(+971) 8007 4267

(+971) 8007 4267 (+91) 946 340 7140

(+91) 946 340 7140 (+1) 628 432 4305

(+1) 628 432 4305

Blockchain technology has changed to become as significant as the internet itself, from being viewed as overhyped to being recognized as a crucial part by banks, governments, and a range of businesses.

All sizes of enterprises and industries as well as a wide range of industries are beginning to utilize blockchain technology. Businesses can benefit a lot from utilizing blockchain technology, even if there have been many examples of its integration in commercial settings.

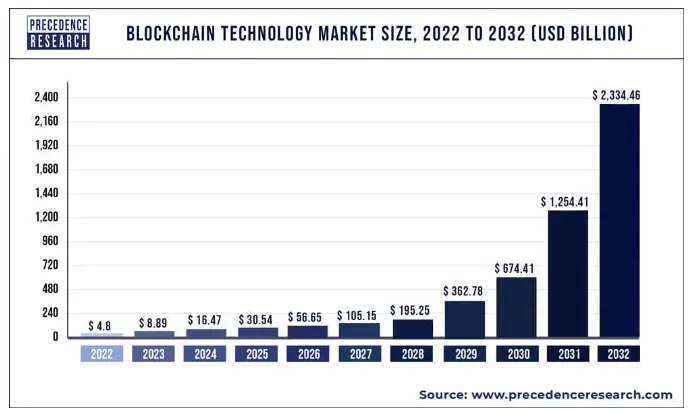

Source: PrecedenceResearch

Additionally, blockchain technology has established collaborations with well-known companies like Walmart, IBM, Oracle, and others, and it has gained a substantial footing in several high-level operations.

This article seeks to provide insight into the fundamental concepts of blockchain, its relevance for startups, the process of developing a blockchain tailored for startup needs, and how it can not only optimize business operations but also elevate the brand as a beacon of innovation.

What Is A Blockchain?

Blockchain is a cutting-edge technology that supports a decentralized network of linked nodes by acting as a distributed database. The word “blockchain” refers to its basic structure, in which data is progressively connected to create an immutable chain after being organized into blocks and cryptographically protected.

Each block in this novel method of data management includes a timestamp and a reference to the preceding block, forming a chronological and impenetrable ledger that guarantees transparency, security, and integrity throughout the network.

Blockchain was invented before it was widely used in many other industries, most notably because of the rise of cryptocurrencies like Bitcoin. Though blockchain technology makes it easier to create decentralized apps (dApps), smart contracts, decentralized finance (DeFi) platforms, and non-fungible tokens (NFTs), its promise goes well beyond virtual currency.

These applications leverage the inherent properties of blockchain, such as decentralization, transparency, and immutability, to revolutionize traditional industries and create new paradigms of interaction and value exchange.

Foundation Pillars of Blockchain Technology

Explore the foundational technologies that underpin Blockchain and drive technological advancement, recognizing that Blockchain extends beyond transactions and cryptocurrencies.

1. ICO (Initial Coin Offering)

ICOs are a fundraising model utilized by startups and enterprises that incorporate blockchain technology into their business models. It involves the issuance of digital tokens or coins to investors in exchange for capital. ICOs typically involve stages such as pre-announcement, offering, and marketing campaigns to attract investors.

- ICOs exploded in popularity during the cryptocurrency boom of 2017, raising billions of dollars for various blockchain projects.

- Some notable ICOs include Ethereum, which raised $18 million in its ICO in 2014, and EOS, which raised over $4 billion in its year-long ICO in 2017-2018.

- The ICO market saw a decline in popularity and regulatory scrutiny in subsequent years due to numerous scams and fraudulent projects.

2. Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. These contracts run on the blockchain and automatically execute actions when predefined conditions are met. Smart contracts ensure accuracy, eliminate disputes, offer high transaction speed, and embed trust in business transactions.

- The concept of smart contracts was first proposed by computer scientist Nick Szabo in the 1990s, but it wasn’t until the advent of blockchain technology that they became feasible.

- Ethereum, with its Turing-complete programming language, Solidity, became the leading platform for deploying smart contracts, enabling developers to create a wide range of decentralized applications (dApps).

- Smart contracts have been applied in various industries beyond finance, including supply chain management, real estate, healthcare, and gaming.

3. Cryptocurrency Wallets

Cryptocurrency wallets are software tools used to store, send, and receive digital currencies. There are various types of cryptocurrency wallets available, including desktop wallets, mobile wallets, online web wallets, hardware wallets, paper wallets, etc. These wallets provide users with options for managing their digital assets securely.

- Hardware wallets, such as Ledger and Trezor, are considered the most secure type of cryptocurrency wallets as they store private keys offline, making them immune to online hacking attacks.

- Paper wallets involve printing out the private and public keys onto a physical piece of paper, providing a secure cold storage solution.

- Mobile wallets offer convenience for everyday transactions, allowing users to access their funds on the go via smartphone apps.

4. Blockchain NFTs (Non-Fungible Tokens)

NFTs are unique digital assets that represent ownership of a specific item or piece of content. Unlike cryptocurrencies such as Bitcoin, NFTs are non-fungible, meaning they cannot be exchanged on a one-to-one basis. NFTs are typically based on smart contracts on blockchain platforms like Ethereum and have gained popularity for representing digital art, music, collectibles, and other unique digital assets.

- NFTs have sparked debates about digital ownership, copyright, and the valuation of digital art and collectibles.

- Beyond digital art, NFTs have been used to tokenize real-world assets such as real estate, luxury goods, and even tweets.

Business Benefits of Blockchain Solutions

The business world is entering the most revolutionary age thanks to blockchain technology, as forward-thinking companies, inventors, and investors embrace blockchain solutions to promote transparency and trust. Let us determine which Blockchain solution is most suitable for your organization, ranging from developing mobile applications to facilitating international transactions.

1. Enhanced Security and Trust

Blockchain technology offers unparalleled security and trust through several key mechanisms. Firstly, data stored on a blockchain is immutable, meaning it cannot be altered or tampered with, ensuring a reliable record of transactions. Additionally, transactions are secured using robust cryptographic techniques, making them highly resistant to fraud and cyberattacks. Furthermore, the use of a distributed ledger ensures that all participants in the network have a synchronized copy of the ledger, fostering transparency and accountability among all stakeholders.

2. Improved Transparency and Traceability

Blockchain enhances transparency and traceability through shared visibility and auditability. Authorized participants can access and track data changes in real-time, facilitating collaboration and improving transparency across processes. Moreover, every transaction is recorded and traceable, providing a clear audit trail for regulatory compliance and internal investigations. This provenance tracking capability enables the tracking of goods, assets, or data throughout the supply chain, enhancing accountability and reducing the risk of fraud.

3. Increased Efficiency and Speed

Blockchain drives efficiency and speed through automation, streamlined workflows, and real-time updates. Smart contracts, which are self-executing agreements on the blockchain, automate many manual processes, leading to increased efficiency. Eliminating intermediaries and paperwork-heavy processes reduces transaction times and costs significantly. Additionally, real-time updates ensure that all participants have immediate access to the latest information, eliminating delays and bottlenecks in processes.

4. Cost Savings

Blockchain enables significant cost savings through reduced operational costs, improved fraud detection, and streamlined regulatory compliance. Automation of processes and elimination of intermediaries lead to lower operational expenses. Moreover, the secure nature of blockchain technology helps prevent fraud, reducing associated costs. Transparent and auditable records simplify regulatory compliance processes, thereby reducing compliance-related expenses.

5. Improved Customer Experience

Enhanced transparency and security provided by blockchain technology can greatly improve the customer experience. Customers can trust that their transactions are secure and transparent, leading to increased satisfaction and loyalty. Additionally, the ability to track the origin and movement of goods or assets in real-time enhances transparency and builds trust with customers.

6. New Business Models

Blockchain opens up opportunities for new business models and revenue streams through innovative applications. The decentralized nature of blockchain allows for the creation of decentralized autonomous organizations (DAOs) and new ways of funding projects through initial coin offerings (ICOs) or tokenization. These new business models enable greater efficiency, transparency, and inclusivity, driving innovation and growth in various industries.

7. Competitive Advantage

Early adopters of blockchain technology can gain a significant competitive advantage by leveraging its benefits. By improving efficiency, transparency, and trust, organizations can differentiate themselves from competitors and attract customers who value these attributes. Moreover, embracing blockchain early allows companies to stay ahead of regulatory changes and industry trends, positioning them as leaders in their respective fields.

Use Cases of Blockchain in Different Industries

Blockchain technology has rapidly evolved beyond its cryptocurrency origins, finding applications across diverse industries, each presenting unique challenges and opportunities for innovation. Explore use cases of blockchain technology in each of these industries.

1. Blockchain in Healthcare

Blockchain technology offers numerous benefits and applications in the healthcare industry, revolutionizing various aspects of data management, patient care, and supply chain logistics. One prominent use case is the secure management of patient health records. By utilizing blockchain’s immutable and decentralized nature, healthcare organizations can ensure the integrity and privacy of sensitive patient data. Each transaction or update to a patient’s record is securely recorded on the blockchain, providing a transparent and tamper-proof audit trail. This enhances data security, reduces the risk of data breaches, and gives patients greater control over their personal health information.

2. Blockchain in FinTech

Blockchain technology has made significant strides in the FinTech sector, promising substantial enhancements across various financial domains. Its integration with FinTech has catalyzed digital transformation, offering a plethora of benefits such as streamlined KYC processes, accelerated transactions, heightened security against hacks, and reduced transactional costs. The impact of Blockchain extends beyond traditional banking, permeating into realms like digital payments, insurance, loans, and credits, where processes are poised to become more efficient and trustworthy.

3. Blockchain in Real Estate

Blockchain technology has emerged as a transformative force in the real estate industry, offering decentralized solutions to streamline processes and enhance efficiency. This technology has garnered significant attention not only from individual property developers and real estate agents but also from governmental bodies seeking to optimize their real estate ecosystems. By leveraging blockchain, various stakeholders within the real estate sector can ensure transparency, security, and immutability in transactions, thereby mitigating fraud and reducing administrative overhead.

4. Blockchain in Manufacturing

Blockchain technology is revolutionizing the manufacturing sector by seamlessly integrating with the Industrial Internet of Things (IIoT). Through this integration, a sophisticated synergy emerges, automating processes and enhancing efficiency within supply chains and manufacturing operations. By directly linking IoT devices with blockchain, a comprehensive history of connected devices is maintained, facilitating streamlined troubleshooting and operational oversight. Additionally, the fusion of IoT and blockchain introduces robust consensus and agreement mechanisms through smart contracts, fortifying the system against external threats and ensuring seamless operations.

Role Of Blockchain in Modern Startups

Blockchain companies use cases generated by those that have incorporated the technology to their process are too efficient and profitable to ignore, even though the scale of organizations that have used Blockchain for business is still more skewed towards those who haven’t.

1. Enhanced Security and Transparency

Blockchain technology is increasingly becoming a cornerstone in the realm of modern startups, offering distinct advantages across various crucial aspects. One of its paramount contributions lies in bolstering security and transparency within startup operations. By storing data in immutable blocks, blockchain ensures a tamper-proof environment, thus instilling heightened trust and transparency between startups and their stakeholders. The decentralized nature of blockchain further fortifies security by eliminating single points of failure and reducing the susceptibility to data breaches, fostering a more resilient ecosystem for startups to thrive.

2. Improved Efficiency and Cost Reduction

Moreover, blockchain facilitates enhanced efficiency and cost reduction, pivotal for startups aiming to optimize their operations. Through the automation of processes via smart contracts, blockchain enables startups to streamline tasks and agreements, mitigating the need for manual interventions and enhancing overall operational efficacy. Additionally, the elimination of intermediaries in peer-to-peer transactions engendered by blockchain not only expedites transactional processes but also leads to significant cost savings, empowering startups with a competitive edge in the market.

3. Innovative Business Models

Furthermore, blockchain’s capacity for fostering innovative business models opens up new avenues for startups to explore. Through asset tokenization, startups can digitize physical or intangible assets, thereby unlocking novel investment and funding opportunities previously inaccessible. Leveraging decentralized applications (dApps) on blockchain platforms, startups can pioneer groundbreaking solutions across diverse sectors such as finance, supply chain management, and voting systems, revolutionizing traditional business paradigms and driving unprecedented value creation.

4. Specific Applications for Startups

In addition to its overarching contributions, blockchain offers specific applications tailored to the unique needs of startups. For instance, blockchain-based fundraising mechanisms like Initial Coin Offerings (ICOs) and Security Token Offerings (STOs) democratize access to capital, enabling startups to raise funds directly from the public and circumvent traditional financing constraints. Moreover, blockchain’s utility extends to optimizing supply chain management by enabling transparent tracking of goods and materials, thereby enhancing accountability and reducing instances of fraud along the supply chain.

Role Of Blockchain In Business Mobile Apps

Blockchain technology can play several roles in business mobile apps, offering various benefits such as transparency, security, and decentralization. Here are some of the roles blockchain can play in business mobile apps:

1. Secure Transactions

Blockchain technology provides a secure platform for transactions through the use of cryptographic techniques. By leveraging blockchain in business mobile apps, companies can ensure that transactions such as payments, contracts, and transfers are conducted securely without the need for intermediaries, thus reducing the risk of fraud and enhancing trust between parties.

2. Transparency and Traceability

One of the key features of blockchain is its ability to maintain an immutable ledger of transactions, offering transparency and traceability. When integrated into business mobile apps, blockchain enables the tracking and recording of every transaction, ensuring accountability and providing a clear audit trail. This transparency not only enhances trust but also helps mitigate the risk of fraudulent activities.

3. Identity Management

Blockchain-based identity management solutions provide a secure and decentralized method for managing digital identities. When integrated into business mobile apps, blockchain technology can be used to verify the identity of users securely. This reduces the risk of identity theft and fraud, enhances user privacy, and ensures compliance with data protection regulations.

4. Data Security and Privacy

Blockchain offers robust security features such as encryption and decentralization, making it an ideal solution for enhancing data security and privacy. By storing sensitive data on the blockchain, businesses can protect it from unauthorized access and ensure compliance with data protection regulations. Integrating blockchain technology into business mobile apps helps safeguard sensitive information and build trust with users.

5. Tokenization and Rewards Programs

Blockchain enables tokenization, allowing businesses to create digital assets that represent ownership or value. Business mobile apps can leverage tokenization to implement rewards programs, loyalty points, and incentive schemes. By offering digital tokens as rewards, companies can enhance user engagement and retention, driving customer loyalty and increasing brand value.

6. Decentralized Applications (DApps)

Blockchain facilitates the development of decentralized applications (DApps), which run on a distributed network of computers rather than a centralized server. Integrating DApps into business mobile apps enables companies to offer decentralized services such as decentralized finance (DeFi) or decentralized marketplaces. This decentralization enhances security, reduces dependency on intermediaries, and fosters innovation in the mobile app ecosystem.

Steps To Blockchain Implementation For Startups

Implementing blockchain technology for startups involves several key steps to ensure successful integration and utilization. Here’s a guide to help you get started:

1. Identify Use Case

Exploring potential applications of blockchain technology across various industries and sectors is crucial for startups. By delving into areas such as supply chain management, healthcare records management, decentralized finance (DeFi), digital identity verification, and more, startups can uncover transformative opportunities. However, it’s essential to align the chosen blockchain use case with the startup’s core objectives and values. This alignment ensures that the implementation of blockchain technology contributes directly to streamlining operations, enhancing transparency, reducing costs, or creating new revenue streams.

2. Feasibility Study

Conducting a comprehensive feasibility study involves assessing multiple facets of blockchain implementation. Startups need to evaluate the technical feasibility of integrating blockchain, considering scalability, interoperability, consensus mechanisms, and network infrastructure requirements. Additionally, analyzing the economic viability is crucial, encompassing development costs, operational expenses, and potential return on investment (ROI). Furthermore, understanding the operational impact is essential to anticipate any challenges or disruptions that may arise during implementation and to prepare strategies for mitigation.

3. Select Blockchain Platform

Choosing the right blockchain platform entails thorough research and evaluation of available options. Startups should explore platforms like Ethereum, Hyperledger Fabric, Corda, among others, considering factors such as consensus algorithms, governance models, developer tools, and community support. Scalability needs should also be taken into account, ensuring that the selected platform can accommodate the startup’s growth trajectory and transaction volumes. Moreover, regulatory compliance is a critical consideration, necessitating alignment with relevant industry and geographical regulations governing data privacy, security, and other compliance aspects.

4. Design Architecture

Designing the architecture of a blockchain solution involves several key considerations. Startups need to define the network structure, including the number of nodes, their roles, and the communication protocols for transaction validation. For use cases involving smart contracts, thorough planning and development are required to automate business processes and enforce predefined rules and agreements. Integration with existing systems is another crucial aspect, necessitating careful planning to ensure seamless interoperability with the startup’s IT infrastructure, databases, and applications.

5. Develop Prototype/MVP

The development phase typically follows an agile approach, focusing on building and refining a prototype or minimum viable product (MVP) of the blockchain solution. Startups prioritize key features and functionalities to demonstrate the value proposition to stakeholders effectively. Gathering feedback from users, partners, and other stakeholders throughout the development process is critical. This feedback informs iterative improvements to the prototype, addressing usability issues and refining the user experience. Proof of concept (POC) testing is also conducted to validate the technical feasibility and performance of the blockchain solution in a controlled environment, identifying any technical limitations or scalability concerns that need to be addressed.

6. Testing and Quality Assurance

Thorough testing and quality assurance are critical stages in the blockchain implementation process. Startups need to conduct comprehensive testing across different environments to identify and rectify any bugs, vulnerabilities, or performance issues. By simulating real-world scenarios, startups can ensure the reliability, scalability, and performance of their blockchain solution. Rigorous testing also helps validate the functionality of smart contracts and ensure they operate as intended.

7. Deployment

Deploying the blockchain solution into a production environment requires careful planning and execution. Startups should follow best practices for deployment, configuration, and monitoring to ensure a smooth and seamless transition. This involves collaborating with IT professionals and blockchain experts to configure the network, set up nodes, and establish monitoring mechanisms. Continuous monitoring and maintenance are essential post-deployment to ensure the ongoing security and performance of the blockchain solution.

Challenges Of Using Blockchain For Startups

While blockchain technology offers numerous potential benefits for startups, such as enhanced security, transparency, and efficiency, there are also several challenges associated with its adoption and implementation which we have mentioned in detail:

1. Complexity

Blockchain technology is complex, requiring a deep understanding of cryptographic principles, distributed systems, consensus mechanisms, and smart contract development. Startups may struggle to find qualified talent with the necessary expertise to build and maintain blockchain-based solutions.

2. Scalability

Scalability remains a significant challenge for blockchain networks, especially public ones like Bitcoin and Ethereum. As the number of users and transactions increases, so does the strain on the network, leading to issues such as slow transaction processing times and high fees. Startups must carefully consider the scalability limitations of existing blockchain platforms and explore solutions to mitigate these challenges.

3. Regulatory Uncertainty

The regulatory landscape surrounding blockchain and cryptocurrencies is constantly evolving and varies significantly from one jurisdiction to another. Startups operating in this space must navigate complex regulatory frameworks, which can pose legal and compliance challenges. Regulatory uncertainty can also deter potential investors and customers, impacting the growth and viability of blockchain startups.

4. Security Concerns

While blockchain technology is often touted for its security features, it is not immune to vulnerabilities and cyber attacks. Smart contract bugs, and exploits targeting decentralized applications are just a few examples of security risks associated with blockchain technology. Startups must prioritize security throughout the development lifecycle and implement robust measures to protect their blockchain-based systems from potential threats.

5. User Adoption

Despite the potential benefits of blockchain technology, mainstream adoption remains relatively low. Many users are still unfamiliar with blockchain concepts and skeptical about its practical applications. Startups may encounter challenges when trying to onboard users onto their blockchain platforms or convince existing users to switch from traditional solutions. Educating consumers and building user-friendly interfaces are essential steps in overcoming this barrier to adoption.

6. Cost

Building and maintaining blockchain-based solutions can be costly, particularly for startups with limited financial resources. Costs associated with infrastructure, development, security audits, and regulatory compliance can quickly add up, making it challenging for startups to justify the investment required to leverage blockchain technology effectively.

Cost Affecting Factors To Consider For A Blockchain App Development

When considering the cost of developing a blockchain application, several factors come into play. The first determinant is the category of the blockchain app itself. Whether it falls under cryptocurrency-based solutions or non-cryptocurrency based solutions significantly impacts the development cost.

1. Blockchain App Category

When considering the cost of developing a blockchain application, the first significant factor to analyze is the category of the blockchain app itself. Whether it falls under cryptocurrency-based solutions or non-cryptocurrency based solutions significantly impacts the development cost.

2. Cryptocurrency Based Solution

Cryptocurrency-based solutions often involve complex algorithms and security measures inherent to digital currencies, such as Bitcoin or Ethereum. Implementing features like wallet management, transaction processing, and blockchain integration can significantly influence the overall cost.

3. Non-Cryptocurrency Based Solutions

Non-cryptocurrency based solutions may involve utilizing blockchain technology for purposes beyond digital currencies, such as supply chain management or identity verification. The complexity of the desired functionalities will influence the cost accordingly.

4. Blockchain App Services

Another critical factor affecting cost is the specific services required within the blockchain application. Services like crypto-wallet development, smart contract functionality, ICO management, and integration with crypto-exchanges will impact the cost based on their intricacy and customization needs.

5. Crypto-Wallet

Developing a crypto-wallet involves creating secure digital wallets for storing cryptocurrencies. The cost may vary depending on factors such as security features, user interface design, and integration with other blockchain services.

6. A Distributed Decentralized Ledger for IoT

If the application aims to eliminate single points of failure and secure device data within the Internet of Things (IoT) ecosystem, specialized considerations come into play. Implementing a distributed and decentralized ledger suitable for IoT applications requires robust encryption, efficient consensus mechanisms, and seamless integration with IoT devices, all of which can impact development costs.

7. Smart Contract Development

Smart contracts automate the execution of contract terms, and their development involves coding and testing complex business logic. The cost of smart contract development depends on factors such as the complexity of the contract logic, security requirements, and integration with other blockchain components.

8. ICO (Initial Coin Offering)

If the application involves managing an ICO, additional complexities arise. These may include compliance with regulatory frameworks, security considerations, and user interface design tailored to the specific requirements of ICO participants.

9. Distributed Ledger Technology

Developing a distributed ledger technology (DLT) infrastructure serves as the backbone of blockchain applications. The cost depends on factors such as scalability, consensus mechanisms, and interoperability requirements.

10. Crypto-Exchange

Integration with crypto-exchanges introduces additional complexities such as compliance, security, and user experience design. The cost of integrating with crypto-exchanges will vary based on factors such as the number of supported exchanges, trading features, and regulatory compliance requirements.

Conclusion

Blockchain technology offers a myriad of benefits for startups, revolutionizing the way they operate and interact with their stakeholders.

However, adopting blockchain technology is not without its challenges. Startups may face technical complexities, such as scalability issues and interoperability concerns, which require specialized expertise to navigate.

Given these challenges, collaborating with a specialized blockchain development company can significantly mitigate risks and accelerate the adoption of blockchain technology for startups.

By partnering with a development company, startups can access a talent pool of blockchain developers, architects, and consultants who can tailor solutions to their specific needs and ensure seamless integration with existing systems.

How Idea Usher Can Help Your Business with Blockchain?

Idea Usher offers comprehensive support to businesses seeking to leverage blockchain technology to enhance their operations. Our expertise spans a diverse array of decentralized solutions aimed at enhancing security and scalability within your system.

Whether you require consultation on blockchain application development, smart contract implementation, or crypto token creation, our team is dedicated to providing expert guidance every step of the way.

We work closely with our clients to develop bespoke blockchain solutions that align with their unique objectives and requirements. Whether you’re looking to optimize supply chain management, enhance data security, or facilitate transparent transactions, we have the knowledge and expertise to bring your vision to life.

Contact us today to understand more about how we can help you with our blockchain development services.

FAQ

Q. What are the main benefits of blockchain for startups?

A. Blockchain technology offers several advantages for startups. Firstly, it ensures security and transparency by creating an immutable record of transactions, fostering trust within the ecosystem. Moreover, by automating processes and eliminating intermediaries, blockchain reduces operational costs and transaction fees. Efficiency and speed are also enhanced as processes are streamlined and data is verified instantly.

Q. What are some common use cases for blockchain in startups?

A. Startups can leverage blockchain technology across various domains. For instance, in supply chain management, blockchain facilitates tracking the movement and origin of goods, enhancing transparency and efficiency. It also finds applications in digital identity management, payment processing for cross-border transactions, fundraising through ICOs or STOs, data sharing with revenue generation opportunities, creating secure voting systems for decentralized organizations, and implementing tamper-proof loyalty programs.

Q. Do businesses need a cryptocurrency to use blockchain?

A. While some blockchain platforms incorporate cryptocurrencies, it’s not a mandatory requirement. Startups can harness the benefits of blockchain, such as security, transparency, and decentralization, without involving cryptocurrencies. This flexibility enables startups to focus solely on leveraging blockchain technology to address their specific needs and challenges.

Q. What are the challenges of using blockchain for startups?

A. Implementing blockchain technology poses several challenges for startups. These include grappling with technical complexity, navigating regulatory uncertainty as blockchain regulations evolve, sourcing experienced blockchain developers due to limited talent availability, and addressing scalability limitations present in some blockchain platforms compared to traditional systems.