Mortgages are complex and long-term financial instruments built on layered contracts, payment schedules, and regulatory oversight. Yet the infrastructure managing them remains fragmented and slow to adapt. These limitations are driving interest in mortgage tokenization platform development, where loan ownership and cash flows can be represented digitally through more transparent and programmable systems.

Tokenizing mortgages requires accurately modeling that complexity on chain rather than simplifying it. Loan origination data, repayment logic, investor rights, compliance rules, and servicing events must remain aligned with legal documentation. The platform needs to support ownership transfers, reporting, and lifecycle management without disrupting financial or regulatory continuity.

In this blog, we explore mortgage tokenization platform development by breaking down core infrastructure components, architectural considerations, and practical steps involved in creating digital systems that support compliant, scalable, and reliable mortgage-backed token platforms.

What is a Mortgage Tokenization Platform?

A mortgage tokenization platform is a blockchain-based digital system that converts traditional mortgage assets into programmable digital tokens representing ownership or economic rights, enabling secure tracking, trading, and fractional investment. These platforms use smart contracts and distributed ledgers to enhance liquidity, transparency, and accessibility in mortgage markets, letting lenders, investors, and other participants manage, trade, and interact with tokenized mortgage assets more efficiently than traditional paper-based systems.

A. Mortgage Note vs Property Title: What’s Actually Tokenized?

The fundamental distinction is between debt and ownership. Mortgage tokenization focuses on the mortgage note (promissory note), the legal document recording the borrower’s obligation to repay the loan under agreed terms like interest rate, duration, and repayment schedule. The token represents economic rights to loan cash flows, not property ownership.

Why tokenize payment rights rather than the property?

- Regulatory Simplicity: Mortgage notes qualify as financial securities, placing tokenization under established securities regulations. This is more practical than attempting to digitize fragmented property titles across multiple jurisdictions.

- Operational Feasibility: Property titles are controlled by local land registries, making direct tokenization impractical. Instead, platforms keep titles with custodians and tokenize the financial claim, avoiding complex government system integrations.

- Investor Expectation: Most investors seek yield from debt payments, not the responsibilities of fractional property ownership (maintenance, taxes, etc.).

B. Primary vs Secondary Mortgage Markets

Tokenization can be applied at two distinct stages, with different implications.

| Stage | Origination-Side Tokenization (Primary Market) | Trading-Side Tokenization (Secondary Market) |

| What is tokenized? | A newly issued mortgage loan at the point of creation. | An existing pool of mortgages (like a Mortgage-Backed Security – MBS). |

| Process | Loan funding occurs through token sales, with capital flowing directly to the borrower. | Existing mortgage assets are pooled into an SPV, and fractional ownership tokens are issued. |

| Impact on Compliance | High. Must comply with lending laws (TILA, RESPA) and securities issuance regulations simultaneously. | Focused. Primarily deals with securities regulations, as the underlying loans already exist. |

| Impact on Liquidity & Access | Potentially Transformative. Creates a direct, global capital market for new loans, bypassing traditional securitization pipelines. | Incremental Improvement. Enhances the tradability and transparency of existing MBS markets, attracting new investors with smaller capital requirements. |

C. Mortgage Lifecycle Events: The Smart Contract Crucible

This is where the promise of automation meets real-world complexity. A robust platform’s smart contracts must be programmed to handle these core events:

1. Origination: The contract is deployed with immutable loan terms (principal, rate, amortization schedule). Tokens are minted and distributed to initial investors. Funds are escrowed and released to the borrower upon closing.

2. Monthly Repayments: The contract automatically receives payments (via integration with a payment processor), distributes principal and interest to token holders based on their share, and updates the remaining balance. This is the core automation benefit.

3. Prepayment: The contract must logic to handle a full or partial early payoff. It should calculate any applicable penalty, terminate the relevant token balance, and distribute the final payout.

4. Default and Foreclosure: This is the most legally intensive event. The smart contract cannot physically foreclose. Instead, it must be programmed to:

- Flag a loan as delinquent after a set period.

- Trigger notifications to a designated off-chain servicer or trustee who initiates legal proceedings.

- Upon the servicer’s instruction (via a verified oracle), distribute any recovered proceeds from the foreclosure sale to token holders, often resulting in token redemption/burning.

5. Refinancing: When a borrower refinances, the old loan is paid off. The smart contract must treat this as a prepayment event, closing out the original tokens and potentially allowing investors to use proceeds to purchase tokens in the new refinanced loan pool.

The real innovation goes beyond placing mortgages on a blockchain. It lies in encoding the mortgage’s legal and financial lifecycle into smart contracts, while seamlessly integrating with essential off-chain servicing, compliance, and enforcement processes.

How a Mortgage Tokenization Platform Works?

A mortgage tokenization platform functions as a hybrid financial system. Legal ownership, servicing, and enforcement remain off-chain, while cash-flow logic, investor rights, and transparency are handled on-chain through smart contracts.

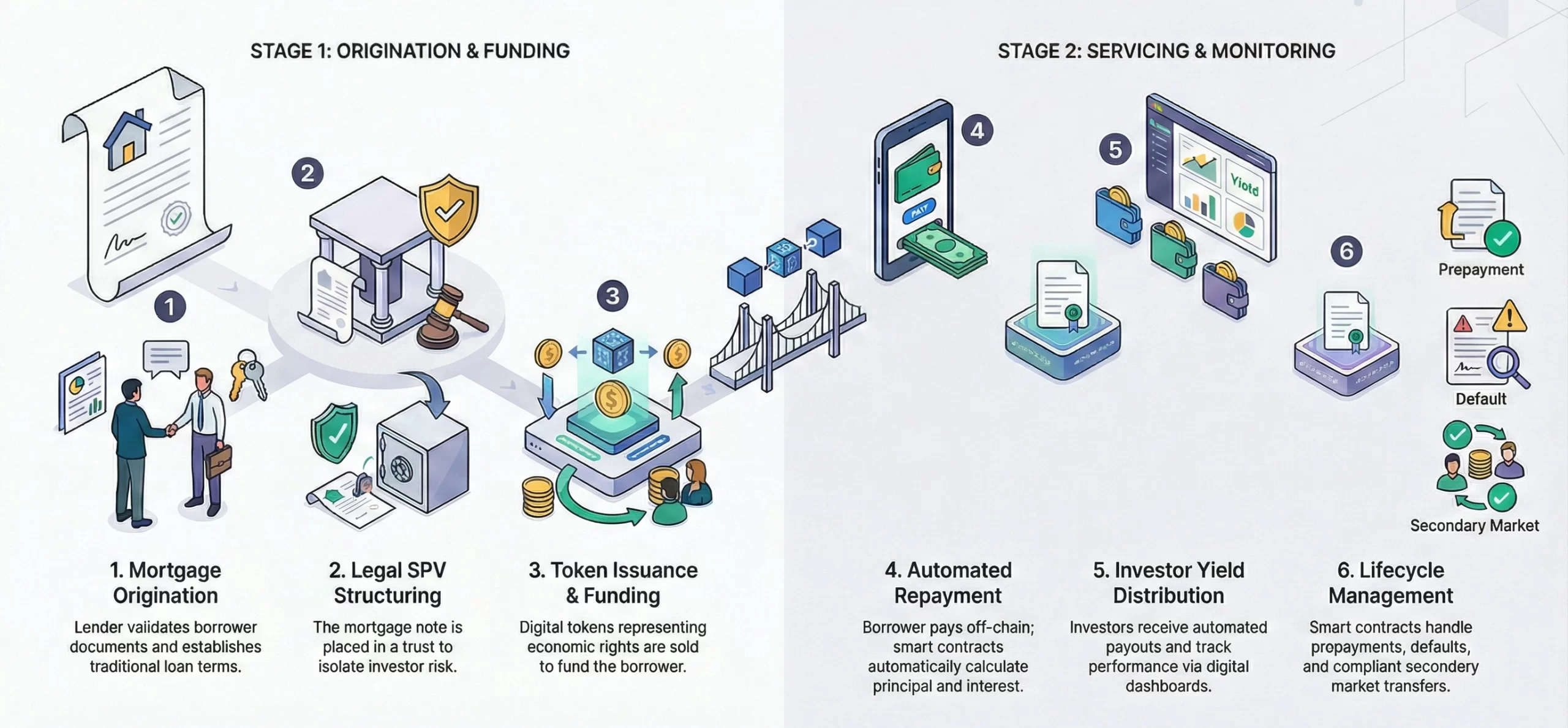

Phase 1: Mortgage Origination & Structuring

This phase establishes the legal and financial foundation of the mortgage. Loan terms, compliance requirements, and servicing responsibilities are finalized before tokenization begins.

A. Borrower: The borrower applies for a mortgage through a lender or platform partner. Loan underwriting, credit checks, and documentation follow traditional lending processes.

B. Lender / Originator: Once approved, the lender structures the mortgage note and defines loan terms including interest rate, tenure, repayment schedule, and servicing arrangements.

C. Platform: The platform prepares the mortgage for tokenization by validating documentation, structuring compliance logic, and defining how cash flows will be represented on-chain.

Phase 2: Tokenization & Funding

The mortgage is legally structured and converted into investable tokens. Investor capital is raised at origination and disbursed as loan funding.

A. Legal Structuring: The mortgage note is placed into a legal SPV or trust. This entity holds the financial asset and isolates investor risk.

B. Token Issuance: Tokens are issued to represent fractional economic rights to the mortgage’s principal and interest cash flows. No property ownership is transferred.

C. Investor Participation: Investors purchase tokens during origination. Capital raised through token sales is disbursed to the borrower as loan funding.

Phase 3: Active Loan Servicing & Cash-Flow Automation

During this phase, borrower repayments are collected off-chain while smart contracts automate amortization, accounting, and investor yield distribution on-chain.

A. Borrower: The borrower makes monthly EMI payments using standard banking channels, exactly as in a traditional mortgage.

B. Servicer: A licensed mortgage servicer collects repayments, manages borrower communication, and handles delinquencies or exceptions.

C. Platform & Smart Contracts: Repayment data flows from servicing systems to the blockchain, and smart contracts process, verify, and execute repayment logic accordingly.

- Apply amortization logic to calculate scheduled repayments and adjust loan terms over time

- Split each repayment into principal and interest components with accuracy

- Update outstanding loan balances after every repayment event

- Distribute yield automatically to investors based on tokenized ownership and entitlement

Phase 4: Ongoing Monitoring & Risk Handling

The platform manages performance tracking, compliant secondary transfers, and exception events such as prepayments or defaults across the mortgage lifecycle.

A. Investors: Investors receive periodic payouts and monitor performance through dashboards showing yield earned, repayment status, and remaining principal.

B. Secondary Transfers: If permitted, investors can transfer tokens through allowlisted, compliant mechanisms. Transfers are restricted by jurisdiction and investor eligibility rules.

C. Prepayment or Default Events: Prepayment or default events trigger off-chain legal and servicing actions, while the platform records outcomes on-chain without executing foreclosure or asset sales.

- Prepayment: Smart contracts recalculate balances and settle investor positions

- Default: Loan state changes on-chain while legal recovery proceeds off-chain

Why Mortgage Tokenization Platform Gaining Popularity?

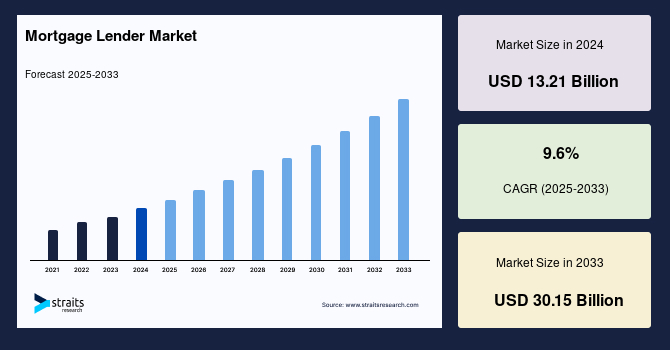

The global mortgage lender market, valued at USD 13.21 billion in 2024, is projected to grow from USD 14.48 billion in 2025 to USD 30.15 billion by 2033, with a CAGR of 9.6% (2025-2033). This growth boosts investment in digital infrastructure, automation, and tokenized lending.

Tokenization is emerging as a defining layer of this digital shift, with the global tokenized RWA market projected to reach $3.2 trillion by 2030 and potentially $4 trillion by 2035, up from under $300 billion in 2024. The RWA market grew 308% in three years, while tokenized equities expanded nearly 2,900% in one year.

Operational efficiency drives adoption. Tokenized mortgage infrastructure can save lenders approximately $850 per $100,000 mortgage by reducing origination, reconciliation, and servicing costs. Loan-level MBS reporting shrinks from 55 days to under 30 minutes, enabling near-real-time transparency for issuers, servicers, and investors.

Investor demand and institutional participation validate the shift. Around 80% of high-net-worth investors and 67% of institutional investors plan to allocate capital to tokenized assets, with entry thresholds falling to $50. As of mid-2024, 12% of global real estate firms implemented tokenization and 46% were piloting, while Pineapple Financial tokenized CAD 716 million across 1,250+ mortgages.

Why Liquidity Is Important in Mortgage Tokenization Platforms?

Liquidity plays a foundational role in mortgage tokenization because mortgages are long-term, cash-flow–based financial instruments. Unlike traditional assets that naturally trade frequently, mortgage investments require carefully designed liquidity to balance investor flexibility with regulatory and servicing stability.

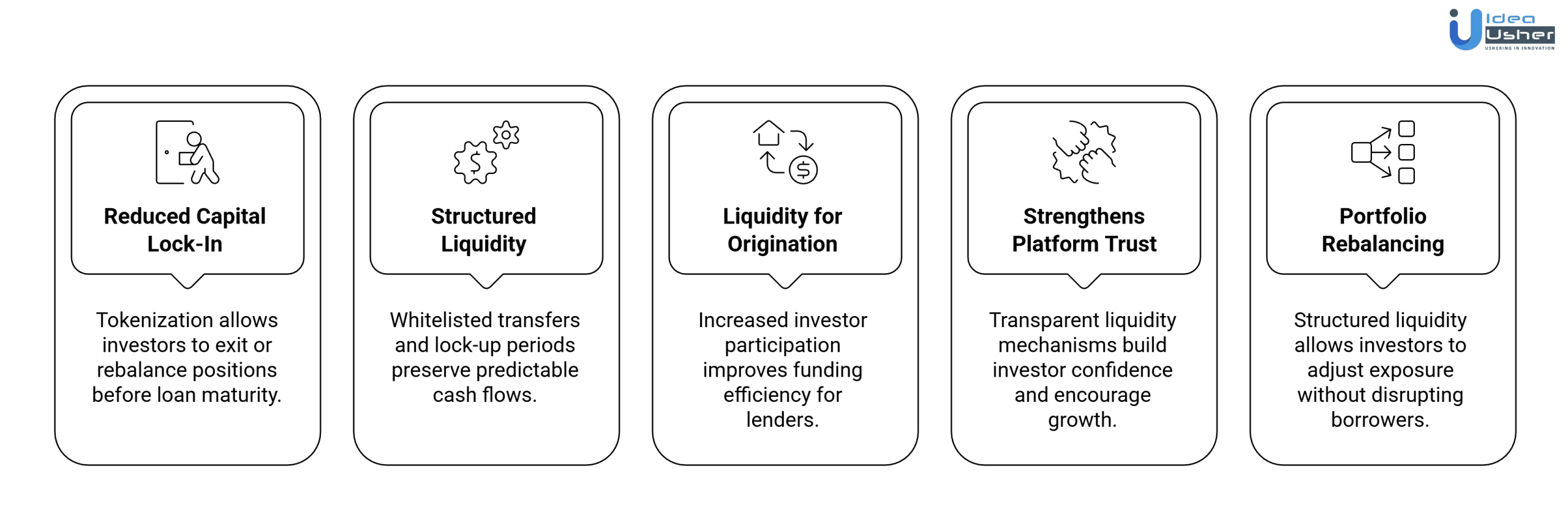

1. Reduced Capital Lock-In for Investors

Traditional mortgage investments lock capital for decades, limiting participation. Tokenization enables investors to exit or rebalance positions before loan maturity through structured transfers, making mortgage-backed investments more accessible without changing borrower obligations.

2. Structured Liquidity & Investor Participation

Mortgage liquidity must be controlled rather than speculative. Allowlisted transfers, lock-up periods, and eligibility checks allow investor exits while preserving predictable cash flows, servicing integrity, and compliance with securities and lending regulations.

3. Liquidity for Mortgage Origination

When investors know capital can be reallocated later, participation at origination increases. This improves funding efficiency for lenders, reduces balance-sheet pressure, and enables faster deployment of capital into new mortgage loans.

4. Strengthens Platform Trust and Market Confidence

Transparent, rule-based liquidity mechanisms give investors confidence in both entry and exit scenarios. This trust encourages long-term platform usage, repeat investment, and sustainable growth of tokenized mortgage ecosystems.

5. Portfolio Rebalancing Liquidity

Structured liquidity allows investors to adjust exposure by transferring tokens instead of triggering loan prepayments, refinancing, or asset sales. This protects borrowers from disruption while giving investors flexibility at the portfolio level.

Key Features of Mortgage Tokenization Platform

A mortgage tokenization platform relies on core features that enable secure digitization, transparency, and efficient asset management. These capabilities support compliant operations and scalable growth. The following section showcases essential features shaping modern mortgage tokenization platforms.

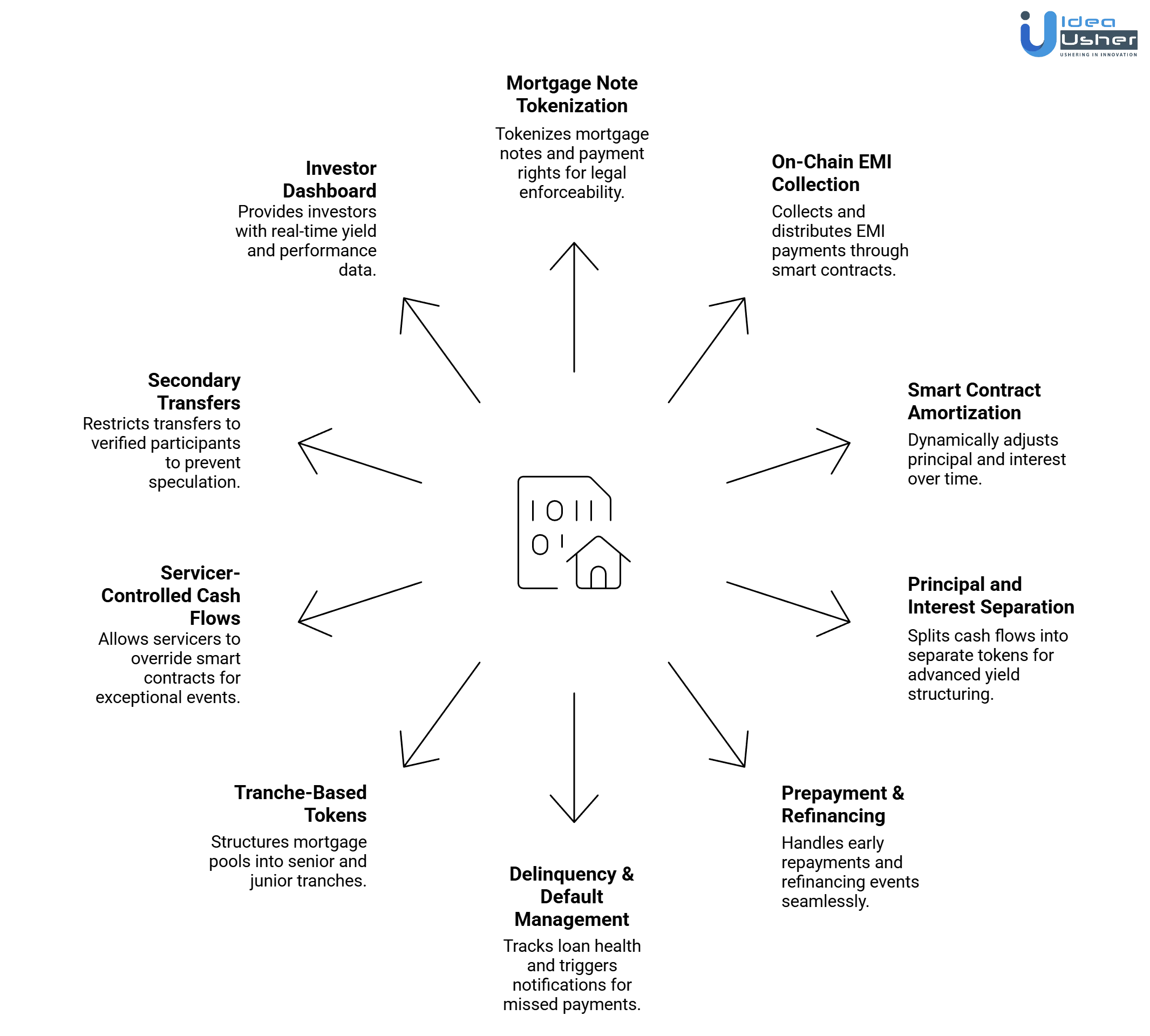

1. Mortgage Note–Level Tokenization

The platform tokenizes the mortgage note and payment rights, not the physical property. This ensures legal enforceability, aligns with lending regulations, and allows investors to earn yield from borrower repayments without holding or transferring real estate ownership.

2. On-Chain EMI Collection & Cash Flow

Monthly EMI payments are collected through integrated fiat rails and programmatically mapped to on-chain logic. Smart contracts automatically distribute principal and interest to token holders, reducing servicing friction, manual reconciliation, and payout delays for investors.

3. Smart Contract Amortization

Each mortgage token embeds its amortization schedule directly into smart contracts. The system dynamically adjusts outstanding principal, interest allocation, and investor returns over time, ensuring transparent, predictable cash flows aligned with real-world mortgage repayment structures.

4. Principal and Interest Token Separation

The platform supports splitting mortgage cash flows into separate principal and interest tokens. This enables advanced yield structuring, differentiated risk exposure, and institutional strategies similar to mortgage-backed securities, without compromising transparency or repayment accuracy.

5. Prepayment & Refinancing Logic

Smart contracts include logic to handle early repayments, refinancing events, and loan closures. When prepayment occurs, the remaining principal is recalculated, tokens are settled accordingly, and investors receive accurate payouts without disrupting platform-wide accounting or compliance.

6. Delinquency & Default Management

Missed payments automatically trigger delinquency states, grace periods, and risk notifications. The platform tracks loan health in real time, enabling investors and servicers to monitor exposure while preserving clear, auditable state transitions before legal recovery actions begin.

7. Tranche-Based Mortgage Tokens

Mortgage pools can be structured into senior and junior tranches, allowing differentiated risk and return profiles. This feature attracts institutional capital by mirroring traditional structured finance models while maintaining on-chain transparency and automated cash-flow prioritization.

8. Servicer-Controlled Cash Flows

Authorized mortgage servicers retain controlled override permissions for exceptional events such as disputes or legal actions. This balances automation with regulatory reality, ensuring smart contracts reflect operational decisions without compromising investor trust or on-chain auditability.

9. Secondary Transfers for Mortgage Tokens

Secondary transfers are restricted to verified, jurisdiction-compliant participants. This prevents speculative trading, enforces securities regulations, and enables structured liquidity while preserving long-term mortgage stability and protecting both issuers and investors from regulatory exposure.

10. Investor Yield & Performance Dashboard

Investors access a dashboard displaying realized yield, remaining principal, delinquency status, and payment history. Returns are calculated from actual borrower repayments, not market speculation, reinforcing trust, transparency, and long-term income predictability.

Development Process of a Mortgage Tokenization Platform

A structured mortgage tokenization platform development process ensures that the platform is secure, compliant, and scalable for real-world financial use cases. Our developers follow a systematic approach to design, build, and deploy reliable mortgage tokenization solutions.

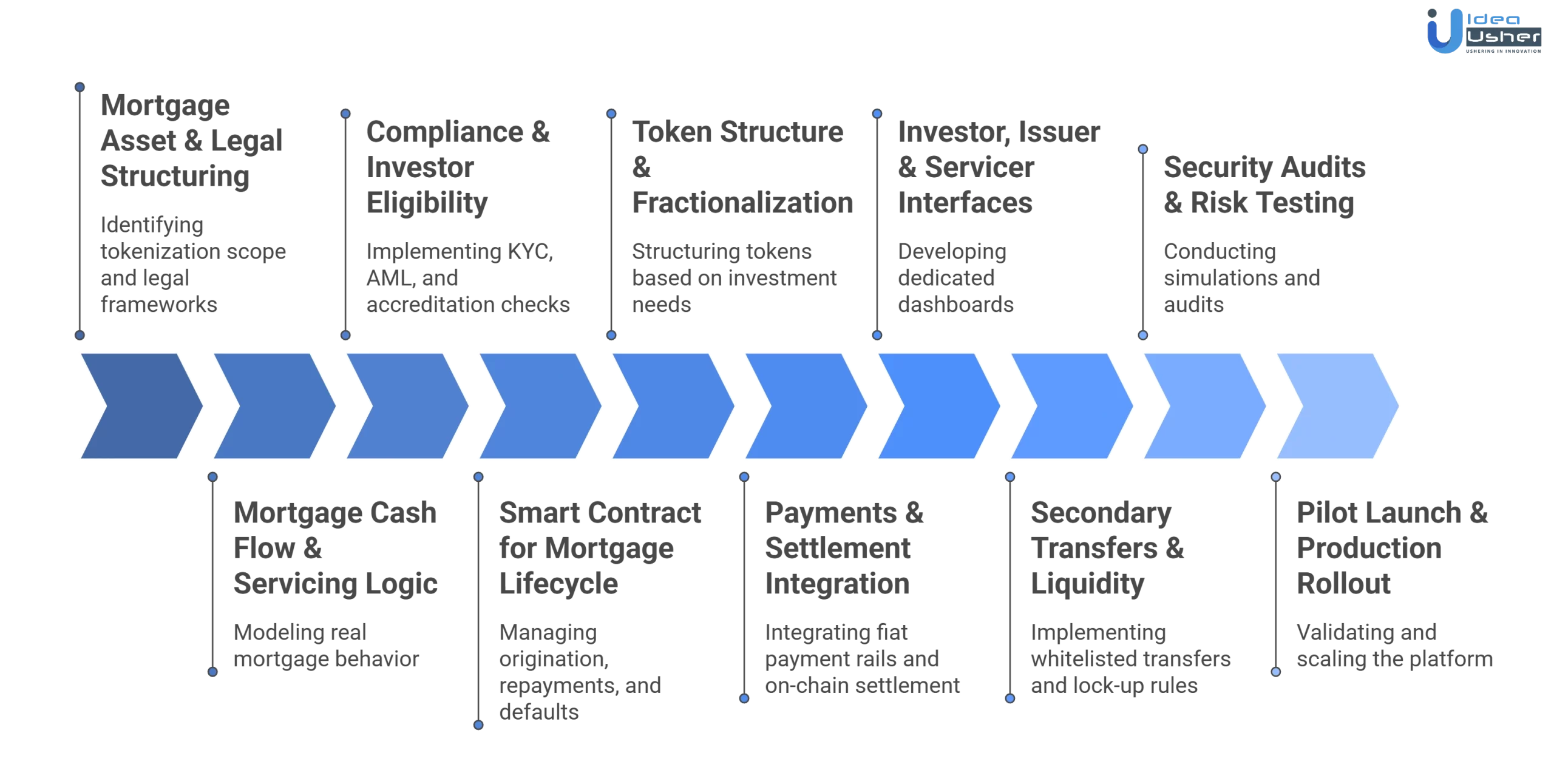

1. Mortgage Asset & Legal Structuring

We begin by identifying what will be tokenized: the mortgage note, repayment rights, or pooled receivables. Our developers work with legal frameworks to ensure enforceability, securities classification, and trustee or SPV structures are clearly defined before development starts.

2. Mortgage Cash Flow & Servicing Logic

Our developers model real mortgage behavior, including EMI schedules, amortization logic, interest calculations, servicing fees, and prepayment scenarios. This ensures the platform mirrors actual mortgage cash flows rather than simplified token revenue assumptions.

3. Compliance & Investor Eligibility

We design compliance directly into the platform architecture. Our developers implement KYC, AML, accreditation checks, and jurisdiction-based transfer rules at the workflow and smart-contract level to ensure ongoing regulatory adherence after launch.

4. Smart Contract for Mortgage Lifecycle

Our developers build smart contracts to manage origination, repayments, principal reduction, delinquency states, defaults, and loan closure. Contracts are designed for long-term upgradeability, auditability, and operational reliability across multi-year mortgage lifecycles.

5. Token Structure & Fractionalization

We structure mortgage tokens based on investment and risk requirements, including fractional ownership, principal–interest separation, or tranche-based models. Our developers align token behavior directly with mortgage agreements and servicing obligations.

6. Payments & Settlement Integration

We integrate fiat payment rails for EMI collection and automate on-chain settlement for investor payouts. Our developers build reconciliation systems that ensure every off-chain payment is accurately reflected in on-chain cash-flow distributions.

7. Investor, Issuer & Servicer Interfaces

We develop dedicated dashboards for investors, lenders, and servicers. These interfaces provide visibility into repayment performance, outstanding principal, yield metrics, delinquency status, and operational controls focused on income transparency.

8. Secondary Transfers & Liquidity

Our developers implement allowlisted secondary transfers, lock-up rules, and jurisdiction-based restrictions. This allows compliant liquidity while preventing speculative trading and ensuring mortgage tokens remain aligned with securities and lending regulations.

9. Security Audits & Risk Testing

We conduct extensive testing, repayment simulations, and smart contract audits. Our developers validate edge cases such as prepayment spikes, defaults, and servicing disruptions to ensure platform stability throughout the mortgage lifecycle.

10. Pilot Launch & Production Rollout

We launch the platform with a controlled mortgage pool to validate servicing accuracy, payment flows, and investor reporting. Once aligned, our developers scale the system to support larger portfolios and institutional-grade usage.

Mortgage Tokenization Platform Development Cost

Mortgage tokenization platform development cost varies based on technology architecture, compliance requirements, and integration complexity. Evaluating these factors helps organizations plan investments effectively. The following overview showcases key elements influencing overall development costs.

| Cost Component | Estimated Cost Range | What We Build | Why This Cost Exists |

| Mortgage Structuring & Legal Design | $8,000 – $15,000 | Tokenization model (note-level), SPV/trustee flow, asset mapping | Mortgages require legal enforceability, debt modeling, and securities alignment |

| Cash-Flow & Amortization Logic | $10,000 – $18,000 | EMI schedules, interest calculations, pre-payment handling | Generic token platforms do not model long-term loan cash flows |

| Mortgage Smart Contracts | $18,000 – $30,000 | Repayments, principal reduction, defaults, closures | Must handle 10–30 year mortgage lifecycles reliably |

| Token & Fractionalization Design | $10,000 – $20,000 | Fractional tokens, P&I separation, tranche logic (if required) | Advanced mortgage investment structuring |

| Compliance & Investor Controls | $8,000 – $15,000 | KYC/AML flows, accreditation rules, jurisdiction checks | Mortgage tokens often qualify as securities |

| Payments & Settlement Layer | $10,000 – $18,000 | EMI collection, reconciliation, investor payouts | Core to investor trust and yield accuracy |

| Investor & Servicer Dashboards | $8,000 – $14,000 | Yield view, principal tracking, delinquency status | Investors care about cash flow, not token price |

| Transfer & Liquidity Controls | $6,000 – $12,000 | Allowlisted transfers, lockups, compliance logic | Prevents speculative trading and regulatory risk |

| Security & Risk Validation | $6,000 – $12,000 | Smart contract audits, default simulations, stress tests | Mortgage platforms manage real financial risk |

| Pilot Launch & Deployment | $5,000 – $10,000 | MVP launch, mortgage pool testing, scaling setup | Validates servicing and payment accuracy |

Total Estimated Cost: $62,000 – $125,000+

Note: Actual mortgage tokenization platform development costs vary based on jurisdiction, compliance depth, mortgage complexity, integrations, and scalability requirements.

Consult with IdeaUsher to receive a precise cost estimate tailored to your mortgage tokenization platform development.

Cost-Affecting Factors of Mortgage Tokenization Platform

Several factors influence the mortgage tokenization platform development cost, including technology scope and compliance needs. The following highlights showcase key cost considerations.

1. Local Mortgage & Securities Regulations

Mortgage tokenization must comply with local lending laws, securities regulations, and investor eligibility rules, requiring jurisdiction-aware logic, documentation workflows, and transfer restrictions across the platform.

Estimated Cost Impact: $6,000–$12,000

Why This Adds Cost: Every jurisdiction introduces unique regulatory constraints that must be hardcoded and tested to avoid post-launch legal exposure.

2. Mortgage Servicing Integration Complexity

Integrating with real-world mortgage servicers requires handling payment files, reconciliation delays, reversals, and exception handling rather than simple API-based payment confirmations.

Estimated Cost Impact: $8,000–$15,000

Why This Adds Cost: Servicing systems are legacy-heavy and inconsistent, demanding custom adapters and extensive testing to ensure cash-flow accuracy.

3. Amortization Accuracy Over Long Loan Durations

Mortgage smart contracts must calculate interest, principal reduction, and balances accurately across multi-year timelines, including rate variations, prepayments, and partial settlements.

Estimated Cost Impact: $7,000–$14,000

Why This Adds Cost: Even minor calculation errors compound over time, requiring extensive modeling, simulations, and audit reviews before deployment.

4. Default, Recovery, and Legal Event Handling

The platform must track delinquency states, legal escalation milestones, and recovery outcomes without executing on-chain asset sales or violating borrower protections.

Estimated Cost Impact: $6,000–$11,000

Why This Adds Cost: These workflows involve conditional logic tied to off-chain legal actions, increasing implementation and validation complexity.

5. Investor Structuring and Risk Layer Customization

Supporting tranche-based structures, principal–interest separation, or pooled mortgages requires custom token logic aligned with institutional investment expectations.

Estimated Cost Impact: $8,000–$16,000

Why This Adds Cost: Structured products require waterfall logic and priority-based distributions, which significantly increase smart contract design and audit scope.

Monetization Models of Mortgage Tokenization That Work in Reality

Mortgage tokenization monetization models leverage blockchain, fees, and yield structures to generate sustainable returns. This section showcases proven revenue approaches operating in real-world financial markets globally today at scale.

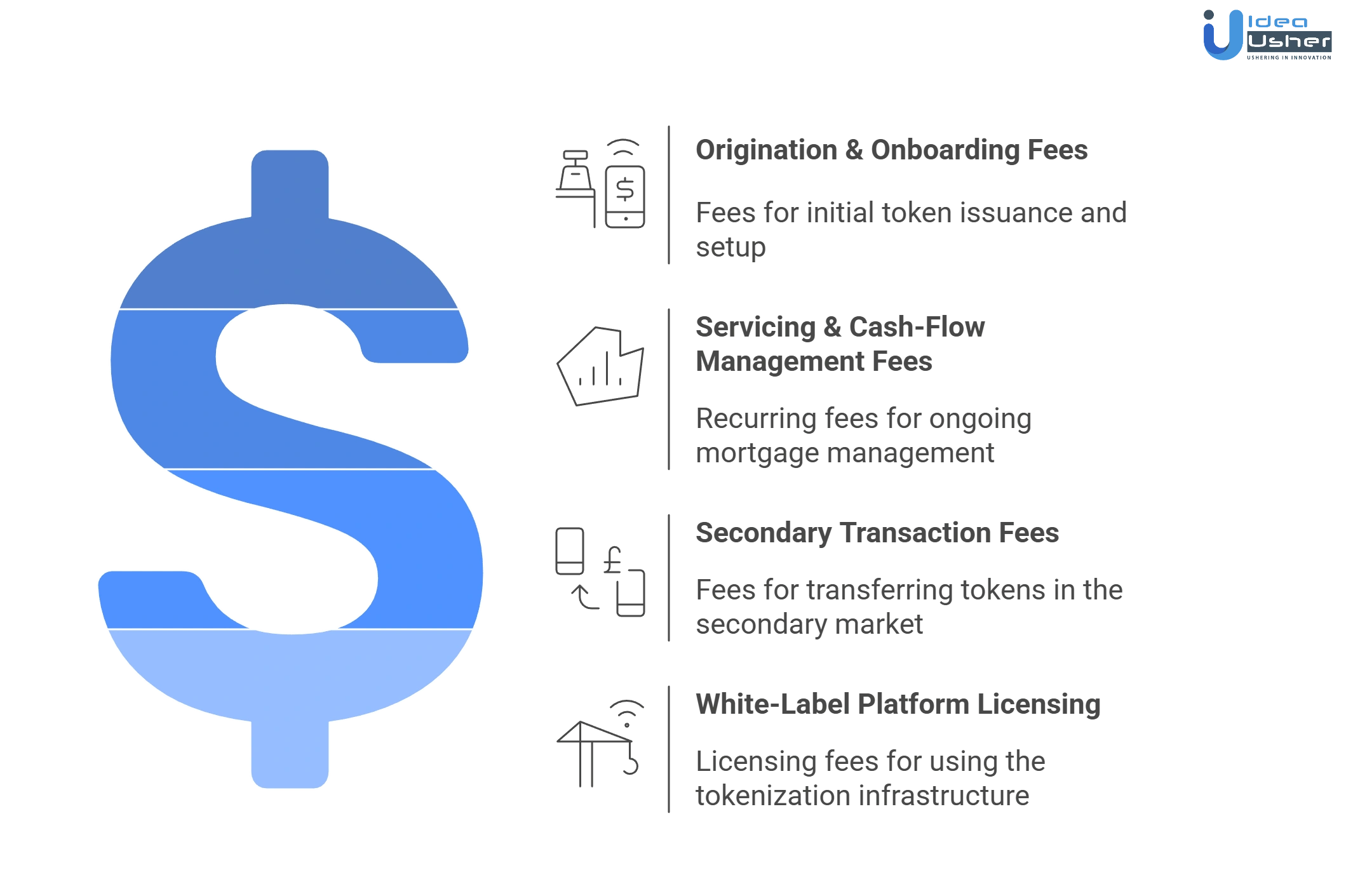

1. Mortgage Origination & Onboarding Fees

Platforms can charge origination and onboarding fees when lenders or issuers tokenize new mortgage notes or mortgage pools. These fees typically cover asset validation, structuring, compliance configuration, and initial token issuance within the platform.

2. Ongoing Servicing & Cash-Flow Management Fees

Platforms generate recurring revenue by charging servicing fees for EMI collection, repayment reconciliation, amortization updates, and periodic investor distributions. This model aligns platform revenue with long-term mortgage performance and ongoing operational usage.

3. Secondary Transaction Fees

Platforms apply transaction fees when approved and compliant secondary mechanisms transfer mortgage tokens. This approach creates incremental revenue, maintains controlled liquidity, and avoids the speculative trading behavior common in open marketplaces.

4. White-Label Platform Licensing for Lenders

Platforms can license their mortgage tokenization infrastructure to banks, NBFCs, or mortgage lenders under a white-label model. Licensing fees typically include platform access, customization, compliance updates, and ongoing technical maintenance.

Real-World Mortgage Tokenization Platforms

Real-world mortgage tokenization platforms demonstrate how blockchain technology is transforming traditional mortgage infrastructure through digitization, transparency, and automation. The following examples showcase active platforms shaping the evolution of on-chain mortgage systems.

1. ETHZilla

ETHZilla represents a blockchain-native mortgage tokenization initiative focused on converting mortgage value and repayment rights into Ethereum-based digital assets. Its uniqueness lies in leveraging smart contracts and DeFi-compatible infrastructure to explore on-chain mortgage liquidity and programmability.

2. Figure

Figure operates a mortgage-focused tokenization infrastructure through its Provenance Blockchain, digitizing home-equity and mortgage loans end-to-end. Its key differentiator is full lifecycle automation from origination to securitization, making mortgages natively blockchain-recorded financial assets.

3. Pineapple Financial

Pineapple Financial delivers institutional-grade mortgage tokenization by bringing real mortgage records from its multibillion-dollar portfolio on-chain. Its uniqueness lies in tokenizing verified mortgage data itself, enabling transparency, auditability, and future secondary market innovation.

4. Securitize

Securitize supports regulated mortgage tokenization by enabling compliant issuance of tokenized mortgage-backed instruments. Its key strength is combining blockchain infrastructure with securities law compliance, making it suitable for institutional mortgage debt tokenization and regulated secondary trading.

5. Centrifuge

Centrifuge enables on-chain mortgage financing by tokenizing mortgage cash flows and collateral into asset pools usable in decentralized finance. Its uniqueness lies in connecting mortgage assets directly to liquidity via DeFi protocols while maintaining asset-level transparency.

Conclusion

Mortgage tokenization platform development represents a structural shift in how the industry creates, manages, and distributes mortgage assets through digital infrastructure. It brings together blockchain, smart contracts, compliance frameworks, and secure data flows to address long-standing inefficiencies in mortgage markets. Lenders, investors, and technology providers focus on building systems that operate reliably within regulatory and operational realities rather than on experimentation. When teams design these platforms thoughtfully, they support transparency, liquidity, and scalability, maintain trust across all participants in the mortgage lifecycle, and enable sustainable, globally aligned digital financial ecosystems.

Build a Mortgage Tokenization Platform with IdeaUsher

We specialize in blockchain, tokenization, and financial technology development for regulated, asset-backed use cases. Leveraging this expertise, our experienced engineers build mortgage tokenization platforms that securely digitize mortgage assets and support real-world financial operations.

Why Work With Us?

- Mortgage & Financial Domain Understanding: We design platforms aligned with lending workflows, investor participation, and servicing requirements.

- Tokenized Asset Architecture: Our team structures tokens around verified mortgage assets with clear ownership and cash flow logic.

- Compliance-Driven Development: We integrate KYC, AML, reporting, and audit readiness into the platform architecture.

- Scalable Digital Infrastructure: We build our solutions for institutional scale, strong security, and long-term market adoption.

Explore our portfolio to see how we deliver blockchain solutions for complex financial ecosystems.

Connect with us for a free consultation and begin building a reliable mortgage tokenization platform.

FAQs

A.1. A mortgage tokenization platform requires asset digitization, smart contract automation, investor onboarding, compliance controls, and secure ledger management. These features ensure accurate ownership representation, regulatory alignment, transparent transactions, and efficient lifecycle management of tokenized mortgage assets.

A.2. Blockchain records every transaction on an immutable ledger, allowing stakeholders to verify ownership, payment flows, and asset performance in real time. This reduces manual reconciliation, improves auditability, and builds trust across lenders, investors, and regulators.

A.3. Smart contracts automate processes such as token issuance, interest distribution, repayments, and compliance checks. This reduces manual intervention, minimizes errors, and ensures consistent execution of predefined mortgage and investment terms.

A.4. The platform manages data security through encryption, permissioned blockchain access, secure APIs, and role-based controls. These measures protect sensitive borrower and investor information and ensure that only authorized participants can view or interact with asset data.