Key Takeaways

- Multi-currency banking apps protect purchasing power by enabling users to hold, exchange and spend in stronger global currencies.

- Core capabilities include multi-currency wallets, real-time FX, local accounts and low-cost cross-border payments.

- Competitive exchange rates, currency diversification and smart FX tools help reduce inflation and currency depreciation risks.

- Secure banking infrastructure, compliance and global payment integrations are essential for scalable multi-currency banking platforms.

- How Idea Usher can help you build multi-currency banking app with secure fintech architecture, global banking integrations and enterprise-grade compliance.

Inflation is increasingly becoming a currency management problem rather than simply a cost-of-living issue. This shift is accelerating multi-currency banking app development as consumers, freelancers, global businesses and investors seek greater control over how, where and in which currencies they store and move their money.

Traditional banking relied on single-currency accounts, limited foreign exchange access, and costly international transfers. Today, users expect multi-currency wallets, real-time FX, local and international accounts, cross-border payments, global debit cards, instant currency conversion, exchange rate alerts, AI spending insights, virtual cards, and enterprise-grade security to preserve purchasing power, reduce FX costs, and respond quickly to currency volatility.

In this blog, we’ll explore how multi-currency banking apps help protect users against inflation, covering their core features, banking architecture, foreign exchange workflows, security considerations, and how IdeaUsher builds secure, scalable multi-currency banking app for a borderless financial ecosystem where money moves seamlessly across global markets.

Why Inflation Is Changing How People Manage Money

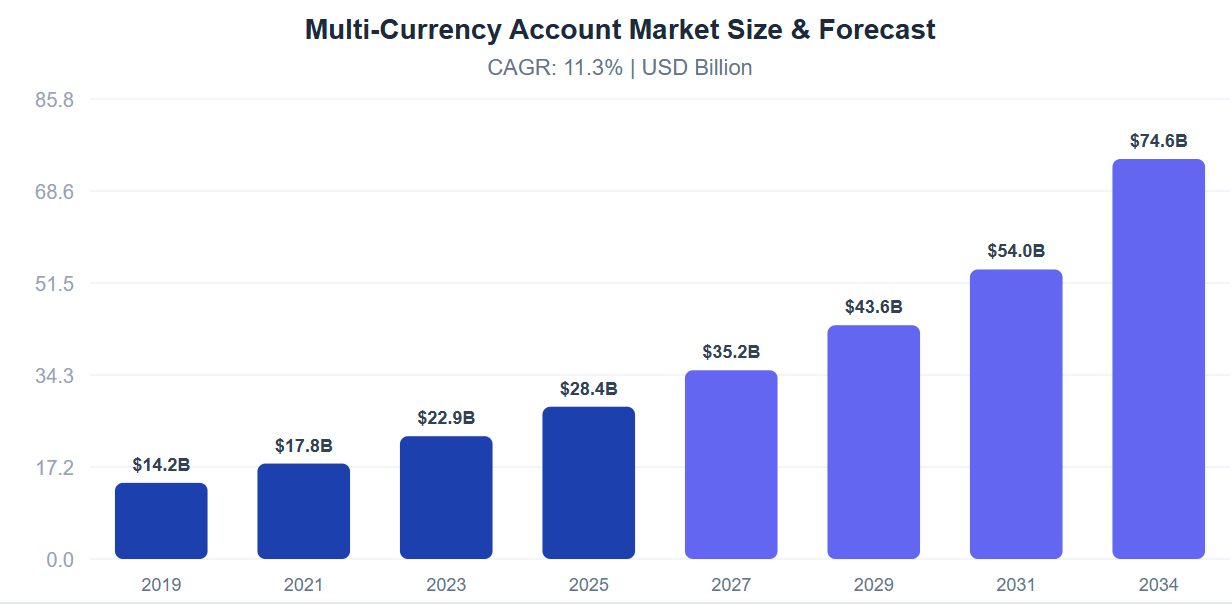

The global multi-currency wallets market is estimated at $28.4 billion in 2025 and is expected to reach $74.6 billion by 2034, growing at a 11.3% CAGR. Increasing cross-border payments, global travel, e-commerce, and demand for seamless currency management continue to drive adoption of multi-currency banking apps worldwide.

The baseline architecture of personal capital preservation has hit a historic global turning point. The International Monetary Fund (IMF) projects the global average inflation rate at 4.4%, with severe inflation persisting in countries like Venezuela (387.4%), Sudan (75.1%), and Iran (68.9%), highlighting the growing challenge of protecting purchasing power.

Even major economies continue to face inflationary pressure. The U.S. Bureau of Labor Statistics (BLS) reported a 4.2% annual increase in the Consumer Price Index (CPI-U), driven by a 23.5% rise in energy prices and a 6.1% increase in grocery costs. As traditional savings accounts struggle to outpace inflation, consumers are increasingly adopting alternative financial strategies to preserve purchasing power.

A. Why Local Currency Alone Is No Longer Enough

The core problem with legacy wealth management is the structural blind spot of relying entirely on a single domestic currency. When macroeconomic shifts look less like temporary spikes and more like structural changes, holding unhedged local cash reserves exposes individuals to severe capital-drag:

- The Global Purchasing Squeeze: Global goods prices have risen 2.0% annually, compared with a 0.9% baseline in previous cycles. While retail spending remains positive, real purchasing power has grown by only 0.1%–0.2%.

- The Negative Real-Yield Trap: In many emerging markets, savings accounts generate negative real returns after inflation and taxes, reducing purchasing power by 2.0%–5.0% annually.

- The Diversification Gap: Traditional banks keep savings concentrated in a single currency, limiting access to foreign currencies and dollar-pegged assets that can help reduce geopolitical and currency risk.

B. How Currency Depreciation Impacts Daily Purchasing Power

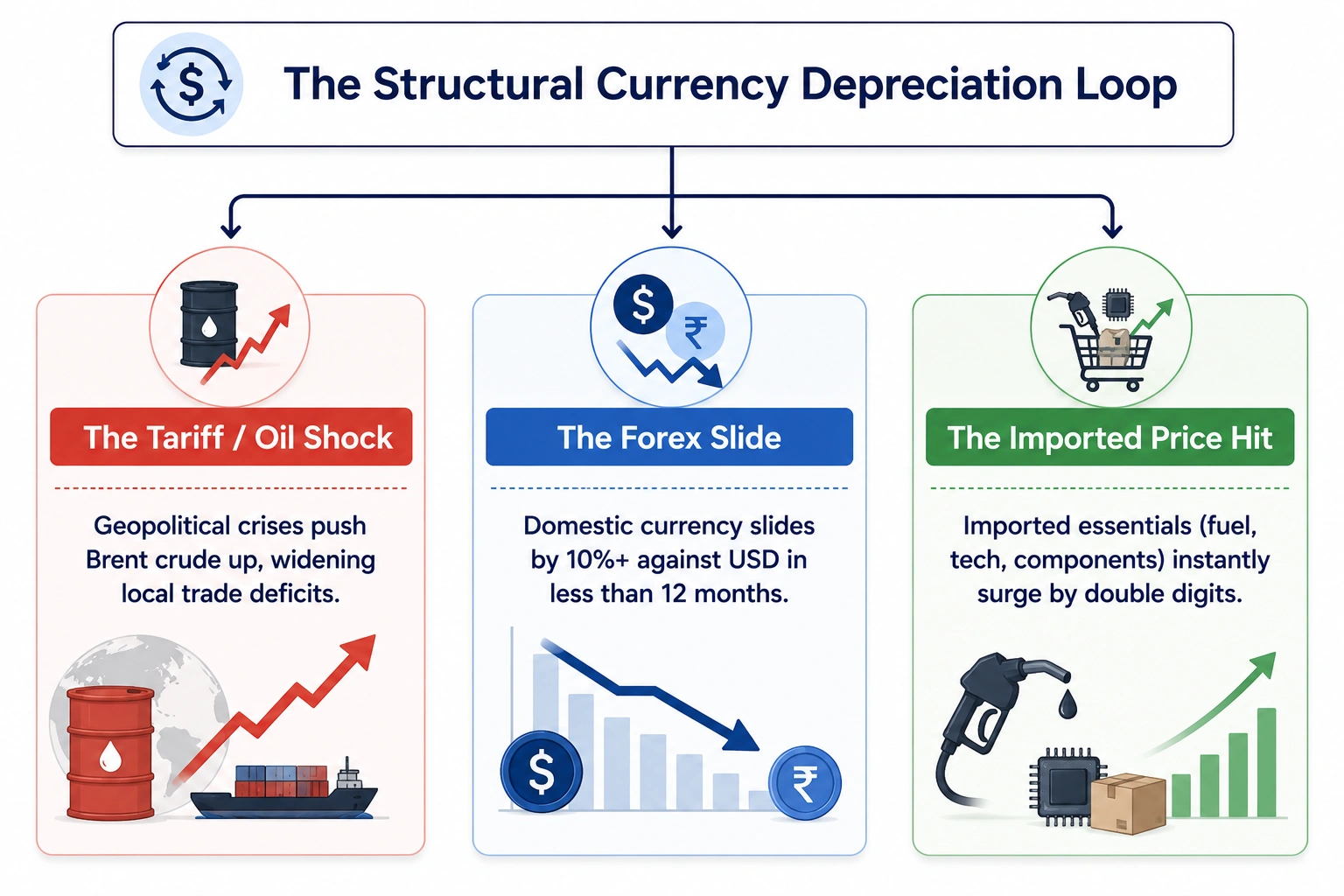

When a domestic currency undergoes a rapid slide against global reserve benchmarks, the economic damage hits household budgets immediately through imported inflation. This dynamic is clearly visible in major import-dependent corridors experiencing sharp currency corrections:

Understanding these economic trends reveals why preserving purchasing power has become a priority for consumers, businesses, and investors navigating today’s volatile global economy.

- The Double-Digit Currency Decline: The Indian Rupee (INR) fell 11% since the start of 2025, dropping to a record ₹96 per USD amid rising Brent crude prices and $17–18 billion in foreign portfolio outflows.

- The Inflation Multiplier Effect: With 88% of its crude oil imported, a 10% currency depreciation significantly increases fuel, transportation, manufacturing, and raw material costs, accelerating domestic inflation.

- The Global Currency Debasement: Currency weakness extends beyond emerging markets. Rising deficits and debt across the UK, Japan, and France have eroded fiat purchasing power, driving investors toward hard assets like gold, which has reached record highs.

C. Why Borderless Banking Is Becoming a Financial Necessity

To survive this continuous loss of purchasing power, consumers and global freelancers are bypassing legacy local banking systems in favor of decentralized, borderless financial platforms. Managing capital through a digital-first, multi-currency framework completely shifts how individuals protect their earnings.

Comprehensive digital adoption and global payment data highlight the massive scale of this financial migration:

| Financial Metric Vector | Traditional Retail Banking Rails | Borderless Stablecoin & Multi-Currency Platforms | The Direct Individual Impact |

| Cross-Border Transfer Costs | 6.2% – 6.5% global average fee per remittance. | Sub-1.0% total programmatic transfer costs. | Keeps an extra $50 to $65 in the pocket of an expat sender for every $1,000 sent home. |

| Capital Settlement Velocity | 3 to 5 Business Days via SWIFT and intermediary links. | Under 10 Minutes end-to-end global settlement. | Completely eliminates inflight capital lockups across weekends and banking holidays. |

| Asset Access & Optionality | Tied 100% to local currency and domestic bank risk. | Instant access to global digital dollars (USDC/USDT) and 3.5% – 5.0% APY tokenized yields. | Allows individuals in high-inflation regions to instantly hedge their liquid net worth. |

| The Contractor Shift | Manual invoice collection with heavy cross-border wire fees. | Seamless digital payroll integrations. | 35% of international contractors now actively request digital-dollar payouts for speed. |

The Structural Shift: This transformation is driving record adoption, with on-chain stablecoin transfer volume reaching an annualized $11.6 trillion. By replacing volatile local currencies with borderless financial infrastructure, individuals can access automated treasury strategies once reserved for multinational corporations, strengthening wealth preservation and purchasing power.

What Is a Multi-Currency Banking App?

A multi-currency banking app is a borderless digital financial platform that lets users hold, manage, send, and spend in multiple currencies from a single account. Instead of opening bank accounts in multiple countries, users receive local bank details such as a U.S. Routing Number, European IBAN, or UK Sort Code through one unified interface.

As cross-border payments accelerate toward $320 trillion, traditional single-currency accounts have become increasingly inefficient. Multi-currency banking apps overcome these limitations by providing real-time access to foreign exchange markets, enabling users to diversify currency exposure, hedge against inflation, and manage global funds as easily as local money.

A. How a Multi-Currency Banking Platform Works

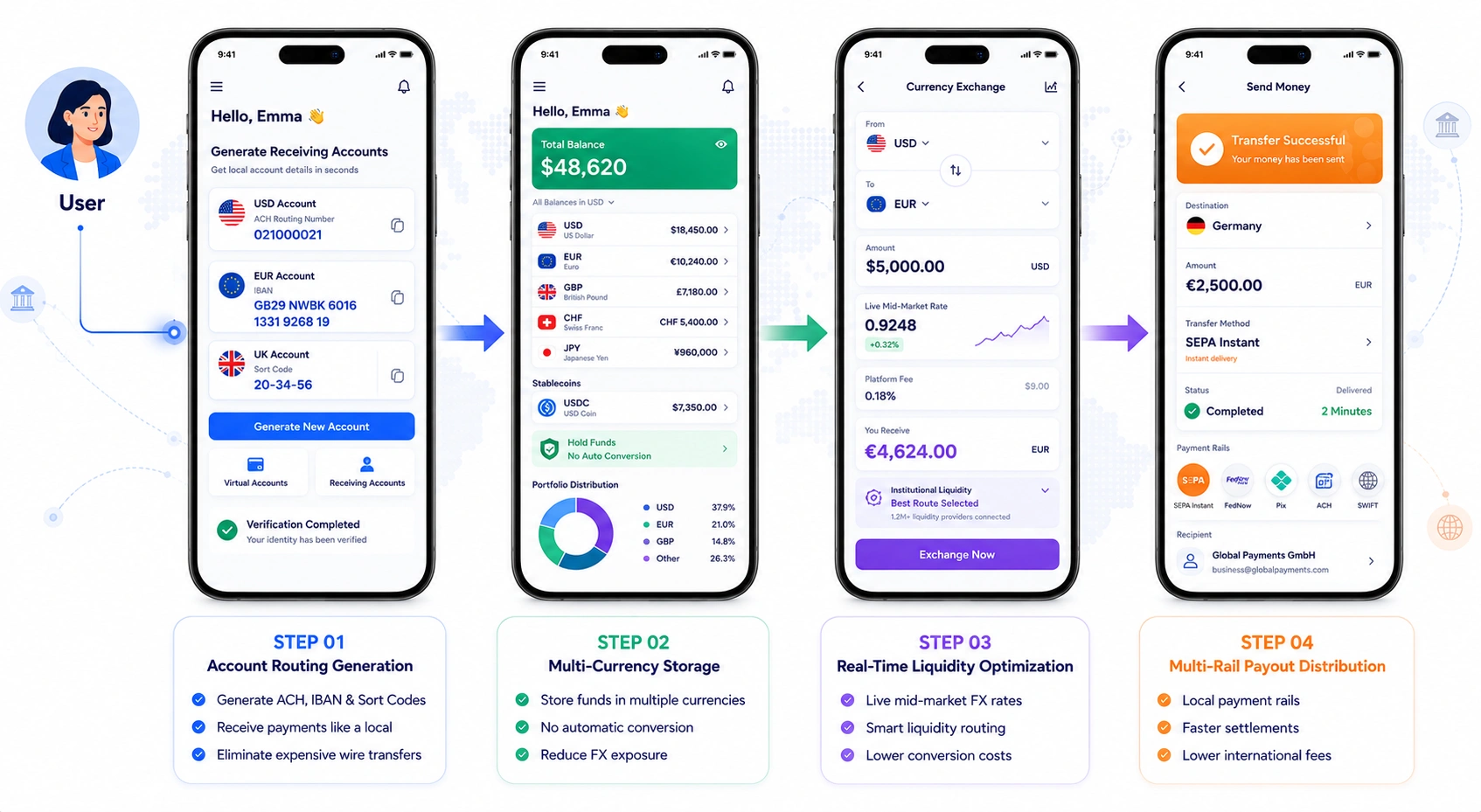

Behind the user-friendly interface, a multi-currency platform replaces the aging paperwork of traditional international banking with a programmatic, automated ledger loop.

Step 1: Account Routing Generation

The payment journey begins as the platform provisions local receiving accounts across multiple jurisdictions through API integrations. Users instantly receive ACH routing numbers, IBANs, or Sort Codes, allowing international payments to arrive as low-cost domestic transfers. For example, users in India or Europe can generate a native ACH routing number for U.S. clients, eliminating expensive international wire transfers.

Step 2: Multi-Currency Storing

Once funds arrive, they are stored in dedicated multi-currency sub-ledgers instead of being automatically converted. Users can hold USD, EUR, GBP, stablecoins, and other currencies under a unified account, reducing FX exposure, currency depreciation, and market volatility.

Step 3: Real-Time Liquidity Optimization

When users exchange or spend funds, the platform connects to institutional interbank liquidity providers for real-time mid-market FX rates matching. Intelligent routing minimizes the 3%–6% FX markups typically charged by traditional banks, delivering faster and more cost-efficient currency conversion.

Step 4: Multi-Rail Payout Distribution

For outbound transfers, the platform bypasses correspondent banks by routing payments through SEPA Instant, Pix, FedNow, and other local clearing networks. This enables rapid, low-cost international settlements with fewer delays than traditional cross-border payment systems.

B. Who Benefits Most From These Banking Apps

Multi-currency platforms are engineered specifically for actors operating within high-velocity, borderless economic corridors who require real-time control over their international cash flows.

- Global Freelancers & Independent Contractors: Around 35% of international contractors now prefer digital-dollar or multi-currency payouts to avoid 3–5 day banking delays and costly wire fees.

- Cross-Border E-Commerce Merchants: SMEs use these platforms to manage multi-vendor settlements and global marketplace earnings while avoiding double currency conversions that can reduce invoice values by up to 6%.

- Expatriates & Digital Nomads: Users rely on multi-currency accounts to manage international expenses, taxes, and family remittances while avoiding traditional remittance fees averaging 6.2%–6.5%.

C. How They Differ From Traditional Banking Apps

Traditional banking apps are structurally tethered to a single domestic currency and localized regulatory framework. When a traditional account interacts with international capital, it treats the transaction as an outlier, routing it through an opaque web of high-fee intermediary institutions.

The structural and architectural divergence across these two environments is distinct:

| Operational Feature | Traditional Banking Applications (Legacy Brick-and-Mortar) | Modern Multi-Currency Platforms (Digital-First / AI-Native) | Direct Financial & User Impact |

| Foreign Exchange (FX) Fees | Opaque retail markups running between 3.0% and 6.0% above spot price. | Transparent, mid-market exchange rates with tight 0.2% – 0.5% spreads. | Saves up to $50 to $55 on fee leakage for every $1,000 converted or spent. |

| Cross-Border Speed | 1 to 5 Business Days via SWIFT batch-processing networks. | Under 10 Minutes or instant via multi-rail instant payment network integrations. | Eliminates inflight capital bottlenecks across weekends and banking holidays. |

| Account Ownership | Requires local physical residency, domestic tax IDs, and utility bills per country. | Instant virtual account provisioning for 10+ global currencies from one dashboard. | Unlocks immediate global market access with zero international corporate setup friction. |

| Data Synchronization | Static, delayed end-of-day statements requiring manual spreadsheet balancing. | Rich data structures enabled by ISO 20022 and continuous real-time webhooks. | Delivers immediate, straight-through processing (STP) and slashes manual data entry by 25%. |

| Operating Availability | Mon-Fri, 9-to-5 banking hours; restricted by regional holiday calendar blocks. | 24/7/365 Continuous automated ledger processing. | Enables autonomous, real-time payouts exactly when international vendors require fulfillment. |

The Structural Reality: Multi-currency banking has evolved from a travel convenience into essential financial infrastructure. With 93% of leading financial institutions modernizing their payment systems for multi-rail, tokenized, and real-time transactions, relying on a single-currency account creates a lasting cost and speed disadvantage. Multi-currency apps give individuals and businesses access to treasury strategies once reserved for multinational enterprises.

How Multi-Currency Banking Apps Protect Users Against Inflation

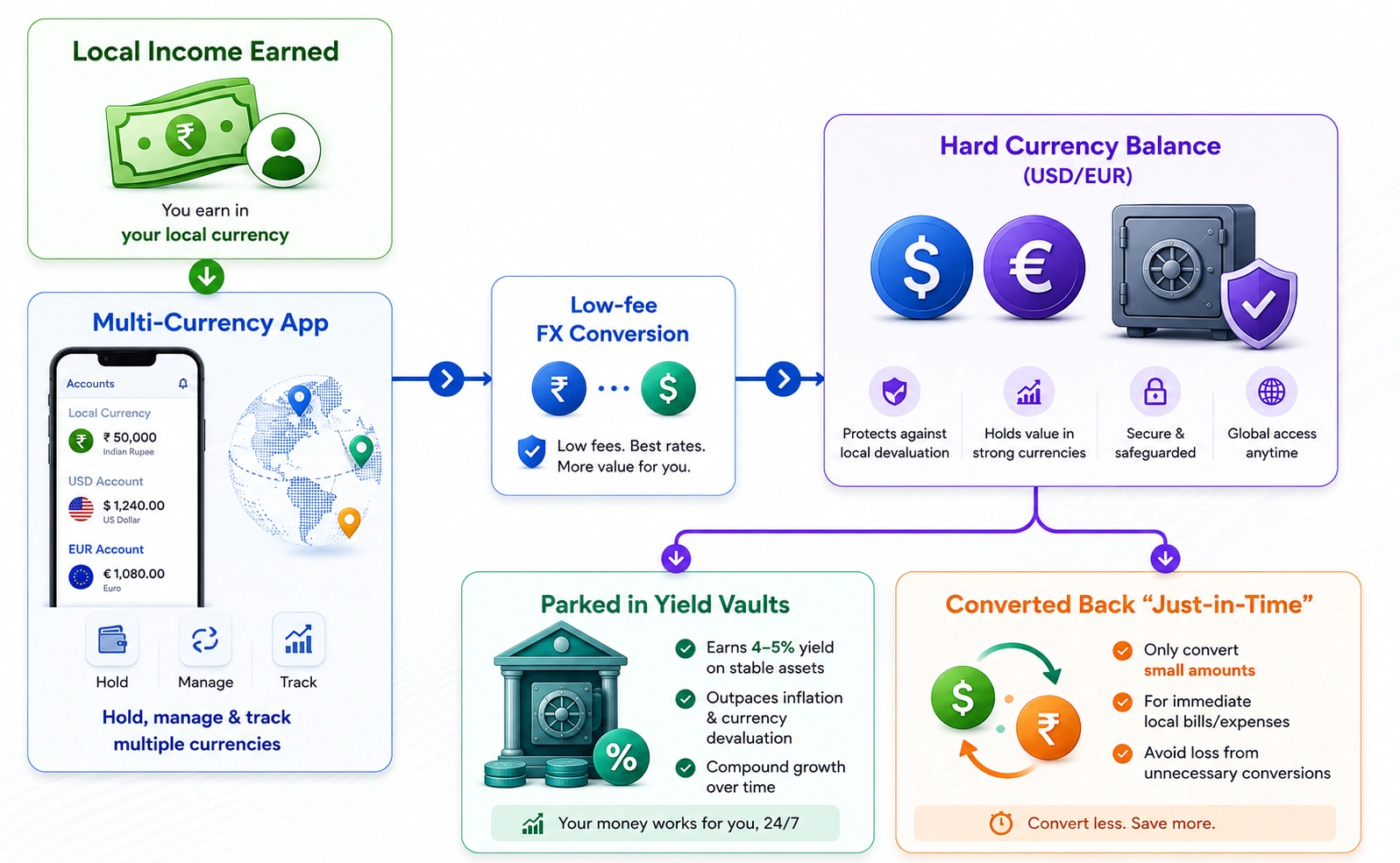

When a local currency faces heavy inflation, holding cash in a traditional bank account can feel like watching your purchasing power evaporate in real time. Multi-currency banking apps (like Wise, Revolut, or specialized digital wallets) act as a financial shield by allowing regular consumers and businesses to bypass geographic limitations and access global financial safe havens.

Instead of keeping all their funds tied to a devaluing home currency, users can employ several built-in mechanisms to outmaneuver domestic inflation.

1. Currency Hedging via Stable Foreign Assets

The most direct way these apps protect users is through instant currency diversification. If a country is experiencing 20% annual domestic inflation while a major global currency like the US Dollar (USD) or the Euro (EUR) is stable at 2–3%, keeping money in the local currency means losing massive purchasing power.

Multi-currency apps allow users to instantly exchange local funds into “hard currencies” that traditionally serve as global safe havens. Users can keep their wealth parked in USD, EUR, or Swiss Francs (CHF), insulating it from domestic monetary devaluation.

2. Exploiting Mid-Market Rates and Low Fees

In a hyper-inflationary environment, traditional banks often capitalize on customer panic by widening their foreign exchange (FX) spreads, sometimes charging a hidden 2% to 5% markup to convert local cash into foreign currency.

Modern multi-currency fintechs use the real-time mid-market exchange rate (the exact midpoint between global buy and sell volumes) and charge a transparent, minimal fee (typically 0.3% to 1%). By cutting out predatory retail banking margins, users retain significantly more of their baseline capital during the conversion process.

3. High-Yield “Vaults” and Interest-Bearing Balances

Inflation requires money to actively grow just to maintain its baseline value. Many multi-currency apps offer tokenized or integrated savings products attached to their foreign currency balances:

- Government Bond Access: Some apps allow users to sweep their USD or EUR balances directly into short-term Western government Treasury bills or money market funds.

- High-Yield Multi-Currency Interest: Users can earn competitive yields (often 4% to 5% annually on USD balances) that match or exceed the stable currency’s native inflation rate, ensuring that the parked global assets continue to outpace rising costs.

4. Seamless International “Local” Accounts

True multi-currency apps do not just hold a digital representation of a currency; they provide users with virtual, localized banking details (like a US Routing/Account number or an EU IBAN) regardless of where the user physically lives.

This enables freelancers, remote workers, and cross-border businesses to protect themselves against local inflation at the source:

- They can invoice and receive payments directly in stable foreign currencies.

- They can keep those earnings entirely offshore in a stable currency ledger, only converting micro-amounts back into the devaluing local currency as needed for immediate, everyday living expenses.

5. Automated Exchange Guardrails

To prevent users from having to constantly monitor fluctuating FX charts during volatile hyper-inflationary cycles, these platforms leverage automation:

- Limit Orders: Users can set target exchange rates. If the local currency spikes slightly or a hard currency drops, the app automatically triggers a pre-set conversion, optimizing the entry point.

- Auto-Shielding rules: Businesses can configure the app to automatically convert a set percentage of daily local sales revenue into a hard currency the moment it hits the account, minimizing exposure to rapid currency drops.

How Different Users Protect Against Inflation

Managing inflation requires different financial strategies depending on how you earn, spend, save, or invest. The table below highlights common inflation-related challenges faced by different user groups and shows how a multi-currency banking app helps protect purchasing power through practical features.

| User Segment | Financial Challenge During Inflation | How the App Helps | Key Platform Features Used |

| Freelancers | Local currency depreciation reduces the value of overseas earnings. | Receive payments in stable currencies, hold balances, and convert at favorable FX rates. | Multi-currency wallets, local receiving accounts, real-time FX conversion, rate alerts |

| Remote Workers | International salaries lose purchasing power after immediate conversion. | Hold income in stronger currencies and convert strategically. | Global currency balances, live exchange rates, smart FX conversion |

| International Travelers | Currency exchange fees and poor FX rates increase travel costs. | Pre-convert funds, spend from local balances, and avoid FX markups. | Multi-currency debit cards, auto FX routing, global wallets |

| Families Sending Remittances | Transfer fees and poor exchange rates reduce the amount received. | Send money with lower FX costs, transparent pricing, and faster settlements. | Cross-border payments, competitive FX rates, international transfers |

| Global Investors | Holding cash in a single currency increases inflation and FX risk. | Diversify holdings across multiple currencies and rebalance as markets change. | Multi-currency accounts, currency management tools, exchange rate monitoring |

Core Features of Multi-Currency Banking Apps Against Inflation

A multi-currency banking app delivers the greatest value through features that help users hold, move, convert, and spend money efficiently across borders. These capabilities reduce foreign exchange costs, improve financial flexibility, and help users protect purchasing power during periods of inflation and currency volatility.

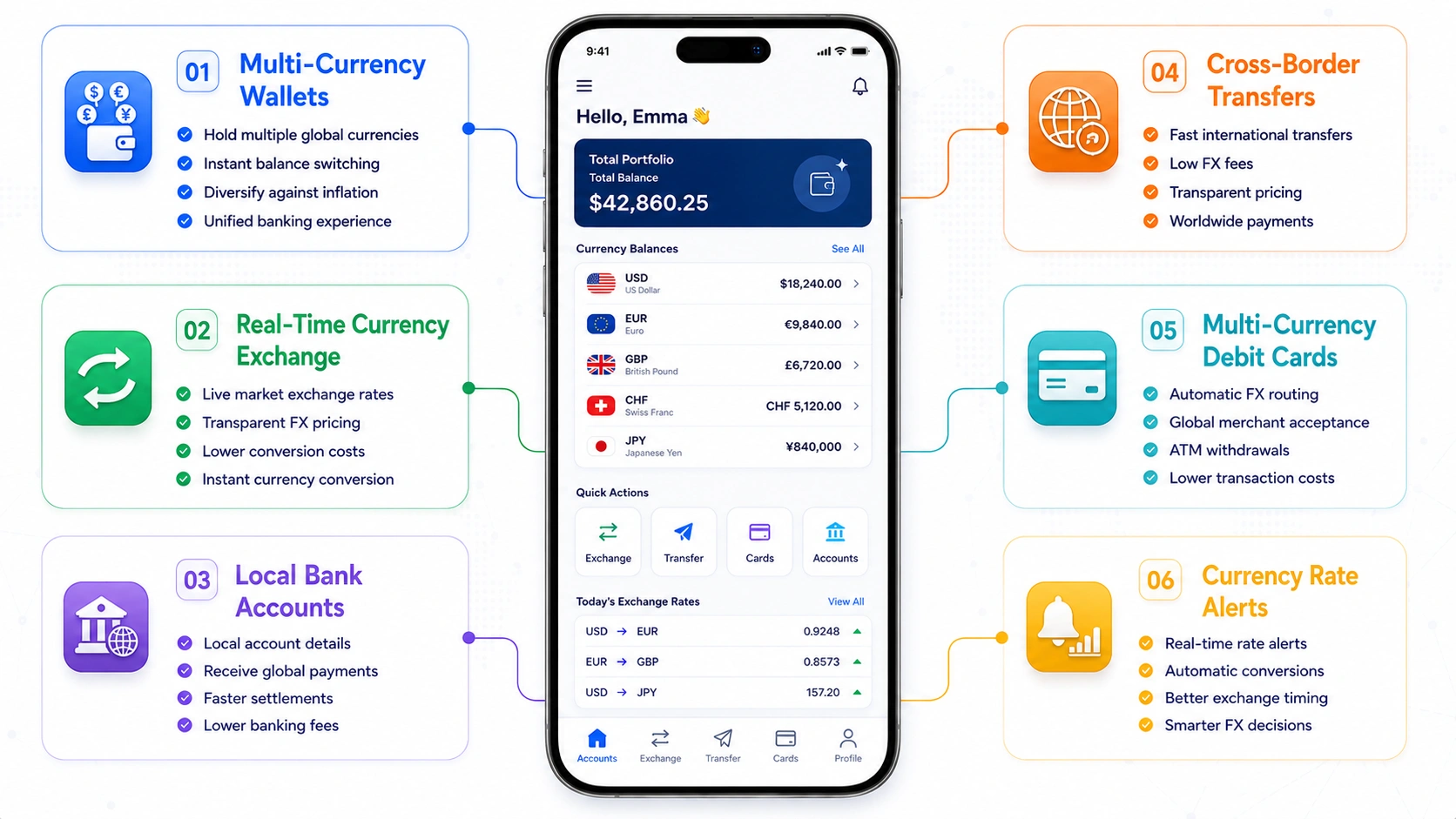

1. Multi-Currency Wallets for Holding Global Balances

Multi-currency wallets allow users to store and manage multiple currencies within a single account without opening separate bank accounts. This feature enables instant balance switching, simplifies global money management, and helps users diversify funds across stronger currencies to reduce inflation and exchange rate risks.

2. Real-Time Currency Exchange at Competitive Rates

Real-time currency exchange enables users to convert funds instantly using competitive market rates with transparent fees. Including this feature helps users avoid excessive foreign exchange costs, optimize conversion timing, and preserve more value when dealing with fluctuating currencies and international transactions.

3. Local Bank Accounts in Multiple Countries

Providing local bank account details in major currencies allows users to receive salaries, client payments, and business transfers as local residents. This feature reduces international banking charges, accelerates settlements, improves payment convenience, and strengthens the platform’s cross-border banking capabilities.

4. Cross-Border Transfers With Low FX Fees

Low-cost cross-border transfers enable users to send money internationally with faster settlements and transparent pricing. This feature minimizes transfer expenses, supports personal and business payments, simplifies global remittances, and offers a more efficient alternative to traditional international banking services.

5. Multi-Currency Debit Cards With Auto FX Routing

Multi-currency debit cards automatically use the matching currency balance during purchases, reducing unnecessary foreign exchange conversions. This feature improves global spending, lowers transaction costs, supports worldwide merchant acceptance and ATM withdrawals, and delivers a seamless international payment experience.

6. Currency Conversion Controls and Rate Alerts

Currency conversion controls and exchange rate alerts help users decide when to convert funds based on favorable market conditions. By offering manual and automated conversion options, this feature enables smarter foreign exchange decisions and helps users maximize purchasing power during currency fluctuations.

How Much Does It Cost to Build a Multi-Currency Banking App?

The multi-currency banking app development cost depends on its feature set, regulatory requirements, banking integrations, security standards, and supported markets. The estimates below break down the development cost by project phase, platform complexity, and the major factors that influence the overall investment.

A. Development Cost by Project Phase

The table below outlines each multi-currency banking app development phase involved in building a multi-currency banking app, highlighting key activities covered and estimated cost ranges aligned with MVP to Enterprise-level development.

| Development Phase | Estimated Cost Range (MVP → Enterprise) | What the Phase Covers |

| Define the Target User and Supported Markets | $8,000 – $25,000 | Research target users, supported countries, currencies, business model, compliance requirements, and create a detailed product roadmap. |

| Design the Banking and Currency Architecture | $12,000 – $40,000 | Design system architecture, multi-currency wallets, transaction workflows, database structure, APIs, and intuitive user experience across platforms. |

| Develop Core Banking Features | $40,000 – $150,000 | Build wallets, currency exchange, transfers, local accounts, transaction history, budgeting, notifications, and account management capabilities. |

| Integrate Banking, FX, and Payment Partners | $20,000 – $100,000 | Connect Banking-as-a-Service providers, FX APIs, payment gateways, card issuing, remittance networks, and local banking services. |

| Build Security, Compliance, and KYC Modules | $20,000 – $120,000 | Implement KYC, AML, fraud detection, encryption, authentication, audit logs, regulatory compliance, and risk monitoring systems. |

| Test, Deploy, and Launch the Platform | $10,000 – $65,000 | Perform quality assurance, security testing, cloud deployment, app publishing, production monitoring, and post-launch stabilization activities. |

| Total Estimated Cost | $100,000 – $700,000+ | Combined estimated investment across all development phases required to build a functional multi-currency banking application platform. |

Note: These estimated multi-currency banking app development cost provide a general guideline; actual costs may vary based on project scope, technology choices, regulatory requirements, and development team expertise, ensuring flexibility in budgeting and strategic planning decisions.

B. Development Cost by Platform Complexity

The following table compares multi-currency banking app development costs based on platform complexity, outlining key capabilities and estimated investment ranges to help businesses choose the right solution aligned with their goals and budget.

| Platform Complexity | Estimated Cost Range | Key Capabilities |

| MVP Platform | $100,000 – $180,000 | Multi-currency wallets, currency exchange, basic transfers, local accounts, KYC, and essential security features. |

| Mid-Level Platform | $180,000 – $350,000 | Advanced FX management, debit cards, budgeting, rate alerts, remittances, enhanced compliance, and analytics. |

| Enterprise Platform | $350,000 – $700,000+ | Global banking integrations, AI-powered insights, enterprise security, large-scale infrastructure, advanced compliance, and business banking capabilities. |

Note: Choosing the right platform complexity depends on business goals, target audience, and scalability needs, ensuring optimal balance between development cost, feature richness, regulatory compliance, and long-term growth potential. Typically, businesses begin with an MVP multi-currency banking app development to validate their idea and gradually scale to an enterprise-level platform through a well-defined development roadmap.

C. Factors That Influence Development Cost

Several technical, regulatory, and business decisions determine the final multi-currency banking app development cost of a multi-currency banking app. The more advanced the platform’s capabilities and global coverage, the higher the investment required for development, compliance, and long-term scalability.

- Supported Currencies & Countries: Expanding into additional markets adds $10,000–$30,000 for banking integrations, localization, regulatory compliance, and regional testing.

- Banking-as-a-Service (BaaS) Integrations: Integrating BaaS providers for account creation, card issuing, payments, and financial services adds $15,000–$40,000, depending on the number and complexity of integrations.

- Foreign Exchange (FX) Infrastructure: Building a live FX engine with real-time exchange rates, liquidity providers, competitive pricing, and automated currency conversion adds $10,000–$25,000.

- Security & Regulatory Compliance: Implementing KYC, AML, fraud detection, encryption, MFA, audit trails, and regulatory reporting increases costs by $20,000–$50,000.

- Core Feature Complexity: Features like multi-currency wallets, local receiving accounts, debit cards, budgeting, AI insights, and transaction management add $25,000–$70,000, depending on functionality.

- Scalability & Cloud Infrastructure: Supporting global users, high transaction volumes, and real-time financial operations requires $15,000–$35,000 for scalable cloud architecture and continuous monitoring.

Technologies Behind Inflation-Ready Banking Apps

The multi-currency banking app development requires a combination of banking infrastructure, payment technologies, compliance systems, and intelligent financial tools. The technologies below enable secure cross-border banking, real-time currency management, and regulatory compliance while helping users better protect their purchasing power.

| Technology Layer | Purpose in the Platform | Key Technologies & Solutions |

| Real-Time Foreign Exchange APIs | Deliver live exchange rates, instant FX conversion, rate monitoring, and transparent pricing across supported currencies. | Open Exchange Rates, Currencylayer, XE, OANDA, Wise Platform APIs |

| Global Payment Rails & Banking Integrations | Enable cross-border payments, local account creation, card issuing, and seamless banking connectivity. | Banking-as-a-Service (BaaS), SWIFT, SEPA, ACH, Faster Payments, Visa Direct, Mastercard Send |

| AI-Powered Financial Intelligence | Analyze spending behavior, generate budgeting insights, and recommend optimal currency conversions. | Machine Learning, Predictive Analytics, Transaction Categorization, Personal Finance AI Models |

| Security, Fraud Detection & Identity Protection | Protect accounts, transactions, and financial data while detecting fraud in real time. | Biometric Authentication, Multi-Factor Authentication (MFA), End-to-End Encryption, AI Fraud Detection, Tokenization |

| Compliance & Regulatory Infrastructure | Support KYC, AML, identity verification, regulatory compliance, and transaction monitoring. | KYC, AML, GDPR, PCI DSS, OFAC Screening, Sanctions Monitoring, Transaction Monitoring |

| Cloud Infrastructure & Scalability | Deliver real-time processing, high availability, and scalable infrastructure for global financial operations. | AWS, Microsoft Azure, Google Cloud Platform (GCP), Kubernetes, Docker, Redis, PostgreSQL |

Top 5 Multi-Currency Banking Apps for Inflation Protection

As inflation and currency fluctuations continue to affect purchasing power, choosing the right multi-currency banking app can help you manage international finances more efficiently. These are five leading platforms offering currency diversification, competitive exchange rates, and global payment solutions.

1. Wise

Wise is best for freelancers, remote workers, and global travelers seeking transparent international banking. It supports 40+ currencies, local receiving accounts, mid-market exchange rates, and rate alerts, allowing users to hold stronger currencies and convert strategically, reducing purchasing power loss during inflation and currency depreciation.

2. Revolut

Revolut is ideal for frequent travelers, digital nomads, and everyday users. Its multi-currency wallets, competitive foreign exchange rates, international debit card, and budgeting tools help users avoid excessive FX fees, maintain balances in stronger currencies, and minimize the impact of inflation on global spending.

3. Payoneer

Payoneer is designed for freelancers, e-commerce sellers, and international businesses. Users can receive payments through local receiving accounts, hold multiple currency balances, and convert funds when exchange rates are favorable, helping preserve overseas earnings against inflation and volatile currency movements.

4. N26

N26 is best for European residents, travelers, and remote workers. The app offers seamless international payments, spending controls, budgeting features, and competitive exchange rates, helping users reduce foreign transaction costs and maintain greater purchasing power during periods of rising inflation.

5. Airwallex

Airwallex is best suited for startups, global businesses, and cross-border entrepreneurs. It provides multi-currency accounts, local receiving accounts, competitive FX conversion, and international payment capabilities, enabling businesses to diversify currency holdings and reduce inflation and exchange-rate risks across global operations.

How IdeaUsher Builds Secure Global Banking Platforms

With 11+ years of experience, 250+ specialists, 1,000+ successful projects across 50+ countries, and a 4.9/5 Clutch rating, IdeaUsher builds secure, scalable fintech platforms for complex global financial ecosystems.

Rather than relying on off-the-shelf templates, we engineer custom multi-currency banking platforms with banking-grade security, scalable architecture, and seamless financial integrations, helping businesses launch enterprise-ready banking ecosystems with a lasting competitive advantage.

A. End-to-End Product Strategy and Development

Business leaders choose us because we turn complex regulatory and banking workflows into simple, automated, and highly accessible user experiences. From concept and compliance to deployment and continuous optimization, we build scalable fintech solutions that support long-term growth and evolving customer needs.

B. Expertise in Fintech, Payments, and Compliance

Our expertise in fintech, digital payments, and regulatory compliance helps businesses build secure, scalable, and compliant financial platforms while delivering seamless user experiences across global markets.

- Automated Regulatory Guardrails: We build real-time verification and screening systems directly into your user onboarding pipelines to ensure strict compliance with global AML and KYC laws.

- Instant Payment Gateway Bridging: We integrate reliable API connections with major payment networks and card networks, enabling seamless international bank transfers, virtual card creation, and fast multi-currency conversions.

- AI-Powered Fraud Monitoring: Our developers install smart anomaly-detection tools that monitor active transactions 24/7, flagging suspicious account behavior and shielding user balances before fraud can happen.

C. Scalable Architecture for Global Expansion

We design scalable, cloud-native architectures that support global growth, high transaction volumes, seamless integrations, and reliable multi-region financial operations without compromising performance, security, or compliance.

- Isolated High-Volume Cloud Containers: We run core platform infrastructure within secure, independent cloud layers, guaranteeing that high transfer volumes on one tenant will never cause lag or system crashes on another.

- Seamless Third-Party API Syncing: We engineer a smart data-bridge that securely connects your system with external core banking software and insurance portals, letting you add new financial features without breaking underlying code.

- Multi-Region Balance Sheets: Our database architecture easily handles localized currencies and regional tax parameters, maintaining accurate transactional ledgers across separate international branches instantly.

D. Why Businesses Choose IdeaUsher

Businesses choose IdeaUsher for secure, future-ready fintech solutions that prioritize data protection, platform ownership, and long-term flexibility to support sustainable growth and innovation.

- Enterprise Data Encryption: We hardcode financial systems using industry-leading AES-256 data security frameworks and multi-factor logins, ensuring sensitive customer financial records stay fully protected.

- Zero Vendor Lock-In Asset Packaging: We ensure total asset transparency by providing clean, standard-compliant source code packages that you can easily export and manage as your business expands globally.

Ready to transform global finance with a highly secure, scalable banking ecosystem? Partner with IdeaUsher’s fintech software experts to design your custom platform today.

Conclusion

Multi-currency banking apps are redefining how people manage money in an increasingly global economy. By enabling users to hold stronger currencies, access competitive exchange rates, and make seamless cross-border transactions, these platforms help reduce the impact of inflation and currency volatility. As demand for borderless financial services continues to grow, businesses have a significant opportunity to enter this space with innovative solutions. Partnering with an experienced fintech development company, IdeaUsher can help transform that multi-currency banking app development vision into a secure, scalable, and future-ready banking platform.

FAQs

A.1. Core features in multi-currency banking app development include multi-currency wallets, real-time currency exchange, local bank accounts, cross-border transfers, global debit cards, KYC verification, fraud detection, and strong security for seamless international banking.

A.2. The multi-currency banking app development costs typically range from $100,000 to $700,000+, depending on platform complexity, banking integrations, regulatory compliance, supported markets, security requirements, and the overall feature set.

A.3. Regulatory compliance in multi-currency banking app development ensures the platform operates legally across different regions while protecting users through KYC, AML, data privacy, and financial security standards that build long-term trust.

A.4. Yes. A well-designed platform can serve individuals, freelancers, remote workers, enterprises, and global businesses by offering personal banking, international payments, expense management, and business financial tools.