indexing (The Graph / Goldsky) | $15,000 – $25,000 |

| Phase 4 Total | $35,000 – $65,000 |

Cross-chain state mismatches are among the largest failure vectors in omnichain systems.

Phase 5: Gas Abstraction & UX Layer

Focus: Account abstraction and omnichain dashboard.

| Step | Sub-Step | Estimated Cost (USD) |

| 5. Gas Abstraction | ERC-4337 Smart Accounts & Paymaster logic | $30,000 – $55,000 |

| UX Development | Omnichain Dashboard & Mobile compatibility | $40,000 – $75,000 |

| Phase 5 Total | $70,000 – $130,000 |

User experience becomes critical at this stage. Gas abstraction significantly improves onboarding and retention.

Phase 6: Security, Audits & Launch

Focus: Protocol defense against cross-chain exploits and economic manipulation.

| Step | Sub-Step | Estimated Cost (USD) |

| 6. Security Defense | Quorum verification & Circuit breakers | $20,000 – $40,000 |

| 6. Security Defense | Third-party audits (Minimum 2 firms) | $80,000 – $150,000+ |

| Deployment | Multi-chain deployment & Gas provisioning | $5,000 – $15,000 |

| Phase 6 Total | $105,000 – $205,000+ |

This is a strategic estimate based on scope and complexity, with a projected total cost ranging from $250,000 to $650,000+, depending on chain integrations and feature depth.

Final pricing always depends on your exact architecture, security model, and roadmap priorities. For a more accurate quote tailored to your vision, feel free to connect with us for a free consultation.

Factors Affecting the Cost of a DeFi App like Superform

When you build an omnichain yield marketplace, costs do not scale linearly. It expands based on architectural depth, interoperability design, and security surface area. Here are the core variables that materially influence development investment and how they actually move your budget.

1. Number of Chains Integrated

Each additional chain increases complexity in messaging, liquidity routing, and state synchronization. Supporting 2 chains is infrastructure work. Supporting 6 or more becomes distributed systems engineering with significantly higher testing and audit requirements.

Cost Fluctuation:

- $45K to $65K for 2 EVM chains

- $95K to $140K for 6+ chains, including non-EVM networks like Solana

2. Cross-Chain Messaging Protocol Selection

Choosing between LayerZero, CCIP, Wormhole, or a hybrid model affects integration time and security architecture. Some solutions require deeper custom verification layers, which increase engineering and audit costs.

Cost Fluctuation:

- $25K to $40K for single bridge integration

- $70K to $110K for multi-AMB quorum systems with failover logic

3. Intent Engine Sophistication

A basic routing engine is far less complex than a solver-based intent marketplace with slippage protection, MEV resistance, and dynamic path optimization. The more autonomous and capital-efficient the engine becomes, the more backend logic and economic modeling it requires.

Cost Fluctuation:

- $35K to $55K for basic Pathfinder

- $90K to $150K+ for solver network with Dutch auctions and rescue mechanisms

4. Vault and Yield Adapter Complexity

Integrating simple ERC 4626 vaults is manageable. Building dynamic yield adapters across multiple protocols with composability hooks and rebalancing logic significantly increases the scope of smart contracts and audit depth.

Cost Fluctuation:

- $30K to $50K for 5 to 10 standard vaults

- $80K to $130K for 50+ protocols with custom adapters and SuperPosition contracts

5. Gas Abstraction and Account Abstraction

Implementing ERC-4337 smart accounts, paymasters, and meta-transaction support improves user onboarding. However, it adds infrastructure overhead, relayer services, and security considerations that increase cost.

Cost Fluctuation:

- $20K to $35K for basic gas sponsorship

- $60K to $95K for full account abstraction stack with paymaster bundlers and session keys

Is Liquidity Ownership Necessary to Launch a Yield Marketplace?

Liquidity ownership is not required when users are building an aggregation-based yield marketplace that routes capital into existing vaults. Users should prioritize cross-chain adapters and routing logic, as infrastructure typically provides stronger defensibility than treasury-funded TVL. Owned liquidity may validate safety in some cases, but it does not define scalability.

The Old Playbook

The intuition makes sense. If you build a DEX, you need liquidity pairs. If you build a lending market, you need deposits. If you build a yield aggregator, you need vaults with assets in them.

So naturally, when founders design a yield marketplace, they assume the critical path is:

- Raise $10M–$50M

- Deploy it into your own vault strategies

- Display impressive APYs to attract retail

- Hope organic users replace treasury funds before the yield farming incentive program ends

This worked in 2021. It is financial suicide in 2026.

A. The Liquidity Provider Has Become the Customer

In 2021, LPs were mercenaries. They chased the highest APY, dumped the token, and left. Today, sophisticated LPs expect protocol ownership, governance rights, and sustainable fee models. Treating them as seed capital rather than core users creates immediate misalignment.

B. The Cost of Yield Farming Has Exploded

With Protocol Owned Liquidity POL, you bear 100 percent of the downside and zero percent of the upside. You pay gas. You pay slippage. You pay opportunity cost. And you get no loyalty. When yields normalize, your liquidity exits instantly.

You absorb the risk. The market absorbs the upside.

C. Permissionless Vaults Kill the Need for Inventory

This is the critical shift that most founders miss. In 2026, you do not need to own the yield-generating assets. You need to aggregate them.

The Superform Model: Liquidity Agnosticism.

Superform does not own the liquidity in its vaults.

Superform owns the router, the ERC-1155A position standard, and the validator network, where participants stake UP tokens to verify vault data and face slashing for malicious behavior. The liquidity itself belongs to:

- The protocols that created the vaults Aave, Morpho, Pendle, Euler

- The users who deposited into those vaults via Superform

- The LPs who provided the underlying assets

Superform is a marketplace, not a supplier. With $144M in TVL and over 150,000 users, it has achieved escape velocity without deploying a single dollar of owned liquidity into its own vaults.

This distinction is everything.

The Two Types of Yield Marketplaces

To determine whether you need owned liquidity, you must first identify the type of yield marketplace you are building.

Type A: The Principal Marketplace

You originate the yield.

Examples: Pendle, Sense, Swivel.

These protocols create new yield-bearing assets by splitting principal and yield. They require deep, self-owned liquidity to bootstrap the initial markets because the assets do not exist elsewhere.

Verdict: Liquidity ownership is likely necessary.

Type B: The Aggregation Marketplace

You surface existing yield.

Examples: Superform, Yearn, Beefy.

These protocols do not create new primitives. They aggregate and route capital to existing primitives. The vaults already exist. The strategies already work. The yields are already being generated.

Verdict: Liquidity ownership is a tax, not a requirement.

If you are building a Type B marketplace, which describes 90 percent of yield platform pitches today, owning liquidity is not just unnecessary. It is actively counterproductive.

The Trap: When Aggregators Try to Act Like Principals

The most expensive mistake in DeFi right now is the Type B protocol trying to operate like Type A.

We see this constantly. A founder building a yield aggregator raises $20M and immediately deploys $15M into their own vaults. They point to the TVL chart and call it traction. They point to APY and call it product-market fit.

TVL funded by your treasury is not traction. It is accounting.

Then the treasury needs to rebalance. Or the market turns. Or the token unlocks hit. And that $15M exits, taking 75 percent of their TVL.

The market does not distinguish between owned liquidity and user liquidity.

It only shows the chart declining.

Five Pillars DeFi 5PT launched in late 2025 with a very different approach. Over $5 million in liquidity locked for a full decade, backed by real-world assets across five asset classes. This is the extreme opposite of the Superform and Yearn model. It is liquidity ownership as the entire value proposition.

For 5PT, owned liquidity is not a bootstrap mechanism. It is the product. The token is the vault. This is valid for their specific use case. But it is not yield aggregation. It is asset-backed tokenization.

If you are building a marketplace, you are not Five Pillars. Do not let the success of locked liquidity models in adjacent verticals trick you into believing they apply to yours.

The Alternative: Permissionless Liquidity Bootstrapping

How do you launch a yield marketplace without owning the liquidity?

Step 1: Build the Adapter Layer

The real moat of a modern yield marketplace is not treasury size but integration depth. Users should build standardized adapters so that any compliant vault can list with minimal friction. Seamless onboarding may drive scale without relying on owned capital.

This means:

- Supporting the ERC 4626 standard out of the box

- Building adapters for non-standard vault implementations

- Creating a permissionless factory contract that requires no manual approval

When listing requires a multi-signature vote and a two-week integration timeline, you are bottlenecking supply.

When listing is a five-minute permissionless transaction, supply becomes infinite.

Step 2: Incentivize the Suppliers

Traditional DeFi protocols spend millions bribing depositors with farm tokens. Capital-efficient yield marketplaces do the opposite. They pay the vaults, not the users.

If you are a vault creator with $10M in deposits on Aave or Morpho, what would convince you to also list on Superform?

- Access to a new user base

- Cross-chain messaging infrastructure

- Validator verification that increases user trust with slashing protections

- Fee rebates for early adopters

You pay vaults in infrastructure and distribution, not in inflationary token emissions.

Superform’s UP token is explicitly designed as a coordination token rather than a profit-sharing or yield-farming token. Validators stake it. Strategists post bonds with it. Governance participants lock it for sUP.

It is not emitted to attract mercenary liquidity.

Step 3: Bootstrap Demand Through Intent

You do not need $50M in owned liquidity to demonstrate that your platform works. You need one user with one deposit.

Build the product. Show that the routing works. Show that the positions are composable. Show that the validator quorum prevents fraud.

Then go to the protocols and say:

“We have built the infrastructure for you to access 10 new chains and 100,000 new users. List your vault. We take no cut for the first 6 months. You keep 100 percent of fees.”

This is how you bootstrap supply without a balance sheet.

When Should You Own Liquidity?

There are specific, narrow cases where owned liquidity is strategically defensible.

- To demonstrate technical safety: A small, transparent deployment of treasury funds $500k to $2M into your own highest conviction vaults can signal dogfooding. It shows you are willing to put capital behind your own contracts.

- To subsidize novel strategy creation: If you are incubating entirely new yield strategies that do not exist elsewhere, such as complex cross-point farming loops, you may need to seed the first iteration to prove the mechanism.

As part of a balanced liquidity incentive program, protocol-owned liquidity can be one of many tools. The mistake is making it the only tool.

Conclusion

Building a DeFi app like Superform is not about copying an interface. You must design cross-chain routing logic, intent-based execution layers, and hardened smart contract systems that can scale securely. The investment may range from one hundred eighty thousand to five hundred thousand dollars or more, depending on protocol depth and audit scope, but if structured correctly, it can steadily generate yield-driven revenue and strategically position your business at the core of decentralized financial infrastructure.

Looking to Develop a DeFi App like Superform?

IdeaUsher can architect your DeFi app, such as Superform, from protocol design through audited smart contracts to scalable frontend systems. We would carefully structure cross-chain routing, yield-vault logic, and governance layers to enable your platform to securely manage liquidity at scale.

Our team of ex-MAANG/FAANG engineers brings 500,000+ hours of production blockchain experience to your project.

What we actually build:

- Multi-AMB Quorum systems — No single bridge failure points

- ERC-1155A SuperPosition contracts — Composable yield that moves across chains

- Intent-based routers — One-click deposits from any chain to any vault

- Validator slashing logic — Economic security, not just code audits

- Mobile-first interfaces — Because your users expect Robinhood, not Etherscan

FAQs

A1: Building a DeFi app like Superform is not a weekend project, and you should realistically plan for six to nine months for a solid MVP. That timeline usually includes smart contract engineering, frontend integration protocol integrations, and at least one full security audit. If you want cross-chain routing, advanced yield strategies, and governance modules, the cycle may extend further because testing and validation must be done very carefully.

A2: You can build a DeFi yield marketplace without cross-chain support, and it will still function correctly on a single network. However, you may quickly notice liquidity fragmentation, as capital now moves across multiple chains. If you limit deployment to a single ecosystem, the protocol may struggle to aggregate competitive yields, and user growth may slow over time.

A3: For yield marketplaces that manage multiple vault positions, ERC-1155 can be more technically efficient than ERC-20. It allows you to represent multiple strategy tokens within one contract, and batch transfers can significantly reduce gas usage. If your design involves dynamic position minting and multi-asset accounting, this standard will often provide better operational flexibility.

A4: In most serious DeFi builds the largest cost driver is security architecture and formal audits. Smart contracts that manage pooled liquidity must be rigorously verified, as a single exploit could permanently damage the protocol. Cross-chain messaging infrastructure also adds complexity, and audit scope increases substantially when bridges and routing logic are involved.