(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

For many years, crypto platforms primarily served retail traders, while large financial institutions remained cautious. The interest from banks and hedge funds was always present, yet they required stronger governance and clear regulatory structures. The popularity of crypto bank platforms has started increasing because institutions now need regulated custody and reliable asset protection.

Financial firms must also carefully manage compliance requirements for digital assets. Modern crypto banking infrastructure can therefore provide institutional-grade security and controlled transaction environments. These systems may also integrate auditing and risk monitoring tools for regulated operations.

Over the past decade, we have developed numerous crypto bank solutions powered by programmable compliance architecture and MPC-based digital asset custody frameworks. With this experience behind us, we are sharing this blog to break down the practical steps required to build a compliant crypto bank platform like Anchorage.

Why Federally Chartered Crypto Banks Are Gaining Trust?

According to Data Bridge Market Research, the cryptocurrency banking market was valued at USD 1.49 billion in 2021 and is expected to reach USD 2.52 billion by 2029, at a CAGR of 6.80% during the forecast period. This steady growth reflects a fundamental shift toward institutional-grade infrastructure. Federally chartered crypto banks now bridge the gap between digital assets and the Office of the Comptroller of the Currency.

Source: Data Bridge Market Research

Federal charters provide a seal of approval, ensuring banks meet the same capital and liquidity requirements as national commercial banks. As digital assets move onto corporate balance sheets, the risks of unregulated exchanges have become unacceptable. This regulatory alignment allows institutions to move away from fragmented state level trusts toward unified national providers.

Federal Charters and Institutional Adoption

Federal charters provide the legal operating system required by pension funds and insurance companies. An OCC charter from the National Trust Bank simplifies multi-state operations by providing a preemptive legal framework. Instead of managing dozens of state licenses, a chartered bank operates under a single set of federal rules.

The GENIUS Act further clarifies this role by establishing frameworks for stablecoins and reserve management. Federal oversight transforms digital assets into auditable, bankable classes. This facilitates the tokenization of real-world assets like U.S. Treasuries by providing a regulated environment for institutional participation.

Why Regulated Custody Matters

For hedge funds, custody is about bankruptcy remoteness and asset segregation. Regulated custody ensures client assets are held in a fiduciary capacity, separate from the bank’s own balance sheet. This protects clients from becoming unsecured creditors if a provider fails, as federal law mandates strict asset separation.

Professional managers also utilize chartered banks to satisfy the SEC’s Qualified Custodian requirements. Partnering with a federal entity enables access to prime brokerage and automated settlement within a supervised perimeter. This reduces the operational risk and cost associated with moving assets between multiple unregulated providers.

What Makes Anchorage a Unique Crypto Banking Platform?

Anchorage Digital redefined institutional participation by moving beyond simple cold storage. It treats digital assets with the same legal and operational discipline as traditional equities, bridging the gap between decentralized protocols and Tier-1 financial oversight.

Federally Chartered Infrastructure

Anchorage holds a national trust charter from the Office of the Comptroller of the Currency. This elevates it above state-regulated entities, providing a uniform federal framework that simplifies compliance for global institutions.

- Fiduciary Standard: It operates as a qualified custodian, meeting the highest legal requirements for asset protection.

- National Preemption: A single regulatory standard replaces the need for a fragmented patchwork of state-by-state licenses.

- Institutional Trust: This charter puts the platform on equal footing with major Wall Street banks.

Secure Institutional Custody

The platform eliminated the trade-off between security and liquidity. By utilizing FIPS 140-2 Level 3 HSMs, Anchorage provides warm storage where assets are instantly accessible for trading but protected by hardware-enforced governance.

Key Innovation: Anchorage replaced manual paper in safes cold storage with biometric-based, multi-user quorums. This removes human error and single points of failure while allowing for 24/7 transaction execution.

Integrated Trading and Staking

Anchorage functions as a full-stack prime broker. Instead of moving assets between disconnected exchanges and custodians which introduces counterparty risk, clients manage the entire lifecycle in one place.

- Staking: Clients earn rewards directly from their secure vaults.

- Settlement: Instant, internal settlement through the Atlas network.

- Trading: Access to deep, aggregated liquidity with no slippage from asset transfers.

Global Regulatory Approach

Rather than moving fast and breaking things, Anchorage secures licenses before entering new jurisdictions. This proactive stance ensures long-term stability and bankruptcy-remote protection for client funds.

- United States: OCC National Bank Charter and NY BitLicense.

- Singapore: Major Payment Institution (MPI) license via MAS.

- Europe: Strategic presence in Portugal to navigate EU digital asset frameworks.

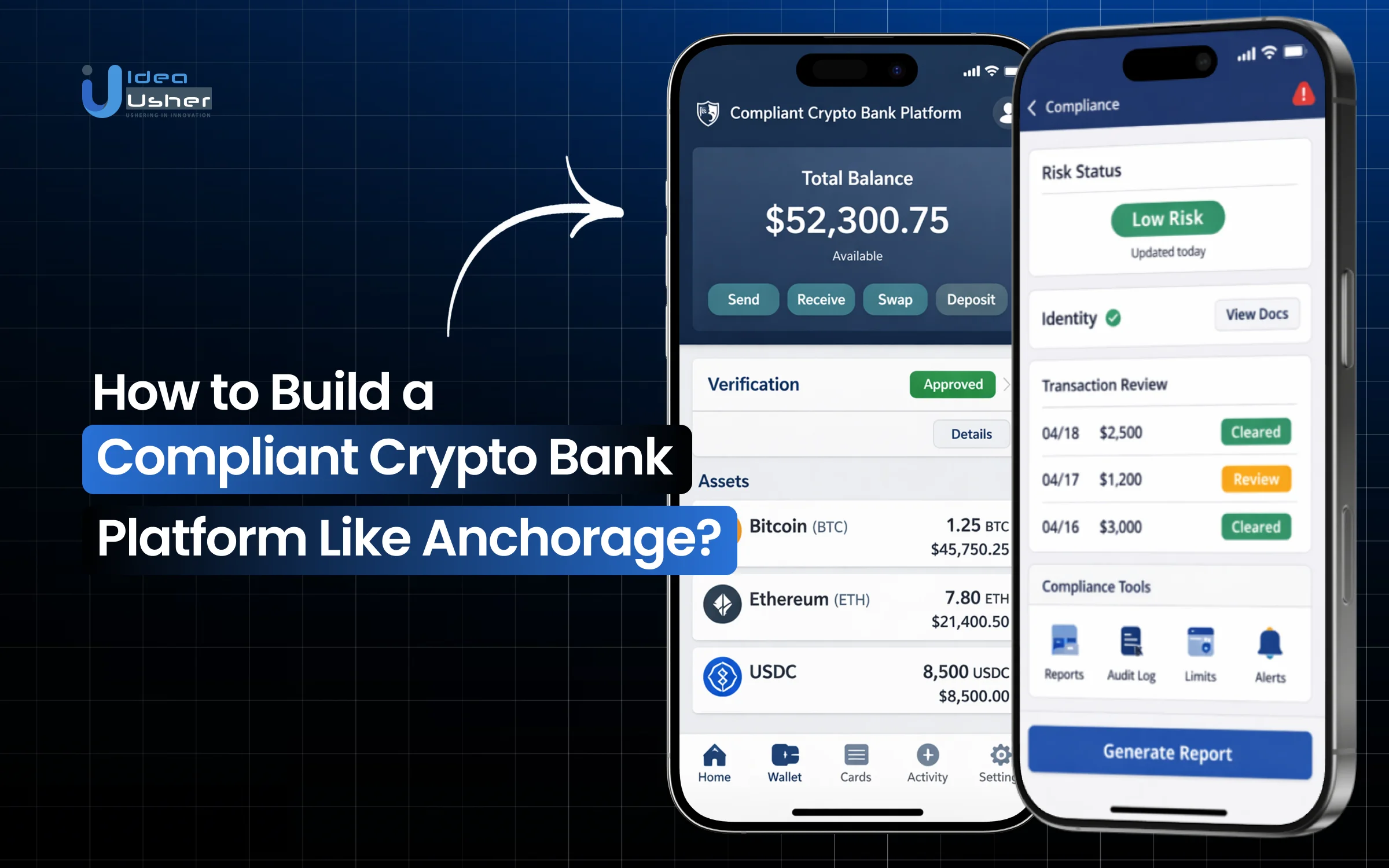

Core Features of a Crypto Bank Platform Like Anchorage

Building a crypto bank platform like Anchorage requires a shift from retail-centric models to infrastructure designed for the highest tiers of global finance. A crypto bank does not just hold assets; it provides a comprehensive operating system for digital wealth, ensuring every transaction is governed by strict institutional protocols.

1. Institutional Custody System

The bedrock of the platform is a custody solution that moves beyond the limitations of traditional cold storage. By utilizing FIPS 140-2 Level 3 Hardware Security Modules, the system ensures that private keys are never exposed in a vulnerable state.

- Warm Storage Efficiency: Assets remain “warm,” meaning they are cryptographically secure but immediately accessible for institutional workflows.

- Bankruptcy Remoteness: The legal architecture ensures client assets are segregated from the bank’s own balance sheet, protecting them from creditors.

- Audit Transparency: Real-time on-chain verification provides clients and regulators with constant visibility into asset reserves.

2. Multi-layer Key Management

Security is achieved through Multi-Party Computation, which eliminates the single point of failure inherent in traditional private keys. Instead of a single key, multiple “shards” are generated and distributed across isolated environments.

- Distributed Governance: No single individual can authorize a withdrawal; transactions require a quorum of approved signers.

- Biometric Enforcement: Identity verification is tied to physical biometric data rather than easily compromised passwords.

- Policy Engines: Organizations can set granular limits on transaction sizes, whitelisted addresses, and time-based approvals.

3. Trading and Liquidity Routing

To serve large-scale investors, the platform must offer deep liquidity without the price slippage common on retail exchanges. This is achieved through sophisticated Smart Order Routing (SOR).

Strategic Edge:

By aggregating liquidity from multiple top-tier exchanges and over-the-counter (OTC) desks, the platform ensures that a multi-million dollar buy order is executed at the best possible global price.

This infrastructure allows for seamless execution of large blocks while maintaining the anonymity and security of the client’s core custody account.

4. Settlement and Transfer Controls

A compliant platform must mitigate delivery-versus-payment risks. The settlement layer acts as a trusted intermediary, ensuring that assets and fiat currency change hands simultaneously and securely.

- Internal Ledger Settlement: Transfers between clients on the same platform happen instantly off-chain, reducing gas fees and latency.

- Strict Whitelisting: Assets can only be sent to pre-vetted, verified addresses, drastically reducing the risk of fraud or accidental loss.

- Speed and Finality: Modern settlement networks provide near-instant finality, a critical requirement for high-frequency institutional trading.

5. Staking and Yield Infrastructure

Institutional clients increasingly view digital assets as productive capital. The platform must provide safe, compliant access to protocol-level rewards through staking.

| Feature | Institutional Requirement |

| Direct Staking | Assets remain in custody while participating in network consensus. |

| Validator Selection | Only high-repute, audited validator nodes are utilized to minimize slashing risk. |

| Reporting | Automated tax and accounting reports for all generated rewards and yields. |

6. Institutional Compliance Dashboards

For a regulated bank, transparency is the final product. A dedicated compliance dashboard provides the data necessary for clients to satisfy their own internal and external auditors.

The dashboard integrates AML and Know Your Transaction tools directly into the UI. This allows compliance officers to monitor the “travel rule” status of every incoming and outgoing transfer. It also provides automated SOC 1 and SOC 2 Type II reports, ensuring the platform meets the highest standards for operational security and financial reporting.

Regulatory Frameworks Needed for a Crypto Bank Platform

Operating a crypto bank is a regulatory undertaking disguised as a technology project. The primary barrier to entry is satisfying the requirements of financial oversight bodies. A robust framework provides the legal certainty required for institutional capital to enter the digital asset space with confidence.

1. US Federal Banking Regulations

The gold standard for US crypto banking is the National Trust Charter from the Office of the Comptroller of the Currency. This allows an entity to operate as a bank dedicated specifically to digital assets.

- Fiduciary Responsibility: Assets are strictly segregated from the bank’s operational funds.

- Capital Requirements: Regulators mandate liquidity ratios to ensure resilience during market volatility.

- Safety and Soundness: Platforms undergo rigorous examinations of IT infrastructure and internal management.

2. Licensing for Custody

Different business models require specific licensing paths. Not every platform requires a full federal charter to be successful.

- State Trust Company: Often started via the NY DFS, this offers a path to becoming a qualified custodian.

- Special Purpose Depository Institution (SPDI): A Wyoming model allowing digital asset banking without lending requirements.

- Qualified Custodian Status: Essential for SEC-registered investment advisers to manage pension and endowment funds.

3. KYC, AML, and Monitoring

Anti-money-laundering and Know Your Customer protocols are the frontline defense. For a crypto bank, these must be automated and continuous.

- Identity Verification: Multi-factor checks, including biometric liveness and global PEP screening.

- The Travel Rule: Compliance with FATF Recommendation 16 for the exchange of identifying information.

- Real-time KYT: Using tools like Chainalysis to scan for tainted funds before transactions are processed.

4. Institutional Compliance Architecture

Compliance must be baked into the software architecture. This creates a permissioned environment within the permissionless world of blockchain.

Strategic Implementation:

Platforms use a Compliance-as-Code approach. If a transaction lacks a Travel Rule packet or triggers a high-risk flag, the system automatically freezes the movement of funds.

This architecture ensures an immutable audit trail. Every action and automated check is logged in a tamper-proof manner, simplifying annual audits into a streamlined data export process.

How to Develop a Crypto Bank Platform like Anchorage?

To develop a crypto bank like Anchorage, you must build secure custody systems that protect digital assets and support regulated transactions. The platform may also integrate blockchain settlement and compliance monitoring to support institutional crypto banking.

We have built multiple crypto banking platforms similar to Anchorage for our clients, and here is how we usually develop them.

1. Institutional Asset Strategy

We begin by architecting a product roadmap tailored to your specific institutional demographic, whether that involves corporate treasuries or sovereign wealth funds. We curate an asset list based on liquidity and regulatory status, ensuring your platform supports core assets alongside sophisticated yield-bearing instruments and governance tokens.

2. Compliance-First Architecture

We design your system with compliance as the foundational layer, isolating sensitive core ledgers from public-facing interfaces. Our architects implement strict Role-Based Access Control and geographic redundancy, ensuring your platform remains resilient to attacks and compliant with the operational standards required by federal regulators.

3. Hardened Custody Infrastructure

We deploy a warm custody solution that replaces archaic cold storage with high-velocity, high-security Multi-Party Computation. By sharding private keys across FIPS 140-2 Level 3 HSMs, we enable your clients to execute transactions 24/7 through biometric-backed approval quorums, eliminating any single point of failure.

4. Native Node Integration

To ensure your bank has direct, unmediated access to the chain, we build and manage dedicated, load-balanced node clusters. This infrastructure allows for real-time transaction indexing and sophisticated gas-price management, ensuring that institutional-scale transfers are never delayed by network congestion or third-party provider failures.

5. Trading and Settlement Layer

We bridge your internal ledger with global liquidity by integrating Smart Order Routing that connects to top-tier OTC desks and exchanges. This allows us to provide your clients with atomic settlement or near-instant internal transfers and best-in-class execution prices for even the largest block trades without causing market slippage.

6. Automated Monitoring Deployment

The final layer involves embedding automated oversight directly into the transaction flow. We integrate real-time KYT and Travel Rule protocols, creating an immutable audit trail that automates SAR reporting and ensures your platform remains a clean, compliant environment for institutional participation.

Cost to Build a Crypto Bank Platform Like Anchorage

Building an institutional crypto bank is a capital-intensive venture where the primary expenses are driven by the uncompromising need for security and legal standing. You are not just building an app; you are building a fortified financial institution. The budget must account for both the initial engineering sprint and the ongoing operational rigors of a regulated entity.

Infrastructure and Security Development Costs

The core technical spend focuses on creating a zero-trust environment. Unlike standard fintech, a crypto bank requires specialized hardware and cryptographic expertise.

- MPC and HSM Integration: Developing or licensing FIPS 140-2 Level 3 HSMs and MPC protocols typically ranges from $250,000 to $600,000.

- Security Audits: Institutional clients demand multiple third-party audits (SOC 1, SOC 2 Type II, and penetration testing), which can cost $100,000 to $200,000 annually.

- Architecture Engineering: Building the redundant, isolated backend systems requires a senior team of blockchain and security engineers, with payroll often exceeding $500,000 for the initial build phase.

Compliance and Licensing Expenses

Regulatory capital is often the largest “hidden” cost. These expenses vary significantly based on the jurisdiction and the specific charter pursued.

Professional Insight:

Licensing is not a one-time fee but an ongoing capital commitment. For example, an OCC National Trust Charter requires significant “capital under management” and high-tier legal counsel to navigate the application process.

| Expense Category | Estimated Cost Range |

| Legal Counsel & Filings | $200,000 – $500,000+ |

| Regulatory Capital Reserves | $2,000,000 – $10,000,000+ (Varies by Charter) |

| AML/KYC Software Licenses | $50,000 – $150,000 (Annual) |

Blockchain Integration and Maintenance Costs

Maintaining direct connectivity to multiple blockchains requires a dedicated DevOps infrastructure. This is a recurring operational expense that scales with the number of supported assets.

- Node Infrastructure: Running dedicated, high-availability nodes for BTC, ETH, and other protocols can cost $5,000 to $15,000 per month in cloud compute fees.

- Custom Indexing: Building and maintaining proprietary indexers to ensure data accuracy for client balances requires ongoing engineering support.

- Gas and Bridge Management: Managing liquidity and transaction fees for the platform’s own settlement layer requires a standing float of digital assets.

Estimated Timeline for Development

Developing a platform of this complexity is a marathon, not a sprint. The timeline is often dictated more by regulatory approval windows than by coding speed.

- Phase 1: Discovery & Architecture (Months 1–3): Defining the legal framework and designing the security schematics.

- Phase 2: Core Development (Months 4–10): Building the MPC custody engine, node infrastructure, and internal ledger.

- Phase 3: Integration & Testing (Months 11–14): Connecting liquidity providers, finishing compliance dashboards, and undergoing rigorous security audits.

- Phase 4: Regulatory Licensing (Months 6–24+): This phase runs in parallel with development but often extends well beyond the technical completion date.

Total estimated time to market for a fully compliant, federally chartered platform is typically 18 to 24 months, though a state-level trust model may be achieved in 12 to 15 months.

Security Infrastructure Required for Crypto Bank Platforms

Building a crypto bank necessitates a departure from standard web security. Because blockchain transactions are immutable, the infrastructure must prevent unauthorized access even in the event of a partial system compromise. This requires a defense-in-depth strategy, layering physical hardware with sophisticated cryptographic protocols.

MPC and Hardware Security Modules

To achieve institutional-grade custody, we move away from single private keys. Instead, we utilize a combination of Multi-Party Computation and Hardware Security Modules.

- MPC Technology: Private keys are never generated in their entirety. They exist as distributed shards across isolated environments.

- FIPS 140-2 Level 3 HSMs: We anchor shards within specialized, physically tamper-resistant hardware. If the hardware is compromised, the data is zeroized.

- Warm Storage: This setup provides clients with the speed of an online wallet with the security profile of an offline vault.

Multi-signature Authorization Frameworks

Governance is the cornerstone of institutional trust. We implement multi-signature frameworks, ensuring no single individual, whether a rogue employee or a compromised client, can move funds unilaterally.

Every institutional transaction requires an M of N approval. A withdrawal might require authorization from two out of three designated executives, plus a final biometric verification. This is programmatically enforced at the protocol level, ensuring the underlying HSMs reject any transaction that does not meet the predefined quorum.

Transaction Risk Monitoring Systems

Security involves identifying suspicious behavior before a loss occurs. We integrate real-time risk monitoring that analyzes behavioral and cryptographic data for every request.

- Behavioral Analytics: The system flags deviations from patterns, such as unusual transaction sizes or login attempts from new locations.

- Velocity Limits: Automated circuit breakers freeze accounts if they exceed preset transaction thresholds within a specific window.

- On-Chain Screening: Every destination address is screened against global blacklists. High-risk activities are automatically blocked.

Secure API Layers

Institutional clients often connect internal portfolio systems to the bank via API. This creates a potential attack vector that we harden through several layers of security.

| Security Layer | Function |

| IP Whitelisting | Allows for read-only or trade-only keys to limit access. |

| Mutual TLS (mTLS) | Ensures both client and server verify each other’s certificates. |

| API Key Scoping | Ensures that both the client and the server verify each other’s certificates. |

Integrating Staking and Yield Services for Institutions

Institutional clients increasingly view digital assets as productive capital. We build staking and yield infrastructure that allows these organizations to earn protocol rewards without compromising the security of their principal or their regulatory standing.

Institutional Staking Infrastructure

We bridge the gap between secure custody and active network participation. Our design ensures that assets remain within your bank’s secure perimeter while they are cryptographically delegated to the blockchain.

- Non-Custodial Delegation: We implement a framework where the power to stake is separated from the power to move funds. The principal remains in the vault.

- Warm Staking Integration: By leveraging MPC technology, we enable staking directly from warm wallets, enabling quick unbonding and liquidity when needed.

- Slashing Protection: We build automated monitoring to detect validator downtime or double-signing risks, protecting the client’s principal from protocol-level penalties.

Validator Management and Rewards

Managing the lifecycle of a stakeholder requires precision. We automate the technical complexities of validator selection and the subsequent accounting of rewards for institutional reporting.

We deploy and manage high-repute, dedicated validator nodes to ensure zero-risk participation. Our system automatically tracks every reward event, calculating the cost basis and performance metrics. This data is then fed into a unified dashboard, providing clients with a clear view of their APY and total yield across multiple protocols.

Compliance for Staking Services

Staking introduces unique legal and tax challenges. We build the necessary tools to ensure these services meet the requirements of auditors and tax authorities.

- Reward Attribution: We provide granular reporting that distinguishes between original principal and earned rewards for tax purposes.

- Jurisdictional Routing: Our platform can restrict staking to specific geographic regions or validators to comply with localized financial regulations.

- Audit Trails: Every delegation and reward claim is logged with a cryptographic timestamp, creating an immutable record for institutional SOC 1 and SOC 2 audits.

How Crypto Bank Platforms Support Institutional Trading Workflows?

Institutional trading in the digital asset space requires the same level of sophistication as traditional equities or FX. Trading workflows must prioritize capital efficiency, minimize market impact, and eliminate the security risks associated with keeping assets on-exchange.

Liquidity Aggregation

To prevent price slippage on large orders, a platform must access a deep, fragmented market through a single entry point. Integration with a global network of regulated exchanges, market makers, and OTC desks is essential.

- Unified Order Book: Aggregating bid and ask data from multiple venues into one interface gives traders a holistic view of global liquidity.

- API Standardization: Normalizing diverse data feeds from providers like Coinbase Prime or BitGo allows internal systems to communicate with dozens of venues through a single integration.

- Direct Access: For high-touch requirements, direct connections to principal OTC desks ensure large blocks can be executed with minimal disclosure to the broader market.

Smart Order Routing

Moving a hundred-million-dollar position requires more than a simple buy button. Smart Order Routing and advanced execution algorithms hide trading intent and achieve the best possible fill price.

The SOR engine dynamically analyzes market depth and latency across all connected venues. If one exchange has a tighter spread but lower volume, the system automatically splits the order, routing portions to various venues simultaneously. This passive-first execution strategy minimizes market impact while proprietary algorithms like TWAP and VWAP ensure smooth entry into large positions.

Secure Trade Settlement

The greatest risk in institutional trading is often exchange risk (the danger of losing assets if a trading venue fails). Integrating trade execution directly with a secure custody system solves this.

The Prime Model:

Following the industry standard set by Anchorage Digital, an off-exchange settlement model is used. Assets remain in regulated custody until the moment a trade is matched, at which point they are settled instantly via an internal ledger or a secure atomic swap.

This eliminates the need to pre-fund exchange accounts with large balances. By keeping the vast majority of capital in a “qualified custodian” environment during the entire trading lifecycle, clients receive the highest level of bankruptcy-remoteness and operational safety.

Institutional Crypto Bank Platform Capabilities That Drive Adoption

Modern adoption relies on consolidating complex digital asset services into a single, high-performance ecosystem. Leading platforms provide the operational efficiency of traditional banking while leveraging the speed and transparency of blockchain.

1. Unified Custody, Trading, and Staking

Integrating core services reduces capital friction and operational risk. Similar to the models used by Anchorage Digital or Coinbase Prime, these platforms allow assets to move between storage and market participation without delay.

- Capital Efficiency: Assets in secure custody can be deployed for trading or staking instantly.

- Consolidated Security: A single, hardened layer protects the asset lifecycle from purchase to yield.

- Simplified Accounting: Unified systems provide one source of truth for holdings, rewards, and trades, easing institutional audits.

2. APIs for Fintech Integrations

Scalability depends on how well a platform interacts with existing financial software. Robust API layers allow banks and fintech firms to build custom products on regulated crypto infrastructure.

These APIs support high-frequency data and secure execution. Mirroring the standards of FalconX or BitGo, these interfaces enable firms to automate treasury management and wealth management portals. Secure protocols like mTLS ensure these connections remain private and tamper-proof.

3. Portfolio Management for Asset Managers

Managing large digital portfolios requires tools beyond simple balance tracking. Institutional dashboards provide deep insights into risk, performance, and allocation across multiple networks.

- Risk Analytics: Real-time monitoring of volatility and counterparty exposure keeps managers within their mandates.

- Multi-Entity Support: Large firms manage hundreds of sub-accounts under one master profile with specific permissions.

- Automated Rebalancing: Advanced tools allow managers to set target allocations and execute trades automatically when markets drift.

Why Do Businesses Choose IdeaUsher for Crypto Bank Development?

Selecting a development partner is the difference between a prototype and a production-ready institution. Businesses choose IdeaUsher because the engineering process is led by elite talent with a deep understanding of the security and regulatory demands of the digital asset sector.

Extensive Engineering Experience

With over 500,000 hours of coding experience, the team of ex-MAANG/FAANG developers brings a high-performance culture to every project. This collective expertise enables the construction of scalable, low-latency systems that meet the rigorous requirements of global finance.

Regulatory-Compliant Architectures

Navigating the legal landscape is as critical as the code itself. Expertise in building architectures that adhere to KYC, AML, and GDPR standards ensures platforms are audit-ready. By embedding compliance directly into the software, operational friction is reduced while maintaining alignment with global regulators.

End-to-End Infrastructure Development

Development covers the entire lifecycle of a crypto bank. This holistic approach ensures all components (custody, trading, staking, and fiat on-ramps) work together in a unified, secure ecosystem.

- Custom Custody: Building proprietary MPC and HSM-based environments to eliminate single points of failure.

- Seamless Integrations: Connecting platforms to a global network of liquidity providers and traditional banking rails.

- Future-Ready Stack: Utilizing modern frameworks like Flutter for apps and Solidity for audited smart contracts.

Conclusion

Building a regulated crypto bank requires a perfectly synchronized blend of high-end cryptography and rigorous financial engineering. Our team will technically architect your entire ecosystem to ensure that every MPC shard and liquidity API operates with absolute precision. You can certainly rely on our deep blockchain expertise to deploy a truly resilient platform that will effectively scale alongside your institutional needs.

Looking to Build a Compliant Crypto Bank Platform Like Anchorage?

IdeaUsher can help you build a compliant crypto bank platform that securely manages digital assets and institutional transactions. Our team can design custody systems compliance monitoring and blockchain settlement infrastructure for regulated operations.

With over 500,000 hours of coding experience, our team of ex-MAANG/FAANG developers builds resilient architectures designed to satisfy both federal examiners and high-net-worth clients. We don’t just build apps; we architect the future of digital finance.

Why Partner with IdeaUsher?

- Elite Engineering: Access a talent pool previously at Google, Meta, and Amazon to build your core ledger.

- Hardened Security: Implementation of FIPS 140-2 Level 3 HSMs and MPC protocols for zero-trust custody.

- Regulatory Readiness: Automated KYC/AML and Travel Rule integrations built directly into the transaction flow.

- Institutional Trading: Smart Order Routing and atomic settlement for high-velocity institutional workflows.

Check out our latest projects to see the kind of work we can do for you.

FAQs

A1: Launching a crypto bank requires specialized licensing and advanced blockchain engineering. You must first secure a banking charter to legally handle client funds. Our team can then effectively develop your technical core by integrating secure MPC custody. You should definitely prioritize finding an experienced development partner to ensure long-term success.

A2: Operating a crypto bank involves technical and regulatory challenges that you must proactively manage. Smart contract vulnerabilities or private key compromises could potentially lead to irreversible asset losses. Regulatory shifts might also affect your model suddenly as global standards continue to evolve. You should always implement a defense-in-depth strategy to mitigate these sophisticated threats.

A3: Building a high-performance platform requires substantial capital for development and legal fees. An enterprise system usually costs between $500,000 and $1,000,000, depending on your specific features. You will also need to budget for recurring expenses like security audits and node maintenance. Investing in a robust architecture early will certainly save you from higher costs later.

A4: Layer 3 is a specialized application layer built directly on top of Layer 2 scaling solutions. It allows developers to create app-specific blockchains with tailored privacy and extremely low fees. These networks can effectively handle high-volume microtransactions without congesting the underlying layers. You might use this technology to implement specific compliance rules not feasible on general-purpose chains.