Key Takeaways

- Increasing adoption of stablecoin card platforms enables faster global payments through blockchain-based settlement.

- Platforms like Rain integrate stablecoin wallets, card issuing, compliance tools, and unified APIs for modern payment infrastructure.

- A successful platform requires secure wallet architecture, card integrations, liquidity management, and regulatory compliance for seamless operations.

- Stablecoin card platforms improve global treasury management, cross-border payouts, corporate spending, and payment efficiency while reducing delays.

- How Idea Usher can help businesses build stablecoin card platforms with blockchain infrastructure, secure wallets, card integrations, and scalable fintech architecture.

For years, payment companies invested in better apps and smoother user experiences, but the systems moving money behind the scenes barely evolved. That is starting to change. Businesses today need payments that move faster, work across borders, and support a global customer base without adding unnecessary complexity. Stablecoin card platforms like Rain are gaining attention because they make that possible. They combine the speed of blockchain with the convenience of traditional card payments, giving businesses a modern payment infrastructure that is built for how money moves today.

Over the years, we’ve developed several stablecoin card platforms that combine blockchain payment infrastructure with card issuing APIs to enable seamless payments. As IdeaUsher has this experience, we’re writing this blog to break down what it takes to build a stablecoin card platform like Rain. Let’s start!

Market Potential of Stablecoin Card Platforms

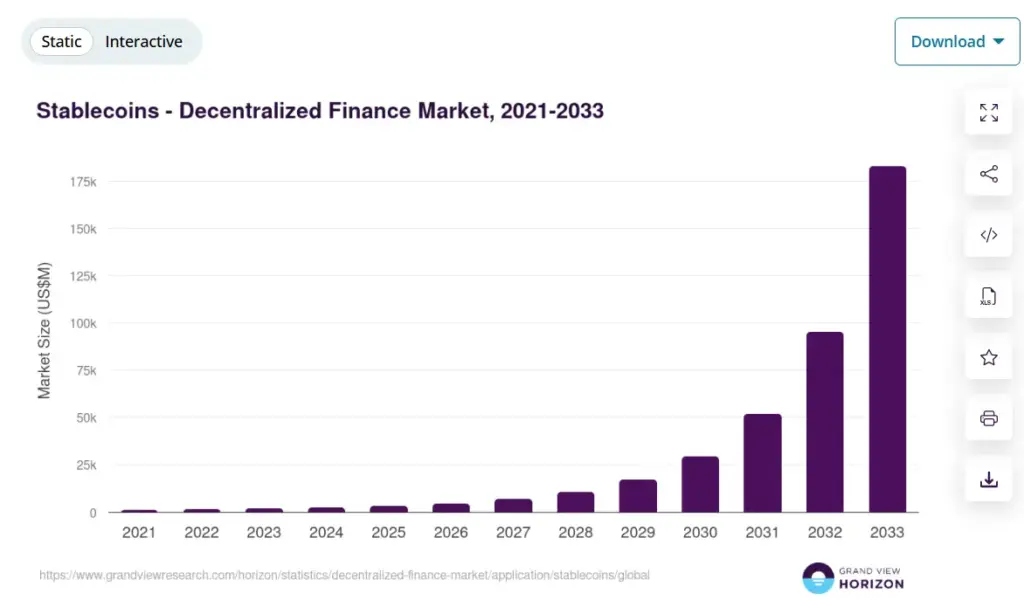

According to Grand View Research, the global stablecoin market generated USD 3,333.5 million in revenue in 2025 and is projected to reach USD 182,789.7 million by 2033. This rapid growth reflects how businesses are moving beyond traditional banking for faster and more efficient payments. One of the biggest reasons is cross-border settlement. International wire transfers can still take days to complete, slowing business operations.

Source: Grand View Research

Stablecoin infrastructure enables near-instant settlements, which is why fintechs, banks, and payment providers are increasingly adopting it for global money movement. Building a stablecoin card platform allows you to capture a slice of these enterprise payment volumes. Instead of routing funds through multiple intermediary banks, businesses use stablecoins to move capital instantly.

- 24/7 Liquidity: Traditional banking halts on weekends and holidays. Stablecoin rails operate continuously, allowing companies to optimize working capital.

- Cost Reduction: Eliminating correspondent banks strips out unnecessary layers of fees.

- Treasury Efficiency: Multi-national firms can consolidate regional balances into a unified digital treasury without maintaining dozens of local currency accounts.

Institutional interest is no longer theoretical. Capital allocators are funding card platforms because these networks bridge legacy banking with modern digital asset rails, creating a highly profitable B2B ecosystem.

A prime example of this model in action is Crypto.com and its tiered Visa card infrastructure. By capturing massive retail and institutional deposits, the company has scaled its operations into a financial powerhouse, generating over $1 billion in annual revenue primarily through transaction fees, staking spreads, and card-related volume conversions.

Cross-Border Fueling Growth

Global payments are becoming faster, but traditional cross-border banking still comes with high fees and settlement delays. Stablecoin card platforms offer a practical alternative by letting businesses move digital dollars almost instantly. This is especially valuable in countries where banking access is limited or local currencies are unstable, giving users a reliable way to store and spend money.

For businesses, the impact goes beyond faster payments. Companies can pay freelancers, vendors, or employees across different countries without the delays of international bank transfers, while recipients can use their funds immediately with a payment card. Platforms like BitPay highlight the strength of this model, generating around $50 million in annual revenue through crypto payment processing and prepaid card services.

New Regulatory Opportunities

Stablecoin regulations are becoming more defined across major markets, making it easier for businesses to build compliant financial products. At the same time, Visa and Mastercard are expanding their support for stablecoin settlement, signaling that digital asset payments are moving into the mainstream.

For startups, this lowers the barrier to entry. Instead of building an entirely new payment network, businesses can use existing card infrastructure while blockchain handles faster settlement behind the scenes. Focusing on compliance from day one also helps build trust with customers, partners, and investors as the industry continues to grow.

How Rain Bridges Stablecoins and Traditional Card Networks?

Rain is an enterprise payment infrastructure platform that helps fintechs, banks, and businesses connect stablecoins with everyday card payments. It provides the tools to launch branded card programs that work with digital asset wallets, making it easier to build modern payment products without creating the entire infrastructure from scratch.

What makes Rain stand out is its ability to bridge blockchain and traditional finance. As a Visa Principal Member, it can issue payment cards that let users spend stablecoins through the existing Visa network while blockchain handles the underlying settlement. This gives businesses a familiar payment experience with the speed and efficiency of digital assets.

The company’s commercial trajectory underscores the explosive growth of this niche. Its financial standing and network scale include the following benchmarks:

- Platform Valuation: A $250 million Series C funding round pushed the company’s valuation to $1.95 billion.

- Capital Invested: Total institutional funding surpassed $338 million from tier-one venture firms.

- Transaction Velocity: The platform handles over $3 billion in annualized transaction volume for more than 200 global partners.

- User Reach: Integrated card programs are structurally capable of reaching a network of 2.5 billion potential end users worldwide.

1. Wallet-to-Visa Connections

Rain connects stablecoin wallets with Visa’s global payment network, allowing users to spend digital assets just like they would with a traditional debit card. Unlike many crypto cards that require users to convert their holdings into fiat before making a purchase, Rain keeps funds in stablecoins until the payment is processed.

When a user pays at a merchant, Rain verifies the available stablecoin balance and completes the transaction through the Visa network. The customer spends stablecoins, while the merchant receives payment in local currency without changing their existing payment system. This creates a smooth payment experience and makes stablecoins practical for everyday purchases.

2. Real-Time Authorization

Every transaction requires rapid processing to prevent checkout delays. The platform achieves real-time authorization through an optimized backend infrastructure that processes transaction approvals in seconds. The system calculates the exact currency exchange rates, verifies the available onchain collateral, and guarantees payment delivery across the card network simultaneously.

The true operational efficiency lies in the backend reconciliation. The platform leverages native USDC settlement directly with Visa. This integration eliminates the need to route funds through the traditional SWIFT banking network or regional clearinghouses.

- Weekend Processing: Settlement occurs 365 days a year, bypassing the standard banking holidays that stall legacy finance.

- Collateral Efficiency: Real-time settlement windows reduce the reserve capital that fintech companies must hold to back their card programs.

- Multi-Chain Orchestration: The network maintains native infrastructure across major layers, including Base, Solana, Polygon, and Arbitrum, optimizing speed and gas fees for onchain settlement.

3. Abstracting Tech Complexity

Building a card program from scratch is a long and complex process that involves banking partnerships, licensing, compliance, and card network integrations. Rain simplifies this by providing a unified API that handles card issuing, wallet connectivity, KYC, and compliance, allowing businesses to launch payment products much faster.

The platform also creates new revenue opportunities. Every time a customer uses a card, businesses can earn a share of the interchange fees generated from those transactions. Instead of managing complex payment infrastructure, companies can focus on growing their products while Rain takes care of the backend operations.

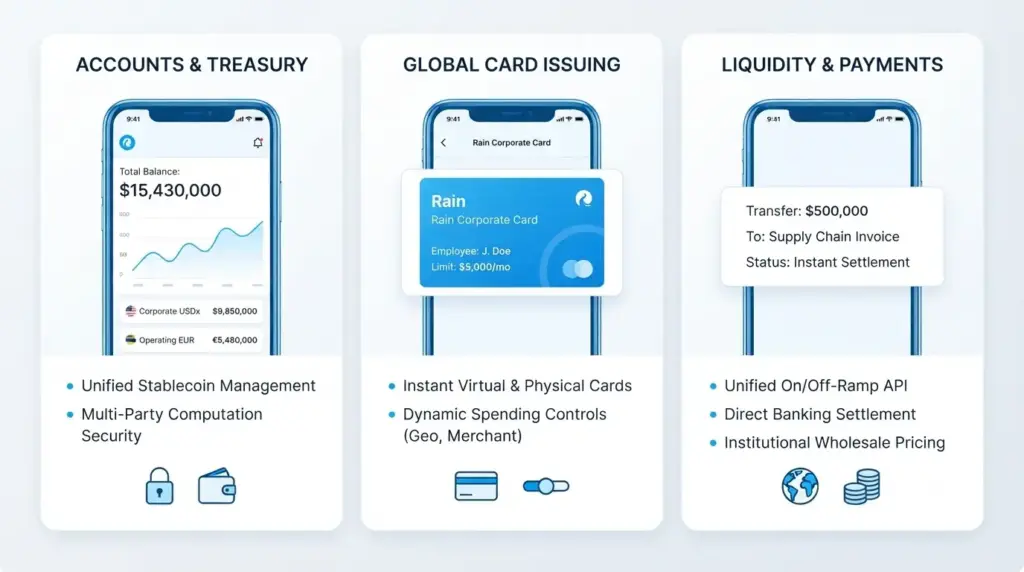

Rain’s Product Ecosystem Explained

Rain offers more than just card issuing. It brings together stablecoin management, payment cards, and money movement into a single platform, giving businesses one place to manage customer payments, corporate funds, and payouts. This unified approach reduces operational complexity and makes it easier to build and scale stablecoin-powered financial products.

The business model derives profitability from multiple structural layers rather than high retail markup fees. The platform operates on institutional-grade pricing designed for major transaction volumes:

- Platform Access Fee: SaaS subscription models starting at $2,500 per month for enterprise API access.

- Interchange Split: Rain captures standard merchant interchange fees, splitting the average 1.5% to 2.5% fee with the issuing partner.

- Conversion Costs: A wholesale 0.25% to 0.50% spread on large-volume stablecoin-to-fiat liquidations.

- Onchain Execution: Passing raw network gas fees directly to developers while offering sponsored gas optimization via smart account bundling.

Wallets and Virtual Accounts

The platform combines secure digital wallets with virtual banking features, making it easier for businesses to manage stablecoins alongside traditional payments. Companies can receive funds through virtual account details, while incoming transfers are converted into digital dollars for faster and more efficient treasury management.

Security is built into the platform through technologies such as multi-party computation, which helps protect corporate funds without limiting usability. This gives businesses greater control over global transactions while reducing the risks associated with managing digital assets.

Card Issuing for Global Spending

The issuing infrastructure lets businesses deploy custom virtual and physical payment cards linked natively to their stablecoin treasuries. Partners can configure spending parameters, authorization rules, and treasury limits dynamically via dashboard controls.

When an employee or end-user swipes a physical card, the platform avoids pre-funding requirements. Pre-funding forces businesses to lock up capital in legacy bank accounts weeks in advance. Instead, the transaction triggers an instant debit against the platform’s live stablecoin reserves.

- Instant Virtual Cards: Generated via API calls for immediate deployment in digital wallets, online ad-spend managers, or vendor payment systems.

- Physical Card Customization: High-quality plastic or metal options featuring custom brand aesthetics, functional for global ATMs and point-of-sale terminals.

- Custom Control Configurations: Dynamic spending limits capped by merchant category codes, geographic locations, or transaction frequencies to eliminate internal fraud.

On/Off-Ramps and Payments

Managing independent connections for crypto liquidity, compliance monitoring, and card production adds massive overhead to engineering teams. Rain unifies these disjointed services into a single API layer. This integration handles everything from fraud screening to direct banking settlement, removing the need to manage multiple vendor contracts.

The single API handles high-volume cross-border liquidity transfers instantly. When an enterprise needs to off-ramp $500,000 to settle a traditional supply chain invoice, the system handles the liquidity routing automatically.

Core Features of a Stablecoin Card Platform Like Rain

Building a stablecoin card platform requires clear infrastructure. Rain provides the essential components out of the box, allowing enterprises to offer stablecoin tools without engineering the baseline systems from scratch. Users interact with these integrated features to move capital seamlessly between digital ledgers and traditional commerce.

The financials behind Rain reflect an enterprise-scale architecture. The platform operates on a clear fee structure designed to support sustainable growth for its corporate clients.

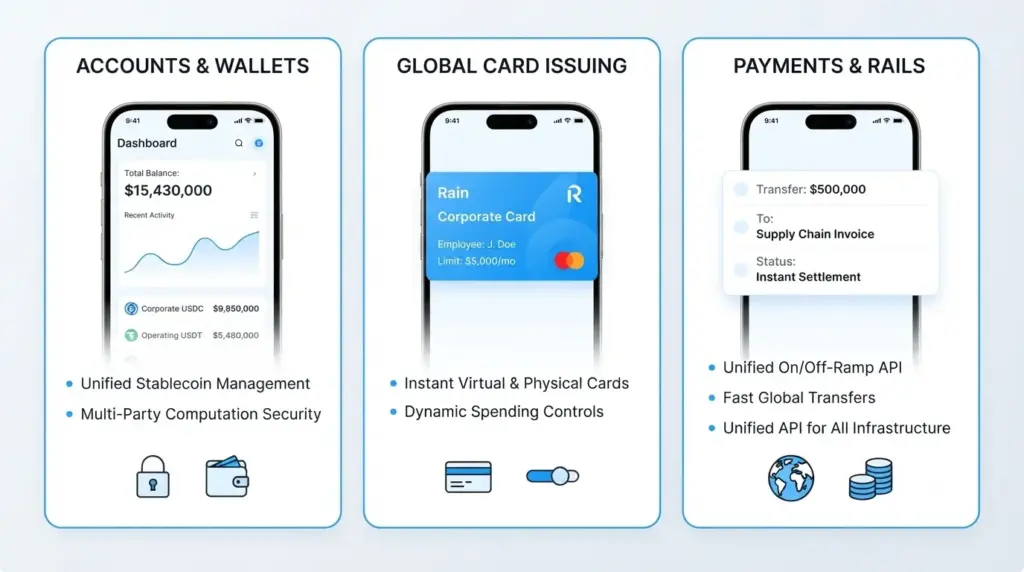

1. Stablecoin Wallets and Digital Dollar Accounts

Corporate clients use Rain to set up dedicated digital dollar accounts tied to multi-party computation wallets. This framework ensures that corporate teams can store and manage assets like USDC and USDT securely without a single employee holding total control over the private keys. These digital dollar accounts connect directly to real-time treasury metrics. Users can monitor account balances, review transaction histories, and organize inbound capital streams from an enterprise dashboard.

- Corporate Control: Rain assigns unique sub-wallets to individual corporate departments to segment operational capital.

- Onchain Verification: Funds remain visible on public block explorers, assuring treasury managers that balances match their reporting.

- Direct Spendability: The wallet layer feeds capital into the card processing engine instantly, removing the need for internal treasury transfers.

2. Virtual and Physical Card Issuing

Rain enables businesses to issue branded virtual and physical Visa cards for employees, partners, or customers. These cards can be used for online purchases, vendor payments, business travel, and everyday corporate spending. Instead of pre-funding multiple expense accounts, companies keep their funds in stablecoin reserves and use them only when a payment is made, improving cash flow while simplifying expense management.

3. Fiat On-Ramps and Off-Ramps

Rain makes it easy for businesses to move funds between traditional bank accounts and stablecoins through built-in fiat on-ramps and off-ramps. Companies can fund accounts using regular bank transfers, while digital asset balances can be converted back into bank deposits whenever needed. The platform also keeps transaction costs competitive, offering $0 local transfers and institutional conversion spreads of around 0.25%–0.50% for large-volume settlements.

4. Cross-Border Payments

Traditional international business payments suffer from slow settlement speeds and opaque fee structures. Rain tackles these challenges by utilizing blockchain rails as a universal settlement network. Users execute wallet-to-wallet transfers that settle globally in seconds. For international distribution, corporate clients schedule mass contractor payouts across multiple regions simultaneously without using traditional correspondent banking networks.

- Immediate Settlement: Transfers execute instantly, regardless of destination or time zones.

- Fixed Overseas Pricing: International wires incur a transparent $15 fee, eliminating the hidden intermediary fees common in legacy banking.

- Network Diversity: Rain handles transactions across multiple networks, allowing users to choose the ledger with the lowest network fees.

5. Unified API for Payment Infrastructure

Developing custom card integrations usually forces fintech companies to connect separate services for compliance, card production, and banking access. Rain eliminates this complexity by packaging all these workflows into a single API. Engineering teams connect to Rain’s endpoints to deploy complete card programs. This structural integration saves businesses months of software development and removes the overhead of managing relationships with different technical vendors.

6. Compliance and Risk Management

Rain simplifies compliance by automating KYC, AML, and fraud monitoring throughout the payment lifecycle. It verifies user identities during onboarding, screens transactions against global sanctions lists, and continuously monitors wallet activity for suspicious behavior. By detecting potential risks before transactions are completed, the platform helps businesses stay compliant while reducing fraud and operational overhead.

7. Rewards and Card Program Management

To drive platform usage, businesses need tools that incentivize transaction volume. Rain includes customizable reward mechanics that let operators structure custom cashback and loyalty systems for their card programs. Corporate administrators manage these programs through a central dashboard, setting up spending caps, merchant category blocks, and custom card rewards.

How to Build a Stablecoin Card Platform Like Rain?

Building a stablecoin card platform requires balancing blockchain tech with traditional banking rules. To compete with platforms like Rain, you need a clear strategy that connects digital assets to retail networks. We help entrepreneurs navigate this process by engineering the core software layer and managing the complex vendor integrations required for launch.

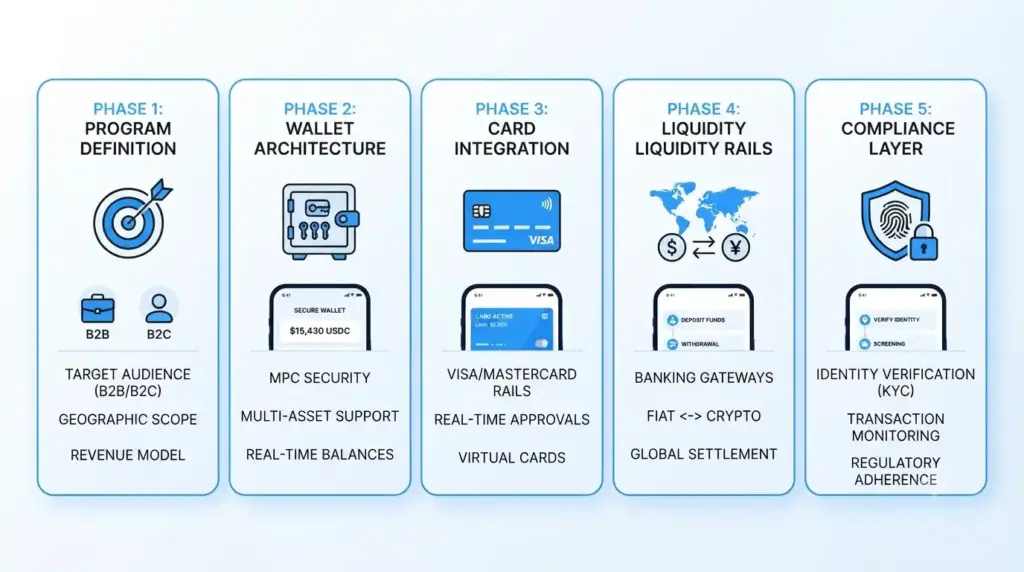

Our team approaches development by breaking the architecture into clear, modular phases. This structured path ensures your product launches securely without wasting capital on redundant technical systems.

1. Program and Target Definition

Before writing code, you must identify your core audience. Building an enterprise expense tool requires different features than creating a consumer rewards card. This choice determines your regulatory needs, target regions, and revenue model. We work alongside you during this discovery phase to map out the technical architecture.

If you target international businesses, the focus shifts toward high-limit physical cards and deep corporate treasury dashboards. For consumer wallets, the priority becomes instant virtual card generation and mobile app integrations.

- B2B Focus: Prioritizes corporate spend controls, multi-user permissions, and high-volume settlement rails.

- B2C Focus: Emphasizes quick onboarding, mobile wallet integrations, and interactive loyalty features.

- Geographic Scope: Determines which regional licenses and banking partners your platform requires.

2. Secure Wallet Architecture

A stablecoin card platform needs a secure wallet infrastructure that supports major assets like USDC and USDT across multiple blockchain networks. We build this foundation using institutional-grade security technologies such as multi-party computation, ensuring funds remain protected while transaction histories and balances are updated in real time. This gives users a reliable experience across both mobile and web applications.

3. Card and Network Integration

To let users spend stablecoins in everyday transactions, your platform needs to connect with Visa or Mastercard through a licensed issuer or network partner. We build the integration between your blockchain infrastructure and traditional payment rails, enabling secure real-time transaction approvals. This allows users to pay with stablecoins while merchants continue receiving local currency through their existing payment systems.

4. Liquidity and Transfer Rails

A card platform needs fluid movement between cash and crypto. Users require intuitive tools to fund accounts via traditional bank transfers and convert digital tokens back into local currencies. We integrate compliant banking gateways that handle these fiat interactions smoothly. By connecting your system to regional clearinghouses, we automate local funding and withdrawals while keeping processing costs low.

- Inbound Transfers: Automated systems convert incoming local bank wires into digital tokens instantly.

- Outbound Liquidation: Deep liquidity routing moves funds from stablecoins back to legacy bank accounts with minimal slippage.

- Wallet Transfers: Instant onchain distribution allows users to send international payments without using slow correspondent banking systems.

5. Transaction Compliance Layer

Operating a global payment platform means meeting strict financial regulations. You must verify user identities, track fund sources, and prevent unauthorized transactions across different jurisdictions. We integrate automated compliance tools into your core payment architecture. This software runs identity verifications and screens wallet addresses concurrently with transaction processing.

Our architecture also maintains high data security standards, including PCI DSS compliance. This protects sensitive customer data and card numbers, ensuring your business stands up to strict banking audits.

6. Launching Developer APIs

To scale like Rain, your platform should offer APIs that let other businesses build on top of your infrastructure. We develop secure and well-documented APIs for card issuing, wallet creation, and balance management, making it easy for fintechs to integrate your services into their own products. This expands your platform beyond a single application and creates new opportunities for enterprise partnerships and recurring B2B revenue.

7. Testing and Optimization

Before launching, your platform needs thorough testing to ensure it can handle real-world transaction volumes without performance issues. We test the infrastructure in secure sandbox environments, simulate large numbers of transactions, perform security audits, and optimize system performance before deployment. This helps deliver a stable, secure, and scalable platform that is ready for production use.

Cost to Build a Stablecoin Card Platform Like Rain

Capital allocation for a digital asset payment platform depends entirely on product scale and compliance scope. Launching a platform like Rain requires balancing specialized blockchain engineering with legacy banking integrations. We map out these costs transparently so your leadership team can budget effectively and avoid capital waste.

The choice between a streamlined market entry and an institutional ecosystem dictates your upfront investment. We specialize in building both models, ensuring your engineering capital directly fuels your strategic business goals.

MVP Cost Breakdown

An MVP for a stablecoin card platform typically costs between $80,000 and $180,000. At this stage, the focus is on launching the core payment experience, validating market demand, and attracting early users without overspending. We accelerate development by integrating trusted third-party services for compliance, card issuing, and payment processing, helping you launch faster while keeping the initial investment under control.

| Development Component | Estimated Allocation | Primary Deliverables |

| Core Wallet Architecture | $25,000 – $45,000 | Embedded USDC/USDT wallets, multi-party computation security |

| Virtual Card Rails | $20,000 – $40,000 | Visa/Mastercard API connections, instant card generation |

| Identity & Compliance | $15,000 – $30,000 | Automated KYC/AML partner plugins, user onboarding |

| Management Interfaces | $20,000 – $65,000 | Admin dashboard, transaction ledger, customer mobile web app |

Enterprise Platform Cost

An enterprise-grade stablecoin card platform typically costs between $250,000 and $600,000+, depending on the scale and level of customization. This investment is ideal for fintechs and established businesses that need high transaction capacity, advanced compliance, and dedicated infrastructure. We build these platforms with custom architecture, enterprise-grade security, and scalable systems designed to support long-term growth and large user bases.

This means fewer dependencies on middleman providers, lower per-transaction processing fees, and higher long-term profit margins for your business.

- Physical and Virtual Issuing: Custom plastic or metal card production pipelines integrated with global distribution networks.

- Multi-Chain Treasury: Native liquidity routers across networks like Solana, Base, and Ethereum to optimize transaction fees.

- Advanced Risk Engines: Custom fraud detection algorithms that block suspicious transactions before settlement.

- Institutional Standards: Full bank reconciliation systems, deep analytics suites, and audited PCI DSS data environments.

Factors Influencing Development Cost

Your final budget depends heavily on specific technical and regulatory choices. Understanding these variables helps you avoid unexpected expenses during the development cycle. Our team helps you evaluate these variables early in the planning stage to choose the most cost-effective path forward:

- Card Network Tier: Securing a direct Principal Membership with Visa involves high capital reserves. Partnering with a sponsored BIN issuer lowers initial costs but requires a small revenue share.

- Licensing and Compliance: Operating your own money transmitter licenses involves heavy legal costs. Utilizing our pre-integrated compliance networks bypasses this hurdle during your launch phase.

- Blockchain Selection: Supporting a single stablecoin on one network keeps costs down. Expanding to a multi-chain environment requires more complex smart contracts and deeper liquidity management systems.

- Security Audits: Institutional platforms require thorough code reviews from top-tier cybersecurity firms to protect corporate funds and secure banking trust.

Stablecoin Cards vs Traditional Card Programs: Business Comparison

Deploying capital into a card payment program requires understanding the differences between legacy banking systems and decentralized finance. While both models allow users to spend funds at global merchant locations, the underlying technologies create distinct business realities. Evaluating these trade-offs helps you determine which framework aligns best with your commercial goals.

Settlement Speed and Payment Infrastructure

Traditional card programs operate on a fragmented banking network built decades ago. When a user swipes a legacy card, the payment goes through multiple clearinghouses and correspondent banks. This architecture requires rolling settlement windows, meaning businesses often wait two to five business days to access their transaction capital.

Stablecoin card platforms completely bypass these legacy clearing windows by settling transactions directly on the blockchain.

- Constant Liquidity: Onchain transactions settle in real time, giving your business 24/7 access to capital without weekend or holiday delays.

- Simplified Accounting: Immediate transaction execution eliminates the complex balancing routines required by multi-day bank settlements.

- Minimized Settlement Risk: Instant asset verification prevents payment defaults and lowers the operational capital required to protect the network.

Consider Nexo and its hybrid Mastercard model. By allowing users to spend stablecoins or borrow instantly against digital assets, Nexo captures massive transaction velocities. This real-time settlement infrastructure sustains their substantial market operations, driving an ecosystem that supports over $7 billion in assets under management while generating consistent transactional fee revenue.

Cost, Scalability, and Global Expansion

Expanding a traditional card program across multiple countries usually means setting up local banking partnerships, meeting different regulatory requirements, and maintaining separate payment infrastructure. Stablecoin card platforms simplify this process by using a single blockchain-based system, making it easier to launch globally while reducing operational costs.

A good example is Wirex, which operates its card programs in over 130 countries through a unified infrastructure. This approach has helped the company generate an estimated $27 million in annual revenue, showing how stablecoin-based payment platforms can achieve global scale without the complexity of traditional banking expansion.

Which Model Is Better for Modern Fintechs?

For founders launching digital-first financial tools, the choice depends on balancing market entry speed against your core product goals. Traditional card networks offer immediate brand recognition, but their rigid structures can limit product flexibility and slow down development timelines.

We design and deploy stablecoin payment architectures that blend the strengths of both worlds. By utilizing blockchain rails for backend settlement and global card networks for retail acceptance, we help you launch highly flexible financial products quickly.

| Business Metric | Traditional Card Programs | Stablecoin Card Platforms |

| Launch Timeline | 9 to 12+ months | 2 to 4 months with our infrastructure |

| Settlement Windows | 2 to 5 business days | Instantaneous, 24/7/365 |

| Cross-Border Fees | High interchange and FX markups | Fractional onchain network fees |

| Target Audience | Domestically banked consumers | Global businesses, freelancers, unbanked regions |

Build a Stablecoin Card Platform with Idea Usher

Deploying a complex fintech asset requires an engineering partner who understands both decentralized protocols and legacy banking infrastructure. At Idea Usher, we take your vision and transform it into a secure, market-ready card platform. Our process focuses on reducing development friction, protecting your investment capital, and building infrastructure that scales smoothly from day one.

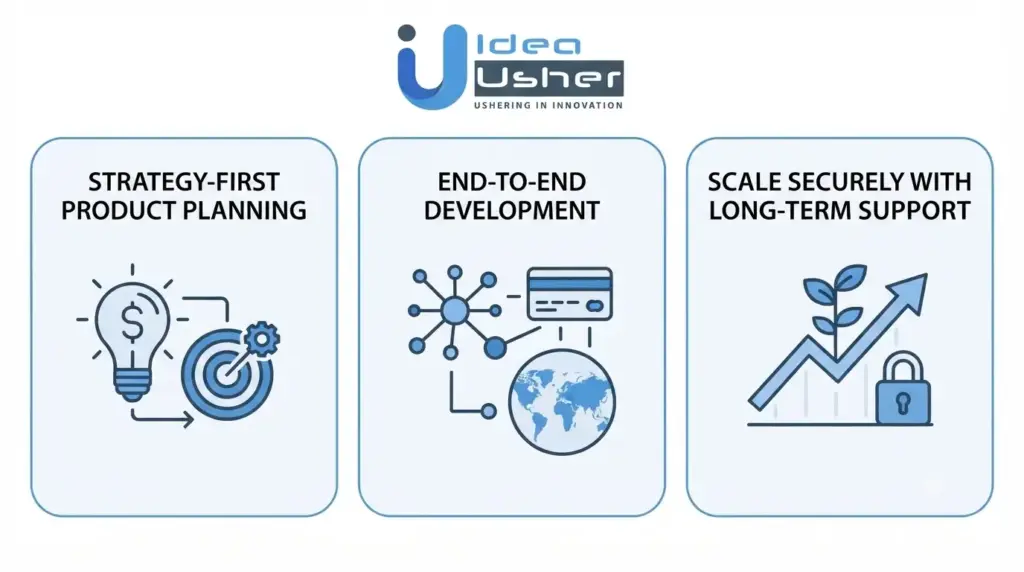

Strategy-First Product Planning

Every successful stablecoin card platform starts with a clear strategy. We work closely with your team to define the product vision, identify the most valuable features, and choose the right blockchain, card network, and monetization model before development begins. This early planning keeps the project focused, reduces unnecessary costs, and helps you launch with a platform built for long-term growth.

End-to-End Development

We handle the entire development lifecycle of your stablecoin card platform. Our engineers design the core ledger systems, build secure wallet layers, and integrate global payment APIs seamlessly. With over 500,000 hours of coding experience, our team of ex-MAANG/FAANG developers delivers secure, enterprise-grade fintech solutions built to last. Our development expertise spans across every technical layer of the application:

- Sovereign Cryptography: Building robust multi-party computation wallets to eliminate single points of failure.

- Network Integration: Connecting your core backend software smoothly into Visa and Mastercard transaction rails.

- API Architecture: Designing clean, developer-friendly endpoints that allow your enterprise clients to launch custom card programs.

- Data Security Standards: Programming secure server environments that maintain absolute PCI DSS compliance guidelines.

Scale Securely with Long-Term Support

Launching your platform is only the beginning. We continue to support your product with performance monitoring, security updates, infrastructure scaling, and new feature integrations as your user base grows. As regulations and blockchain technologies evolve, we help keep your platform secure, compliant, and ready to scale without disrupting your business.

Conclusion

Building a stablecoin card platform like Rain requires much more than integrating blockchain with payment cards. Success depends on combining secure wallet infrastructure, card network integrations, regulatory compliance, and scalable payment systems into a seamless user experience. With the right development partner, businesses can launch a platform that supports global payments, creates new revenue opportunities, and is ready to grow as stablecoin adoption continues to accelerate.

Things to Know About Stablecoin Card Platforms

A1: A stablecoin card platform lets people spend digital currencies like USDC or USDT just as they would with a regular debit or credit card. Behind the scenes, the platform converts blockchain transactions into payments that work with existing card networks. For users, the experience feels familiar, while businesses benefit from faster settlements and the ability to serve customers across different countries.

A2: Most platforms earn money every time users make card payments. They also generate revenue by offering premium business features, charging for card programs, or providing APIs that other fintech companies can integrate into their products. As transaction volume grows, these recurring revenue streams become increasingly valuable.

A3: Most businesses start with USDC because it is widely accepted and trusted by enterprises. USDT is another common choice for global payments. The right option depends on where your users are located and how they plan to use the platform, so many products eventually support more than one stablecoin.

A4: They can be, but compliance needs to be built into the platform from day one. This usually means verifying users before they access financial services, monitoring transactions for suspicious activity, and following the regulations of every country where the platform operates. Getting compliance right is one of the biggest factors behind a successful launch.