For decades, getting a loan meant bowing to the almighty FICO score, a rigid and outdated report card that decides your financial fate based on a narrow snapshot of your past. But here’s the harsh truth: your credit score is lying.

After doing some research, we found out that:

- 26 million Americans are considered “credit invisible”, shut out of loans because they don’t fit traditional scoring models

- 79 percent of freelancers struggle to access credit despite having steady income (PYMNTS)

- Immigrants pay 3.5 percent higher interest rates due to thin or nonexistent credit files (New York Fed)

Traditional credit scoring often overlooks individuals with steady finances but nontraditional credit profiles, such as freelancers without credit cards, immigrants starting fresh, or those who avoid debt. AI credit scoring models are now helping bridge this gap by analyzing a broader range of data to provide fairer and more accurate assessments.

By evaluating real financial activity such as spending habits, utility payments, and income flow, it gives lenders a clearer view of a person’s true creditworthiness. This makes the lending process faster, more inclusive, and grounded in real behavior, not outdated formulas.

In this blog, we’ll break down what’s involved in building an AI-powered credit scoring app, from core technologies to regulatory safeguards, and how businesses can use it to offer faster, fairer lending experiences. With deep experience in mobile app development and real-world expertise in AI-driven credit solutions, Idea Usher has helped clients bring powerful, compliant lending platforms to life across diverse markets.

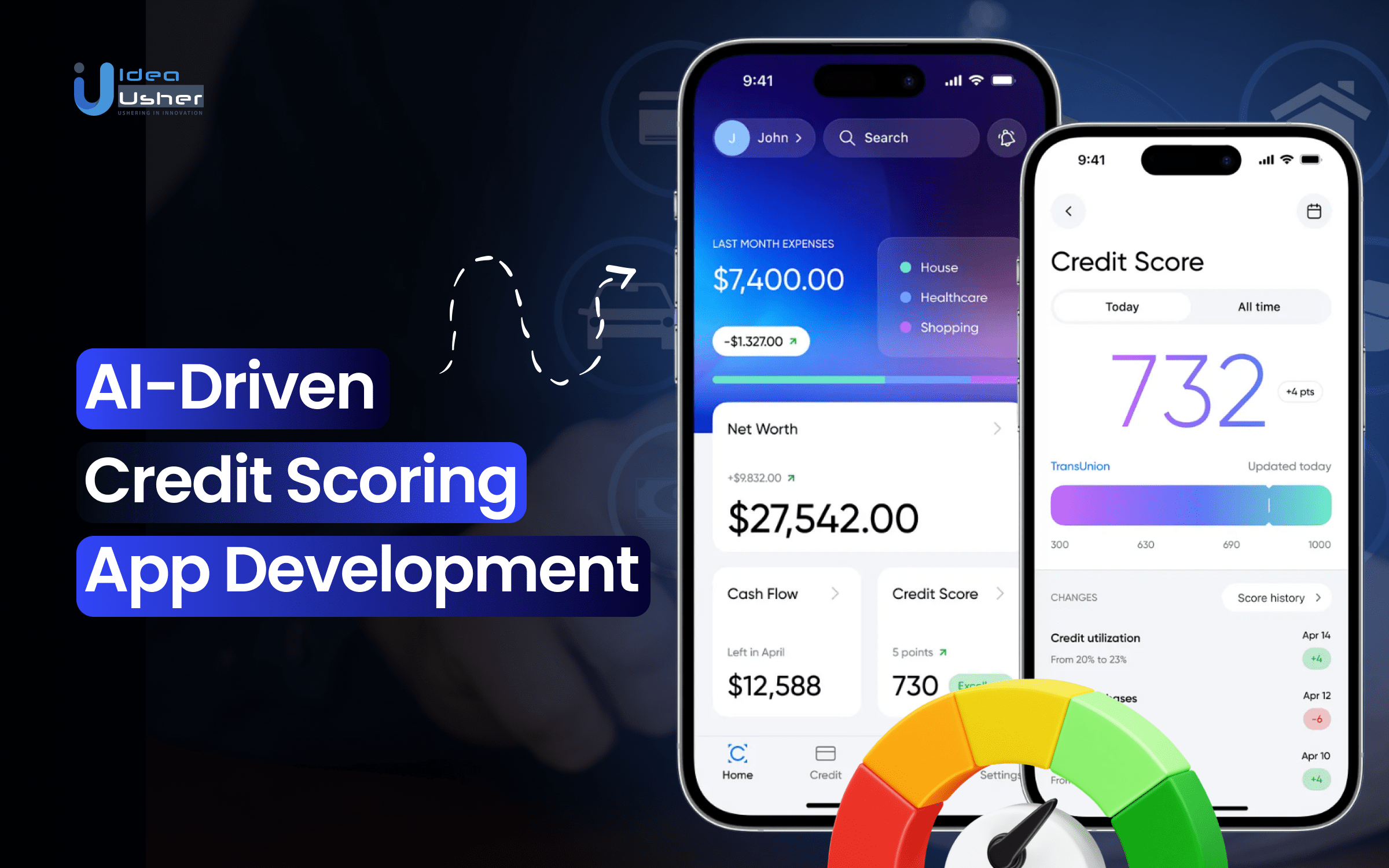

Overview of an AI-Driven Credit Scoring App

An AI-driven credit scoring app is a modern financial tool that uses machine learning, real-time data processing, and non-traditional data sources to assess a person’s creditworthiness. Rather than relying only on FICO scores or credit bureau records, these systems evaluate how individuals manage their money based on actual behavior.

Unlike traditional credit scoring models, AI-powered systems:

- Review thousands of real-time data points including bank transactions, rent and utility payments, and even mobile or online activity

- Continuously update risk assessments, rather than depending on monthly bureau reports

- Focus on financial behavior, not demographics, helping reduce bias in lending decisions

- Provide fair assessments for thin-file or “credit invisible” users often overlooked by legacy systems

AI vs. Traditional Credit Scoring: A Breakdown

| Factor | Traditional Scoring | AI-Driven Scoring |

| Data Used | FICO score, credit history, debt-to-income | Bank transactions, utility payments, gig income |

| Approval Speed | Days to weeks | Minutes to hours |

| Bias Risk | High – depends on legacy demographic models | Lower – behavior-based and adaptive |

| Flexibility | Fixed criteria (e.g., “must have 2 credit cards”) | Dynamic rules based on evolving user data |

| Default Prediction | 60–70% accuracy | 85–90%+ accuracy (based on Upstart internal reports, 2023) |

Why It Matters?

AI-driven credit scoring doesn’t just automate existing systems, it transforms how risk is measured. By evaluating what people actually do with their money, rather than relying on outdated scoring formulas, these tools offer a fairer path to credit for millions who have long been excluded from traditional financial systems.

Key Market Takeaways for AI-Driven Credit Scoring Apps

According to InsightaceAnalytic, the AI-driven credit scoring market is on a sharp upward trajectory, projected to grow at a CAGR of 25.9 percent from 2024 to 2031. This surge is driven by the rise of machine learning and the increasing use of alternative data sources, which enable more precise and real-time credit evaluations. By 2034, the market is expected to grow from USD 2.25 billion in 2025 to over USD 16 billion, signaling a major shift in how financial institutions assess creditworthiness.

Source: InsightaceAnalytic

AI-powered credit scoring apps are quickly reshaping lending practices. Instead of relying solely on credit history, these systems utilize unconventional data, such as education, employment background, online shopping patterns, or even mobile activity, to build a more comprehensive financial profile.

Platforms such as Upstart, Zest AI, and LenddoEFL have shown how effective this approach can be. For instance, Upstart has cut default rates by 75 percent while expanding credit access to borrowers with limited or no traditional credit history.

Partnerships are accelerating this shift. Scienaptic AI’s integration with DigiFi gives lenders access to AI signals that improve approval rates by up to 40 percent without increasing risk.

In the MENA region, Fintech Galaxy and FinbotsAI are making AI-based credit decisioning more accessible to regional banks and lenders.

A Perfect Time to Invest in Developing AI Credit Scoring Apps

The lending industry is undergoing a major shift as traditional credit models fall short of serving today’s diverse borrower base. Millions of consumers are still denied access to credit due to outdated scoring systems that overlook real-world financial behavior. AI credit scoring models power innovative credit scoring apps that analyze alternative data, such as transaction history, utility payments, and gig income, giving lenders faster and more accurate insights.

This expanded lens allows institutions to approve more responsible borrowers while keeping default rates in check.

The business case for investing in this space is already proven. Upstart, one of the pioneers in AI-based lending, reported $637 million in revenue in 2024 with loan originations reaching $5.9 billion.

Zest AI, which helps lenders deploy explainable AI risk models, grew its revenue to $87.7 million in 2023, up from just $5 million in 2021. These numbers reflect not just user adoption, but real financial traction and profitability in a market hungry for innovation.

From a product standpoint, these platforms are scalable, modular, and monetizable in multiple ways. Businesses can generate revenue by licensing technology to banks and credit unions, launching their own lending services, or offering premium features such as real-time fraud detection and credit decisioning APIs.

Key Features We Include in AI Credit Scoring Apps

After working on many AI credit scoring projects, we’ve noticed certain features consistently make the biggest difference in usability, performance, and compliance. While developing similar solutions for our clients, we drew inspiration from some of the best in the industry to build practical, effective tools.

1. Streamlined Onboarding with AI-Powered KYC

A smooth onboarding process is essential. Inspired by how Upstart uses AI for identity verification, we include biometric authentication and document scanning to speed up sign-ups. This reduces friction for users and helps meet regulatory requirements without unnecessary delays.

2. Multi-Source Data Aggregation

To provide a fuller picture of creditworthiness, we gather data from multiple sources like bank accounts, utility bills, and mobile behavior, much like Kueski does. This approach helps include people who don’t have a traditional credit history, ensuring fairer lending decisions.

3. Real-Time Risk Scoring Engine

Our risk engines learn and improve continuously, inspired by Upstart’s success in lowering defaults through adaptive models. By analyzing up-to-date financial data, lenders get accurate risk scores that help make better, faster decisions.

4. Auto-Generated Credit Reports

Consistent and clear credit reports matter. Following Zest AI’s lead, we build tools that generate detailed, customizable reports so lenders can quickly understand an applicant’s profile and make informed decisions.

5. Custom Rule Configuration

Every lender has different standards. Taking a page from Nova Credit’s flexible systems, we build rule engines that let lenders set their own criteria for approvals and risk thresholds, adapting to different loan products and markets.

6. Decisioning Dashboard

Quick access to application data is vital. Scienaptic AI’s dashboards inspired us to create intuitive interfaces where lenders can see application statuses and risk factors in real time, speeding up approvals and monitoring.

7. Audit Logs & Explainable AI

Transparency and trust go hand in hand. We follow Zest AI’s example by including full audit trails and explanations for every credit decision. This supports compliance and helps lenders understand how decisions were made.

8. Admin Controls & Access Management

Strong security and governance are non-negotiable. Inspired by Upstart’s strict role-based access controls, our admin panels ensure only authorized users can manage sensitive data or change scoring logic, safeguarding compliance and data integrity.

How AI Enhances Credit Scoring Accuracy?

Traditional credit scoring relies on fixed rules and limited data, often leading to outdated and unfair decisions. AI credit scoring models transform this process by using machine learning and diverse data sources, making credit evaluations more accurate, adaptable, and inclusive for a wider range of borrowers.

Supervised Learning Models: The Core of AI Credit Scoring

AI credit scoring systems learn from large datasets linking borrower information to repayment outcomes. Key techniques include:

- XGBoost: This method helps identify the most important factors, like income stability over age. For example, Upstart uses XGBoost to weigh education and job history, cutting defaults by 27% compared to traditional models.

- Random Forest: By averaging multiple decision trees, this approach reduces errors and improves clarity. Zest AI applies this to make lending decisions more transparent.

- Neural Networks: These models find complex patterns in unstructured data, such as transaction details, revealing subtle risk indicators.

Alternative Data: A Fuller Financial Picture

AI examines non-traditional data to fairly score people with limited credit history:

| Data Type | Use Case | Example Apps |

| Bank Transactions | Detect steady income, like freelance earnings | Nova Credit, Tala |

| Mobile Usage | Phone bills and app behavior show reliability | Kueski |

| Rent & Utilities | Show responsible payment without credit cards | Experian Boost |

| Social Signals | Verify employment while managing bias risks | LenddoEFL |

In many regions, Tala uses smartphone data to approve loans in minutes, making credit more accessible.

How We Build AI-Powered Credit Scoring Platforms?

We follow a structured, proven process to develop AI-driven credit scoring apps that meet the unique needs of our clients and their markets. Here’s how we bring these advanced platforms to life:

1. In-Depth Market Research and Requirement Analysis

We begin by thoroughly understanding the client’s target market, regulatory environment, and user needs. This helps us identify pain points in existing credit scoring systems and tailor features that add real value.

2. Identifying and Integrating Diverse Data Sources

We work closely with clients to pinpoint both traditional and alternative data sources—such as bank statements, utility payments, and behavioral data, and build secure, scalable integrations to collect and normalize this data.

3. Ensuring Regulatory Compliance from Day One

Compliance is baked into our design. We align with GDPR, AML, and fair lending regulations, implementing data privacy measures, secure storage, and explainability features that satisfy regulatory standards and build user trust.

4. Designing and Training Custom AI Models

Our data scientists select and customize machine learning algorithms, such as XGBoost, Random Forest, and Neural Networks, that best fit the client’s data and risk profile. These models are rigorously trained on relevant datasets to provide accurate, unbiased credit risk predictions.

5. Building Robust Data Pipelines and Infrastructure

We develop efficient data pipelines that handle ingestion, cleansing, and transformation, ensuring data flows seamlessly through the system. Our infrastructure supports real-time processing to keep credit scores up to date.

6. Crafting User-Friendly Interfaces

From borrower onboarding with AI-powered KYC to lender dashboards displaying credit reports and risk analytics, we design intuitive, secure, and compliant user experiences that drive adoption and ease decision-making.

7. Integrating Risk Engines and Customizable Rule Sets

We embed AI credit scoring models into the platform’s decision engine and provide clients with flexible rule engines. This allows lenders to tailor approval criteria and automate workflows based on their specific policies, ensuring smarter and more efficient lending decisions.

8. Rigorous Testing and Bias Auditing

Before launch, we conduct extensive testing for accuracy, fairness, and resilience. Our bias audits help detect and mitigate potential discrimination, ensuring the models treat all applicants equitably.

9. Deployment, Monitoring, and Continuous Enhancement

Post-launch, we monitor system performance closely and retrain AI models regularly with new data. This ongoing support helps clients stay ahead of market changes and regulatory updates while continuously improving predictive power.

Cost of Developing an AI-Driven Credit Scoring App

Developing an AI-driven credit scoring app involves a combination of advanced technology, data integration, and regulatory compliance, all of which influence the overall cost.

| Phase / Component | Description | Estimated Cost Range (USD) |

| 1. Research & Discovery | Market research, requirements, feasibility, compliance analysis, and AI strategy | $500 – $2,500 |

| 2. UI/UX Design | Wireframes, prototyping, visual design using lean methods | $1,000 – $10,000 |

| 3. AI / ML Development | Data prep, AI model integration or basic ML model, feature engineering | $2,500 – $20,000 |

| → Data Acquisition & Cleaning | Sourcing and cleaning public or proprietary datasets | $1,000 – $5,000 |

| → AI Model Integration or Custom Build | API integration (e.g., GiniMachine) or basic in-house model (scikit-learn) | $5,000 – $15,000 |

| → Feature Engineering (if custom model) | Transforming raw data into AI-usable features | $2,500 – $5,000 (included) |

| 4. Backend Development | User auth, API services, DB setup, cloud hosting | $2,000 – $17,500 |

| 5. Frontend Development | UI development using React Native or Flutter, dashboard, score display | $1,500 – $12,500 |

| 6. App Features (Component Breakdown) | ||

| → User Registration | Email/password login, basic auth flow | $500 – $2,000 |

| → Loan Application Form | Input form for user financial data | $700 – $2,500 |

| → Credit Score Display | Visual output of score with insights | $500 – $1,500 |

| → Basic User Dashboard | Simple summary view of user’s credit activities | $500 – $1,500 |

| → API Integrations | Integrations with credit APIs or payment services | $1,000 – $5,000 per API |

| → Push Notifications | Alerts and reminders | $300 – $800 |

| 7. Testing & QA | Functional, usability, security, and AI output testing | $1,000 – $7,500 |

| 8. Project Management & DevOps | Coordination, versioning, deployment, and basic monitoring | $500 – $5,000 |

Total Estimated Cost: $10,000 – $50,000

Please note that this is a general estimate intended to provide a starting point. We’re happy to connect with you directly to discuss your specific requirements and deliver a more accurate, tailored cost assessment for your AI-driven credit scoring app.

Factors Affecting the Development Cost of an AI-Driven Credit Scoring App

The cost of developing any application depends on factors such as team size, location, technology choices, and project complexity. AI credit scoring models add another layer of complexity to credit scoring apps, impacting the budget due to their intensive data requirements, advanced algorithms, and the need to meet strict regulatory standards.

Several key factors affect development costs unique to these apps:

- Data Volume, Variety, and Quality: The amount and diversity of data—ranging from traditional credit reports to alternative sources like utility payments—impact expenses for acquiring, storing, cleaning, and preparing data. Poor data quality requires extra effort to make it usable, which raises costs.

- AI Model Complexity and Customization: A basic predictive model is relatively inexpensive, but designing and fine-tuning sophisticated deep learning or ensemble models demands more time, expertise, and computing power, increasing overall costs.

- Use of Third-Party APIs vs. Building In-House Models: Leveraging existing credit scoring or AI services through APIs can reduce costs compared to developing custom AI models from scratch, which requires a skilled data science team and extensive datasets.

- Bias Detection and Mitigation: Ensuring the AI system treats all applicants fairly involves ongoing monitoring, testing, and adjustments. This process requires specialized tools and expertise, adding unique costs beyond typical app development.

Compliance and Ethical Considerations in AI-Driven Credit Scoring

AI is transforming how lenders assess credit risk, enabling faster and more data-driven decisions. However, this shift brings new challenges around fairness, transparency, and privacy. To build trustworthy and compliant systems, lenders and fintech companies must ensure their AI credit scoring models address these concerns effectively.

1. Explainability and Model Transparency

Credit decisions affect people’s financial lives deeply, so it’s essential that AI models can clearly explain why someone was approved or declined. Many advanced AI systems act like “black boxes,” making their reasoning hard to understand. This opacity creates problems for regulators, lenders, and borrowers alike.

To solve this, AI credit scoring should use explainability methods such as:

- SHAP: Measures how each factor (like income or payment history) impacts the score.

- LIME: Creates simple, easy-to-understand explanations for individual cases.

- Simpler Models: Tools like decision trees offer clearer, auditable decision paths compared to complex neural networks.

These approaches help companies comply with laws and build user confidence by making decisions transparent.

2. Navigating Data Privacy and Credit Regulations

AI credit scoring must respect the growing landscape of privacy laws and financial regulations. Key frameworks include:

| Regulation | Impact on AI Credit Scoring |

| GDPR (EU) | Requires clear consent for data collection and grants borrowers the right to understand how their scores are calculated. |

| CCPA (California) | Allows consumers to opt out of data sharing and demands transparency for automated decisions. |

| Fair Credit Reporting Act (U.S.) | Ensures credit reports are accurate and provides borrowers with dispute rights. |

| Anti-Discrimination Laws (e.g., ECOA) | Prohibits bias against protected groups based on race, gender, age, and more. |

To comply, lenders should implement:

- Data anonymization to protect personal information.

- Clear explanations of credit decisions to borrowers.

- Regular audits to verify models align with legal standards.

3. Tackling Bias in AI Models

Historical credit data often reflects systemic inequalities. Without careful management, AI can reinforce these biases, unfairly limiting opportunities for some groups.

Effective bias mitigation includes:

- Cleaning Training Data: Removing or reweighting factors that correlate with protected attributes (for instance, ZIP codes tied to racial demographics).

- Adversarial Learning: Teaching models to ignore sensitive features such as ethnicity or gender.

- Fairness-Aware Algorithms: Adjusting classification thresholds to balance approval rates across diverse groups.

For example, Upstart’s AI platform demonstrates the power of these methods, reducing minority applicant approval disparities by nearly half.

Most Successful Business Models for AI-Driven Credit Scoring Apps

Here are the most successful business models for AI-driven credit-scoring apps,

1. Subscription-Based Model

In the subscription model, users pay a regular fee to access credit scoring tools powered by AI. This setup suits people and small businesses who want ongoing monitoring and personalized advice to improve their credit health over time. The steady income from subscriptions allows companies to improve their AI and add useful features continuously.

- For example, Credit Karma offers free credit monitoring but generates revenue through premium subscription services like identity theft protection and personalized financial advice.

- In 2023, Credit Karma reported over 110 million users globally, with subscription-based upsells contributing to a 20% revenue growth year-over-year.

2. Freemium Model with Upsells

This model gives users free access to basic AI credit insights while charging for advanced features or services. It’s a great way to attract a large audience fast, then gently guide some of them to paid options that provide deeper insights or extra protections.

- Experian Boost uses this model effectively. They provide free credit scores enhanced by AI that pulls in alternative payment data.

- Users can choose to pay for extra services like identity theft protection. This approach helped them grow to over 75 million users, with about 15% eventually upgrading to paid plans.

3. Data-as-a-Service to Financial Institutions

Some AI credit scoring companies don’t charge consumers directly. Instead, they package their AI-powered credit insights and sell them to banks and lenders. These financial institutions use the data to better assess risk and approve more loans responsibly.

- Zest AI is a prime example. Their AI models help lenders expand credit access to underserved borrowers while cutting defaults by up to 20%.

- This win-win approach increases loan approvals by 10-15%, helping both lenders and consumers.

Top 5 AI-Powered Credit Scoring Apps in the USA

After thorough research, we identified several AI-driven credit scoring apps that stand out for their innovative use of data and analytics to improve credit decisions.

1. Gaviti

Gaviti is an AI-powered credit management platform that streamlines the entire credit decision process. Its analytics engine provides real-time insights into payment behaviors and automates credit approvals and follow-ups. By consolidating all applicant data in one place, Gaviti reduces manual work and overdue receivables, helping businesses maintain healthier cash flow.

2. HighRadius

HighRadius uses advanced machine learning to assess creditworthiness, predict defaults, and automate credit limit reviews. It integrates smoothly with ERP systems, enabling large enterprises to automate complex credit workflows and make accurate, data-driven decisions at scale.

3. YayPay by Quadient

YayPay combines automation with predictive analytics to offer a comprehensive view of accounts receivable. Its AI forecasts payment behavior, prioritizes collections, and automates customer communications, reducing the time businesses spend chasing overdue invoices and improving cash flow management. It’s popular among mid-sized companies for proactive risk management.

4. ZestFinance

ZestFinance applies AI to both traditional and alternative data like online behavior to create more precise credit scores. This helps lenders include consumers with limited credit histories, expanding access for thin-file borrowers. Trusted by several major US lenders, ZestFinance has broadened credit availability to millions.

5. RiskSeal

Founded in 2022, RiskSeal enriches borrower profiles by analyzing digital footprints across 200+ platforms and over 300 data points. This deep data analysis allows lenders to evaluate applicants with little or no traditional credit history, increasing approval rates for underserved groups. RiskSeal is gaining rapid adoption among US lenders focused on smarter credit risk management.

Conclusion

AI-driven credit scoring is reshaping lending by making decisions smarter, more inclusive, and faster. Companies that leverage AI credit scoring models can stand out in a crowded market by delivering credit solutions that truly meet users’ needs. If you’re ready to build an AI-powered credit scoring app that sets you apart, Idea Usher is here to help bring your idea to life with expertise and care.

Looking to Develop an AI-Driven Credit Scoring App?

If you’re frustrated with outdated credit models that overlook freelancers, immigrants, and thin-file borrowers, it’s time to explore AI-powered credit scoring. At Idea Usher, we bring deep technical expertise and real-world experience to build smarter, fairer scoring systems.

- Our team, including former MAANG/FAANG engineers, has logged over 500,000 hours creating high-performance AI models like XGBoost, NLP, and federated learning that surpass traditional methods.

- We prioritize compliance and ethics, embedding transparency, bias reduction, and data privacy from the start.

- We know how to unlock value from alternative data like bank transactions, rent histories, and behavioral signals, to evaluate borrowers who’ve been ignored for too long.

From initial prototypes through to navigating complex regulations, we’re your partner every step of the way. Explore our recent projects to see how we bring these solutions to life.

FAQs

A1: Start by understanding who will use your app and what data you can access. Collect financial and behavioral information, then create AI models that learn to evaluate credit risk more accurately than traditional methods. Build a simple, secure interface, follow the rules around data privacy, and keep improving your system as you gather real user feedback.

A2: Costs depend on how complex your AI needs to be, the quality of data you use, and how strict the compliance requirements are. It’s an investment that includes skilled developers, data management, and ongoing updates. Going for the cheapest option can lead to problems with accuracy and user trust.

A3: A good app scores credit risk quickly using many data sources, including non-traditional ones. It detects fraud, offers personalized advice, keeps users informed with clear dashboards, and stays compliant with privacy laws. It also helps users understand how to improve their credit over time.

A4: They usually earn through subscriptions, free basic access with paid upgrades, selling insights to banks or lenders, or earning commissions by recommending financial products. The key is providing real value that keeps users and partners coming back.